Audit Report on the Accounts of Union Administrations District Sialkot

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Punjab Roads Component

Due Diligence Report on Social Safeguards Loan 3264-PAK: Flood Emergency Reconstruction and Resilience Project (FERRP)–Punjab Roads Component Due Diligence Report on Social Safeguards on Reconstruction of Pasrur – Narowal Road March 2017 Prepared by: Communication and Works Department, Government of the Punjab NOTES (i) The fiscal year (FY) of the Government of the Islamic Republic of Pakistan and its agencies ends on 30 June. (ii) In this report, "$" refers to US dollars. This Social Safeguards due diligence report is a document of the borrower. The views expressed herein do not necessarily represent those of ADB's Board of Directors, Management, or staff, and may be preliminary in nature. In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area. Social Due Diligence Report Document stage: Final Date: March, 2017 PAK: Flood Emergency Reconstruction and Resilience Project, Loan No. 3264 Social Due Diligence Report of Reconstruction of 28 km long Pasrur – Narowal Road from RD 0+000 to RD 28+000), District Sialkot Prepared by: Abdul Hameed, TA Resettlement Specialist for Project Implementation Unit, Communications and Works Department, Government of Punjab, Lahore. This due diligence report is a document of the borrower. The views expressed herein do not necessarily represent those of ADB's Board of -

Ethnomedicinal Profile of Flora of District Sialkot, Punjab, Pakistan

ISSN: 2717-8161 RESEARCH ARTICLE New Trend Med Sci 2020; 1(2): 65-83. https://dergipark.org.tr/tr/pub/ntms Ethnomedicinal Profile of Flora of District Sialkot, Punjab, Pakistan Fozia Noreen1*, Mishal Choudri2, Shazia Noureen3, Muhammad Adil4, Madeeha Yaqoob4, Asma Kiran4, Fizza Cheema4, Faiza Sajjad4, Usman Muhaq4 1Department of Chemistry, Faculty of Natural Sciences, University of Sialkot, Punjab, Pakistan 2Department of Statistics, Faculty of Natural Sciences, University of Sialkot, Punjab, Pakistan 3Governament Degree College for Women, Malakwal, District Mandi Bahauddin, Punjab, Pakistan 4Department of Chemistry, Faculty of Natural Sciences, University of Gujrat Sialkot Subcampus, Punjab, Pakistan Article History Abstract: An ethnomedicinal profile of 112 species of remedial Received 30 May 2020 herbs, shrubs, and trees of 61 families with significant Accepted 01 June 2020 Published Online 30 Sep 2020 gastrointestinal, antimicrobial, cardiovascular, herpetological, renal, dermatological, hormonal, analgesic and antipyretic applications *Corresponding Author have been explored systematically by circulating semi-structured Fozia Noreen and unstructured questionnaires and open ended interviews from 40- Department of Chemistry, Faculty of Natural Sciences, 74 years old mature local medicine men having considerable University of Sialkot, professional experience of 10-50 years in all the four geographically Punjab, Pakistan diversified subdivisions i.e. Sialkot, Daska, Sambrial and Pasrur of E-mail: [email protected] district Sialkot with a total area of 3106 square kilometres with ORCID:http://orcid.org/0000-0001-6096-2568 population density of 1259/km2, in order to unveil botanical flora for world. Family Fabaceae is found to be the most frequent and dominant family of the region. © 2020 NTMS. -

