Morningstar Global Fixed Income Classification Methodology

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Section 1256 and Foreign Currency Derivatives

Section 1256 and Foreign Currency Derivatives Viva Hammer1 Mark-to-market taxation was considered “a fundamental departure from the concept of income realization in the U.S. tax law”2 when it was introduced in 1981. Congress was only game to propose the concept because of rampant “straddle” shelters that were undermining the U.S. tax system and commodities derivatives markets. Early in tax history, the Supreme Court articulated the realization principle as a Constitutional limitation on Congress’ taxing power. But in 1981, lawmakers makers felt confident imposing mark-to-market on exchange traded futures contracts because of the exchanges’ system of variation margin. However, when in 1982 non-exchange foreign currency traders asked to come within the ambit of mark-to-market taxation, Congress acceded to their demands even though this market had no equivalent to variation margin. This opportunistic rather than policy-driven history has spawned a great debate amongst tax practitioners as to the scope of the mark-to-market rule governing foreign currency contracts. Several recent cases have added fuel to the debate. The Straddle Shelters of the 1970s Straddle shelters were developed to exploit several structural flaws in the U.S. tax system: (1) the vast gulf between ordinary income tax rate (maximum 70%) and long term capital gain rate (28%), (2) the arbitrary distinction between capital gain and ordinary income, making it relatively easy to convert one to the other, and (3) the non- economic tax treatment of derivative contracts. Straddle shelters were so pervasive that in 1978 it was estimated that more than 75% of the open interest in silver futures were entered into to accommodate tax straddles and demand for U.S. -

Master Thesis the Use of Interest Rate Derivatives and Firm Market Value an Empirical Study on European and Russian Non-Financial Firms

Master Thesis The use of Interest Rate Derivatives and Firm Market Value An empirical study on European and Russian non-financial firms Tilburg, October 5, 2014 Mark van Dijck, 937367 Tilburg University, Finance department Supervisor: Drs. J.H. Gieskens AC CCM QT Master Thesis The use of Interest Rate Derivatives and Firm Market Value An empirical study on European and Russian non-financial firms Tilburg, October 5, 2014 Mark van Dijck, 937367 Supervisor: Drs. J.H. Gieskens AC CCM QT 2 Preface In the winter of 2010 I found myself in the heart of a company where the credit crisis took place at that moment. During a treasury internship for Heijmans NV in Rosmalen, I experienced why it is sometimes unescapable to use interest rate derivatives. Due to difficult financial times, banks strengthen their requirements and the treasury department had to use different mechanism including derivatives to restructure their loans to the appropriate level. It was a fascinating time. One year later I wrote a bachelor thesis about risk management within energy trading for consultancy firm Tensor. Interested in treasury and risk management I have always wanted to finish my finance study period in this field. During the master thesis period I started to work as junior commodity trader at Kühne & Heitz. I want to thank Kühne & Heitz for the opportunity to work in the trading environment and to learn what the use of derivatives is all about. A word of gratitude to my supervisor Drs. J.H. Gieskens for his quick reply, well experienced feedback that kept me sharp to different levels of the subject, and his availability even in the late hours after I finished work. -

Buying Options on Futures Contracts. a Guide to Uses

NATIONAL FUTURES ASSOCIATION Buying Options on Futures Contracts A Guide to Uses and Risks Table of Contents 4 Introduction 6 Part One: The Vocabulary of Options Trading 10 Part Two: The Arithmetic of Option Premiums 10 Intrinsic Value 10 Time Value 12 Part Three: The Mechanics of Buying and Writing Options 12 Commission Charges 13 Leverage 13 The First Step: Calculate the Break-Even Price 15 Factors Affecting the Choice of an Option 18 After You Buy an Option: What Then? 21 Who Writes Options and Why 22 Risk Caution 23 Part Four: A Pre-Investment Checklist 25 NFA Information and Resources Buying Options on Futures Contracts: A Guide to Uses and Risks National Futures Association is a Congressionally authorized self- regulatory organization of the United States futures industry. Its mission is to provide innovative regulatory pro- grams and services that ensure futures industry integrity, protect market par- ticipants and help NFA Members meet their regulatory responsibilities. This booklet has been prepared as a part of NFA’s continuing public educa- tion efforts to provide information about the futures industry to potential investors. Disclaimer: This brochure only discusses the most common type of commodity options traded in the U.S.—options on futures contracts traded on a regulated exchange and exercisable at any time before they expire. If you are considering trading options on the underlying commodity itself or options that can only be exercised at or near their expiration date, ask your broker for more information. 3 Introduction Although futures contracts have been traded on U.S. exchanges since 1865, options on futures contracts were not introduced until 1982. -

