RBC LPIM Canadian Technical and Quantitative Total Return Securities

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Notice of 2009 Annual Meeting of Shareholders And

NOTICE OF 2009 ANNUAL MEETING OF SHAREHOLDERS AND MANAGEMENT PROXY CIRCULAR WHAT'S INSIDE NOTICE OF 2009 ANNUAL SHAREHOLDER MEETING ...................................................................................... 2 MANAGEMENT PROXY CIRCULAR ...................................................................................................................... 3 VOTING YOUR SHARES........................................................................................................................................... 4 BUSINESS OF THE MEETING................................................................................................................................ 10 THE NOMINATED DIRECTORS............................................................................................................................. 12 STATEMENT OF GOVERNANCE PRACTICES.................................................................................................... 19 COMMITTEES........................................................................................................................................................... 24 COMPENSATION OF CERTAIN EXECUTIVE OFFICERS .................................................................................. 29 AIR CANADA'S EXECUTIVE COMPENSATION PROGRAM............................................................................. 34 PERFORMANCE GRAPHS ...................................................................................................................................... 39 OTHER IMPORTANT -

THE ROYAL INSTITUTION for the ADVANCEMENT of LEARNING/Mcgill UNIVERSITY

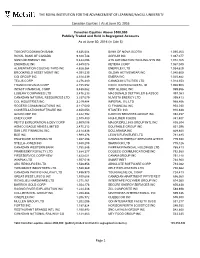

THE ROYAL INSTITUTION FOR THE ADVANCEMENT OF LEARNING/McGILL UNIVERSITY Canadian Equities │ As at June 30, 2016 Canadian Equities Above $500,000 Publicly Traded and Held in Segregated Accounts As at June 30, 2016 (in Cdn $) TORONTO DOMINION BANK 9,836,604 BANK OF NOVA SCOTIA 1,095,263 ROYAL BANK OF CANADA 9,328,748 AGRIUM INC 1,087,077 SUNCOR ENERGY INC 5,444,096 ATS AUTOMATION TOOLING SYS INC 1,072,165 ENBRIDGE INC 4,849,078 KEYERA CORP 1,067,040 ALIMENTATION COUCHE-TARD INC 4,628,364 ENERFLEX LTD 1,054,629 BROOKFIELD ASSET MGMT INC 4,391,535 GILDAN ACTIVEWEAR INC 1,040,600 CGI GROUP INC 4,310,339 EMERA INC 1,025,882 TELUS CORP 4,276,480 CANADIAN UTILITIES LTD 1,014,353 FRANCO-NEVADA CORP 4,155,552 EXCO TECHNOLOGIES LTD 1,008,903 INTACT FINANCIAL CORP 3,488,562 WSP GLOBAL INC 999,856 LOBLAW COMPANIES LTD 3,476,233 MACDONALD DETTWILER & ASSOC 997,083 CANADIAN NATURAL RESOURCES LTD 3,337,079 NUVISTA ENERGY LTD 995,413 CCL INDUSTRIES INC 3,219,484 IMPERIAL OIL LTD 968,856 ROGERS COMMUNICATIONS INC 3,117,080 CI FINANCIAL INC 954,030 CONSTELLATION SOFTWARE INC 2,650,053 STANTEC INC 910,638 GOLDCORP INC 2,622,792 CANYON SERVICES GROUP INC 892,457 ONEX CORP 2,575,400 HIGH LINER FOODS 841,407 PEYTO EXPLORATION & DEV CORP 2,509,098 MAJOR DRILLING GROUP INTL INC 838,304 AGNICO EAGLE MINES LIMITED 2,475,212 EQUITABLE GROUP INC 831,396 SUN LIFE FINANCIAL INC 2,414,836 DOLLARAMA INC 829,840 BCE INC 1,999,278 LEON'S FURNITURE LTD 781,495 ENGHOUSE SYSTEMS LTD 1,867,298 CANADIAN ENERGY SERVICES &TECH 779,690 STELLA-JONES INC 1,840,208 SHAWCOR LTD 775,126 -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

