Return of Private Foundation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Israel's National Religious and the Israeli- Palestinian Conflict

Leap of Faith: Israel’s National Religious and the Israeli- Palestinian Conflict Middle East Report N°147 | 21 November 2013 International Crisis Group Headquarters Avenue Louise 149 1050 Brussels, Belgium Tel: +32 2 502 90 38 Fax: +32 2 502 50 38 [email protected] Table of Contents Executive Summary ................................................................................................................... i Recommendations..................................................................................................................... iv I. Introduction ..................................................................................................................... 1 II. Religious Zionism: From Ascendance to Fragmentation ................................................ 5 A. 1973: A Turning Point ................................................................................................ 5 B. 1980s and 1990s: Polarisation ................................................................................... 7 C. The Gaza Disengagement and its Aftermath ............................................................. 11 III. Settling the Land .............................................................................................................. 14 A. Bargaining with the State: The Kookists ................................................................... 15 B. Defying the State: The Hilltop Youth ........................................................................ 17 IV. From the Hills to the State .............................................................................................. -

Ben-Gurion University of the Negev the Jacob Blaustein Institutes for Desert Research the Albert Katz International School for Desert Studies

Ben-Gurion University of the Negev The Jacob Blaustein Institutes for Desert Research The Albert Katz International School for Desert Studies Evolution of settlement typologies in rural Israel Thesis submitted in partial fulfillment of the requirements for the degree of "Master of Science" By: Keren Shalev November, 2016 “Human settlements are a product of their community. They are the most truthful expression of a community’s structure, its expectations, dreams and achievements. A settlement is but a symbol of the community and the essence of its creation. ”D. Bar Or” ~ III ~ תקציר למשבר הדיור בישראל השלכות מרחיקות לכת הן על המרחב העירוני והן על המרחב הכפרי אשר עובר תהליכי עיור מואצים בעשורים האחרונים. ישובים כפריים כגון קיבוצים ומושבים אשר התבססו בעבר בעיקר על חקלאות, מאבדים מאופיים הכפרי ומייחודם המקורי ומקבלים צביון עירוני יותר. נופי המרחב הכפרי הישראלי נעלמים ומפנים מקום לשכונות הרחבה פרבריות סמי- עירוניות, בעוד זהותה ודמותה הייחודית של ישראל הכפרית משתנה ללא היכר. תופעת העיור המואץ משפיעה לא רק על נופים כפריים, אלא במידה רבה גם על מרחבים עירוניים המפתחים שכונות פרבריות עם בתים צמודי קרקע על מנת להתחרות בכוח המשיכה של ישובים כפריים ולמשוך משפחות צעירות חזקות. כתוצאה מכך, סובלים המרחבים העירוניים, הסמי עירוניים והכפריים מאובדן המבנה והזהות המקוריים שלהם והשוני ביניהם הולך ומיטשטש. על אף שהנושא מעלה לא מעט סוגיות תכנוניות חשובות ונחקר רבות בעולם, מעט מאד מחקר נעשה בנושא בישראל. מחקר מקומי אשר בוחן את תהליכי העיור של המרחב הכפרי דרך ההיסטוריה והתרבות המקומית ולוקח בחשבון את התנאים המקומיים המשתנים, מאפשר התבוננות ואבחנה מדויקים יותר על ההשלכות מרחיקות הלכת. על מנת להתגבר על הבסיס המחקרי הדל בנושא, המחקר הנוכחי החל בבניית בסיס נתונים רחב של 84 ישובים כפריים (קיבוצים, מושבים וישובים קהילתיים( ומצייר תמונה כללית על תהליכי העיור של המרחב הכפרי ומאפייניה. -

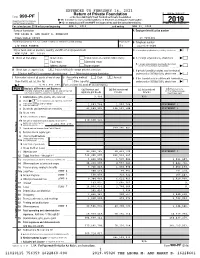

990-PF Or Section 4947(A)(1) Trust Treated As Private Foundation | Do Not Enter Social Security Numbers on This Form As It May Be Made Public