Audit Report on the Accounts of Union Administrations District Sialkot

AUDIT REPORT ON THE ACCOUNTS OF UNION ADMINISTRATIONS DISTRICT SIALKOT AUDIT YEAR 2016-17 AUDITOR GENERAL OF PAKISTAN TABLE OF CONTENTS ABBREVIATIONS AND ACRONYMS ................................................ i PREFACE .............................................................................................. ii EXECUTIVE SUMMARY ................................................................... iii SUMMARY OF TABLES AND CHARTS .......................................... vi Table 1: Audit Work Statistics ......................................................................vi Table 2: Audit Observations Classified by Categories ...................................vi Table 3: Outcome Statistics ..........................................................................vi Table 4: Irregularities Pointed Out ...............................................................vii Table 5: Cost – Benefit Ratio.......................................................................vii CHAPTER 1 ........................................................................................... 1 1.1 UNION ADMINISTRATIONS, DISTRICT SIALKOT ................... 1 1.1.1 INTRODUCTION ........................................................................... 1 1.1.2 Comments on Budget and Accounts (Variance Analysis) for the Financial Years 2013-16.................................................................. 2 1.1.3 Comments on Budget and Accounts (Variance Analysis) ................. 2 1.1.4 Brief Comments on the Status of Compliance with PAC/UAC Directives -

Sialkot District Reference Map September, 2014

74°0'0"E G SIALKOT DISTRICT REFBHEIMRBEER NCE MAP SEPTEMBER, 2014 Legend !> GF !> !> Health Facility Education Facility !>G !> ARZO TRUST BHU CHITTI HOSPITAL & SHEIKHAN !> MEDICAL STORE !> Sialkot City !> G Basic Health Unit !> High School !> !> !> G !> MURAD PUR BASHIR A CHAUDHARY AL-SHEIKH HOSPITAL JINNAH MEMORIAL !> MEMORIAL HOSPITAL "' CHRISTIAN HOSPITAL ÷Ó Children Hospital !> Higher Secondary IQBAL !> !> HOSPITAL !>G G DISPENSARY HOSPITAL CHILDREN !> a !> G BHAGWAL DHQ c D AL-KHIDMAT HOSPITAL OA !> SIALKOT R Dispensary AWAN BETHANIA !>CHILDREN !>a T GF !> Primary School GF cca ÷Ó!> !> A WOMEN M!>EDICAaL COMPLEX HOSPITAL HOSPITAL !> ÷Ó JW c ÷Ó !> '" A !B B D AL-SHIFA HOSPITAL !> '" E ÷Ó !> F a !> '" !B R E QURESHI HOScPITAL !> ALI HUSSAIN DHQ O N !> University A C BUKH!>ARI H M D E !>!>!> GENERAL E !> !> A A ZOHRA DISPENSARY AG!>HA ASAR HOSPITAL D R R W A !B GF L AL-KHAIR !> !> HEALTH O O A '" Rural Health Center N MEMORIAL !> HOSPITAL A N " !B R " ú !B a CENTER !> D úK Bridge 0 HOSPITAL HOSPITAL c Z !> 0 ' A S ú ' D F úú 0 AL-KHAIR aA 0 !> !>E R UR ROA 4 cR P D 4 F O W SAID ° GENERAL R E A L- ° GUJORNAT !> AD L !> NDA 2 !> GO 2 A!>!>C IQBAL BEGUM FREE DISPENSARY G '" '" Sub-Health Center 3 HOSPITAL D E !> INDIAN 3 a !> !>!> úú BHU Police Station AAMNA MEDICAL CENTER D MUGHAL HOSPIT!>AL PASRUR RD HAIDER !> !>!> c !> !>E !> !> GONDAL G F Z G !>R E PARK SIALKOT !> AF BHU O N !> AR A C GF W SIDDIQUE D E R A TB UGGOKI BHU OA L d ALI VETERINARY CLINIC D CHARITABLE BHU GF OCCUPIED !X Railway Station LODHREY !> ALI G !> G AWAN Z D MALAGAR -

