Lord Abbett Bond Debenture Fund - Class a 06-30-21

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mortgage-Backed Securities & Collateralized Mortgage Obligations

Mortgage-backed Securities & Collateralized Mortgage Obligations: Prudent CRA INVESTMENT Opportunities by Andrew Kelman,Director, National Business Development M Securities Sales and Trading Group, Freddie Mac Mortgage-backed securities (MBS) have Here is how MBSs work. Lenders because of their stronger guarantees, become a popular vehicle for finan- originate mortgages and provide better liquidity and more favorable cial institutions looking for investment groups of similar mortgage loans to capital treatment. Accordingly, this opportunities in their communities. organizations like Freddie Mac and article will focus on agency MBSs. CRA officers and bank investment of- Fannie Mae, which then securitize The agency MBS issuer or servicer ficers appreciate the return and safety them. Originators use the cash they collects monthly payments from that MBSs provide and they are widely receive to provide additional mort- homeowners and “passes through” the available compared to other qualified gages in their communities. The re- principal and interest to investors. investments. sulting MBSs carry a guarantee of Thus, these pools are known as mort- Mortgage securities play a crucial timely payment of principal and inter- gage pass-throughs or participation role in housing finance in the U.S., est to the investor and are further certificates (PCs). Most MBSs are making financing available to home backed by the mortgaged properties backed by 30-year fixed-rate mort- buyers at lower costs and ensuring that themselves. Ginnie Mae securities are gages, but they can also be backed by funds are available throughout the backed by the full faith and credit of shorter-term fixed-rate mortgages or country. The MBS market is enormous the U.S. -

Convertible Bond Investing Brochure (PDF)

Convertible bond investing Invesco’s Convertible Securities Strategy 1 Introduction to convertible bonds A primer Convertible securities provide investors the opportunity to participate in the upside of stock markets while also offering potential downside protection. Because convertibles possess both stock- and bond-like attributes, they may be particularly useful in minimizing risk in a portfolio. The following is an introduction to convertibles, how they exhibit characteristics of both stocks and bonds, and where convertibles may fit in a diversified portfolio. Reasons for investing in convertibles Through their combination of stock and bond characteristics, convertibles may offer the following potential advantages over traditional stock and bond instruments: • Yield advantage over stocks • More exposure to market gains than market losses • Historically attractive risk-adjusted returns • Better risk-return profile • Lower interest rate risk Introduction to convertibles A convertible bond is a corporate bond that has the added feature of being convertible into a fixed number of shares of common stock. As a hybrid security, convertibles have the potential to offer equity-like returns due to their stock component with potentially less volatility due to their bond-like features. Convertibles are also higher in the capital structure than common stock, which means that companies must fulfill their obligations to convertible bondholders before stockholders. It is important to note that convertibles are subject to interest rate and credit risks that are applicable to traditional bonds. Simplified convertible structure Bond Call option Convertible Source: BofA Merrill Lynch Convertible Research. The bond feature of these securities comes from their stated interest rate and claim to principal. -

Corporate Bonds and Debentures

Corporate Bonds and Debentures FCS Vinita Nair Vinod Kothari Company Kolkata: New Delhi: Mumbai: 1006-1009, Krishna A-467, First Floor, 403-406, Shreyas Chambers 224 AJC Bose Road Defence Colony, 175, D N Road, Fort Kolkata – 700 017 New Delhi-110024 Mumbai Phone: 033 2281 3742/7715 Phone: 011 41315340 Phone: 022 2261 4021/ 6237 0959 Email: [email protected] Email: [email protected] Email: [email protected] Website: www.vinodkothari.com 1 Copyright & Disclaimer . This presentation is only for academic purposes; this is not intended to be a professional advice or opinion. Anyone relying on this does so at one’s own discretion. Please do consult your professional consultant for any matter covered by this presentation. The contents of the presentation are intended solely for the use of the client to whom the same is marked by us. No circulation, publication, or unauthorised use of the presentation in any form is allowed, except with our prior written permission. No part of this presentation is intended to be solicitation of professional assignment. 2 About Us Vinod Kothari and Company, company secretaries, is a firm with over 30 years of vintage Based out of Kolkata, New Delhi & Mumbai We are a team of qualified company secretaries, chartered accountants, lawyers and managers. Our Organization’s Credo: Focus on capabilities; opportunities follow 3 Law & Practice relating to Corporate Bonds & Debentures 4 The book can be ordered by clicking here Outline . Introduction to Debentures . State of Indian Bond Market . Comparison of debentures with other forms of borrowings/securities . Types of Debentures . Modes of Issuance & Regulatory Framework . -

