Digital India: Technology to Transform a Connected Nation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The World Wide Web: Not So World Wide After All?, 16 Pub

Public Interest Law Reporter Volume 16 Article 8 Issue 1 Fall 2010 2010 The orW ld Wide Web: Not So World Wide After All? Allison Lockhart Follow this and additional works at: http://lawecommons.luc.edu/pilr Part of the Internet Law Commons Recommended Citation Allison Lockhart, The World Wide Web: Not So World Wide After All?, 16 Pub. Interest L. Rptr. 47 (2010). Available at: http://lawecommons.luc.edu/pilr/vol16/iss1/8 This Article is brought to you for free and open access by LAW eCommons. It has been accepted for inclusion in Public Interest Law Reporter by an authorized administrator of LAW eCommons. For more information, please contact [email protected]. Lockhart: The World Wide Web: Not So World Wide After All? No. 1 • Fall 2010 THE WORLD WIDE WEB: NOT SO WORLD WIDE AFTER ALL? by ALLISON LOCKHART It’s hard to imagine not having twenty-four hour access to videos of dancing Icats or Ashton Kutcher’s hourly musings, but this is the reality in many countries. In an attempt to control what some governments perceive as a law- less medium, China, Saudi Arabia, Cuba, and a growing number of other countries have begun censoring content on the Internet.1 The most common form of censorship involves blocking access to certain web- sites, but the governments in these countries also employ companies to prevent search results from listing what they deem inappropriate.2 Other governments have successfully censored material on the Internet by simply invoking in the minds of its citizens a fear of punishment or ridicule that encourages self- censoring.3 47 Published by LAW eCommons, 2010 1 Public Interest Law Reporter, Vol. -

Telecommunications Regulation - Competition - ICT Access in the Asia Pacific Region

Telecommunications Regulation - Competition - ICT Access in the Asia Pacific Region Prepared by Hon David Butcher February 2010 Table of Contents Table of Contents .................................................................................................... - 1 - List of Tables ........................................................................................................... - 1 - List of Figures.......................................................................................................... - 2 - List of Appendixes................................................................................................... - 2 - List of Acronyms and Abbreviations........................................................................ - 2 - Glossary of Terms.................................................................................................... - 3 - 1. Introduction..................................................................................................... - 5 - 1.1 Background......................................................................................................- 5 - 1.2 Adapt to Change...............................................................................................- 6 - 2. Importance of Telecommunications ................................................................ - 7 - 2.1 Potential Market................................................................................................- 7 - 2.2 Economic Benefits.............................................................................................- -

Role of Librarian in Internet and World Wide Web Environment K

Informing Science Information Sciences Volume 4 No 1, 2001 Role of Librarian in Internet and World Wide Web Environment K. Nageswara Rao and KH Babu Defence Research & Development Laboratory Kanchanbagh Post, India [email protected] and [email protected] Abstract The transition of traditional library collections to digital or virtual collections presented the librarian with new opportunities. The Internet, Web en- vironment and associated sophisticated tools have given the librarian a new dynamic role to play and serve the new information based society in bet- ter ways than hitherto. Because of the powerful features of Web i.e. distributed, heterogeneous, collaborative, multimedia, multi-protocol, hyperme- dia-oriented architecture, World Wide Web has revolutionized the way people access information, and has opened up new possibilities in areas such as digital libraries, virtual libraries, scientific information retrieval and dissemination. Not only the world is becoming interconnected, but also the use of Internet and Web has changed the fundamental roles, paradigms, and organizational culture of libraries and librarians as well. The article describes the limitless scope of Internet and Web, the existence of the librarian in the changing environment, parallelism between information sci- ence and information technology, librarians and intelligent agents, working of intelligent agents, strengths, weaknesses, threats and opportunities in- volved in the relationship between librarians and the Web. The role of librarian in Internet and Web environment especially as intermediary, facilita- tor, end-user trainer, Web site builder, researcher, interface designer, knowledge manager and sifter of information resources is also described. Keywords: Role of Librarian, Internet, World Wide Web, Data Mining, Meta Data, Latent Semantic Indexing, Intelligent Agents, Search Intermediary, Facilitator, End-User Trainer, Web Site Builder, Researcher, Interface Designer, Knowledge Man- ager, Sifter. -

