Peoplefund (CDC) 504 Checklist and Loan Application

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Financing Your Business Financial Options and Funding Sources

FINANCING YOUR BUSINESS Financial Options and Funding Sources 25 • Financing Options » SBA’s Loan Guaranty Programs 26 » Commercial Loans 29 » SBA Micro Lenders 29 30 • Funding Sources » Arizona’s Incentives, Programs and Grants 31 » Funding for Innovation and Technology Companies 32 While every effort has been made to ensure the reliability of the information presented in this publication, the Arizona Commerce Authority cannot guarantee the accuracy of this information due to the fact that much of the information is created by external sources. Changes/updates brought to the attention of the Arizona Commerce Authority and verified will be corrected in future editions. 3 The Access to Capital Academy presented by the Phoenix Community & Economic Development and Investment Corporation (PCDIC) – helps entrepreneurs learn how to approach potential lenders with confidence and an increased chance at securing loans. 24 AZ EE FINANCING OPTIONS FI NAN CI NG YOUR There are several sources to consider when looking for three years of business tax returns, etc.) and financing. It is important to explore all of your options prospective (projections) basis. before making a decision. Collateral – property pledged by a borrower to protect the interest of the lender. By putting up collateral, you B The primary source of capital for most new businesses US show that you are committed to the success of your come from personal savings and other forms of personal I NESS resources such as friends and family, when starting out. business. While credit cards often are used to finance business A financial institution avoids making loans without needs, there may be better options available, even for F collateral. -

Personal Vs. Business Credit

The Keys to Successful Small Business Ownership, Finance and Credit™ Client Curriculum - Personal vs. Business Credit Small Business Owner Financial With financial support from: Education brought to you by: Sharpen Your Financial Focus® The Keys to Successful Small Business Ownership, Finance and Credit™ National Foundation for Credit Counseling® (NFCC®) - Small Business Owner Counseling Program Client Workbook Version 6.0 March 26, 2018 INTRODUCTION Welcome! It is our goal you find this material helpful as it was hand selected to address some of the most common challenges faced by the self-employed or small business owners. We aim for this content to complement budget counseling sessions for people like you engaged with a member agency of the National Foundation for Credit Counseling® (NFCC®) across the U.S. Whether you just started on a self-employment journey, have a business on the side or have dreams of serving millions, you are important to our national economy and local community by creating a job for yourself or others. It is our hope this program empowers you to make informed decisions about being self-employed and a small business owner by providing you access to a NFCC counselor, information, resources, and tools. As you develop a greater understanding of personal and business finance best practices, you can choose the best course of action to meet your goals. We would like to thank and acknowledge TD Bank, America’s Most Convenient Bank®, and the TD Charitable Foundation, the charitable giving arm of TD Bank, for their support of the NFCC Small Business Owner Financial Counseling and Education Program supporting Small Business Owner Financial Wellness. -

Can I Qualify for a Business Loan SBDC

Can I Qualify for a Business Loan? Whether you are applying for an SBA loan or a traditional bank loan, there are certain factors that improve your ability to obtain financing. This self-test is designed to assist you in understanding important issues that lenders consider when making a decision on a small business loan. Do you have a good personal credit history? Research indicates that good personal credit history is one of the most important factors in identifying borrowers that will repay their business loans. When a lender makes a decision on a small business loan, he/she will consider the personal credit history of the borrower. A bad credit history can be the basis for denial for a small business loan. a) If you do not have a recent credit report, find out about ordering one by go to the following web site: http://www.ftc.gov/freereports You can also contact the individual organizations: TransUnion (www.transunion.com), Experian (www.experian.com), or Equifax (www.equifax.com). If you have credit problems but they can be explained by a one-time incident such as a medical problem, provide specific information, as an addendum to your loan proposal, to a potential lender about the problem and how it has been rectified. b) If you have filed for bankruptcy in the past 7 years (10 yrs for an SBA loan), or have slow payments, collections, etc. then it may be difficult to obtain financing now. If your poor credit history can be explained by a particular incident, supply information on the situation and how you attempted to repair past credit problems. -