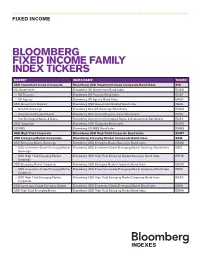

Bloomberg Fixed Income Family Index Tickers

///////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////// FIXED INCOME BLOOMBERG FIXED INCOME FAMILY INDEX TICKERS MARKET INDEX NAME TICKER USD Investment Grade Composite Bloomberg USD Investment Grade Composite Bond Index BIG US Government Bloomberg US Government Bond Index BUSG » US Treasury Bloomberg US Treasury Bond Index BUSY » US Agency Bloomberg US Agency Bond Index BAGY USD Government Related Bloomberg USD Government Related Bond Index BGRL » Non-US Sovereign Bloomberg Non-US Sovereign Bond Index BNSO » Government Regional/Local Bloomberg Government Regional/Local Bond Index BRGL » Gov Developed Banks & Supra Bloomberg Government Developed Banks & Supranational Bond Index BDEV USD Corporate Bloomberg USD Corporate Bond Index BUSC US MBS Bloomberg US MBS Bond Index BMBS USD High Yield Corporate Bloomberg USD High Yield Corporate Bond Index BUHY USD Emerging Market Composite Bloomberg Emerging Market Composite Bond Index BEM USD Emerging Market Sovereign Bloomberg USD Emerging Market Sovereign Bond Index BEMS » USD Investment Grade Emerging Market Bloomberg USD Investment Grade Emerging Market Sovereign Bond Index BEIS Sovereign » USD High Yield Emerging Market Bloomberg USD High Yield Emerging Market Sovereign Bond Index BEHS Sovereign USD Emerging Market Corporate Bloomberg USD Emerging Market Corporate Bond Index BEMC » USD Investment Grade Emerging Market Bloomberg USD Investment Grade Emerging Market Corporate Bond Index BIEM Corporate -

Derivative Securities

2. DERIVATIVE SECURITIES Objectives: After reading this chapter, you will 1. Understand the reason for trading options. 2. Know the basic terminology of options. 2.1 Derivative Securities A derivative security is a financial instrument whose value depends upon the value of another asset. The main types of derivatives are futures, forwards, options, and swaps. An example of a derivative security is a convertible bond. Such a bond, at the discretion of the bondholder, may be converted into a fixed number of shares of the stock of the issuing corporation. The value of a convertible bond depends upon the value of the underlying stock, and thus, it is a derivative security. An investor would like to buy such a bond because he can make money if the stock market rises. The stock price, and hence the bond value, will rise. If the stock market falls, he can still make money by earning interest on the convertible bond. Another derivative security is a forward contract. Suppose you have decided to buy an ounce of gold for investment purposes. The price of gold for immediate delivery is, say, $345 an ounce. You would like to hold this gold for a year and then sell it at the prevailing rates. One possibility is to pay $345 to a seller and get immediate physical possession of the gold, hold it for a year, and then sell it. If the price of gold a year from now is $370 an ounce, you have clearly made a profit of $25. That is not the only way to invest in gold. -

How Municipal Bonds Are Sold in a Public Offering JUNE 2020

UNDERSTANDING MUNICIPAL BONDS How Municipal Bonds Are Sold in a Public Offering JUNE 2020 anonymous to all underwriters, each underwriter can see the Municpal Bonds–Method of Sale ranking of its own bid relative to competing bids. Therefore, the Many of us are familiar with municipal bonds, either as an issuer, underwriter with the second best bid knows that it ranks second an investor, or, for a much smaller number of us, a participant and can continuously submit better bids until it holds the top in the municipal bond industry. Generally speaking, the idea is position. This bid competition continues until the predetermined simple. A unit of government needs to borrow money for any timeframe for the auction expires, unless there is a new top- number of public purposes, and investors have the capital to ranked bid within the last two minutes of the auction, in which lend to these governments in exchange for a rate of return. What case the auction is extended for another two minutes. Eventually, is far less familiar to many is an understanding of the intricacies the underwriter that submits the bid with the lowest TIC for a full of the municipal bond market. As a result, PMA’s Public Finance two minutes will be the winning bidder. See below for a sample group has created the “Understanding Municipal Bonds” series bid summary in an open-auction competitive sale. to help educate our issuer clients on nuanced aspects of the Sample Bid Summary–Open Auction bond market. In this edition, we provide insight on the method of sale options available to issuers when selling their bonds in the primary market (i.e., a public offering of municipal securities). -

What Are High-Yield Corporate Bonds?

