BP in Azerbaijan Baku September 2006 Cautionary Statement

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Project Financing of Cross-Border Pipelines a Presentation to the Energy Charter Workshop Brussels

The Project Financing of Cross-Border Pipelines a presentation to the Energy Charter Workshop Brussels by Rubin Weston Chadbourne & Parke 17 October 2006 Regis House, 45 King William Street London EC4R 9AN Tel: +44 (0) 20 7337 8031 [email protected] © 2006, CHADBOURNE & PARKE All Rights Reserved Chadbourne & Parke: Legal Leaders in Energy Representing EBRD on the $180 million and $170 million financings of LUKoil’s and SOCAR’s respective investments in the Shah Deniz gas field and the South Caucasus Gas Pipeline Representing SOCAR on a $750 million loan facility in respect of the repayment of carry financing provided by TPAO and Exxon in respect of the ACG oil field and the financing of future cash calls Representing IFC on a $82 million loan to SC Petrotel-Lukoil SA to finance the modernisation of its refinery in Ploesti, Romania Represented Black Sea Trade and Development Bank and IFC on the financing of the Galata Gas Field, located offshore of Varna, Bulgaria in the Black Sea, the first limited recourse upstream project financing in the Black Sea Represented Transneft on a US $150 million syndicated receivable based financing facility arranged by Raiffeisen, Transneft’s first syndicated loan Represented IFC on the financing for a portion of LUKoil’s share of development of the Karachaganak field, the largest limited recourse petroleum project financing in Kazakhstan Represented Nations Energy on a US $150 million syndicated financing arranged by CSFB for the development of the Karazhanbas oil field in Kazakhstan and the -

The Struggle for Democratic Environmental Governance Around

The struggle for democratic environmental governance around energy projects in post-communist countries: the role of civil society groups and multilateral development banks by Alda Kokallaj A thesis submitted to the Faculty of Graduate and Postdoctoral Affairs in partial fulfillment of the requirements for the degree of Doctor of Philosophy in Political Science Carleton University Ottawa, Ontario © 2014 Alda Kokallaj Abstract This dissertation focuses on the struggle for democratic environmental governance around energy projects in post-communist countries. What do conflicts over environmental implications of these projects and inclusiveness reveal about the prospects for democratic environmental governance in this region? This work is centred on two case studies, the Baku-Tbilisi-Ceyhan oil pipeline and the Vlora Industrial and Energy Park. These are large energy projects supported by the governments of Azerbaijan, Georgia and Albania, and by powerful international players such as oil businesses, multilateral development banks (MDBs), the European Union and the United States. Analysis of these cases is based on interviews with representatives of these actors and civil society groups, narratives by investigative journalists, as well as the relevant academic literature. I argue that the environmental governance of energy projects in the post-communist context is conditioned by the interplay of actors with divergent visions about what constitutes progressive development. Those actors initiating energy projects are shown to generally have the upper hand in defining environmental governance outcomes which align with their material interests. However, the cases also reveal that the interaction between civil society and MDBs creates opportunities for society at large, and for non-government organizations who seek to represent them, to have a greater say in governance outcomes – even to the point of stopping some elements of proposed projects. -

Azerbaijan 2021 Energy Policy Review Co-Funded by the European Union

Co-funded by the European Union Azerbaijan 2021 Energy Policy Review Co-funded by the European Union Azerbaijan 2021 Energy Policy Review INTERNATIONAL ENERGY AGENCY The IEA examines IEA member IEA association the full spectrum countries: countries: of energy issues including oil, gas Australia Brazil and coal supply and Austria China demand, renewable Belgium India energy technologies, Canada Indonesia electricity markets, Czech Republic Morocco energy efficiency, Denmark Singapore access to energy, Estonia South Africa demand side Finland Thailand management and France much more. Through Germany its work, the IEA Greece advocates policies Hungary that will enhance Ireland the reliability, Italy affordability and Japan sustainability of Korea energy in its 30 Luxembourg member countries, Mexico 8 association Netherlands countries and New Zealand beyond. Norway Poland Portugal Slovak Republic Spain Sweden Switzerland Turkey United Kingdom United States The European Commission also participates in the work of the IEA Please note that this publication is subject to specific restrictions that limit its use and distribution. The terms and conditions are available online at www.iea.org/t&c/ Source: IEA. All rights reserved. International Energy Agency Website: www.iea.org Foreword The International Energy Agency (IEA) has been conducting in-depth peer reviews of the energy policies of its member countries – and of other countries – since 1976, and it recently modernised these reviews to focus on some of the countries’ key energy transition and security challenges. FOREWORD Azerbaijan is one of the focus countries of the EU4Energy programme, which is carried out by the IEA and the European Union along with the Energy Community Secretariat and the Energy Charter Secretariat. -

