IFX Day 2003

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Development of Plug-In Air Powered Four Wheels Motorcycle Drivetrain Control Unit

DEVELOPMENT OF PLUG-IN AIR POWERED FOUR WHEELS MOTORCYCLE DRIVETRAIN CONTROL UNIT TAN BENG LENG Report submitted in partial fulfillment of requirements for award of the Degree of Bachelor of Mechanical Engineering with Automotive Engineering Faculty of Mechanical Engineering UNIVERSITI MALAYSIA PAHANG JUNE 2013 v ABSTRACT This thesis is related to the development of plug-in air powered four wheel motorcycles drive train system that transfers rotational energy from power train to the driving wheel. The objective of this thesis is to develop an air hybrid drivetrain unit and control the power and torque from the powertrain to the driving wheel by using sequential manual transmission. This thesis describes the process of developing sequential shift-by-wire system to make gear shifting for easier for 4 wheel motorcycle. The controller used in this project was 18F PIC 4550 microprocessor. The system programming performed using FLOWCODE version 4.0. 2 units of electromechanical linear actuator were used in this project as an actuator for gear shifting on a manual transmission. Chain drives were selected as power transfer linkage from air hybrid engine to the driving wheel with under drive configuration. Besides the development of shift-by-wire system, the torque on the driving wheel also had been calculated and analysed. In additional, the maximum speed that can be achieved by four wheel motorcycles was also calculated. vi ABSTRAK Tesis ni berkaitan dengan pembangunan sistem pacuan yang memindahkan tenaga putaran ke roda pacuan untuk “plug-in hybrid air powered” motosikal empat roda. Objectif tesis ini ialah untuk membangunkan pacaun “ air hybrid” and mengawal kuasa and tork daripada janakuasa kepada roda paduan mengunakan transmisi manual berturutan. -

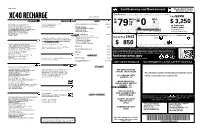

XC40 RECHARGE Mpge MPG Gallons PERFORMANCE AUTHORIZED RETAILER PRICING Per 100

2021Volvo Fuel Economy and Environment Plug-In Hybrid Vehicle Electricity-Gasoline Fuel Economy Small SUV range from 16 to 120 MPGe. The best vehicle rates 120 MPGe. Volvo Car USA LLC Electricity + Gasoline Gasoline Only You save www.volvocars.com/us Charge Time: 8hours ( 240 V) XC40 RECHARGE MPGe MPG gallons PERFORMANCE AUTHORIZED RETAILER PRICING per 100 ...................................................................................................... ...................................................................................................... .................................................................................................................... 1.0 miles .0 kW-hrs $ 3,250 Pure Electric, Zero Tailpipe Emission VOLVO CARS BELLEVUE 5702 IMPORTER'S SUGGESTED LIST PRICE P.O.E.: $ 53,990.00 gallons per per 100 85 72 Front and Rear Electric Motors 420 116TH AVENUE NE 43 miles 100 miles in fuel costs combined city/highway 0combined city/highway 78 kWh Lithium Ion High Voltage Battery BELLEVUE, WA 98004 Climate Package 750.00 79 over 5 years Shift-by-Wire Single Speed Transmission Heated Windshield Wiper Blades Driving Range Anti-Lock Braking Sys (ABS) w/ Hill Start Assist compared to the 402 Horsepower and 486 lb-ft torque Heated Rear Seats Electricity + Gasoline Gasoline Only Electric Power Assisted Steering Heated Steering Wheel 0 0 0 0 0 average new vehicle. All-Wheel-Drive with Instant Traction All Electric range = 0 to 8 miles 0 miles Dynamic Chassis Advanced Package 1,300.00 19" Alloy Wheels Headlight High Pressure Cleaning Fuel Economy & Greenhouse Gas Rating (tailpipe only) Smog Rating (tailpipe only) ......................................................................................................WARRANTY Pilot Assist Driver Assistance System with Annual Fuel 48 Month/50,000 Mile Limited Warranty Coverage cost MPG Adaptive Cruise Control 144 Month Corrosion Protection "Unlimited Mileage" 360 Surround View Camera Refer to Warranty Info Book for Specific Limitations. -