Minority Media and Community Agenda Setting a Study on Muslim Press in Kerala

Minority Media and Community Agenda Setting A Study On Muslim Press In Kerala Muhammadali Nelliyullathil, Ph.D. Dean, Faculty of Journalism and Head, Dept. of Mass Communication University of Calicut, Kerala India Abstract Unlike their counterparts elsewhere in the country, Muslim newspapers in Kerala are highly professional in staffing, payment, and news management and production technology and they enjoy 35 percent of the newspaper readership in Kerala. They are published in Malayalam when Indian Muslim Press outside Kerala concentrates on Urdu journalism. And, most of these newspapers have a promising newsroom diversity employing Muslim and non-Muslim women, Dalits and professionals from minority and majority religions. However, how effective are these newspapers in forming public opinion among community members and setting agendas for community issues in public sphere? The study, which is centered on this fundamental question and based on the conceptual framework of agenda setting theory and functional perspective of minority media, examines the role of Muslim newspapers in Kerala in forming a politically vibrant, progress oriented, Muslim community in Kerala, bringing a collective Muslim public opinion into being, Influencing non-Muslim media programming on Muslim issues and influencing the policy agenda of the Government on Muslim issues. The results provide empirical evidences to support the fact that news selection and presentation preferences and strategies of Muslim newspapers in Kerala are in line with Muslim communities’ news consumption pattern and related dynamics. Similarly, Muslim public’s perception of community issues are formed in accordance with the news framing and priming by Muslim newspapers in Kerala. The findings trigger more justifications for micro level analysis of the functioning of the Muslim press in Kerala to explore the community variable in agenda setting schema and the significance of minority press in democratic political context. -

Regulatory Bottlenecks of Wireless Expansion of Internet in India

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Omkarappa, Bhavya; Benseny, Jaume; Hämmäinen, Heikki Conference Paper Regulatory Bottlenecks of Wireless Expansion of Internet in India 29th European Regional Conference of the International Telecommunications Society (ITS): "Towards a Digital Future: Turning Technology into Markets?", Trento, Italy, 1st - 4th August, 2018 Provided in Cooperation with: International Telecommunications Society (ITS) Suggested Citation: Omkarappa, Bhavya; Benseny, Jaume; Hämmäinen, Heikki (2018) : Regulatory Bottlenecks of Wireless Expansion of Internet in India, 29th European Regional Conference of the International Telecommunications Society (ITS): "Towards a Digital Future: Turning Technology into Markets?", Trento, Italy, 1st - 4th August, 2018, International Telecommunications Society (ITS), Calgary This Version is available at: http://hdl.handle.net/10419/184934 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. -

Internet Freedom in China: U.S. Government Activity, Private Sector Initiatives, and Issues of Congressional Interest

Internet Freedom in China: U.S. Government Activity, Private Sector Initiatives, and Issues of Congressional Interest Patricia Moloney Figliola Specialist in Internet and Telecommunications Policy May 18, 2018 Congressional Research Service 7-5700 www.crs.gov R45200 Internet Freedom in China: U.S. Government and Private Sector Activity Summary By the end of 2017, the People’s Republic of China (PRC) had the world’s largest number of internet users, estimated at over 750 million people. At the same time, the country has one of the most sophisticated and aggressive internet censorship and control regimes in the world. PRC officials have argued that internet controls are necessary for social stability, and intended to protect and strengthen Chinese culture. However, in its 2017 Annual Report, Reporters Without Borders (Reporters Sans Frontières, RSF) called China the “world’s biggest prison for journalists” and warned that the country “continues to improve its arsenal of measures for persecuting journalists and bloggers.” China ranks 176th out of 180 countries in RSF’s 2017 World Press Freedom Index, surpassed only by Turkmenistan, Eritrea, and North Korea in the lack of press freedom. At the end of 2017, RSF asserted that China was holding 52 journalists and bloggers in prison. The PRC government employs a variety of methods to control online content and expression, including website blocking and keyword filtering; regulating and monitoring internet service providers; censoring social media; and arresting “cyber dissidents” and bloggers who broach sensitive social or political issues. The government also monitors the popular mobile app WeChat. WeChat began as a secure messaging app, similar to WhatsApp, but it is now used for much more than just messaging and calling, such as mobile payments, and all the data shared through the app is also shared with the Chinese government. -