Caspian Oil and Gas Complements Other IEA Studies of Major Supply Regions, Such As Middle East Oil and Gas and North African Oil and Gas

3 FOREWORD The Caspian region contains some of the largest undeveloped oil and gas reserves in the world. The intense interest shown by the major international oil and gas companies testifies to its potential. Although the area is unlikely to become “another Middle East”, it could become a major oil supplier at the margin, much as the North Sea is today. As such it could help increase world energy security by diversifying global sources of supply. Development of the region’s resources still faces considerable obstacles. These include lack of export pipelines and the fact that most new pipeline proposals face routing difficulties due to security of supply considerations,transit complications and market uncertainties. There are also questions regarding ownership of resources, as well as incomplete and often contradictory investment regimes. This study is an independent review of the major issues facing oil and gas sector developments in the countries along the southern rim of the former Soviet Union that are endowed with significant petroleum resources: Azerbaijan, Kazakstan,Turkmenistan and Uzbekistan. Caspian Oil and Gas complements other IEA studies of major supply regions, such as Middle East Oil and Gas and North African Oil and Gas. It also expands on other IEA studies of the area, including Energy Policies of the Russian Federation and Energy Policies of Ukraine. The study was undertaken with the co-operation of the Energy Charter Secretariat, for which I would like to thank its Secretary General, Mr. Peter Schütterle. Robert Priddle Executive Director 5 ACKNOWLEDGEMENTS The IEA wishes to acknowledge the very helpful co-operation of the Energy Charter Secretariat, with special thanks to Marat Malataev, Temuri Japaridze, Khamidulah Shamsiev and Galina Romanova. -

The Role of Greece in Europe's Southern Gas Corridor Strategy

Policy Paper / Κείμεμο Πολιτικής No 17 / February 2012 A Strategic Challenge: The role of Greece in Europe’s Southern Gas Corridor Strategy Dr. Thanos Dokos / Director General, ELIAMEP Dr. Theodoros Tsakiris / ELIAMEP Coordinator Geopolitics of Energy Programme 1 PP No 17 | February 2012 A Strategic Challenge: The role of Greece in Europe’s Southern Gas Corridor Strategy Thanos Dokos, Theodoros Tsakiris Copyright © 2012 Hellenic Foundation for European & Foreign Policy (ELIAMEP) 49, Vas. Sofias Ave, 106 76 Athens, Greece Tel.: +30 210 7257 110 | Fax: +30 210 7257 114 | www.eliamep.gr | [email protected] All Rights Reserved A Strategic Challenge: The role of Greece in Europe’s Southern Gas Corridor Strategy by Dr. Thanos Dokos / Director General, ELIAMEP Dr. Theodoros Tsakiris / Coordinator ELIAMEP Geopolitics of Energy Programme with the contribution of Dr. Ioannis Armakolas, “STAVROS COSTOPOULOS” Research Fellow ELIAMEP offers a forum for debate on international and European issues. Its non-partisan character supports the right to free and well documented discourse. ELIAMEP publications aim to contribute to scholarly knowledge and to provide policy relevant analyses. As such, they solely represent the views of the author(s) and not necessarily those of the Foundation. 2 Table of Contents Executive Summary .......................................................................................................................................5 Main conclusions ...........................................................................................................................................5 -