948TE Introduction Webinar Handout

ZF9HP48 / 948TE Introduction Presented by: Mike Souza ATRA Senior Research Technician 948TE Intro Webinar ©2015 ATRA. All Rights Reserved. Vehicle Application Acura (ZF9HP48) Land Rover MDX 2014-15 AWD V6 3.5L Range Rover Evoque 2013-15 FWD/4X4 L4 2.0/2.2L RLX 2014-15 FWD V6 3.5L/3.7L Discovery (LR4) 2015 FWD/AWD L4 2.0 Chrysler (948TE) TL 2014-15 AWD V6 3.5L/3.7L 200 2014-15 FWD L4 2.4L V6 3.2L Town & Country 2013-15 FWD 2013-14 L4 2.4L V6 3.6L Dodge (948TE) Caravan 2014-15 FWD V6 3.6L Fiat (EP2) 500X 2014-15 FWD L4 2.4L Doblo 2015 FWD L4 2.4L Jeep (948TE) Cherokee (KL) 2013-15 FWD L4 2.4L V6 3.2L Renegade 2014-15 FWD L4 2.4L Honda (ZF9HP48) Civic 2014-15 FWD L4 1.6L CRV 2014-15 FWD L4 1.6L Transmission Identification Chrysler 948TE (Kokomo IN) ZF 9HP48 (Germany) • Externally the two units are visually similar • Parts cannot be interchanged. • VIN should always be used as the key for parts lookup. • Barcode label includes the manufacturer identification in the second and third characters of the traceability number. 9 Nine forward gear speeds 48 480 Nm torque capacity 354 lbs ft T Transverse mounted E Electronic control HP Hydraulic planetary Introduction ZF developed the first nine-speed automatic transmission for front wheel drive vehicles. Although it was built in June 2011 it did not make it’s debut until mid 2013. This new transmission delivers extremely short shifting times and exceptionally smooth shifts. -

Design of Automotive X-By-Wire Systems Cédric Wilwert, Nicolas Navet, Ye-Qiong Song, Françoise Simonot-Lion

Design of automotive X-by-Wire systems Cédric Wilwert, Nicolas Navet, Ye-Qiong Song, Françoise Simonot-Lion To cite this version: Cédric Wilwert, Nicolas Navet, Ye-Qiong Song, Françoise Simonot-Lion. Design of automotive X-by- Wire systems. Richard Zurawski. The Industrial Communication Technology Handbook, CRC Press, 2005, 0849330777. inria-00000562 HAL Id: inria-00000562 https://hal.inria.fr/inria-00000562 Submitted on 27 Aug 2007 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. Design of automotive X-by-Wire systems Cédric Wilwert PSA Peugeot - Citroën 92000 La Garenne Colombe - France Fax: +33 3 83 58 17 01 Phone: +33 3 83 58 17 17 [email protected] Nicolas Navet LORIA UMR 7503 – INRIA Campus Scientifique - BP 239 - 54506 VANDOEUVRE-lès-NANCY CEDEX Fax: +33 3 83 58 17 01 Phone : +33 3 83 58 17 61 [email protected] Ye Qiong Song LORIA UMR 7503 – Université Henri Poincaré Nancy I Campus Scientifique - BP 239 - 54506 VANDOEUVRE-lès-NANCY CEDEX Fax: +33 3 83 58 17 01 Phone : +33 3 83 58 17 64 [email protected] Françoise Simonot-Lion LORIA UMR 7503 – Institut National Polytechnique de Lorraine Campus Scientifique - BP 239 - 54506 VANDOEUVRE-lès-NANCY CEDEX Fax: +33 3 83 27 83 19 Phone : +33 3 83 58 17 62 [email protected] CONTENTS Design of automotive X-by-Wire systems ...................................................................................................... -

Kia-K900-2016-CA.Pdf

2016 K900 A NEW CONCEPT OF LUXURY. Why follow a well-worn path when you can follow a path of your own? That mode of thinking applies to the way you select a truly ground-breaking luxury automobile. It also describes how Kia Premium pursued its reinvention of luxury driving – a pursuit that reaches its ultimate expression in the newly redesigned 2016 Kia K900. It’s the rear-drive performance luxury sedan that embodies a fresh and unpretentious approach that’s sure to heighten your enthusiasm. Highlights include everything from the supremely confident performance of the available 420-horsepower9 5.0L Gasoline Direct Injection (GDI) V8 engine to such top-tier amenities as the concert-hall sound quality of the premium Lexicon Discrete Logic 7® 4 surround-sound audio system. The exquisite craftsmanship of the available glove-soft Nappa leather trim and available genuine wood trim accents rounds out the experience with exceptional refinement. In the 2016 K900. INTERNATIONAL MODEL SHOWN. Some features may vary. IT LEADS BY EXAMPLE. When you’re entering uncharted territory, you need to have a singular sense of direction. Kia knew exactly how it wanted to transform performance luxury driving to deliver on “The Power to Surprise”. The results are on vivid display in the K900, beginning with its evocative design. The superbly balanced, extended wheelbase rear-drive platform provides a solid foundation for the scintillating performance of the 311-horsepower 3.8L GDI V6 engine or the available 420-horsepower9 5.0L GDI V8. The robust power is complemented by the K900’s precision shifting eight-speed automatic transmission with its available shift-by-wire gear selector. -