EXTENDED TO FEBRUARY 16, 2021 Return of Private Foundation OMB No. 1545-0047 Form 990-PF or Section 4947(a)(1) Trust Treated as Private Foundation | Do not enter social security numbers on this form as it may be made public. Department of the Treasury 2019 Internal Revenue Service | Go to www.irs.gov/Form990PF for instructions and the latest information. Open to Public Inspection For calendar year 2019 or tax year beginning APR 1, 2019 , and ending MAR 31, 2020 Name of foundation A Employer identification number THE LEONA M. AND HARRY B. HELMSLEY CHARITABLE TRUST 13-7184401 Number and street (or P.O. box number if mail is not delivered to street address) Room/suite B Telephone number 230 PARK AVENUE 659 212-679-3600 City or town, state or province, country, and ZIP or foreign postal code C If exemption application is pending, check here ~ | NEW YORK, NY 10169 G Check all that apply: Initial return Initial return of a former public charity D 1. Foreign organizations, check here ~~ | Final return Amended return 2. Foreign organizations meeting the 85% test, Address change Name change check here and attach computation ~~~~ | X H Check type of organization: Section 501(c)(3) exempt private foundation E If private foundation status was terminated Section 4947(a)(1) nonexempt charitable trust Other taxable private foundation under section 507(b)(1)(A), check here ~ | X I Fair market value of all assets at end of year J Accounting method: Cash Accrual F If the foundation is in a 60-month termination (from Part II, col. -

The Economic Base of Israel's Colonial Settlements in the West Bank

Palestine Economic Policy Research Institute The Economic Base of Israel’s Colonial Settlements in the West Bank Nu’man Kanafani Ziad Ghaith 2012 The Palestine Economic Policy Research Institute (MAS) Founded in Jerusalem in 1994 as an independent, non-profit institution to contribute to the policy-making process by conducting economic and social policy research. MAS is governed by a Board of Trustees consisting of prominent academics, businessmen and distinguished personalities from Palestine and the Arab Countries. Mission MAS is dedicated to producing sound and innovative policy research, relevant to economic and social development in Palestine, with the aim of assisting policy-makers and fostering public participation in the formulation of economic and social policies. Strategic Objectives Promoting knowledge-based policy formulation by conducting economic and social policy research in accordance with the expressed priorities and needs of decision-makers. Evaluating economic and social policies and their impact at different levels for correction and review of existing policies. Providing a forum for free, open and democratic public debate among all stakeholders on the socio-economic policy-making process. Disseminating up-to-date socio-economic information and research results. Providing technical support and expert advice to PNA bodies, the private sector, and NGOs to enhance their engagement and participation in policy formulation. Strengthening economic and social policy research capabilities and resources in Palestine. Board of Trustees Ghania Malhees (Chairman), Ghassan Khatib (Treasurer), Luay Shabaneh (Secretary), Mohammad Mustafa, Nabeel Kassis, Radwan Shaban, Raja Khalidi, Rami Hamdallah, Sabri Saidam, Samir Huleileh, Samir Abdullah (Director General). Copyright © 2012 Palestine Economic Policy Research Institute (MAS) P.O. -