13 March 2003 Mr. Alex Himelfarb Clerk of the Privy Council and Secretary to the Cabinet

13 March 2003 Mr. Alex Himelfarb Clerk of the Privy Council and Secretary to the Cabinet Langevin Block 80 Wellington Street Ottawa, Ontario K1A 0A3 Bernard A. Courtois Executive Counsel Dear Mr. Himelfarb: BCE & Bell Canada Subject: Canada Gazette – Notice No. DGTP-001-03 Petition to the Governor in Council from Quebecor Média inc. under Section 12 of the Telecommunications Act in regard to the following CRTC Decision: Quebecor Média inc. – Alleged anti-competitive cross-subsidization of Bell ExpressVu, Telecom Decision CRTC 2002-61 These comments are filed on behalf of BCE Inc. and Bell Canada in response to the petition by Quebecor Média inc. (“Quebecor”) to the Governor in Council regarding Telecom Decision CRTC 2002-61 (“the Decision”). In its application of 4 April 2002, filed with the CRTC pursuant to Part VII of the CRTC Telecommunications Rules of Procedure, Quebecor alleged that BCE has been using profits generated by Bell Canada to anti-competitively cross-subsidize the entry of Bell ExpressVu Limited Partnership (“ExpressVu”) into the Quebec broadcasting distribution market. Quebecor argued that mechanisms put in place by the Commission to prevent cross-subsidization of ExpressVu by Bell Canada be activated in order to prevent Bell Canada, the dominant player in local telephone service, from becoming the dominant broadcasting distribution undertaking (“BDU”). In its Decision of 8 October 2002, the Commission found that Bell Canada was not, in fact, inappropriately cross-subsidizing ExpressVu, and furthermore, that ExpressVu was not the dominant BDU that Quebecor warned about: [T]he Commission remains of the view that the existing mechanisms, including those recently modified in Decision 2002- 34, are appropriate and sufficient to prevent inappropriate cross- subsidization of ExpressVu by Bell Canada, at the expense of users of telecommunications services. -

Form 20-F Quebecor Media Inc

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 20-F REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR _ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2017 OR TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to OR SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of event requiring this shell company report ... ... For the transition period from to Commission file number: 333-13792 QUEBECOR MEDIA INC. (Exact name of Registrant as specified in its charter) Province of Québec, Canada (Jurisdiction of incorporation or organization) 612 St-Jacques Street Montréal, Québec, Canada H3C 4M8 (Address of principal executive offices) Securities registered or to be registered pursuant to Section 12(b) of the Act. Title of each class Name of each exchange on which registered None None Securities registered or to be registered pursuant to Section 12(g) of the Act. None (Title of Class) Table of Contents Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act. 5¾% Senior Notes due January 2023 (Title of Class) Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report. 95,441,277 Common Shares Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. -

Investor Presentation

Videotron Ltd. / Vidéotron Ltée Investor Education Presentation May / June 2021 Strictly Private & Confidential 1 Cautionary Statements General This presentation does not constitute or form part of an offer to sell or the solicitation of an offer to purchase any securities in any jurisdiction. No securities commission or similar authority of the United States, Canada or any other jurisdiction has reviewed or in any way passed upon this document or the merits of the securities described herein, and any representation to the contrary is an offence. Forward Looking Statement This presentation contains forward-looking statements, which are subject to known and unknown risks and uncertainties that could cause Videotron Ltd’s (“Videotron’s”) and Quebecor Media Inc.’s (“QMI’s” and together with Videotron, “the Company’s”) actual results to differ materially from those set forth in the forward-looking statements. These risks include changes in customer demand for the Company's products, changes in raw material and equipment costs and availability, seasonal fluctuations in customer orders, pricing actions by competitors, and general changes in the economic environment. For additional information on such risks and uncertainties relating to the Company, you can consult QMI’s and Videotron’s Annual Reports on Form 20F which have been filed with the SEC. Except as may be required by applicable securities laws, we do not undertake any obligation to update any forward looking statement, whether as a result of new information, future events or otherwise. Presentation of Financial Information On January 1, 2019, the Company adopted the new rules under IFRS 16 standards. Accordingly, the financial results for the periods ending after January 1, 2019 (and, for comparative purposes, the financial results for the years ended December 31, 2016, 2017 and 2018) presented herein were prepared in accordance with IFRS 16. -