BP in Azerbaijan Sustainability Report 2007

BP in Azerbaijan Sustainability Report 2007 About this report The 2007 BP in Azerbaijan Sustainability Report covers our business 1 Foreword by the president of BP performance, environmental record and wider role in Azerbaijan during 2007. Azerbaijan Strategic Performance This is our fifth Sustainability Report and it reflects feedback we received about Unit (SPU) previous reports. Our earlier publications are available at www.bp.com/caspian. 2 Country context By 'sustainability' we mean the capacity to endure as a commercial organisation by 3 Achievements and challenges 4 Report concept, scope and renewing assets and by creating and delivering better products and services so that process we meet the evolving needs of society, attract successive generations of employees, 5 BP Azerbaijan SPU interests contribute to a sustainable environment and retain the trust and support of our 6 Chapter 1 – BP in Azerbaijan: customers, shareholders and the communities in which we operate. our operations 7 BP in Azerbaijan at a glance References in this report to 'us', 'we' and 'our' relate to BP in Azerbaijan unless otherwise stated. Specific ref- 10 BP in Azerbaijan in perspective erences to 'BP' and the 'BP group' mean BP p.l.c., its subsidiaries and affiliates. Unless otherwise specified, 11 Dialogue and engagement the text does not distinguish between the operations and activities of BP p.l.c. and those of its subsidiaries 14 Our projects and operations and affiliates. 20 Operating responsibly: - HSE management system - Safety A message from Ernst & Young - Environment This report has been substantiated by Ernst & Young, the BP group auditors. The - Health primary purpose of the report substantiation process is to test that the asser- 32 Security and human rights tions, claims and data set out in the text regarding BP’s sustainability perform- 34 People, compliance and ethics ance can be supported by evidence. -

Energy and Security Cooperation in Asia Challenges and Prospects

!"#$%&'(")'*#+,$-.&' /001#$(.-0"'-"'23-(' /4(55#"%#3'(")'6$031#+.3' !)-.#)'7&' /4$-3.014#$'8#"' 259-"'/4#:' Energy and Security Cooperation in Asia Challenges and Prospects Christopher Len Alvin Chew Editors Institute for Security and Development Policy Västra Finnbodavägen 2, 13130 Stockholm-Nacka, Sweden www.isdp.eu Energy and Security Cooperation in Asia: Challenges and Prospects is a Monograph published by the Institute for Security and Development Policy. Monographs provide comprehensive analyses of key issues presented by leading experts. The Institute is based in Stockholm, Sweden, and cooperates closely with research centers worldwide. Through its Silk Road Studies Program, the Institute runs a joint Transatlantic Research and Policy Center with the Central Asia-Caucasus Institute of Johns Hopkins Universi- ty’s School of Advanced International Studies. The Institute is firmly established as a leading research and policy center, serving a large and diverse community of analysts, scholars, policy-watchers, business leaders, and journalists. It is at the forefront of re- search on issues of conflict, security, and development. Through its applied research, publications, research cooperation, public lectures, and seminars, it functions as a focal point for academic, policy, and public discussion. This publication is kindly made possible by support from the Swedish Ministry for For- eign Affairs. The opinions and conclusions expressed are those of the author/s and do not necessarily reflect the views of the Institute for Security and Development Policy or its sponsors. © Institute for Security and Development Policy, 2009 ISBN: 978-91-85937-59-2 Printed in Singapore Cover Photo Credit: Data courtesy of Marc Imhoff of NASA GSFC and Christopher El- vidge of NOAA NGDC. -