Mortgage-Backed Securities & Collateralized Mortgage Obligations

Mortgage-backed Securities & Collateralized Mortgage Obligations: Prudent CRA INVESTMENT Opportunities by Andrew Kelman,Director, National Business Development M Securities Sales and Trading Group, Freddie Mac Mortgage-backed securities (MBS) have Here is how MBSs work. Lenders because of their stronger guarantees, become a popular vehicle for finan- originate mortgages and provide better liquidity and more favorable cial institutions looking for investment groups of similar mortgage loans to capital treatment. Accordingly, this opportunities in their communities. organizations like Freddie Mac and article will focus on agency MBSs. CRA officers and bank investment of- Fannie Mae, which then securitize The agency MBS issuer or servicer ficers appreciate the return and safety them. Originators use the cash they collects monthly payments from that MBSs provide and they are widely receive to provide additional mort- homeowners and “passes through” the available compared to other qualified gages in their communities. The re- principal and interest to investors. investments. sulting MBSs carry a guarantee of Thus, these pools are known as mort- Mortgage securities play a crucial timely payment of principal and inter- gage pass-throughs or participation role in housing finance in the U.S., est to the investor and are further certificates (PCs). Most MBSs are making financing available to home backed by the mortgaged properties backed by 30-year fixed-rate mort- buyers at lower costs and ensuring that themselves. Ginnie Mae securities are gages, but they can also be backed by funds are available throughout the backed by the full faith and credit of shorter-term fixed-rate mortgages or country. The MBS market is enormous the U.S. -

An Analysis of OTC Interest Rate Derivatives Transactions: Implications for Public Reporting

Federal Reserve Bank of New York Staff Reports An Analysis of OTC Interest Rate Derivatives Transactions: Implications for Public Reporting Michael Fleming John Jackson Ada Li Asani Sarkar Patricia Zobel Staff Report No. 557 March 2012 Revised October 2012 FRBNY Staff REPORTS This paper presents preliminary fi ndings and is being distributed to economists and other interested readers solely to stimulate discussion and elicit comments. The views expressed in this paper are those of the authors and are not necessarily refl ective of views at the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the authors. An Analysis of OTC Interest Rate Derivatives Transactions: Implications for Public Reporting Michael Fleming, John Jackson, Ada Li, Asani Sarkar, and Patricia Zobel Federal Reserve Bank of New York Staff Reports, no. 557 March 2012; revised October 2012 JEL classifi cation: G12, G13, G18 Abstract This paper examines the over-the-counter (OTC) interest rate derivatives (IRD) market in order to inform the design of post-trade price reporting. Our analysis uses a novel transaction-level data set to examine trading activity, the composition of market participants, levels of product standardization, and market-making behavior. We fi nd that trading activity in the IRD market is dispersed across a broad array of product types, currency denominations, and maturities, leading to more than 10,500 observed unique product combinations. While a select group of standard instruments trade with relative frequency and may provide timely and pertinent price information for market partici- pants, many other IRD instruments trade infrequently and with diverse contract terms, limiting the impact on price formation from the reporting of those transactions. -

Modeling VXX

Modeling VXX Sebastian A. Gehricke Department of Accountancy and Finance Otago Business School, University of Otago Dunedin 9054, New Zealand Email: [email protected] Jin E. Zhang Department of Accountancy and Finance Otago Business School, University of Otago Dunedin 9054, New Zealand Email: [email protected] First Version: June 2014 This Version: 13 September 2014 Keywords: VXX; VIX Futures; Roll Yield; Market Price of Variance Risk; Variance Risk Premium JEL Classification Code: G13 Modeling VXX Abstract We study the VXX Exchange Traded Note (ETN), that has been actively traded in the New York Stock Exchange in recent years. We propose a simple model for the VXX and derive an analytical expression for the VXX roll yield. The roll yield of any futures position is the return not due to movements of the underlying, in commodity futures it is often called the cost of carry. Using our model we confirm that the phenomena of the large negative returns of the VXX, as first documented by Whaley (2013), which we call the VXX return puzzle, is due to the predominantly negative roll yield as proposed but never quantified in the literature. We provide a simple and robust estimation of the market price of variance risk which uses historical VXX returns. Our VXX price model can be used to study the price of options written on the VXX. Modeling VXX 1 1 Introduction There are three major risk factors which are traded in financial markets: market risk which is traded in the stock market, interest rate risk which is traded in the bond markets and interest rate derivative markets, and volatility risk which up until recently was only traded indirectly in the options market. -

