The Case for Open-Market Purchases in a Liquidity Trap

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Understanding Open Market Operations

Foreword The Federal Reserve Bank of New York is responsible for Michael Akbar Akhtar, vice president of the day-to-day implementation of the nation’s monetary pol- Federal Reserve Bank of New York, leads the reader— icy. It is primarily through open market operations—pur- whether a student, market professional or an interested chases or sales of U.S. Government securities in the member of the public—through various facets of mone- open market in order to add or drain reserves from the tary policy decision-making, and offers a general per- banking system—that the Federal Reserve influences spective on the transmission of policy effects throughout money and financial market conditions that, in turn, the economy. affect output, jobs and prices. Understanding Open Market Operations pro- This edition of Understanding Open Market vides a nontechnical review of how monetary policy is Operations seeks to explain the challenges in formulat- formulated and executed. Ideally, it will stimulate read- ing and implementing U.S. monetary policy in today’s ers to learn more about the subject as well as enhance highly competitive financial environment. The book high- appreciation of the challenges and uncertainties con- lights the broad and complex set of considerations that fronting monetary policymakers. are involved in daily decisions for open market opera- William J. McDonough tions and details the steps taken to implement policy. President Understanding Open Market Operations / i Acknowledgment Much has changed in U.S. financial markets and institu- Partlan for extensive comments on drafts; and to all of tions since 1985, when the last edition of Open Market the Desk staff for graciously and patiently answering my Operations, written by Paul Meek, was published. -

Payment System Disruptions and the Federal Reserve Followint

Working Paper Series This paper can be downloaded without charge from: http://www.richmondfed.org/publications/ Payment System Disruptions and the Federal Reserve Following September 11, 2001† Jeffrey M. Lacker* Federal Reserve Bank of Richmond, Richmond, Virginia, 23219, USA December 23, 2003 Federal Reserve Bank of Richmond Working Paper 03-16 Abstract The monetary and payment system consequences of the September 11, 2001, terrorist attacks are reviewed and compared to selected U.S. banking crises. Interbank payment disruptions appear to be the central feature of all the crises reviewed. For some the initial trigger is a credit shock, while for others the initial shock is technological and operational, as in September 11, but for both types the payments system effects are similar. For various reasons, interbank payment disruptions appear likely to recur. Federal Reserve credit extension following September 11 succeeded in massively increasing the supply of banks’ balances to satisfy the disruption-induced increase in demand and thereby ameliorate the effects of the shock. Relatively benign banking conditions helped make Fed credit policy manageable. An interbank payment disruption that coincided with less favorable banking conditions could be more difficult to manage, given current daylight credit policies. Keywords: central bank, Federal Reserve, monetary policy, discount window, payment system, September 11, banking crises, daylight credit. † Prepared for the Carnegie-Rochester Conference on Public Policy, November 21-22, 2003. Exceptional research assistance was provided by Hoossam Malek, Christian Pascasio, and Jeff Kelley. I have benefited from helpful conversations with Marvin Goodfriend, who suggested this topic, David Duttenhofer, Spence Hilton, Sandy Krieger, Helen Mucciolo, John Partlan, Larry Sweet, and Jack Walton, and helpful comments from Stacy Coleman, Connie Horsley, and Brian Madigan. -

Money Supply ECON 40364: Monetary Theory & Policy

Money Supply ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 59 Readings I Mishkin Ch. 3 I Mishkin Ch. 14 I Mishkin Ch. 15, pg. 341-348 2 / 59 Money I Money is defined as anything that is accepted as payments for goods or services or in the repayment of debts I Money serves three functions: 1. Medium of exchange 2. Unit of account 3. Store of value I Any asset can serve as a store of value (e.g. house, land, stocks, bonds), but most assets do not perform the first two roles of money I Money is a stock concept { how much money you have (in your wallet, in the bank) at a given point in time. Income is a flow concept 3 / 59 Roles of Money I Medium of exchange role is the most important role of money: I Eliminates need for barter, reduces transactions costs associated with exchange, and allows for greater specialization I Unit of account is important (particularly in a diverse economy), though anything could serve as a unit of account I As a store of value, money tends to be crummy relative to other assets like stocks and houses, which offer some expected return over time I An advantage money has as a store of value is its liquidity I Liquidity refers to ease with which an asset can be converted into a medium of exchange (i.e. money) I Money is the most liquid asset because it is the medium of exchange I If you held all your wealth in housing, and you wanted to buy a car, you would have to sell (liquidate) the house, which may not be easy to do, may take a while, and may involve selling at a discount if you must do it quickly 4 / 59 Evolution of Money and Payments I Commodity money: money made up of precious metals or other commodities I Difficult to carry around, potentially difficult to divide, price may fluctuate if precious metal or commodity has consumption value independent of medium of exchange role I Paper currency: pieces of paper that are accepted as medium of exchange. -