Corporate Bonds and Debentures

Corporate Bonds and Debentures FCS Vinita Nair Vinod Kothari Company Kolkata: New Delhi: Mumbai: 1006-1009, Krishna A-467, First Floor, 403-406, Shreyas Chambers 224 AJC Bose Road Defence Colony, 175, D N Road, Fort Kolkata – 700 017 New Delhi-110024 Mumbai Phone: 033 2281 3742/7715 Phone: 011 41315340 Phone: 022 2261 4021/ 6237 0959 Email: [email protected] Email: [email protected] Email: [email protected] Website: www.vinodkothari.com 1 Copyright & Disclaimer . This presentation is only for academic purposes; this is not intended to be a professional advice or opinion. Anyone relying on this does so at one’s own discretion. Please do consult your professional consultant for any matter covered by this presentation. The contents of the presentation are intended solely for the use of the client to whom the same is marked by us. No circulation, publication, or unauthorised use of the presentation in any form is allowed, except with our prior written permission. No part of this presentation is intended to be solicitation of professional assignment. 2 About Us Vinod Kothari and Company, company secretaries, is a firm with over 30 years of vintage Based out of Kolkata, New Delhi & Mumbai We are a team of qualified company secretaries, chartered accountants, lawyers and managers. Our Organization’s Credo: Focus on capabilities; opportunities follow 3 Law & Practice relating to Corporate Bonds & Debentures 4 The book can be ordered by clicking here Outline . Introduction to Debentures . State of Indian Bond Market . Comparison of debentures with other forms of borrowings/securities . Types of Debentures . Modes of Issuance & Regulatory Framework . -

The Arundel Business Loan Fund

Anne Arundel Economic Development Corporation Economic Development Revenue Bonds The ABL Fund is a viable non-bank alternative source of financing ready and Anne Arundel County encourages private- able to assist small businesses in Anne sector financing for economic development Arundel County. The ABL Fund’s partners projects through the issuance of private are: the U.S. Small Business Administration, The Arundel Business activity revenue bonds. Tax-exempt bonds the Maryland Industrial Development Loan Fund Financing Authority (MIDFA), The Maryland provide access to long term capital markets an SBA Lender for fixed-asset financing at tax-exempt Small Business Development Financing rates. Federal tax law limits eligibility to Authority (MSBDFA) and 19 banks Guidelines for a Small Business Loan • Bank of America • Bay Bank • Branch Banking & Trust (BB&T) • Essex Bank • First Mariner Bank • First National Bank • M&T Bank • Old Line Bank • PNC Bank manufacturing facilities, 501(c)(3) non- • Howard Bank profit organizations, and certain energy • Revere Bank projects. Additional limitations apply, • SECU depending on the specific transaction. • Sandy Spring Bank • Severn Savings Bank Most importantly, you have a • SunTrust Bank resource at AAEDC. Contact us • TD Bank with questions and for details. • The Bank of Glen Burnie • The Columbia Bank The Anne Arundel Economic Development Corporation mission is to serve business needs and to increase Anne Arundel County’s economic base through job growth and investment. For more information about the -

Business Financing Opportunities

1st Stop Business Connection www.development.ohio.gov/onestop Revised 08/012010 Business Financing Opportunities Table of Contents Sections Page Number Money 2 -Calculate how much you need Financing 3 - 4 -Types of financing -Business and loan proposals Glossary of Business Terms 5 -A head start on your business vocabulary Federal Loan Programs 6 - 11 State Loan Programs 12 – 17 State Energy Programs 18 - 20 Small Business Development Center Directory 21 -Find the SBDC nearest to you 1 MONEY One of the toughest parts of starting a small business is finding the necessary capital. In other words: Where do you find the money? This publication will help you figure out where to find the money you need to start and run a small business. First, you must know how much money you'll need. Write down the equipment you have and the equipment and inventory you need. How much will it cost to buy or lease the equipment and inventory? Equipment you already have Equipment and inventory you must purchase or lease Cost _______________________ ___________________________________________ $___________ _______________________ ___________________________________________ $___________ _______________________ ___________________________________________ $___________ _______________________ ___________________________________________ $___________ _______________________ ___________________________________________ $___________ TOTAL $ __________ Now, it's time to estimate how much it will cost to keep your business running: Business space $______________________________ -

