Municipal Bond Investor Weekly September 20, 2021 Noreen Mcclure –Director, High Net Worth Drew O’Neil - VP, Fixed Income Strategist

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Evidence from SME Bond Markets

Temi di discussione (Working Papers) Asymmetric information in corporate lending: evidence from SME bond markets by Alessandra Iannamorelli, Stefano Nobili, Antonio Scalia and Luana Zaccaria September 2020 September Number 1292 Temi di discussione (Working Papers) Asymmetric information in corporate lending: evidence from SME bond markets by Alessandra Iannamorelli, Stefano Nobili, Antonio Scalia and Luana Zaccaria Number 1292 - September 2020 The papers published in the Temi di discussione series describe preliminary results and are made available to the public to encourage discussion and elicit comments. The views expressed in the articles are those of the authors and do not involve the responsibility of the Bank. Editorial Board: Federico Cingano, Marianna Riggi, Monica Andini, Audinga Baltrunaite, Marco Bottone, Davide Delle Monache, Sara Formai, Francesco Franceschi, Salvatore Lo Bello, Juho Taneli Makinen, Luca Metelli, Mario Pietrunti, Marco Savegnago. Editorial Assistants: Alessandra Giammarco, Roberto Marano. ISSN 1594-7939 (print) ISSN 2281-3950 (online) Printed by the Printing and Publishing Division of the Bank of Italy ASYMMETRIC INFORMATION IN CORPORATE LENDING: EVIDENCE FROM SME BOND MARKETS by Alessandra Iannamorelli†, Stefano Nobili†, Antonio Scalia† and Luana Zaccaria‡ Abstract Using a comprehensive dataset of Italian SMEs, we find that differences between private and public information on creditworthiness affect firms’ decisions to issue debt securities. Surprisingly, our evidence supports positive (rather than adverse) selection. Holding public information constant, firms with better private fundamentals are more likely to access bond markets. Additionally, credit conditions improve for issuers following the bond placement, compared with a matched sample of non-issuers. These results are consistent with a model where banks offer more flexibility than markets during financial distress and firms may use market lending to signal credit quality to outside stakeholders. -

Mortgage-Backed Securities & Collateralized Mortgage Obligations

Mortgage-backed Securities & Collateralized Mortgage Obligations: Prudent CRA INVESTMENT Opportunities by Andrew Kelman,Director, National Business Development M Securities Sales and Trading Group, Freddie Mac Mortgage-backed securities (MBS) have Here is how MBSs work. Lenders because of their stronger guarantees, become a popular vehicle for finan- originate mortgages and provide better liquidity and more favorable cial institutions looking for investment groups of similar mortgage loans to capital treatment. Accordingly, this opportunities in their communities. organizations like Freddie Mac and article will focus on agency MBSs. CRA officers and bank investment of- Fannie Mae, which then securitize The agency MBS issuer or servicer ficers appreciate the return and safety them. Originators use the cash they collects monthly payments from that MBSs provide and they are widely receive to provide additional mort- homeowners and “passes through” the available compared to other qualified gages in their communities. The re- principal and interest to investors. investments. sulting MBSs carry a guarantee of Thus, these pools are known as mort- Mortgage securities play a crucial timely payment of principal and inter- gage pass-throughs or participation role in housing finance in the U.S., est to the investor and are further certificates (PCs). Most MBSs are making financing available to home backed by the mortgaged properties backed by 30-year fixed-rate mort- buyers at lower costs and ensuring that themselves. Ginnie Mae securities are gages, but they can also be backed by funds are available throughout the backed by the full faith and credit of shorter-term fixed-rate mortgages or country. The MBS market is enormous the U.S. -