Derivative Valuation Methodologies for Real Estate Investments

Derivative valuation methodologies for real estate investments Revised September 2016 Proprietary and confidential Executive summary Chatham Financial is the largest independent interest rate and foreign exchange risk management consulting company, serving clients in the areas of interest rate risk, foreign currency exposure, accounting compliance, and debt valuations. As part of its service offering, Chatham provides daily valuations for tens of thousands of interest rate, foreign currency, and commodity derivatives. The interest rate derivatives valued include swaps, cross currency swaps, basis swaps, swaptions, cancellable swaps, caps, floors, collars, corridors, and interest rate options in over 50 market standard indices. The foreign exchange derivatives valued nightly include FX forwards, FX options, and FX collars in all of the major currency pairs and many emerging market currency pairs. The commodity derivatives valued include commodity swaps and commodity options. We currently support all major commodity types traded on the CME, CBOT, ICE, and the LME. Summary of process and controls – FX and IR instruments Each day at 4:00 p.m. Eastern time, our systems take a “snapshot” of the market to obtain close of business rates. Our systems pull over 9,500 rates including LIBOR fixings, Eurodollar futures, swap rates, exchange rates, treasuries, etc. This market data is obtained via direct feeds from Bloomberg and Reuters and from Inter-Dealer Brokers. After the data is pulled into the system, it goes through the rates control process. In this process, each rate is compared to its historical values. Any rate that has changed more than the mean and related standard deviation would indicate as normal is considered an outlier and is flagged for further investigation by the Analytics team. -

Options Strategy Guide for Metals Products As the World’S Largest and Most Diverse Derivatives Marketplace, CME Group Is Where the World Comes to Manage Risk

metals products Options Strategy Guide for Metals Products As the world’s largest and most diverse derivatives marketplace, CME Group is where the world comes to manage risk. CME Group exchanges – CME, CBOT, NYMEX and COMEX – offer the widest range of global benchmark products across all major asset classes, including futures and options based on interest rates, equity indexes, foreign exchange, energy, agricultural commodities, metals, weather and real estate. CME Group brings buyers and sellers together through its CME Globex electronic trading platform and its trading facilities in New York and Chicago. CME Group also operates CME Clearing, one of the largest central counterparty clearing services in the world, which provides clearing and settlement services for exchange-traded contracts, as well as for over-the-counter derivatives transactions through CME ClearPort. These products and services ensure that businesses everywhere can substantially mitigate counterparty credit risk in both listed and over-the-counter derivatives markets. Options Strategy Guide for Metals Products The Metals Risk Management Marketplace Because metals markets are highly responsive to overarching global economic The hypothetical trades that follow look at market position, market objective, and geopolitical influences, they present a unique risk management tool profit/loss potential, deltas and other information associated with the 12 for commercial and institutional firms as well as a unique, exciting and strategies. The trading examples use our Gold, Silver -

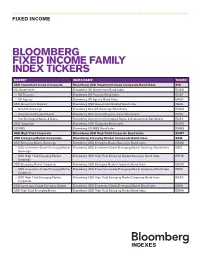

Bloomberg Fixed Income Family Index Tickers

///////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////// FIXED INCOME BLOOMBERG FIXED INCOME FAMILY INDEX TICKERS MARKET INDEX NAME TICKER USD Investment Grade Composite Bloomberg USD Investment Grade Composite Bond Index BIG US Government Bloomberg US Government Bond Index BUSG » US Treasury Bloomberg US Treasury Bond Index BUSY » US Agency Bloomberg US Agency Bond Index BAGY USD Government Related Bloomberg USD Government Related Bond Index BGRL » Non-US Sovereign Bloomberg Non-US Sovereign Bond Index BNSO » Government Regional/Local Bloomberg Government Regional/Local Bond Index BRGL » Gov Developed Banks & Supra Bloomberg Government Developed Banks & Supranational Bond Index BDEV USD Corporate Bloomberg USD Corporate Bond Index BUSC US MBS Bloomberg US MBS Bond Index BMBS USD High Yield Corporate Bloomberg USD High Yield Corporate Bond Index BUHY USD Emerging Market Composite Bloomberg Emerging Market Composite Bond Index BEM USD Emerging Market Sovereign Bloomberg USD Emerging Market Sovereign Bond Index BEMS » USD Investment Grade Emerging Market Bloomberg USD Investment Grade Emerging Market Sovereign Bond Index BEIS Sovereign » USD High Yield Emerging Market Bloomberg USD High Yield Emerging Market Sovereign Bond Index BEHS Sovereign USD Emerging Market Corporate Bloomberg USD Emerging Market Corporate Bond Index BEMC » USD Investment Grade Emerging Market Bloomberg USD Investment Grade Emerging Market Corporate Bond Index BIEM Corporate -