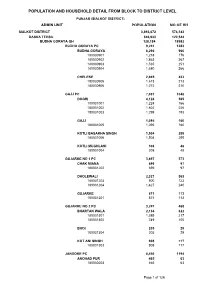

Sialkot Blockwise

POPULATION AND HOUSEHOLD DETAIL FROM BLOCK TO DISTRICT LEVEL PUNJAB (SIALKOT DISTRICT) ADMIN UNIT POPULATION NO OF HH SIALKOT DISTRICT 3,893,672 574,143 DASKA TEHSIL 846,933 122,544 BUDHA GORAYA QH 128,184 18982 BUDHA GORAYA PC 9,241 1383 BUDHA GORAYA 6,296 960 180030901 1,218 176 180030902 1,863 267 180030903 1,535 251 180030904 1,680 266 CHELEKE 2,945 423 180030905 1,673 213 180030906 1,272 210 GAJJ PC 7,031 1048 DOGRI 4,124 585 180031001 1,224 166 180031002 1,602 226 180031003 1,298 193 GAJJ 1,095 160 180031005 1,095 160 KOTLI BASAKHA SINGH 1,504 255 180031006 1,504 255 KOTLI MUGHLANI 308 48 180031004 308 48 GUJARKE NO 1 PC 3,897 573 CHAK MIANA 699 97 180031202 699 97 DHOLEWALI 2,327 363 180031203 900 123 180031204 1,427 240 GUJARKE 871 113 180031201 871 113 GUJARKE NO 2 PC 3,247 468 BHARTAN WALA 2,134 322 180031301 1,385 217 180031302 749 105 BHOI 205 29 180031304 205 29 KOT ANI SINGH 908 117 180031303 908 117 JANDOKE PC 8,450 1194 ANOHAD PUR 465 63 180030203 465 63 Page 1 of 126 POPULATION AND HOUSEHOLD DETAIL FROM BLOCK TO DISTRICT LEVEL PUNJAB (SIALKOT DISTRICT) ADMIN UNIT POPULATION NO OF HH JANDO KE 2,781 420 180030206 1,565 247 180030207 1,216 173 KOTLI DASO SINGH 918 127 180030204 918 127 MAHLE KE 1,922 229 180030205 1,922 229 SAKHO KE 2,364 355 180030201 1,250 184 180030202 1,114 171 KANWANLIT PC 16,644 2544 DHEDO WALI 6,974 1092 180030305 2,161 296 180030306 1,302 220 180030307 1,717 264 180030308 1,794 312 KANWAN LIT 5,856 854 180030301 2,011 290 180030302 1,128 156 180030303 1,393 207 180030304 1,324 201 KOTLI CHAMB WALI -

Flood Emergency Reconstruction and Resilience Project, Loan No. 3264

Due Diligence Report on Social Safeguards Loan 3264-PAK: Flood Emergency Reconstruction and Resilience Project (FERRP)–Punjab Roads Component Due Diligence Report on Social Safeguards on Reconstruction of Daska – Pasrur Road March 2017 Prepared by: Communication and Works Department, Government of the Punjab NOTES (i) The fiscal year (FY) of the Government of the Islamic Republic of Pakistan and its agencies ends on 30 June. (ii) In this report, "$" refers to US dollars. This Social Safeguards due diligence report is a document of the borrower. The views expressed herein do not necessarily represent those of ADB's Board of Directors, Management, or staff, and may be preliminary in nature. In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area. GOVERNMENT OF THE PUNJAB COMMUNICATION & WORKS DEPARTMENT Flood Emergency Reconstruction and Resilience Project (FERRP) Social Due Diligence Report of Reconstruction of Daska- Pasrur Road (RD 0+000 – RD 30+000) March, 2017 Prepared by TA Resettlement Specialist for Communication and Works Department, Government of Punjab, Lahore Table of Contents CHAPTER 1 INTRODUCTION ................................................................................................................... 1 A. Background: ............................................................................................................. -