Return of Private Foundation

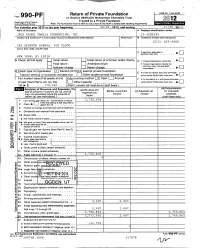

Return of Private Foundation OMB No 1545 -0052 Fonn 990 -PFI or Section 4947( a)(1) Nonexempt Charitable Trust Treated as a Private Foundation 2012 Department of the Treasury Internal Revenue Sennce Note The foundation may be able to use a copy of this return to satisfy state reporting requirements For calendar year 2012 or tax year beginning 12/01 , 2012 , and endii 11/30. 2013 Name of foundation A Employer identification number JACK ADJMT FAMILY FOUNDATION. INC. 13-3202295 Number and street ( or P 0 box number If mail is not delivered to street address ) Room/suite B Telephone number ( see instructions) (212) 629-9600 463 SEVENTH AVENUE, 4TH FLOOR City or town, state , and ZIP code C If exemption application is , q pending , check here . NEW YORK, NY 10018 G Check all that apply: Initial return Initial return of a former public charity D 1 Foreign organ izations . check here El Final return Amended return 2 Foreign organizations meeting the 85% test, check here and attach Address change Name chang e computation . • • • • • • . H Check type of organization X Section 501 ( cJ 3 exempt private foundation E If private foundation status was terminated Section 4947 ( a )( 1 nonexem pt charitable trust Other taxable p rivate foundation under section 507(bxlXA ), check here . Ill. El I Fair market value of all assets at end J Accountin g method X Cash L_J Accrual F If the foundation is in a 60-month termination of year (from Part Il, col. (c), line 0 Other ( specify) _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ under section 507(b )( 1)(B), check here 16) 10- $ 17 0 , 2 4 0 . -

The Absentee Property Law and Its Implementation in East Jerusalem a Legal Guide and Analysis

NORWEGIAN REFUGEE COUNCIL The Absentee Property Law and its Implementation in East Jerusalem A Legal Guide and Analysis May 2013 May 2013 Written by: Adv. Yotam Ben-Hillel Consulting legal advisor: Adv. Sami Ershied Language editor: Risa Zoll Hebrew-English translations: Al-Kilani Legal Translation, Training & Management Co. Cover photo: The Cliff Hotel, which was declared “absentee property”, and its owner Ali Ayad. (Photo by: Mohammad Haddad, 2013). This publication has been produced with the financial assistance of the Norwegian Ministry of Foreign Affairs. The contents of this publication are the sole responsibility of the authors and can under no circumstances be regarded as reflecting the position or the official opinion of the Norwegian Ministry of Foreign Affairs. The Norwegian Refugee Council (NRC) is an independent, international humanitarian non-governmental organisation that provides assistance, protection and durable solutions to refugees and internally displaced persons worldwide. The author wishes to thank Adv. Talia Sasson, Adv. Daniel Seidmann and Adv. Raphael Shilhav for their insightful comments during the preparation of this study. 3 Table of Contents 1. Introduction ...................................................................................................... 8 2. Background on the Absentee Property Law .................................................. 9 3. Provisions of the Absentee Property Law .................................................... 14 3.1 Definitions .................................................................................................................... -

2006 Hamerkaz

HAMERKAZ F ALL 2006 E DITION PRESENTS A P UBLICATION OF THE SEPHARDIC EDUCATIONAL CENTER INSIDE... FREE TRIP TO ISRAEL CHAPTER NEWS LOS ANGELES FILM FESTIVAL 25TH ANNIVERSARY HIGHLIGHTS A C E N T E R F O R A L L J E W S Celebrating the SEC By Dr. Jose A. Nessim Founder The Sephardic Educational Center in Jerusalem (SEC) celebrated its 25th anniversary last year. It is the only such Center in the Jewish world. The SEC campus is composed of three buildings that once served as the headquarters of all the Jews in Ottoman Palestine up until the beginning of the 20th century. Today, the SEC has lodging for up to 250 guests. Over 35,000 young people and adults have visited the SEC in Jerusalem to study and learn over the past 25 years. The SEC is a movement that is open to all Jews. Young people of high school and university age, as well as young single professionals up to age 36 have visited the SEC since we opened our doors in 1980 to learn more about Jewish-Sephardic cul - ture, philosophy, history, etc. Over the years, the SEC established an international Young Adult Movement that continues to unite the next generation with classes, socials, cultural and religious events. Through these activities which have been organized by mostly volunteers, we have brought thousands back to their religious identity and happily boast hundreds of couples who today are mar - ried thanks to the SEC. The SEC also has an accredited university program in Jerusalem, known as Makor, that can be taken for one or two semesters, and we offer scholarships that cover part of the tuition. -

Fourth Edition with CARJACKING SAFETY TIPS!