The Outlook for Azerbaijani Gas Supplies to Europe: Challenges and Perspectives

June 2015 The Outlook for Azerbaijani Gas Supplies to Europe: Challenges and Perspectives OIES PAPER: NG 97 Gulmira Rzayeva OIES Research Associate The contents of this paper are the authors’ sole responsibility. They do not necessarily represent the views of the Oxford Institute for Energy Studies or any of its members. Copyright © 2015 Oxford Institute for Energy Studies (Registered Charity, No. 286084) This publication may be reproduced in part for educational or non-profit purposes without special permission from the copyright holder, provided acknowledgment of the source is made. No use of this publication may be made for resale or for any other commercial purpose whatsoever without prior permission in writing from the Oxford Institute for Energy Studies. ISBN 978-1-78467-028-3 i April 2015: The Outlook for Azerbaijani Gas Supplies to Europe Contents Preface ................................................................................................................................................... v Acknowledgements ............................................................................................................................. vi Introduction ........................................................................................................................................... 1 1. Natural Gas in Azerbaijan – Historical Context .......................................................................... 4 The first stage of Azerbaijan’s oil and gas history (1846-1920)...................................................... -

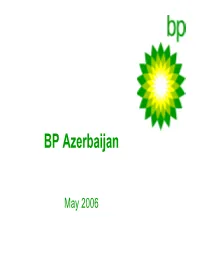

BP Azerbaijan

BP Azerbaijan May 2006 BP Azerbaijan Interests 1998 - 2022 ACG Gross Production Novorossiysk Russia 1400 1200 k 1000 DWG Kaza hstan 800 Black Sea NREP 600 mbd Pipeline 400 Azeri Georgia PSC 200 Exploration 0 1998 2002 2006 2010 2014 2018 2022 Turkey License Georgia WREP 3534 Tbilisi Pipeline Caspian Sea Exploration Supsa Turkmenistan Sangachal Terminal ACG Oil Production South Caucasus Baku BTC Pipeline Oil Pipeline Gas & Development Azerbaijan Shah Deniz Gas Development Turkey Erzurum Inam Exploration 1998 - 2022 Shah Deniz Gross Production Alov Exploration 400 350 300 250 Stage 2 Ceyhan 200 mbd 150 100 Stage 1 Iran 50 d. e 0 M a Se 1998 2002 2006 2010 2014 2018 2022 Syria 0 100 200 300 km Iraq ACG Early Oil Project First oil Nov 1997 2005 production - exported 140 mbd gross 2005 Lifting and transportation cost ~$1.60/bbl Total investment ~$2.2bn RUSSIA Chirag platform Northern Route Chirag platform Export Pipeline Novorossiysk NER Supsa GEORGIA Chirag Tbilisi WER Platform Oil Rocks AZERBAIJAN Baku ARMENIA Western Route Export Pipeline Sangachal Terminal Chirag-1 Platform Sangachal EOP terminal 2 Project Schedule 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 ACG PSA First Oil Early Oil Project First Oil C&WP Start-up Central Azeri & C&WP First Oil WA First Oil EA West & East Azeri First Oil WA First Oil ACG Phase 3 Ceyhan Lifting BTC Shah Deniz PSA First Gas to Turkey Shah Deniz St1 Appraise Select Define Execute PSA signed / Sanction CVP gate Operation 6 5 4 Capex 3 2 1 ($billion) 0 1993 1994 1995 1996 -

Rupert Herbert-Burns Phd Thesis

PETROLEUM GEOPOLITICS : A FRAMEWORK OF ANALYSIS Rupert Herbert-Burns A Thesis Submitted for the Degree of PhD at the University of St Andrews 2012 Full metadata for this item is available in Research@StAndrews:FullText at: http://research-repository.st-andrews.ac.uk/ Please use this identifier to cite or link to this item: http://hdl.handle.net/10023/4035 This item is protected by original copyright Petroleum Geopolitics: A Framework of Analysis Rupert Herbert-Burns A Thesis Submitted for the Degree of Ph.D at the University of St. Andrews April 2011 Abstract The playing field upon which actors, both state and non-state, develop strategies to secure existing supplies of oil and seek access to new ones is as systemically, politically and strategically complex is as it is geographically vast. In considering this activity, the terminology used by pundits and journalists to describe the significance of issues such as oil demand, the complexities of access to petroleum and concerns over security threats to supplies of oil is familiar. Juxtapositions such as the ‘geopolitics of oil’, ‘energy geopolitics’, the ‘geopolitics of resource wars’ and the ‘geopolitics of oil and gas’ are all familiar. But what do they mean when they use ‘geopolitics’ in this context? Thus, by extension, can petroleum geopolitics - a hybrid conceptual construction used in this thesis - be disassembled into its component parts, analysed and systematically understood. This is the aim of this thesis. This thesis contends that the very nature of oil and gas reserves, the processes of exploration and production, and the means that govern and characterise the transportation of petroleum overland and by sea is inherently geopolitical - that some core features of geopolitical theory and key geopolitical concepts are pivotal in determining the ontology and process of the international oil business. -