Tranche 3: Biannual Environmental Monitoring Report, GEPCO

Environmental Monitoring Report __________________________________________ Bi-annual Environmental Monitoring Report Jul - Dec 2017 January 2018 PAK: Power Distribution Enhancement Investment Program, Tranche 3 Prepared by Gujranwala Electric Power Company (GEPCO) for the Asian Development Bank NOTES (i) The fiscal year (FY) of the Government of the Islamic Republic of Pakistan and its agencies ends on 30 June. (ii) In this report “$” refer to US dollars. This environmental monitoring report is a document of the borrower. The views expressed herein do not necessarily represent those of ADB’s Board of Directors, Management, or staff, and may be preliminary in nature. In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area. Bi-annual Environmental Monitoring Report ___________________________________________________________________________ Project Number: 2972-PAK July-December 2017 Pakistan Power Distribution Enhancement Investment Program-Multi-Tranche Financing Facility-Tranche-3) For period: July-December 2017 (Financed by the Asian Development Bank) Prepared By: Assistant Manager (Environment) PMU, GEPCO Gujranwala Electric Power Company (GEPCO) PMU Section 565-A Model Town G.T Road Gujranwala, Pakistan. Executing Agency (EA) Pakistan Electric Power Company (PEPCO) Implementing Agency (IA) GEPCO -

Diversity and Distribution of Dragonfly in District Sialkot, Punjab, Pakistan

Pure Appl. Biol., 10(4):988-994, December, 2021 http://dx.doi.org/10.19045/bspab.2021.100103 Research Article Diversity and distribution of Dragonfly in District Sialkot, Punjab, Pakistan Burhan Hafeez1*, Muhammad Faheem Malik1, Waqas Asghar1, Rabia Shabbir1, Isba Latif1, Aqsa Jabeen1, Hira Basit1 and Farwa Ghafoor1 1. Department of Zoology, University of Gujrat, Gujrat, Punjab-Pakistan *Corresponding author’s email: [email protected] Citation Burhan Hafeez, Muhammad Faheem Malik, Waqas Asghar, Rabia Shabbir, Isba Latif, Aqsa Jabeen, Hira Basit and Farwa Ghafoor. Diversity and distribution of Dragonfly in District Sialkot, Punjab, Pakistan. Pure and Applied Biology. Vol. 10, Issue 4, pp988-994. http://dx.doi.org/10.19045/bspab.2021.100103 Received: 07/10/2020 Revised: 18/12/2020 Accepted: 31/12/2020 Online First: 05/01/2021 Abstract The present research was organized with the objective to explore the diversity and distribution of dragonfly (Odonata; Insecta) in district Sialkot, Punjab, Pakistan. The capturing was done during 2019 from 16 chosen localities of all four tehsils including Sialkot, Sambrial, Daska and Pasroor. Total of 185 specimens of dragonfly was captured with the help of sweep nets and handpicking. Identified specimens up to species level and then preserved. There are 10 species of dragonfly belonging to 7 genera and 2 families pinpointed from collected data. Pantala flavescens, Crocothemis erythraea, Crocothemis survilia, Neurothemis fluctuans, Acisoma panorpoids, Acisoma variegatum, Orthetrum pruinosum, Orthetrum sabina which comes under Pantala, Crocothemis, Ascisoma, Neurorothemis and Orthetrum genera of family Libellulidae. The prevailing 2 species, Anax indicus and Hemianax ephippiger come under Anax and Hemianax genera of family Aeshnidae. -

Data Collection Survey on Infrastructure Improvement of Energy Sector in Islamic Republic of Pakistan