INVESTOR BULLETIN What Are High-yield Corporate Bonds? The SEC’s Office of Investor Education and Advocacy is a high-yield bond, it is important that you understand issuing this Investor Bulletin to educate individual investors the risks involved. about high-yield corporate bonds, also called “junk bonds.” While they generally offer a higher yield than investment-grade Default risk. Also referred to as credit risk, this is the bonds, high-yield bonds also carry a higher risk of default. risk that a company will fail to make timely interest or principal payments and default on its bond. Defaults also What is a high-yield corporate bond? can occur if the company fails to meet certain terms of its A high-yield corporate bond is a type of corporate bond debt agreement. Because high-yield bonds are typically that offers a higher rate of interest because of its higher issued by companies with higher risks of default, this risk risk of default. When companies with a greater estimated is particularly important to consider when investing in default risk issue bonds, they may be unable to obtain high-yield bonds. an investment-grade bond credit rating. As a result, they Interest rate risk. typically issue bonds with higher interest rates in order to Market interest rates have a major entice investors and compensate them for this higher risk. impact on bond investments. The price of a bond moves in the opposite direction than market interest rates—like High-yield bond issuers may be companies characterized opposing ends of a seesaw. This presents investors with as highly leveraged or those experiencing financial interest rate risk, which is common to all bonds. -

Chapter 3 Fixed Income Securities

Chapter 3 Fixed Income Securities Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. • Fixed-income securities. • Stocks. • Real assets (capital budgeting). Part C Determination of risk-adjusted discount rates. Part D Introduction to derivatives. Main Issues • Fixed-Income Markets • Term Structure of Interest Rates • Interest Rate Risk • Inflation Risk • Credit Risk Chapter 3 Fixed Income Securities 3-1 1 Fixed-Income Markets Definition: Fixed-income securities are financial claims with promised cash flows of fixed amount paid at fixed dates. Classification of Fixed-Income Securities: 1. Treasury Securities: • U.S. Treasury securities (bills, notes, bonds). • Bunds, JGBs, U.K. Gilts ... 2. Federal Agency Securities: • Securities issued by federal agencies (FHLB, FNMA ...). 3. Corporate Securities: • Commercial paper. • Medium-term notes (MTNs). • Corporate bonds ... 4. Municipal Securities. 5. Mortgage-Backed Securities. 6. ... Fall 2006 c J. Wang 15.401 Lecture Notes 3-2 Fixed Income Securities Chapter 3 Overview of Fixed-income Markets Composition of U.S. Debt Markets (2005) Market value % (in trillion dollars) Treasury 4.17 16.5 Corporate 4.99 19.7 Mortgage 5.92 23.4 Agency 2.60 10.3 Munies 2.23 8.8 Asset-Backed 1.96 7.7 Money Market 3.47 13.7 Total 25.33 Current Trends T. Corp. MBS Agency ABS Munies MM Total 1995 3.31 1.94 2.35 0.84 0.32 1.29 1.18 11.23 1996 3.44 2.12 2.49 0.93 0.40 1.30 1.39 12.01 1997 3.44 2.36 2.68 1.02 0.54 1.32 1.69 13.05 1998 3.34 2.71 2.96 1.30 0.73 1.40 1.98 14.42 1999 3.27 3.05 3.33 1.62 0.90 1.46 2.34 15.96 2000 2.95 3.36 3.56 1.85 1.07 1.48 2.66 16.95 2001 2.97 3.84 4.13 2.15 1.28 1.60 2.57 18.53 2002 3.20 4.09 4.70 2.29 1.54 1.73 2.55 20.15 2003 3.57 4.46 5.31 2.64 1.69 1.89 2.53 22.10 2004 3.94 3.70 5.47 2.75 1.83 2.02 2.87 23.58 2005 4.17 4.99 4.92 2.60 1.96 2.23 3.47 25.33 15.401 Lecture Notes c J. -

Read the Full Paper

volume 47 number 3 FEBRUARY 2021 jpm.pm-research.com The Stock-Bond Correlation Megan Czasonis, Mark Kritzman, and David Turkington Megan Czasonis Megan Czasonis is a Managing Director for the Portfolio and Risk Research team at State Street Associates. The Portfolio and Risk Research team collaborates with academic partners to develop new research on asset allocation, risk management, and investment strategy. The team delivers this research to institutional investors through indicators, advisory projects, and thought leadership pieces. Megan has co-authored various journal permission. articles and works closely with institutional investors to develop customized solutions based on this research. Megan graduated Summa Cum Laude from Bentley University Publisher with a B.S. in Economics / Finance. without Mark Kritzman Mark Kritzman is a Founding Partner and CEO of Windham Capital Management, a electronically Founding Partner of State Street Associates, and teaches a graduate finance course post at the Massachusetts Institute of Technology. Mark served as a Founding Director of to the International Securities Exchange and has served on several Boards, including the or Institute for Quantitative Research in Finance, The Investment Fund for Foundations, and user, State Street Associates. He has written numerous articles for academic and professional journals and is the author / co-author of seven books including A Practitioner’s Guide to Asset Allocation, Puzzles of Finance, and The Portable Financial Analyst. Mark won Graham unauthorized and Dodd Scrolls in 1993 and 2002, the Research Prize from the Institute for Quantitative an Investment Research in 1997, the Bernstein Fabozzi/Jacobs Levy Award nine times, the to Roger F. -