Bankruptcy Futures: Hedging Against Credit Card Default

CONSUMER LENDING Bankruptcy Futures: Hedging Against Credit Card Default by Russ Ray his article discusses the new bankruptcy futures contract to be launched by the Chicago Mercantile Exchange and examines the mechanics and contract specifications of this innovation, illus- trating its hedging potential in the process. ometime during the latter half of 1999 or early Credit-card debt is becoming particularly burden- 2000, the Chicago Mercantile Exchange intends some. The average credit-card balance is approximately to launch an innovative new futures contract that $2,500, with typical households having at least three dif- will offer consumer-lending institutions, particularly ferent bank cards. The average card holder also uses six credit-card issuers, a hedge against the bankruptcies additional cards at service stations, department stores, filed by their borrowers. Bankruptcy futures—contracts specialty stores, and other vendors issuing their own cred- to buy or sell a cash-valued index based upon the cur- it cards. rent number of actual bankruptcies—will enable con- Commensurate with such increases in consumer sumer lenders to transfer default risk to other lenders debt is an ever-growing rise in consumer bankruptcies, and/or speculators holding opposite expectations. which, in turn, represent an ever-increasing proportion Significantly, this new contract also constitutes a proxy of total bankruptcies. In 1998, 96.9% of all bankruptcy variable for banks' confidence in the value and liquidity filings were personal—not business—bankruptcies. (In of their own loan portfolios, just as other proxy vari- terms of dollar volume, however, businesses continue to ables now measure consumer and investor confidence. -

Derivative Securities

2. DERIVATIVE SECURITIES Objectives: After reading this chapter, you will 1. Understand the reason for trading options. 2. Know the basic terminology of options. 2.1 Derivative Securities A derivative security is a financial instrument whose value depends upon the value of another asset. The main types of derivatives are futures, forwards, options, and swaps. An example of a derivative security is a convertible bond. Such a bond, at the discretion of the bondholder, may be converted into a fixed number of shares of the stock of the issuing corporation. The value of a convertible bond depends upon the value of the underlying stock, and thus, it is a derivative security. An investor would like to buy such a bond because he can make money if the stock market rises. The stock price, and hence the bond value, will rise. If the stock market falls, he can still make money by earning interest on the convertible bond. Another derivative security is a forward contract. Suppose you have decided to buy an ounce of gold for investment purposes. The price of gold for immediate delivery is, say, $345 an ounce. You would like to hold this gold for a year and then sell it at the prevailing rates. One possibility is to pay $345 to a seller and get immediate physical possession of the gold, hold it for a year, and then sell it. If the price of gold a year from now is $370 an ounce, you have clearly made a profit of $25. That is not the only way to invest in gold. -

Interest Rate Derivaties and Asset

ank participation in derivative markets has risen sharply in recent years. The total amotmt of interest rate, currency, commodity, and B equity contracts at U.S. commercial and savings banks soared from $6.8 trillion in 1990 to $11.9 trillion in 1993, an increase of 75 percent. A major concern facing policymakers and bank regulators today is the possibility that the rising use of derivatives has increased the riskiness of individual banks and of the banking system as a whole. Banks have long used one type of derivative instrument, namely interest rate futures, to manage interest rate risk (Koppenhaver 1986; Booth, Smith, and Stoltz 1984; Parkinson and Spindt 1986; Franckle and Senchack 1982). However, the development of newer instruments, such as swaps, caps, collars, and floors (see the glossary in Box 1), has greatly expanded the menu of financial technologies available to banks for asset-liability management. In particular, interest rate swaps have be- come the preferred tool. According to a recent market survey of deriva- tive users, 92 percent of responding financial institutions report using interest rate swaps to manage the interest rate risk of their lending portfolios (Group of Thirty 1993, pp. 40-41). Katerina Simons More recently, studies have focused on the determinants of the broader derivative activities of banks. Sinkey and Carter (1994) studied the determinants of bank use of derivatives between 1989 and 1991. They Economist, Federal Reserve Bank of found that measures of maturity gap and liquidity are consistently Boston. The author thanks Richard significant across banks of different asset sizes. Brewer, Minton and Kopcke, Willimn Lang, and the partic- Moser (1994) focused on the relationship between derivative use and ipants in the se~ninars at the Federal bank lending, concluding that the growth of business lending is posi- Reserve Bank of Boston, the meetings tively related to the presence of swaps on the bank’s books, though the of the Atlantic Economic Society, and presence of futures had no significant effect on bank lending.