Environment We Recognize That Managing Environmental Impacts Is an Essential Part of What It Means to Responsibly Produce Oil and Gas

Environment We recognize that managing environmental impacts is an essential part of what it means to responsibly produce oil and gas. What we are doing Environmental management 27 Advancing low carbon 27 Discharges and waste management 29 Environmental monitoring 31 26 bp in Azerbaijan Sustainability Report 2019 Overview Our operations Our people Safety Environment Society Our Performance Environmental management bp works to avoid, minimize and mitigate environmental impacts wherever we do business. In 2019, we continued to maintain the certification of our operations in accordance with the ISO14001 A crew worker checks gas pipes with hand-held Environmental Management Systems infrared camera to detect leak on board the Shah Deniz Alpha platform. standard and our Compliance Management System. We also further Gross flaring by asset Gross GHG emissions expanded our certification scope (thousand tonnes) 3,699 to cover a number of newly built 4,000 3,830 3,543 3,399 3,331 9.77 operational facilities of the new gas 3,500 300 9.60 export chain. These included Shah 3,000 9.60 9.54 Deniz Bravo platforms, Shah Deniz 2 2,500 250 area of the Sangachal terminal and the 2,000 15.4 1,500 SCPX gas export pipeline. 11.9 8.89 200 1,000 15.8 56.6 3.1 500 Our environmental self-verification 42.4 5.2 3.6 9.9 28.0 2015 2016 2017 2018 2019 processes help us control actual 160 20.4 18.2 17.4 19.4 39.0 21.5 7.8 10.7 16.9 operational activities and identify 12.6 Gross direct GHG, thousand tonnes 9.1 9.3 53.1 33.5 5.8 100 28.7 61.5 areas for improvement. -

The First Sustainability Report Published by Tekfen Holding Co., Inc. (Tekfen

The first sustainability report published by Tekfen Tekfen Holding Sustainability Report 2018 Holding Co., Inc. (Tekfen), presents information about Tekfen’s sustainability priorities and performance. Strategic material issues identified in light of stakeholder values and company strategies provided the framework for this report. Tekfen’s goal is to continue keeping its stakeholders transparently informed on an annual basis about its sustainability vision, targets, and performance. This report has been prepared in accordance with the GRI Standards: Core option and it presents information supplied by Tekfen Holding, the Tekfen Contracting Group (Tekfen Construction, Tekfen Engineering, Tekfen Manufacturing), the Tekfen Agri- industry Group (Toros Tarım), the Tekfen Real Estate Development Group (Tekfen Real Estate, Tekfen Tourism), and Tekfen Insurance.1 Although this report covers the period 1 January 2018 to 31 December 2018, it also includes data from previous years so that comparisons may be made. Data sets other than those pertaining to environmental performance cover Tekfen operations in all countries. In order to ensure compliance with Carbon Disclosure Project (CDP) climate change and water reporting standards, environmental-performance data cover the group’s Turkish operations. Tekfen Tarım is included in the 2018 environmental performance data set. Kültür Mahallesi, Budak Sokak No: 7 Tekfen Sitesi A Blok 34340, Ulus – Beşiktaş / İstanbul, Turkey Please send any opinions and/or suggestions you may P: (90.212) 359 33 00 F: (90.212) 359 33 05 have about our sustainability reporting to www.tekfen.com.tr [email protected] Tekfen Holding Sustainability Report 2018 www.tekfen.com.tr Ticari Sicil No: 111233 2018 TEKFEN 1 Bridging Prosperity Contents The first sustainability report published byTekfen Holding Co., Inc.