2021 RDX Competitive Comparison

2021 RDX Competitive Comparison 2020 Standard (S), Optional (O), Not Available (–) 2021 2021 Audi 2021 2020 2021 2021 Mercedes-Benz Acura RDX Q5 45 TFSI quattro BMW X3 30i Buick Envision Cadillac XT5 Lexus NX 300 GLC SUV ENGINE/MOTOR DOHC 4-cylinder DOHC turbocharged DOHC turbocharged DOHC turbocharged (FWD/AWD); DOHC turbocharged DOHC turbocharged DOHC turbocharged Engine type 4-cylinder 4-cylinder 4-cylinder DOHC turbocharged 4-cylinder 4-cylinder 4-cylinder 4-cylinder (AWD) Engine displacement 2.0 (turbocharged) (liters) 2.0 2.0 2.0 2.5 2.0 2.0 2.0 Power (hp @ rpm) 197 @ 6300 (2.5); (SAE net) 272 @ 6500 261 @ 5000–6000 248 @ 5200–6500 252 @ 5500 (2.0) 235 @ 5000 235 @ 4800–5600 255 @ 5800–6100 273 @ 258 @ 192 @ 4400 (2.5); Torque (lb-ft @ rpm) 280 @ 1600-4500 1600–4500 1450–4800 295 @ 3000 (2.0) 258 @ 1500–4000 258 @ 1650–4000 273 @ 1800–4000 S Direct fuel injection S S S S S (Plus port injection) S S S S S S S S Variable valve timing (VTEC®) Idle stop S S S S S – S DRIVETRAIN S S S S S S 2-wheel drive (Front-wheel) – (Rear-wheel) (Front-wheel) (Front-wheel) (Front-wheel) (Rear-wheel) O S O O O O All-wheel drive (Super Handling All-Wheel ® (Active Twin-Clutch Rear (Active Twin-Clutch Rear O ® Drive™ [SH-AWD®]) (quattro ) (xDrive) Differential) Differential) (4MATIC ) O O O Torque-vectoring (Super Handling All- – – (Active Twin-Clutch Rear (Active Twin-Clutch Rear – – all-wheel drive Wheel Drive™) Differential) Differential) S S S S (6-speed); S S S Automatic transmission (10-speed) (7-speed DCT) (8-speed) O (9-speed) (9-speed) (6-speed) -

Steer-By-Wire Architecture: Case of Study

Design of automotive X-by-Wire systems Cédric Wilwert PSA Peugeot - Citroën 92000 La Garenne Colombe - France Fax: +33 3 83 58 17 01 Phone: +33 3 83 58 17 17 [email protected] Nicolas Navet LORIA UMR 7503 – INRIA Campus Scientifique - BP 239 - 54506 VANDOEUVRE-lès-NANCY CEDEX Fax: +33 3 83 58 17 01 Phone : +33 3 83 58 17 61 [email protected] Ye Qiong Song LORIA UMR 7503 – Université Henri Poincaré Nancy I Campus Scientifique - BP 239 - 54506 VANDOEUVRE-lès-NANCY CEDEX Fax: +33 3 83 58 17 01 Phone : +33 3 83 58 17 64 [email protected] Françoise Simonot-Lion LORIA UMR 7503 – Institut National Polytechnique de Lorraine Campus Scientifique - BP 239 - 54506 VANDOEUVRE-lès-NANCY CEDEX Fax: +33 3 83 27 83 19 Phone : +33 3 83 58 17 62 [email protected] CONTENTS Design of automotive X-by-Wire systems ....................................................................................................... 1 Abstract : ............................................................................................................................................................... 2 1 Why X-by-Wire systems ?.......................................................................................................................... 3 1.1 Steer-by-Wire system .......................................................................................................................... 4 1.2 Brake-by-Wire systems ....................................................................................................................... 4 2 Problem, context and constraints -