A Pooled Municipal Bonding Program

A POOLED MUNICIPAL BONDING PROGRAM Contents Program Overview ………………………………………………... 1 History of the Bond Bank ………………………………………… 2 Tax-Exempt Financing Program ……………………….…………. 4 Other Bond Bank Programs …………………………………….… 5 Benefits to Participating Communities ……………………….…... 5 Loan Application and Financing Process…………………………. 6 Spring 2012 Financing Schedule………………………………….. 7 New Hampshire Municipal Bond Bank 25 Triangle Park Drive Concord, New Hampshire 03301 Email: [email protected] Web-site Address: www.nhmbb.org Revised 3/12 The mission of the New Hampshire Municipal Bond Bank is to provide professional services to assist qualified New Hampshire entities to obtain financing for eligible purposes. To meet its mission, the New Hampshire Municipal Bond Bank is committed to: ! Financial stability ! Strong client relations ! Low issuance costs ! Obtaining the lowest possible borrowing rates ! An efficient application process ! Maintaining strong credit ratings and financial market access ! A well trained team of professional staff & consultants ! Support best possible public finance practices ! Meeting the requirements of all applicable state and federal laws, particularly RSA:35-A “On a number of occasions, I have included the Bond Bank in my requests for proposals, which included the major private banking institutions doing business in New Hampshire at the time. After careful analysis, you have always been chosen due to the Bond Bank’s reasonable fee structure, ease of use and excellent customer service standards. The Bond Bank has seen me through the construction of a number of large projects which include a wastewater treatment facility and a new high school, as well as many others of a smaller magnitude. I look forward to working with the Bond Bank in the future.” Peter A. -

Decomposing Underwriting Spreads for GSE's and Frequent Issuer Financial Firms

Decomposing Underwriting Spreads for GSEs and Frequent Issuer Financial Firms David M. Harrison Associate Professor Rawls College of Business Administration Texas Tech University Lubbock, TX 79409 [email protected] 806.742.3190 phone 806.742.3197 fax Andrea J. Heuson Professor of Finance University of Miami P.O. Box 248094 5250 University Dr., Jenkins Bldg. Coral Gables, FL 33124 [email protected] 305.284.1866 phone 305.284.4800 fax and Michael J. Seiler Professor and Robert M. Stanton Chair of Real Estate Old Dominion University 2154 Constant Hall Norfolk, VA 23529 [email protected] 757.683.3505 phone 757.683.3258 fax Revise and Resubmit at Journal of Real Estate Finance and Economics December 2010 Decomposing Underwriting Spreads for GSEs and Frequent Issuer Financial Firms Home mortgage debt outstanding grew at a nominal rate of more than 10% per year and a real rate of more than 8% per year during the decade that began in 1997. Much of the increase was funded by investors who purchased mortgage-backed securities through a market supported by Fannie Mae and Freddie Mac – two Government Sponsored Enterprises (GSEs) charged with improving intermediation in the residential mortgage market. Furthermore, both housing and non-housing GSEs and large domestic financial institutions took sizeable investment positions in mortgage-backed securities, funding this increased investment by borrowing in the bond market using callable and non-callable debt agreements. Recent developments make clear that many of these investments carried significant credit risk. This paper investigates the determinants of underwriting fees charged to active GSE and financial industry borrowers on debt issuances, how such fees change over time, and how they vary with the characteristics of the debt, the underwriting mechanism, and the issuer. -

Navigating the Municipal Bond Market September 2019

Navigating the Municipal Bond Market September 2019 Craig Brandon, CFA Co-Director of Municipal Investments AN EATON VANCE COMPANY FOR INVESTMENT PROFESSIONAL USE ONLY. NOT FOR USE WITH THE PUBLIC. 2 Fixed Income Asset Class Return Analysis Higher 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 YTD EM (Local EM (Local EM (Local Investment Treasury High Yield Municipal High Yield Municipal Municipal High Yield Municipal Currency) Currency) Currency) Grade 13.74 57.51 10.70 7.42 9.05 3.30 17.49 1.28 15.68 16.76 15.21 13.94 Investment Global Agg MBS Bank Loan High Yield Treasury High Yield Bank Loan MBS Bank Loan MBS High Yield Grade Ex-U.S. 8.34 51.62 15.19 9.81 15.58 5.29 1.51 10.16 0.99 11.15 7.46 10.51 Global Agg EM (Local Investment Investment EM (Local Bank Loan MBS MBS Treasury High Yield Treasury Treasury Ex-U.S. Currency) Grade Grade Currency) 10.13 -1.41 6.08 0.84 7.48 0.86 8.63 4.40 21.98 8.15 9.82 9.94 Investment Investment Investment Investment Investment Investment Municipal MBS Bank Loan Treasury Bank Loan Municipal Grade Grade Grade Grade Grade Grade -2.47 6.23 9.66 5.05 0.44 7.61 18.68 9.00 -1.53 -0.68 6.11 6.42 Investment Global Agg EM (Local Municipal Treasury High Yield Municipal Municipal High Yield Bank Loan MBS Municipal Grade Ex-US Currency) 12.91 5.87 4.38 6.78 -2.55 2.50 -0.69 1.67 5.45 -4.94 -2.15 6.83 EM (Local Global Agg Global Agg Global Agg Global Agg MBS Treasury Bank Loan High Yield Bank Loan High Yield Bank Loan Currency) Ex-U.S. -