←ボックス隠してある Pakistan by Japan International Cooperation Agency (JICA) Data Collection Survey on Infrastructure Improvement of Energy Sector in Islamic Republic of Pakistan Data Collection Survey ←文字上 / 上から 70mm on Infrastructure Improvement of Energy Sector in Pakistan by Japan International Cooperation Agency (JICA) Final Report Final Report February 2014 February 2014 ←文字上 / 下から 70mm Japan International Cooperation Agency (JICA) Nippon Koei Co., Ltd. 4R JR 14-020 ←ボックス隠してある Pakistan by Japan International Cooperation Agency (JICA) Data Collection Survey on Infrastructure Improvement of Energy Sector in Islamic Republic of Pakistan Data Collection Survey ←文字上 / 上から 70mm on Infrastructure Improvement of Energy Sector in Pakistan by Japan International Cooperation Agency (JICA) Final Report Final Report February 2014 February 2014 ←文字上 / 下から 70mm Japan International Cooperation Agency (JICA) Nippon Koei Co., Ltd. 4R JR 14-020 Data Collection Survey on Infrastructure Improvement of Energy Sector in Pakistan Final Report Location Map Islamabad Capital Territory Punjab Province Islamic Republic of Pakistan Sindh Province Source: Prepared by the JICA Survey Team based on the map on http://www.freemap.jp/. February 2014 i Nippon Koei Co., Ltd. Data Collection Survey on Infrastructure Improvement of Energy Sector in Pakistan Final Report Summary Objectives and Scope of the Survey This survey aims to collect data and information in order to explore the possibility of cooperation with Japan for the improvement of the power sector in Pakistan. The scope of the survey is: Survey on Pakistan’s current power supply situation and review of its demand forecast; Survey on the power development policy, plan, and institution of the Government of Pakistan (GOP) and its related companies; Survey on the primary energy in Pakistan; Survey on transmission/distribution and grid connection; and Survey on activities of other donors and the private sector. -

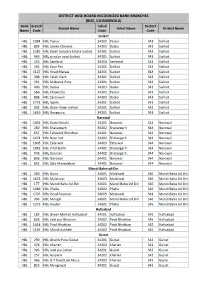

District Wise Board Recognized Bank Branches

DISTRICT WISE BOARD RECOGNIZED BANK BRANCHES (BISE, GUJRANWALA) Bank Branch Tehsil District Branch Name Tehsil Name District Name Name Code Code Code Sialkot HBL 1084 HBL Pasrur 34302 Pasrur 343 Sialkot HBL 895 HBL Jamke Cheema 34303 Daska 343 Sialkot HBL 1285 HBL Small Industry Estate Sialkot 34301 Sialkot 343 Sialkot HBL 969 HBL circular road Sialkot 34301 Sialkot 343 Sialkot HBL 425 HBL Sambrial 34304 Sambrial 343 Sialkot HBL 492 HBL Koor Pur 34301 Sialkot 343 Sialkot HBL 1127 HBL Head Marala 34301 Sialkot 343 Sialkot HBL 308 HBL Fateh Garh 34301 Sialkot 343 Sialkot HBL 291 HBL Mubarak Pura 34301 Sialkot 343 Sialkot HBL 406 HBL Daska 34303 Daska 343 Sialkot HBL 566 HBL Chawinda 34302 Pasrur 343 Sialkot HBL 808 HBL Saranwali 34303 Daska 343 Sialkot HBL 1773 HBL Ugoki 34301 Sialkot 343 Sialkot HBL 992 HBL Bazar Kalan Sialkot 34301 Sialkot 343 Sialkot HBL 1619 HBL Rungpura 34301 Sialkot 343 Sialkot Narowal HBL 1405 HBL Bado Malahi 34401 Narowal 344 Narowal HBL 260 HBL Shakargarh 34402 Shakargarh 344 Narowal HBL 637 HBL Talwandi Bhindran 34401 Narowal 344 Narowal HBL 1474 HBL Noor kot 34402 Shakargarh 344 Narowal HBL 1805 HBL Zafarwal 34403 Zafarwal 344 Narowal HBL 1842 HBL Pindi Bohri 34401 Shakargarh 344 Narowal HBL 978 HBL Darman 34402 Shakargarh 344 Narowal HBL 836 HBL Narowal 34401 Narowal 344 Narowal HBL 852 HBL Qila Ahmedabad 34401 Narowal 344 Narowal Mandi Baha-ud-Din HBL 560 HBL Gojra 34601 Malakwal 346 Mandi Baha Ud Din HBL 1623 HBL Malakwal 34603 Malakwal 346 Mandi Baha Ud Din HBL 177 HBL Mandi Baha Ud Din 34601 Mandi Baha Ud -