UL-ISP Licences Final March 2015.Xlsx

Unified License of ISP Authorization S. No. Name of Licensee Cate Service Authorized person Registered Office Address Contact No. LanLine gory area 1 Mukand Infotel Pvt. Ltd. B Assam Rishi Gupta AC Dutta Lane , FA Road 0361-2450310 fax: no. Kumarpara, Guwahati- 781001, 03612464847 Asaam 2 Edge Telecommunications B Delhi Ajay Jain 1/9875, Gali No. 1, West Gorakh 011-45719242 Pvt. Ltd. Park, Shahdara, Delhi – 110032 3 Southern Online Bio B Andhra Satish kumar Nanubala A3, 3rd Floor, Office Block, Samrat 040-23241999 Technologies Ltd Pradesh Complex, Saifabad, Hyderabad-500 004 4 Blaze Net Limited B Gujarat and Sharad Varia 20, Paraskunj Society, Part I, Nr. 079-26405996/97,Fax- Mumbai Umiyavijay, Satellite Road, 07926405998 Ahmedabad-380015 Gujarat 5 Unified Voice Communication B + Tamilnadu K.Rajubharathan Old No. 14 (New No. 35), 4th Main 044-45585353 Pvt. Ltd. C (including Road, CIT Nagar, Nanthanam, Chennai)+ Chennai – 600035 Bangalore 6 Synchrist Network Services Pvt. B Mumbai Mr. Kiran Kumar Katara Shop No. 5, New Lake Palace Co- 022-61488888 Ltd , Director op-Hsg. Ltd., Plot No. 7-B, Opp Adishankaracharya Road, Powai, Mumbai – 400076 (MH) 7 Vala Infotech Pvt. Ltd. B Gujarat Mr. Bharat R Vala, Dhanlaxmi Building, Room No. 309, (02637) 243752. Fax M.D. 3rd Floor, Near Central Bank, (02637) 254191 Navsari – 396445 Gujarat 8 Arjun Telecom Pvt. C Chengalpatt Mr. N.Kannapaan, New No. 1, Old No. 4, 1st Floor, 044-43806716 Ltd(cancelled) u Managing Direcot, Kamakodi Nagar, Valasaravakkam, (Kancheepu Chennai – 600087 ram) 9 CNS Infotel Services Pvt. Ltd. B Jammu & Reyaz Ahmed Mir M.A. -

Low-Cost Wireless Internet System for Rural India Using Geosynchronous Satellite in an Inclined Orbit

Low-cost Wireless Internet System for Rural India using Geosynchronous Satellite in an Inclined Orbit Karan Desai Thesis submitted to the faculty of the Virginia Polytechnic Institute and State University in partial fulfillment of the requirements for the degree of Master of Science In Electrical Engineering Timothy Pratt, Chair Jeffrey H. Reed J. Michael Ruohoniemi April 28, 2011 Blacksburg, Virginia Keywords: Internet, Low-cost, Rural Communication, Wireless, Geostationary Satellite, Inclined Orbit Copyright 2011, Karan Desai Low-cost Wireless Internet System for Rural India using Geosynchronous Satellite in an Inclined Orbit Karan Desai ABSTRACT Providing affordable Internet access to rural populations in large developing countries to aid economic and social progress, using various non-conventional techniques has been a topic of active research recently. The main obstacle in providing fiber-optic based terrestrial Internet links to remote villages is the cost involved in laying the cable network and disproportionately low rate of return on investment due to low density of paid users. The conventional alternative to this is providing Internet access using geostationary satellite links, which can prove commercially infeasible in predominantly cost-driven rural markets in developing economies like India or China due to high access cost per user. A low-cost derivative of the conventional satellite-based Internet access system can be developed by utilizing an aging geostationary satellite nearing the end of its active life, allowing it to enter an inclined geosynchronous orbit by limiting station keeping to only east-west maneuvers to save fuel. Eliminating the need for individual satellite receiver modules by using one centrally located earth station per village and providing last mile connectivity using Wi-Fi can further reduce the access cost per user. -

The Internet and "Telecommunications Services," Universal Service Mechanisms, Access Charges, and Other Flotsam of the Regulatory System

The Internet and "Telecommunications Services," Universal Service Mechanisms, Access Charges, and Other Flotsam of the Regulatory System Jonathan Weinbergt In troduction .............................................................................................. 2 11 I. B ackground ...................................................................................... 2 14 A . InternetA rchitecture................................................................ 215 B . Telephone Regulation .............................................................. 217 1. The Federal-State Divide ................................................. 218 2. Comp uter II ...................................................................... 220 3. The 1996 Telecommunications Act ................................. 222 II. The Internet and Universal Service Mechanisms ............................ 225 A. The Report to Congress on Universal Service ......................... 225 B. The Breakdown of the Telecommunications/InformationService D istinction................................................................................ 227 C. Why the Telecommunications/InformationService D istinction Doesn't Work ........................................................ 232 D. Universal Service Redux .......................................................... 234 III. The Internet and Access Charges .................................................... 239 A . The Status Q uo ......................................................................... 239 B . Beyond the -

Mass Media in the USA»