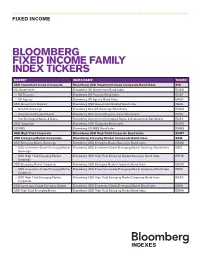

Bloomberg Fixed Income Family Index Tickers

///////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////// FIXED INCOME BLOOMBERG FIXED INCOME FAMILY INDEX TICKERS MARKET INDEX NAME TICKER USD Investment Grade Composite Bloomberg USD Investment Grade Composite Bond Index BIG US Government Bloomberg US Government Bond Index BUSG » US Treasury Bloomberg US Treasury Bond Index BUSY » US Agency Bloomberg US Agency Bond Index BAGY USD Government Related Bloomberg USD Government Related Bond Index BGRL » Non-US Sovereign Bloomberg Non-US Sovereign Bond Index BNSO » Government Regional/Local Bloomberg Government Regional/Local Bond Index BRGL » Gov Developed Banks & Supra Bloomberg Government Developed Banks & Supranational Bond Index BDEV USD Corporate Bloomberg USD Corporate Bond Index BUSC US MBS Bloomberg US MBS Bond Index BMBS USD High Yield Corporate Bloomberg USD High Yield Corporate Bond Index BUHY USD Emerging Market Composite Bloomberg Emerging Market Composite Bond Index BEM USD Emerging Market Sovereign Bloomberg USD Emerging Market Sovereign Bond Index BEMS » USD Investment Grade Emerging Market Bloomberg USD Investment Grade Emerging Market Sovereign Bond Index BEIS Sovereign » USD High Yield Emerging Market Bloomberg USD High Yield Emerging Market Sovereign Bond Index BEHS Sovereign USD Emerging Market Corporate Bloomberg USD Emerging Market Corporate Bond Index BEMC » USD Investment Grade Emerging Market Bloomberg USD Investment Grade Emerging Market Corporate Bond Index BIEM Corporate -

Chapter 3 Fixed Income Securities

Chapter 3 Fixed Income Securities Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. • Fixed-income securities. • Stocks. • Real assets (capital budgeting). Part C Determination of risk-adjusted discount rates. Part D Introduction to derivatives. Main Issues • Fixed-Income Markets • Term Structure of Interest Rates • Interest Rate Risk • Inflation Risk • Credit Risk Chapter 3 Fixed Income Securities 3-1 1 Fixed-Income Markets Definition: Fixed-income securities are financial claims with promised cash flows of fixed amount paid at fixed dates. Classification of Fixed-Income Securities: 1. Treasury Securities: • U.S. Treasury securities (bills, notes, bonds). • Bunds, JGBs, U.K. Gilts ... 2. Federal Agency Securities: • Securities issued by federal agencies (FHLB, FNMA ...). 3. Corporate Securities: • Commercial paper. • Medium-term notes (MTNs). • Corporate bonds ... 4. Municipal Securities. 5. Mortgage-Backed Securities. 6. ... Fall 2006 c J. Wang 15.401 Lecture Notes 3-2 Fixed Income Securities Chapter 3 Overview of Fixed-income Markets Composition of U.S. Debt Markets (2005) Market value % (in trillion dollars) Treasury 4.17 16.5 Corporate 4.99 19.7 Mortgage 5.92 23.4 Agency 2.60 10.3 Munies 2.23 8.8 Asset-Backed 1.96 7.7 Money Market 3.47 13.7 Total 25.33 Current Trends T. Corp. MBS Agency ABS Munies MM Total 1995 3.31 1.94 2.35 0.84 0.32 1.29 1.18 11.23 1996 3.44 2.12 2.49 0.93 0.40 1.30 1.39 12.01 1997 3.44 2.36 2.68 1.02 0.54 1.32 1.69 13.05 1998 3.34 2.71 2.96 1.30 0.73 1.40 1.98 14.42 1999 3.27 3.05 3.33 1.62 0.90 1.46 2.34 15.96 2000 2.95 3.36 3.56 1.85 1.07 1.48 2.66 16.95 2001 2.97 3.84 4.13 2.15 1.28 1.60 2.57 18.53 2002 3.20 4.09 4.70 2.29 1.54 1.73 2.55 20.15 2003 3.57 4.46 5.31 2.64 1.69 1.89 2.53 22.10 2004 3.94 3.70 5.47 2.75 1.83 2.02 2.87 23.58 2005 4.17 4.99 4.92 2.60 1.96 2.23 3.47 25.33 15.401 Lecture Notes c J. -