Fourth Edition WITH CARJACKING SAFETY TIPS! IN THE EVENT OF AN EMERGENCY, CALL POLICE 911 SHOMRIM 718-774-3333 HATZALAH 718-387-1750 Preparing our community today for a safe and secure tomorrow and Rabbi ,ע׳׳ה ,Dr. Bernard Kapiloff .ע׳׳ה ,The Chesed Fund Limited is dedicated in memory of Mordechai & Rebecca Kapiloff .ע׳׳ה ,Project Ezra of Greater Baltimore, Inc. is dedicated in memory of M. Leo Storch .ע׳׳ה ,Norman & Louise Gerstenfeld The guide is in loving memory of Hatomim Hakodosh Aharon Yosef Ben Chananya Sinai Dovid Halberstam, HY”D P ROTECT YOURSELF. PROTECT YOUR WEALTH. Life & Disability Insurance • Annuities Wealth Transfer • Re tirement Planning MOSHE KUPFER, RFC Registered Financial Consultant 718.436.1997 | 917.847.2673 [email protected] Crime surges in our community have become the “norm.” Take responsibility for yourself and your loved ones. Prevention is the key to staying safe. There are no foolproof techniques or hardware that can absolutely guarantee your safety or security, but taking proper precautions can make you less likely to be targeted or victimized by criminals. Don’t make the mistake of thinking that it can only happen to someone else. Since most of us are already familiar with safety and security basics, this checklist provides some new and less well known techniques and technologies to protect you, your family, your home, and your car. Report It To Thwart It!TM If you are a victim of a crime, please report it to police and Shomrim as soon as possible, including on Shabbos or Yom Tov. Report data is used to apprehend criminals and to increase crime-fighting resources in our community. -

Kol Kehillat Kernow 06 09.FH11

KolKol KehillatKehillat KernowKernow Voice of the Jewish community in Cornwall Issue 15 kehillatkernow.com Elul 5766/September 2006 Summer visitors: liturgy, lecture and Limmud Harvey Kurzfield Elkan Levy, co-director of the United Synagogue Office for Small Communities, together with his wife Celia, visited our community for the weekend of 22nd July 2006. Elkan conducted the Friday night service at Milton & Glorias Harvey Kurzfield and Elkan Levy admiring the ark. This was donated by Estelle Moses, who house using the liturgy from the Singer prayer had it made up by a cabinet-maker to a design by Anne Hearle. Anne also added the Hebrew inscription, which translates as Open my heart to wisdom and understanding and made book, reawakening many memories for those the curtains which depict the stone tablets. brought up in the Orthodox tradition. Elkans enthusiasm really engaged those present and On Sunday, Elkan delivered our annual lecture book shop which elicited a great deal of interest the service was enjoyed by all. Members were at Carnon Downs Village Hall. Leslie had and generated excellent sales. also presented with copies of the The Song submitted a notice of this event to the Coracle, Elkan delivered his lecture, Cromwell and the and Spirit of Shabbat CD, a booklet for the Truro Cathedrals newsletter to all churches in rabbi with a terrific sense of drama so that Grace after Meals service and a What Will Cornwall, and this brought a welcome influx you almost felt as if you were viewing events You Do? booklet subtitled 48 things you can of visitors to the event. -

Czech-Israeli Intergovernmental Consultations Joint Statement Prague, May 17, 2012 Today, May 17, 2012, the Government of the C

Czech-Israeli Intergovernmental Consultations Joint Statement Prague, May 17, 2012 Today, May 17, 2012, the Government of the Czech Republic and the Israeli Government are holding their intergovernmental consultations in Prague. The Prime Minister of the Czech Republic, Mr. Petr Ne čas, and the Prime Minister of the State of Israel, Mr. Benjamin Netanyahu, note with satisfaction the friendship and the historical partnership between the two countries, the unrelenting reciprocal support, the mutual respect for each other's sovereign status and the joint recognition in the political, defense and economic requirements of the two countries. The Prime Ministers emphasize their aspiration to further strengthen the close relations between the two Governments and the unique ties between the two peoples, based on a thousand-year-old affinity between the Czech people and the Jewish people. The Prime Ministers wish to thank all those who work tirelessly to advance the ties between the two countries. The following are the Government members participating in the consultations: On the Czech Republic side: Prime Minister Petr Ne čas First Deputy Prime Minister and Minister of Foreign Affairs , Karel Schwarzenberg Minister of Industry and Trade, Martin Kuba Minister of Education, Youth and Sports, Petr Fiala Minister of Labor and Social Affairs, Jaromír Drábek Minister of Transport, Pavel Dobeš Minister for Regional Development, Kamil Jankovský Minister of Culture, Alena Hanáková On the Israeli side: Prime Minister Benjamin Netanyahu Deputy Prime Minister -