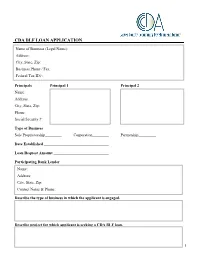

Cda Blf Loan Application

CDA BLF LOAN APPLICATION NameName of of Business Business (Legal (Legal Name): Name): Address:Address: City,City, State, State, Zip: Zip: BusinessBusiness Phone Phone / / Fax: Fax: FederalFederal Tax Tax ID ID#: #: Principals Principal 1 Principal 2 Name: Address: City, State, Zip: Phone: Social Security #: Type of Business Sole Proprietorship Corporation Partnership Date Established Loan Request Amount Participating Bank Lender Name:Name: Address:Address: City,City, State, State, Zip: Zip: ContactContact Person: Name & Phone: Contact Phone: Describe the type of business in which the applicant is engaged. Describe project for which applicant is seeking a CDA BLF loan. 1 EXISTING BUSINESS FINANCING OBLIGATIONS (Date of most recent balance sheet) ORIGINAL AMOUNT/ PRESENT MATURITY INTEREST MONTHLY PAYMENT CREDITOR NAME DATE BALANCE DATE RATE PAYMENT STATUS PROJECT FINANCING SUMMARY SOURCE AND USE OF FUNDS CDA BLF BANK EQUITY OTHER OTHER TOTAL Property Acquisition Site Improvement Building Renovation New Construction Machinery & Equipment Working Capital Inventory Debt Refinancing Other Other Total PROPOSED FINANCING TERMS CDA BLF BANK EQUITY OTHER OTHER TOTAL Amount $ $ $ $ $ $ % of Project Cost % % % % % % Term (years) yrs yrs yrs yrs yrs yrs Interest Rate % % % % % % Debt Service yrs yrs yrs yrs yrs yrs Lien Position Collateral Guarantee ADDITIONAL REQUIRED INFORMATION The information included in the attached “Exhibit A – Application Exhibits” shall also be provided to TCCCF as part of this loan application 2 I declare that the information provided on this application and the accompanying exhibits is true and complete to the best of my knowledge. I understand that the Carver County CDA Business Loan Fund has the right to verify this information and will be in contact with those individuals and institutions involved in the proposed project. -

Pension Obligation Debenture, 2021 Series A

Attachment B No. 2021-1 $_______ COUNTY OF ORANGE PENSION OBLIGATION DEBENTURE, 2021 SERIES A The County of Orange (the “County”), a political subdivision of the State of California, acknowledges itself indebted, and for value received hereby promises to pay, to the Orange County Employees Retirement System (the “System”), a retirement system existing under the County Employees Retirement Law of 1937 of the State of California (the “Act”), or assigns (the “Holder”), the sum of _____________Dollars ($________), payable in the amounts and on the dates set forth in Schedule I. Payment shall be made at such address as shall have been agreed upon by the Holder hereof and the County. This Debenture is a duly authorized debenture of the County designated its “Pension Obligation Debenture, 2021 Series A” (the “Debenture”) issued under and in full compliance with the Constitution and statutes of the State of California, particularly the Act, and under and pursuant to Resolutions adopted by the Board of Supervisors of the County on October 31, 2006 and December 15, 2020 (collectively, the “Resolution”). This Debenture and payments hereunder are subject to the terms and conditions of the Resolution, copies of which are on file at the office of the Clerk of the Board of Supervisors of the County, and reference to the Resolution and any and all supplements thereto and modifications and amendments thereof and to the Act is made for a complete statement of such terms and conditions. THIS DEBENTURE MAY BE PREPAID AT THE OPTION OF THE COUNTY IN WHOLE ON OR BEFORE JANUARY 15, 2021, AT A PREPAYMENT AMOUNT OF $_______. -

Public Sector Duplication of Small Business Administration Loan And

PUBLIC SECTOR DUPLICATION OF SMALL BUSINESS ADMINISTRATION LOAN AND INVESTMENT PROGRAMS: AN ANALYSIS OF OVERLAP BETWEEN FEDERAL, STATE, AND LOCAL PROGRAMS PROVIDING FINANCIAL ASSISTANCE TO SMALL BUSINESSES Final Report January 2008 Prepared for: U.S. Small Business Administration Prepared by: Rachel Brash The Urban Institute 2100 M Street, NW ● Washington, DC 20037 Public Sector Duplication of Small Business Administration Loan and Investment Programs: An Analysis of Overlap between Federal, State, and Local Programs Providing Financial Assistance to Small Businesses Final Report January 2008 Prepared By: Rachel Brash The Urban Institute Metropolitan Housing and Communities Policy Center 2100 M Street, NW Washington, DC 20037 Submitted To: U.S. Small Business Administration 409 Third Street, SW Washington, DC 20416 Contract No. GS23F8198H UI No. 07112-020-00 The Urban Institute is a nonprofit, nonpartisan policy research and educational organization that examines the social, economic, and governance problems facing the nation. The views expressed are those of the authors and should not be attributed to the Urban Institute, its trustees, or its funders. Public Sector Duplication of SBA Loan and Investment Programs i CONTENTS INTRODUCTION ..........................................................................................................................1 BACKGROUND............................................................................................................................2 Definition of Duplication ...........................................................................................................2 -