List of Branches Authorized for Overnight Clearing (Annexure - II) Branch Sr

List of Branches Authorized for Overnight Clearing (Annexure - II) Branch Sr. # Branch Name City Name Branch Address Code Show Room No. 1, Business & Finance Centre, Plot No. 7/3, Sheet No. S.R. 1, Serai 1 0001 Karachi Main Branch Karachi Quarters, I.I. Chundrigar Road, Karachi 2 0002 Jodia Bazar Karachi Karachi Jodia Bazar, Waqar Centre, Rambharti Street, Karachi 3 0003 Zaibunnisa Street Karachi Karachi Zaibunnisa Street, Near Singer Show Room, Karachi 4 0004 Saddar Karachi Karachi Near English Boot House, Main Zaib un Nisa Street, Saddar, Karachi 5 0005 S.I.T.E. Karachi Karachi Shop No. 48-50, SITE Area, Karachi 6 0006 Timber Market Karachi Karachi Timber Market, Siddique Wahab Road, Old Haji Camp, Karachi 7 0007 New Challi Karachi Karachi Rehmani Chamber, New Challi, Altaf Hussain Road, Karachi 8 0008 Plaza Quarters Karachi Karachi 1-Rehman Court, Greigh Street, Plaza Quarters, Karachi 9 0009 New Naham Road Karachi Karachi B.R. 641, New Naham Road, Karachi 10 0010 Pakistan Chowk Karachi Karachi Pakistan Chowk, Dr. Ziauddin Ahmed Road, Karachi 11 0011 Mithadar Karachi Karachi Sarafa Bazar, Mithadar, Karachi Shop No. G-3, Ground Floor, Plot No. RB-3/1-CIII-A-18, Shiveram Bhatia Building, 12 0013 Burns Road Karachi Karachi Opposite Fresco Chowk, Rambagh Quarters, Karachi 13 0014 Tariq Road Karachi Karachi 124-P, Block-2, P.E.C.H.S. Tariq Road, Karachi 14 0015 North Napier Road Karachi Karachi 34-C, Kassam Chamber's, North Napier Road, Karachi 15 0016 Eid Gah Karachi Karachi Eid Gah, Opp. Khaliq Dina Hall, M.A. -

Flood Emergency Reconstruction and Resilience Project Project

Flood Emergency Reconstruction and Resilience Project (RRP PAK 49038) Project Administration Manual Project Number: 49038-001 Loan and Technical Assistance Numbers: {LXXXX; TAXXXX} June 2015 Islamic Republic of Pakistan: Flood Emergency Reconstruction and Resilience Project i Project Administration Manual Purpose and Process The project administration manual (PAM) describes the essential administrative and management requirements to implement the project on time, within budget, and in accordance with Government and Asian Development Bank (ADB) policies and procedures. The PAM should include references to all available templates and instructions either through linkages to relevant URLs or directly incorporated in the PAM. The executing and implementing agencies are wholly responsible for the implementation of ADB financed projects, as agreed jointly between the borrower and ADB, and in accordance with Government and ADB’s policies and procedures. ADB staff is responsible to support implementation including compliance by executing and implementing agencies of their obligations and responsibilities for project implementation in accordance with ADB’s policies and procedures. At Loan Negotiations the borrower and ADB shall agree to the PAM and ensure consistency with the Loan and Project agreements. Such agreement shall be reflected in the minutes of the Loan Negotiations. In the event of any discrepancy or contradiction between the PAM and the Loan and Project Agreements, the provisions of the Loan and Project Agreements shall prevail. After ADB Board approval of the project's report and recommendations of the President (RRP) changes in implementation arrangements are subject to agreement and approval pursuant to relevant Government and ADB administrative procedures (including the Project Administration Instructions) and upon such approval they will be subsequently incorporated in the PAM.