The Behavior of Residential Mortgage Yields Since 1951. Jack M. Guttentag

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Essays on Interest Rates, Volume 1 Volume Author/Editor: Jack M. Guttentag and Phillip Cagan, eds. Volume Publisher: NBER Volume ISBN: 0-87014-201-1 Volume URL: http://www.nber.org/books/gutt69-1 Publication Date: 1969 Chapter Title: The Behavior of Residential Mortgage Yields Since 1951 Chapter Author: Jack M. Guttentag Chapter URL: http://www.nber.org/chapters/c1208 Chapter pages in book: (p. 29 - 76) 2 TheBehavior of Residential Mortgage Yields Since 1951 Jack M. Guttentag This chapter reports some selected findings drawn from a study of the behavior of residential mortgage interest rates in the period since 1951. The findings reported here are based in part on new monthly and quarterly time series on residential mortgage rates and terms drawn from the internal records of some large life insurance com- panies.' These new data have a combination of important attributes heretofore not available in any single series. First, the date of record is the date when loans were committed or authorized by lenders, rather than the date on which funds were dis- bursed. Hence the long and erratic lag characteristic of a series recorded on a disbursement basis is largely eliminated. Second, the data cover all three types of residential mortgages (FHA, VA, and conventional); separate series are also available on mortgages acquired through correspondents as opposed to those originated directly by life insurance companies. Third, the data include loan-value ratios and maturities, as well as fees and charges collected and paid by the lender over and above the contract rate. -

Issuance of Tax-Exempt Municipal Debentures

Issuance of Tax-Exempt Municipal Debentures (City Council on August 1, 2, 3 and 4, 2000, adopted this Clause, without amendment.) The Policy and Finance Committee recommendations the adoption of the following report (July 4, 2000) from the Chief Financial Officer and Treasurer: Purpose: To discuss the potential advantages and disadvantages if the City is legally allowed to issue tax-free municipal bonds and to provide a strategy to proceed with this issue. Financial Implications and Impact Statement: N/A Recommendations: It is recommended that: (1) this report be received for information; and (2) a copy of this report be forwarded to Team Toronto for its consideration with other possible alternative financing strategies being explored with the provincial and federal governments. Background: At the Council meeting held on January 27, 2000, Councillor Davis moved a Notice of Motion requesting Council to establish a Working Committee on Municipal Debt composed of five members of City Council working with staff to establish a proposal for presentation to federal and provincial finance Ministers and officials concerning tax-free municipal bonds. The motion was referred to the Chief Administrative Officer for a report to the Policy and Finance Committee who requested a report from the Chief Financial Officer and Treasurer. Comments: In the United States, the federal government exempts interest payments on municipal debt from federal income taxes, thus lowering the cost of borrowing for state and local governments. Bonds purchased in one’s own jurisdiction are usually also exempt from local and state income taxes, e.g., New York residents who purchase New York City bonds. -

Standard Formulas for the Analysis of Mortgage-Backed Securities and Other Related Securities