Convertible Debentures – a Primer

Portfolio Advisory Group May 12, 2011 Convertible Debentures – A Primer A convertible debenture is a hybrid financial instrument Convertible debentures offer some advantages over that has both fixed income and equity characteristics. In investing in common equity. As holders of a more its simplest terms, it is a bond that gives the holder the senior security, investors have a greater claim on the option to convert into an underlying equity instrument at firm’s assets in the event of insolvency. Secondly, the a predetermined price. Thus, investors receive a regular investor’s income flow is more stable since coupon income flow through the coupon payments plus the payments are a contractual obligation. Finally, ability to participate in capital appreciation through the convertible bonds offer both a measure of protection potential conversion to equity. Convertible debentures in bear markets through the regular bond features and are usually subordinated to the company’s other debt. participation in capital appreciation in bull markets through the conversion option. Unlike traditional Convertible debentures are issued by companies as a bonds, convertible debentures trade on a stock means of deferred equity financing in the belief that exchange but generally have a small issue size which the present share price is too low for issuing common can result in limited liquidity. shares. These securities offer a conversion into the underlying issuer’s shares at prices above the current VALUATION level (referred to as the conversion premium). In A convertible bond can be thought of as a straight return for offering an equity option, firms realize both bond with a call option for the underlying equity interest savings, since coupons on convertible bonds security. -

Stock Market Crash of Bangladesh in 2010-11: Reasons & Roles of Regulators

Stock market crash of Bangladesh in 2010-11: Reasons & roles of regulators Sangit Saha Degree Thesis Förnamn Efternamn International Business 2012 DEGREE THESIS Arcada Degree Programme: International Business Identification number: 11497 Author: Sangit Saha Title: Stock market crash of Bangladesh in 2010-11: Reasons & roles of regulators Supervisor (Arcada): Andreas Stenius Commissioned by: Abstract: The aim of the thesis is to determine reasons of the stock market crash in Bangladesh in 2010-11 and roles of the regulators and government since the crash took place. The theoretical background of the study includes brief introduction of Bangladesh stock market with its structure and different regulatory and intermediary organizations. It also describes one international stock market crash and stock market crash of Bangladesh in 1996. For the theoretical part investigation report of Khondkar Ibrahim Khaled is used as the main secondary resource. The report helps to get background of the crash with reasons and role of different regulatory and intermediary organizations. Self-administered questionnaire is used to obtain primary data for the study. The author sent 25 questionnaires to employees of broker houses and general investors but 18 replied. The result of the Self-administered questionnaire helped author to find some other reason behind the stock market crash in addition with reasons provided in the investigation report. Moreover, the result shows developments of market by the regulators and government since the crash. Finally, the author makes recommendation to the regulators, government and investor. Keywords: stock market, Bangladesh stock market crash, regulators, DSE, CSE, SEC Number of pages: 62 Language: English Date of acceptance: Table of Contents Acknowledgement ........................................................................................................ -

Lord Abbett Bond Debenture Fund - Class a 06-30-21

Release Date Lord Abbett Bond Debenture Fund - Class A 06-30-21 .......................................................................................................................................................................................................................................................................................................................................... Category Multisector Bond Investment Objective & Strategy Portfolio Analysis From the investment's prospectus Composition as of 05-31-21 % Assets Morningstar Fixed Income Style Box™ as of 05-31-21 The investment seeks high current income and the U.S. Stocks 9.7 High Avg Eff Duration 4.63 opportunity for capital appreciation to produce a high total Non-U.S. Stocks 0.8 Avg Eff Maturity 10.22 return. Bonds 88.3 Med Cash 0.0 To pursue its objective, under normal conditions, the Low fund invests at least 80% of its net assets, plus the amount Other 1.2 of any borrowings for investment purposes, in bonds, Ltd Mod Ext debentures and other fixed income securities. It may invest a substantial portion of its net assets in high-yield securities Top 10 Holdings as of 05-31-21 % Assets Morningstar F-I Sectors as of 05-31-21 % Fund (commonly referred to as "below investment grade" or "junk" Crowdstrike Holdings Inc 3% 02-15-29 0.50 ⁄ Government 3.28 bonds). The fund may invest up to 20% of its net assets in Tesla Inc 5.3% 08-15-25 0.48 › Corporate 81.09 equity securities, including common stocks, preferred stocks, Sprint Capital Corporation 6.88% 11-15-28 0.46 € Securitized 12.31 convertible preferred stocks, and similar instruments. Shake Shack Inc A 0.45 ‹ Municipal 3.22 Roblox Corp Ordinary Shares - Class A 0.43 Cash/Cash Equivalents 0.00 ....................................................................................................... fi Volatility and Risk PDC Energy Inc 0.42 ± Other 0.10 Volatility as of 06-30-21 HCA Inc.