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by BSU Digital Library Mass Media In The USA K. Khomtsova, V. Zavatskaya The topic of the research is «Mass media in the USA». It is topical because mass media of the United States are world-known and a lot of people use American mass media, especially internet resources. The subject matter is peculiarities of different types of mass media in the USA. The aim of the survey is to study the types of mass media that are popular in the USA nowadays. To achieve the aim the authors fulfill the following tasks: 1. to define the main types of mass media in the USA; 2. to analyze the popularity of different kinds of mass media in the USA; 3. to mark out the peculiarities of American mass media. The mass media are diversified media technologies that are intended to reach a large audience by mass communication. There are several types of mass media: the broadcast media such as radio, recorded music, film and tel- evision; the print media include newspapers, books and magazines; the out- door media comprise billboards, signs or placards; the digital media include both Internet and mobile mass communication. [4]. In the USA the main types of mass media today are: newspapers; magazines; radio; television; Internet. NEWSPAPERS The history of American newspapers goes back to the 17th century with the publication of the first colonial newspapers. It was James Franklin, Benjamin Franklin’s older brother, who first made a news sheet. -

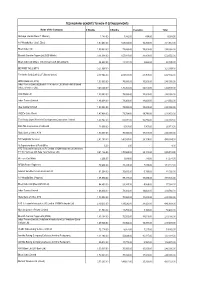

Copy of TP-Concession to Customers R Final 22.04.2021.Xlsx

TECHNOPARK-BENEFITS TO NON-IT ESTABLISHMENTS Name of the Company 6 Months 3 Months Esclation Total Akshaya (Kerala State IT Mission) 1,183.00 7,332.00 488.00 9,003.00 A V Hospitalities ( Café Elisa) 1,97,463.00 1,08,024.00 16,200.00 3,21,687.00 Bharti Airtel Ltd 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Bharath Sanchar Nigam Ltd (BSS Mobile) 3,14,094.00 1,57,047.00 31,409.00 5,02,550.00 Bharti Airtel Ltd (Bharti Tele-Ventures Ltd (Broad band) 26,622.00 13,311.00 2,662.00 42,595.00 BEYOND THE LIMITS 3,21,097.00 - - 3,21,097.00 Fire In the Belly Café L.L.P (Buraq Space) 4,17,066.00 2,08,533.00 41,707.00 6,67,306.00 HDFC Bank Ltd (ATM) 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Indus Towers Limited [Bharti Tele-Ventures Ltd (Mobile-Airtel) Bharti Infratel Ventures Ltd] 3,40,524.00 1,70,262.00 34,052.00 5,44,838.00 ICICI Bank Ltd 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Indus Towers Limited 1,46,604.00 73,302.00 14,660.00 2,34,566.00 Idea Cellular Limited 1,50,000.00 75,000.00 15,000.00 2,40,000.00 JODE's Cake World 1,47,408.00 73,704.00 14,741.00 2,35,853.00 The Kerala State Women's Development Corporation Limited 1,67,742.00 83,871.00 16,774.00 2,68,387.00 RAILTEL Corporation of India Ltd 13,008.00 6,504.00 1,301.00 20,813.00 State Bank of India, ATM 1,50,000.00 75,000.00 15,000.00 2,40,000.00 SS Hospitality Services 2,81,190.00 1,40,595.00 28,119.00 4,49,904.00 Sr.Superintendent of Post Office 6.00 3.00 - 9.00 ATC Telecom Infrastructure (P) Limited (VIOM Networks Ltd (Wireless TT Info Services Ltd, Tata Tele Services Ltd) 3,41,136.00 -

Digital Watermarking Based on DCT Transform

A Survey of Digital Watermarking Technologies Lin Liu [email protected] Abstract: This report introduces the basic concepts in digital watermarking. Common watermarking technologies are reviewed. Some experiment results are provided as well. Index Terms: Digital watermarking, copyright protection 1. INTRODUCTION During the past decade, with the development of information digitalization and internet, digital media increasingly predominate over traditional analog media. However, as one of the concomitant side-effects, it is also becoming easier for some individual or group to copy and transmit digital products without the permission of the owner. The digital watermark is then introduced to solve this problem. Covering many subjects such as signal processing, communication theory and Encryption, the research in digital watermark is to provide copyright protection to digital products, and to prevent and track illegal copying and transmission of them. Watermarking is embedding information, which is able to show the ownership or track copyright intrusion, into the digital image, video or audio. Its purpose determines that the watermark should be indivisible and robust to common processing and attack. Currently the digital watermarking technologies can be divided into two categories by the embedding position——spatial domain and transform domain watermark. Spatial domain techniques developed earlier and is easier to implement, but is limited in robustness, while transform domain techniques, which embed watermark in the host’s transform domain, is more sophisticated and robust. With the development of digital watermarking, spatial techniques, due to their weakness in robustness, are generally abandoned, and frequency algorithm based on DCT or DWT becomes the research focus. Another tendency in watermarking is blind extraction, which means the host is not need when extracting the watermark; otherwise it is hard to avoid the multiple claims of ownerships.