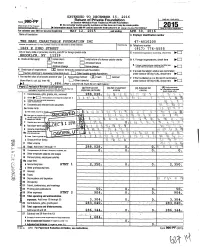

990-PF Return of Private Foundation

I EXTENDED TO DECEMBER 15, 2016 Return of Private Foundation OMB No 1545-0052 Form 990-PF or Section 4947(axl) Trust Treated as Private Foundation Depertrnent or the rreasu y Do not enter social security numbers on this form as it may be made public. 2015 Internal Revenue Service 00, Information about Form 990-PF and its separate Instructions Is at Wt ny rrs. ov/fort en o u is ns ec ion For calendar year 2015 or tax year beginning MAY 12 , 201 5 and ending APR 016 Name of foundation Employer identification number THE MARI CHARI TABLE FOUNDATION INC 47-4010200 Number and street (a P 0 box number if mail is not delivered to street address) RooMswte B Telephone number 1869 E 23RD STREET (917) 776-5555 City or town, state or province, country, and ZIP or foreign postal code C If exemption application is pending , check here ► BROOKLYN, NY 11229 G Check all that apply. XD Initial return initial return of a former public charity D 1. Foreign organizations, check here Final return Amended return 2. Foreign organizations meeting the 85% test, Address chan ge Name chan ge check here and attach computation H Check type of organization: [X Section 501(c)(3) exempt private foundation E If private foundation status was terminated Section 4947(a)( 1 ) nonexem pt charitable trust Other taxable private foundation under section 507(b)(1)(A), check here I Fair market value of all assets at end of year J Accounting method: MX Cash 0 Accrual F If the foundation is in a 60-month termination (from Part II, col. -

CONTROL of SPACE in EAST JERUSALEM Meir Margalit

SEIZING CONTROL OF SPACE IN EAST MeirJERUSALEM Margalit edited by Sam Blatt design by Virginia Paradinas Dr. Meir Margalit May 2010 Editing: Sam Blatt Graphics: Virginia Paradinas Photos: ActiveStills.org Alberto Alcalde Virginia Paradinas Legal adviser: Allegra Pacheco DVD producer: Elan Frenkel Seizing Control of Space in East Jerusalem Introduction Scope of this research The Legality of settlements UN resolutions Taking control of the space Permanent temporariness The colonial model of relationship with the “natives” Changing the landscape Policies of segregation Historical background The demographic factor AreasSEIZING appropriated by government in East Jerusalem Properties under Israeli control in East Jerusalem Institutions that control the land Seized and targeted areas in Eat Jerusalem Settler activity inside the Old City A summary of the numbers Settler activity outside the Old City Silwan/ Ir David DemolitionCONTROL plans for the Al Bustan neighbourhood of Silwan OF Old purposes, new strategies Illegal settler construction in Silwan Four cases Case 1: The “no permit” 7 – storey building Case 2: Revoking of demolition order by Justice Lahovsky Case 3: Dealing with containers, caravans and guard posts SPACECase 4: Using arab residents to buy property for settlers IN Sheikh Jarrah The grey elements of control in Sheikh Jarrah A-Tur Ras Al-Amud Abu Dis Isolated properties in other areas of East Jerusalem EASTProjects by private developers Jabel Mukaber/ Nof Zion Manipulations to erase reality Mar Elias Wallajeh/ Givat Yael The wholesale