DFA Canada Canadian Vector Equity Fund - Class a As of July 31, 2021 (Updated Monthly) Source: RBC Holdings Are Subject to Change

DFA Canada Canadian Vector Equity Fund - Class A As of July 31, 2021 (Updated Monthly) Source: RBC Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. Your use of this website signifies that you agree to follow and be bound by the terms and conditions of -

ANNUAL INFORMATION FORM of METRO INC. Year Ended September 25, 2010

ANNUAL INFORMATION FORM OF METRO INC. Year ended September 25, 2010 DECEMBER 10, 2010 Table of contents 1. Incorporation 1 1.1 Incorporation of the Issuer 1 1.2 Subsidiaries 1 2. General Development of the Business over the Past Three Years 2 3. Description of the Business 3 3.1 Business of the Company 3 3.2 Clients and Suppliers 4 3.3 Human Resources 5 3.4 Trademarks and Trade Names 5 3.5 Social and Environmental Policies 5 3.6 Research and Development 5 3.7 Regulations 6 3.8 Loan Operations 6 3.9 Reorganizations 6 3.10 Risk Factors 6 4. Dividends 6 5. Share Capital Structure 7 6. Market for Securities 8 6.1 Trading Price and Volume 8 6.2 Credit Ratings and Debts 8 6.3 Prior Sales 9 7. Escrowed Securities and Securities Subject to Contractual Restriction on Transfer 9 8. Directors and Officers 10 8.1 Name, Occupation and Security Holding 10 8.2 Cease Trade Orders, Bankruptcies, Penalties or Sanctions 12 8.3 Conflict of Interest 13 9. Legal Proceedings 14 10. Persons with an Interest in Material Transactions 14 11. Transfer Agent and Registrar 14 12. Material Contracts 14 13. Interest of Experts 14 13.1 Name of Experts 14 13.2 Interest of the Company’s External Auditors 14 14. Information on the Audit Committee 14 15. Additional Information 14 SCHEDULE A Information on the Audit Committee 16 SCHEDULE B Mandate of the Audit Committee 18 N.B.: All disclosures in this Annual Information Form are as at September 25, 2010 unless otherwise indicated. -

Women in Leadership at S&P/Tsx Companies

WOMEN IN LEADERSHIP AT S&P/TSX COMPANIES Women in Leadership at WOMEN’S S&P/TSX Companies ECONOMIC Welcome to the first Progress Report of Women on Boards and Executive PARTICIPATION Teams for the companies in the S&P/TSX Composite Index, the headline AND LEADERSHIP index for the Canadian equity market. This report is a collaboration between Catalyst, a global nonprofit working with many of the world’s leading ARE ESSENTIAL TO companies to help build workplaces that work for women, and the 30% Club DRIVING BUSINESS Canada, the global campaign that encourages greater representation of PERFORMANCE women on boards and executive teams. AND ACHIEVING Women’s economic participation and leadership are essential to driving GENDER BALANCE business performance, and achieving gender balance on corporate boards ON CORPORATE and among executive ranks has become an economic imperative. As in all business ventures, a numeric goal provides real impetus for change, and our BOARDS collective goal is for 30% of board seats and C-Suites to be held by women by 2022. This report offers a snapshot of progress for Canada’s largest public companies from 2015 to 2019, using the S&P/TSX Composite Index, widely viewed as a barometer of the Canadian economy. All data was supplied by MarketIntelWorks, a data research and analytics firm with a focus on gender diversity, and is based on a review of 234 S&P/TSX Composite Index companies as of December 31, 2019. The report also provides a comparative perspective on progress for companies listed on the S&P/TSX Composite Index versus all disclosing companies on the TSX itself, signalling the amount of work that still needs to be done. -