GENESIS GV70 Quick Reference Guide I 02 FEATURES and CONTROLS

☐ DEMONSTRATE AUTOMATIC CLIMATE CONTROL - page 17 MAINTENANCE VOICE RECOGNITION TIPS ☐ DEMONSTRATE HOW TO OPERATE WINDSHIELD WIPER AND Scheduled Maintenance (Normal Usage) 2.5T 3.5T BLUETOOTH® WASHER – page 12 Engine Oil And Filter Replace 8,000 or 12 mos. Replace 8,000 or 12 mos. Command Example Fuel Additives Add 7,500 or 12 mos. Add 6,000 or 12 mos. Dial <Phone #> “Dial ☐ HOW TO DEFROST 7-1-4-0-0-0-8-8-8-8” Tire Rotation Perform 7,500 or 12 mos. Perform 6,000 or 12 mos. 1 Call <Name> “Call John Smith” Press the front defrost button. Vacuum Hose Improving how you store your contacts can optimize your 2 Air Conditioning Refrigerant Bluetooth® Voice Recognition performance: Set to warmest temperature setting. • Use full names instead of short or single-syllable names 3 Brake Hoses & Lines (“John or Dad”) Set to highest fan speed. • Avoid using special characters/emojis or abbreviations Drive Shafts & Boots (“Dr.”) when saving contacts ☐ TIRE PRESSURE MONITORING SYSTEM (TPMS)- page 42 Exhaust Pipe & Muffler NAVIGATION Front Brake Disc/Pads, Calipers Inspect 7,500 or 12 mos. Inspect 6,000 or 12 mos. Command Example Low tire pressure indicator / Rear Brake Disc/Pads Find Address “1-2-3-4-5 1st Street, GENESIS Steering Gear Box, Linkage & Boots/ Lower <House #, Street, Fountain Valley” TPMS malfunction indicator Arm Ball Joint, Upper Arm Ball Joint City, State> Find <POI Name> “Find McDonald’s®” NOTE: Tire pressure may vary in colder temperatures causing the Suspension Mounting Bolts low tire pressure indicator to illuminate. Inflate tires according to Propeller Shaft GV70 Located on Rearview Mirror Inspect 7,500 or 6 mos. -

Comparison of Usability Between Gear Shifters with Varied Visual and Haptic Patterns and Complexities

Multimodal Technologies and Interaction Article Comparison of Usability between Gear Shifters with Varied Visual and Haptic Patterns and Complexities Sanna Lohilahti Bladfält * , Camilla Grane and Peter Bengtsson Department of Business Administration, Technology and Social Sciences, Luleå University of Technology, 971 87 Luleå, Sweden; [email protected] (C.G.); [email protected] (P.B.) * Correspondence: [email protected]; Tel.: +46-920-49-33-86 Received: 3 April 2020; Accepted: 27 May 2020; Published: 29 May 2020 Abstract: Shift-by-wire technology enables more options concerning the design, placement and functions of gear shifters compared to traditional gear shifters with manual transmission. These variations can impact usability and driver performance. There is a lack of research regarding the potential advantages and disadvantages of different types of gear shifters. The purpose of this study was to investigate the efficiency and subjective ease-of-use of mono- and polystable joystick gear shifter types at different complexity levels and with full or limited visibility. An experimental study with 36 participants was conducted. The results showed that monostable joysticks, especially those with an I/J-shape, were overall less efficient and easy to use than polystable joysticks. The highest complexity level clearly affected the efficiency for the monostable joystick with an I/J-shape (mono I/J) compared with the other gear shifter types. The monostable joystick with an I/J-shape (mono I/J) was also most affected by reduced visibility at the highest level of complexity, indicating that it was more prone to causing users to take their eyes off the road. -

Borgwarner Egeardrive(For Customer)