The Bond Market Association Uniform Practices/Standard Formulas Chapter SF Standard Formulas for the Analysis of Mortgage-Backed Securities and Other Related Securities Table of Contents A. Computational Accuracy SF-3 B. Prepayments SF-4 1. Cash Flows SF-4 2. Mortgage Prepayment Models SF-5 3. Average Prepayment Rates for Mortgage Pools SF-11 4. ABS Prepayment Rates for Asset Pools SF-13 C. Defaults SF-16 1. Mortgage Cash Flows with Defaults: Description of Basic Concepts SF-16 2. Specifying Mortgage Default Assumptions: Standards and Definitions SF-17 3. Standard Formulas for Computing Mortgage Cash Flows with Defaults SF-18 4. The Standard Default Assumption (SDA) SF-20 5. Use of the SDA for Products Other Than 30-Year Conventional Mortgages SF-22 6. Numerical Examples of SDA SF-22 D. Assumptions for Generic Pools SF-39 1. Mortgage Maturity SF-39 2. Mortgage Age SF-40 3. Mortgage Coupon SF-43 E. Day Counts SF-44 1. Calendar Basis SF-44 2. Delay Days SF-44 02/01/99 SF-1 All rights reserved. Reproduction in any form is strictly forbidden. © 1999 The Bond Market Association. The Bond Market Association Uniform Practices/Standard Formulas F. Settlement-Based Calculations SF-45 1. General Rules SF-45 2. CMO Bonds with Unknown Settlement Factors SF-46 3. Freddie Mac Multiclass PCs (REMICs) SF-47 G. Yield and Yield-Related Measures SF-48 1. General Rules SF-48 2. Calculations for Floating-Rate MBS SF-52 3. Putable Project Loans SF-55 H. Accrual Instruments SF-56 1. Average Life of Accrual Instruments SF-56 2. -

Greenbook Part 2

Prefatory Note The attached document represents the most complete and accurate version available based on original copies culled from the files of the FOMC Secretariat at the Board of Governors of the Federal Reserve System. This electronic document was created through a comprehensive digitization process which included identifying the best- preserved paper copies, scanning those copies,1 and then making the scanned versions text-searchable.2 Though a stringent quality assurance process was employed, some imperfections may remain. Please note that this document may contain occasional gaps in the text. These gaps are the result of a redaction process that removed information obtained on a confidential basis. All redacted passages are exempt from disclosure under applicable provisions of the Freedom of Information Act. 1 In some cases, original copies needed to be photocopied before being scanned into electronic format. All scanned images were deskewed (to remove the effects of printer- and scanner-introduced tilting) and lightly cleaned (to remove dark spots caused by staple holes, hole punches, and other blemishes caused after initial printing). 2 A two-step process was used. An advanced optimal character recognition computer program (OCR) first created electronic text from the document image. Where the OCR results were inconclusive, staff checked and corrected the text as necessary. Please note that the numbers and text in charts and tables were not reliably recognized by the OCR process and were not checked or corrected by staff. Confidential (FR) Class III FOMC June 30, 1993 RECENT DEVELOPMENTS Prepared for the Federal Open Market Committee By the staff of the Board of Governors of the Federal Reserve System CONTENTS II DOMESTIC NONFINANCIAL DEVELOPMENTS Employment and unemployment................................. -

Managing Fixed Income Late in the Credit Cycle: Navigating the Path Forward

INCOME INVESTING Managing fixed income late in the credit cycle: navigating the path forward nuveen knows Highlights • While we are clearly in the late stage of the credit cycle, we don’t think a recession is imminent and believe investors should feel comfortable investing in credit 2Q19 markets throughout the rest of 2019. • We believe investors should focus on higher-quality issues with improving credit fundamentals, while seeking to diversify across industries and geographies. • Nuveen’s sector specialist teams are finding attractive opportunities in U.S. credit sectors, including high yield, but they are increasingly diversifying into other higher-income areas, such as emerging market debt and leveraged loans. • Active management can add value in any environment, but we believe it is especially beneficial at the current stage of the credit cycle. The multi-trillion-dollar question for investors: How late are we in the credit cycle, and what are the portfolio implications? That’s the question we most often hear from our clients. And while there are few certainties in life or markets, we feel confident in our answer: We are clearly in the late stage of the credit cycle. But “late” doesn’t mean “done,” and credit cycles don’t die of old age. Rather, a combination of fundamentals and sentiment bring about their demise, and even in their later stages, savvy investors can find opportunities not only to protect their investments, but to position their portfolios for an emphasis on income as the cycle turns. Nuveen believes most investors should be comfortable investing in the credit markets throughout the rest of 2019.