Bond Issuance Process Overview

BOND ISSUANCE PROCESS OVERVIEW Adams 12 Five Star Schools November 2016 AND CONFIDENTIAL STRICTLY PRIVATE STRICTLY CONFIDENTIAL This presentation was prepared exclusively for the benefit and internal use of the J.P. Morgan client to whom it is directly addressed and delivered (including such client’s affiliates, the “Client”) in order to assist the Client in evaluating, on a preliminary basis, the feasibility of possible transactions referenced herein. The materials have been provided to the Client for informational purposes only and may not be relied upon by the Client in evaluating the merits of pursuing transactions described herein. No assurance can be given that any transaction mentioned herein could in fact be executed. Information has been obtained from sources believed to be reliable but J.P. Morgan does not warrant its completeness or accuracy. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. Any financial products discussed may fluctuate in price or value. This presentation does not constitute a commitment by any J.P. Morgan entity to underwrite, subscribe for or place any securities or to extend or arrange credit or to provide any other services. J.P. Morgan's presentation is delivered to you for the purpose of being engaged as an underwriter, not as an advisor, (including, without limitation, a Municipal Advisor (as such term is defined in Section 975(e) of the Dodd-Frank Wall Street Reform and Consumer Protection Act)) . The role of an underwriter and its relationship to an issuer of debt is not equivalent to the role of an independent financial advisor. -

Pension Obligation Debenture, 2021 Series A

Attachment B No. 2021-1 $_______ COUNTY OF ORANGE PENSION OBLIGATION DEBENTURE, 2021 SERIES A The County of Orange (the “County”), a political subdivision of the State of California, acknowledges itself indebted, and for value received hereby promises to pay, to the Orange County Employees Retirement System (the “System”), a retirement system existing under the County Employees Retirement Law of 1937 of the State of California (the “Act”), or assigns (the “Holder”), the sum of _____________Dollars ($________), payable in the amounts and on the dates set forth in Schedule I. Payment shall be made at such address as shall have been agreed upon by the Holder hereof and the County. This Debenture is a duly authorized debenture of the County designated its “Pension Obligation Debenture, 2021 Series A” (the “Debenture”) issued under and in full compliance with the Constitution and statutes of the State of California, particularly the Act, and under and pursuant to Resolutions adopted by the Board of Supervisors of the County on October 31, 2006 and December 15, 2020 (collectively, the “Resolution”). This Debenture and payments hereunder are subject to the terms and conditions of the Resolution, copies of which are on file at the office of the Clerk of the Board of Supervisors of the County, and reference to the Resolution and any and all supplements thereto and modifications and amendments thereof and to the Act is made for a complete statement of such terms and conditions. THIS DEBENTURE MAY BE PREPAID AT THE OPTION OF THE COUNTY IN WHOLE ON OR BEFORE JANUARY 15, 2021, AT A PREPAYMENT AMOUNT OF $_______. -

Managing Fixed Income Late in the Credit Cycle: Navigating the Path Forward

INCOME INVESTING Managing fixed income late in the credit cycle: navigating the path forward nuveen knows Highlights • While we are clearly in the late stage of the credit cycle, we don’t think a recession is imminent and believe investors should feel comfortable investing in credit 2Q19 markets throughout the rest of 2019. • We believe investors should focus on higher-quality issues with improving credit fundamentals, while seeking to diversify across industries and geographies. • Nuveen’s sector specialist teams are finding attractive opportunities in U.S. credit sectors, including high yield, but they are increasingly diversifying into other higher-income areas, such as emerging market debt and leveraged loans. • Active management can add value in any environment, but we believe it is especially beneficial at the current stage of the credit cycle. The multi-trillion-dollar question for investors: How late are we in the credit cycle, and what are the portfolio implications? That’s the question we most often hear from our clients. And while there are few certainties in life or markets, we feel confident in our answer: We are clearly in the late stage of the credit cycle. But “late” doesn’t mean “done,” and credit cycles don’t die of old age. Rather, a combination of fundamentals and sentiment bring about their demise, and even in their later stages, savvy investors can find opportunities not only to protect their investments, but to position their portfolios for an emphasis on income as the cycle turns. Nuveen believes most investors should be comfortable investing in the credit markets throughout the rest of 2019.