ANNUAL INFORMATION FORM Year Ended December 31, 2019

SNC-LAVALIN GROUP INC. ANNUAL INFORMATION FORM Year Ended December 31, 2019 February 27, 2020 TABLE OF CONTENTS INTERPRETATION .................................................................................................................................... 3 CAUTION REGARDING FORWARD-LOOKING STATEMENTS ................................................................... 3 1. CORPORATE STRUCTURE ........................................................................................................... 5 1.1 INCORPORATION OF THE COMPANY .............................................................................. 5 1.2 SUBSIDIARIES, JOINT ARRANGEMENTS AND ASSOCIATES .............................................. 5 2. GENERAL DEVELOPMENT OF THE BUSINESS ............................................................................. 7 3. DESCRIPTION OF THE BUSINESS .............................................................................................. 11 3.1 GENERAL ....................................................................................................................... 11 3.2 REVENUE BACKLOG ....................................................................................................... 14 3.3 RISK FACTORS ................................................................................................................ 14 3.4 NUMBER OF EMPLOYEES .............................................................................................. 14 3.5 SOCIAL AND OTHER IMPORTANT POLICIES: THE VALUES THAT GUIDE US ................. -

Proxy Circular and Navigation and Task Buttons Notice of Annual Meeting of Shareholders

Welcome to SNC-Lavalin’s Management Proxy Circular and Navigation and Task buttons Notice of Annual Meeting of Shareholders. This pdf version of the Circular has been enhanced with navigation and Close Document task buttons to help you navigate through the document and Search find the information you want more quickly. The table of contents and URLs link to pages and sections within the document as well Print as to outside websites. The task buttons provide quick access to Save to Disk search, print, save to disk and view options, but may not work on all browsers or tablets. Two Page View Single Page View Table of Contents Next Page Previous Page Last Page Visited Table of Contents INVITATION TO SHAREHOLDERS 3 / NOTICE OF 2018 ANNUAL MEETING OF SHAREHOLDERS AND NOTICE OF AVAILABILITY OF MEETING MATERIALS 4 / VOTING INFORMATION 6 / BUSINESS OF THE 2018 ANNUAL MEETING OF SHAREHOLDERS 9 / INFORMATION ON OUR DIRECTOR NOMINEES 11 / DIRECTORS’ COMPENSATION DISCUSSION AND ANALYSIS 18 / BOARD COMMITTEE REPORTS 22 / EXECUTIVE COMPENSATION DISCUSSION AND ANALYSIS 29 / STATEMENT OF CORPORATE GOVERNANCE PRACTICES 50 / OTHER INFORMATION 63 / SCHEDULE A – SHAREHOLDER PROPOSALS 64 / SCHEDULE B – MANDATE OF THE BOARD OF DIRECTORS 67 / SCHEDULE C – SUMMARY OF LEGACY LONG-TERM INCENTIVE PLANS 70 Glossary of Terms AIF Annual Information Form Executive Committee A committee established by AIP Annual Incentive Plan management comprised of the President and CEO and eleven (11) other Senior Officers Atkins WS Atkins plc G&E Committee Governance and Ethics Committee -

Annual Information Form 2019

MTY FOOD GROUP INC. 8210 Trans-Canada Road St-Laurent, Quebec, H4S 1M5 Annual Information Form For the year ended November 30, 2019 February 23, 2020 TABLE OF CONTENTS PRELIMINARY NOTES AND CAUTIONARY STATEMENT .......................................... 5 CORPORATE STRUCTURE .......................................................................................... 6 Name, Address and Incorporation of the Company ...................................................................... 6 Intercorporate Relationships ............................................................................................................. 7 GENERAL DEVELOPMENT OF THE BUSINESS ......................................................... 7 Recent events ................................................................................................................................... 7 3 Year History .................................................................................................................................... 7 DESCRIPTION OF THE BUSINESS OF THE COMPANY ............................................. 9 Overview ............................................................................................................................................. 9 Restaurant Industry ....................................................................................................................... 10 Development of the Business ..................................................................................................... 11 System Sales ..................................................................................................................................