BorgWarner DrivetrainSystems eGearDrive高效电动车驱动桥 8 Dec, 2011 Our Beliefs Respect Collaboration Excellence Integrity Community PDF created with pdfFactory Pro trial version www.pdffactory.com BorgWarner Overview 2 PDF created with pdfFactory Pro trial version www.pdffactory.com BorgWarner = Powertrain Innovation Engine 72% / SALES Drivetrain 28% / SALES Turbo Systems Morse TEC Drivetrain Systems ® • AWD Couplings • Wastegate • Engine Valve Timing Systems • DualTronic Systems for Dual Clutch Transmissions • Variable Turbine Geometry • Timing Chain • Transfer Cases (VTG) • Transmission Control Modules • eGearDrive® Electric • Variable Cam Timing and Solenoids • Regulated 2-stage ® Drive Transmissions • HY-VO Transmission Chain • High Pressure Transmission (R2S™) • eAWD Torque Vectoring Control and Actuation Systems BERU Systems • AWD Electronic Controls • One-way Clutches • Glow Plugs and Systems Integration Thermal Systems • Friction Plates • Thermal Management • Instant Start System Components and Systems • Pressure Sensor Glow Plugs • Visctronic® Systems • Spark Plugs Morse TEC Drivetrain • Fans/Fan Drives • Ignition leads, Ignition Cables Thermal Systems • Ignition Coils Systems Emissions Systems • Sensor Technology • Exhaust Gas Recirculation • PTC Cabin Heaters (EGR) Valves • Tire Pressure Emissions • EGR Coolers & EGR tubes Monitoring System Systems • Integrated EGR Modules • Secondary Air Systems Turbo • Actuators BERU Systems Systems 3 PDF created with pdfFactory Pro trial version www.pdffactory.com Drivetrain Systems Global Footprint -

Features by Trim

2021 Honda Passport FEATURES BY TRIM Passport Sport ENGINEERING • Hill start assist • 4-wheel disc brakes with ABS and Electronic Brake Distribution (EBD) • 3.5-liter, 24-valve SOHC i-VTEC® V-6 • MacPherson strut front suspension engine with direct injection • Brake Assist • Multi-link rear suspension • 280 horsepower @ 6200 rpm (SAE net) • LED Daytime Running Lights (DRL) • Front and rear stabilizer bars • 262 lb-ft of torque @ 4700 rpm (SAE net) • Tire Pressure Monitoring System (TPMS)8 • Electric power-assisted rack-and-pinion with Tire Fill Assist • Available Intelligent Variable Torque steering (EPS) Management™ (i-VCM4®) all-wheel • Advanced front airbags (i-SRS) drive system • 20-inch alloy wheels • SmartVent® front side airbags • Variable Cylinder Management™ (VCM®) • P245/50 R20 102H all-season tires • Side curtain airbags with rollover sensor • Active Control Engine Mount System (ACM) • 3-point seat belts at all seating positions ™ • Active Noise Cancellation (ANC) SAFETY • Driver’s and front passenger’s seat-belt reminder ™ • Eco Assist system • Collision Mitigation Braking System™ (CMBS™)2 • Lower Anchors and Tethers for CHildren • Drive-by-Wire throttle system (LATCH) • Forward Collision Warning (FCW)3 • LEV3-ULEV125 CARB emissions rating1 • Road Departure Mitigation System (RDM)4 • Direct-injection system with immobilizer • Lane Departure Warning (LDW)5 FEATURES • 9-speed automatic transmission • Advanced Compatibility Engineering™ • Adaptive Cruise Control (ACC)9 • Shift-by-wire technology (ACE™) body structure • Lane Keeping -

All-New 2018 Buick Enclave

October 2017, Volume 19, No. 19 All-New 2018 Buick Enclave CONTENTS The 2018 Enclave, Buick’s all-new seven passenger midsize luxury SUV, features a longer wheelbase than the previous generation with a body structure built for safety, strength and mass efficiency. The standard 3.6L V6 engine with Stop/Start technology is paired with an efficient 9-speed automatic trans- mission. Plus, there are 17 radar, camera and ultrasonic sensors, when fully All-New 2018 Buick Enclave ...........1 equipped, that provide a wealth of data for the numerous safety and collision avoidance features. Intake Rocker Arm Oil New Model, New Technology Control Valve Components ............4 The 2018 Enclave is now available in a new Avenir model, which is Buick’s Forward Collision System new luxury sub-brand that offers unique styling cues and an extensive list of Reduced Message ...................4 premium features. Battery Vent Plug Installation ..........5 The new styling of the Enclave showcases a lower roofline and sharper windshield angle than the model it replaces. It includes Buick’s traditional UPDATE: Loose Charge QuietTuning sound-blocking features, yet with a new active noise cancellation Air Cooler Ductwork .................5 system. Also offering additional comfort for passengers is the new available air ionizer that eliminates odors and provides enhanced air quality. The air ionizer works by producing negatively charged particles that attract air-born contaminants Customer Care and Aftersales continued on page 2 All-New 2018 Buick Enclave – continued from page 1 and break down their structure, cleaning the cabin air. The ionizer Selecting a gear is done with the shift-by-wire Electronic Preci- doesn’t require any maintenance, but the traditional cabin filter sion Shift (EPS) gear selector, which eliminates the mechanical should be serviced regularly.