Open Market Operations and Money Supply at Zero Nominal Interest Rates

Open Market Operations and Money Supply at Zero Nominal Interest Rates Roberto Robatto∗ University of Chicago October 21, 2012 (first draft: February 2012) Abstract What are the paths of money supply that are consistent with zero nominal interest rates and that can be implemented through open market operations? To answer this question, I present an Irrelevance Proposition for some open market operations that exchange money and one-period bonds at the zero lower bound. The result has implications for the conduct of monetary policy (non-irrelevant open market operations modify the equilibrium) and for the implementation of the Friedman rule (any growth rate of money supply above the negative of the rate of time preferences can implement zero nominal interest rate forever, even a positive growth rate, provided that the government collects \large enough" surpluses). The result holds under several specifications, including models with heterogeneity, non- separable utility, borrowing constraints, incomplete and segmented markets and sticky prices; and generalizes to any situation in which the cost of holding money vs. bonds is zero, such as the payment of interest on money. ∗Email: [email protected]. I am extremely greatful to Fernando Alvarez for his suggestions and guidance. I would like to thank also John Cochrane, Thorsten Drautzburg, Tom Sargent, Harald Uhlig and participants to the AMT, Capital Theory and Economic Dynamics Working Groups at the University of Chicago for their comments. 1 1 Introduction At zero nominal interest rates, money is perfect substitutes for bonds from the point of view of the private sector. Money demand is thus not uniquely determined, therefore the equilibrium in the money market depends on the supply of money. -

Effect of Open Market Operations (OMO) on Economic Development, 1986 -2016

International Journal of Economics and Financial Management Vol. 3 No. 2 2018 ISSN: 2545 - 5966 www.iiardpub.org Effect of Open Market Operations (OMO) on Economic Development, 1986 -2016. Richard Osadume (Ph.D, FCIB) Nigeria Maritime University, Warri, Nigeria [email protected] [email protected] Abstract This Study examined the Effect of Open Market Operations (OMO) on Economic Development (1986-2016). The objective of this study was to examine the Effect of – Treasury Bills rates and Treasury Certificates rates on economic development. The study employed secondary data and used Nigeria as its sample; the investigation employed the OLS, Co-integration, Granger- causality and ECM Analytical techniques, to test the impact of the independent variables (treasury bill rates and treasury certificate rates) on the dependent variable, economic development (proxied by Human Development index) and tested at the 5% level of significance. The findings showed that Open Market Operations captured by Treasury Bills and treasury certificates, both had no significant effect on economic development in the short-run but showed a positive and significant effect in the long-run period on economic development with significant speed of adjustments. The study concludes that Central Bank Open Market Operations represented by Treasury Bills and Treasury Certificates do exert significant effect in the long-run on economic development and recommends amongst others the creation of adequate product awareness by the monetary authorities to raise public patronage of these financial products and also, to allow enough operational time lag to enable relevant formulated policies achieve their desired objectives. Key Word: Treasury Bills; Treasury Certificate Rates; Human Development index; Economic development; Open Market Operations. -

Managing the Fragility of the Eurozone

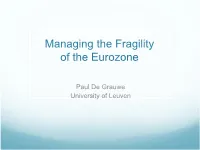

Managing the Fragility of the Eurozone Paul De Grauwe University of Leuven Paradox Gross government debt (% of GDP) 100 90 UK 80 Spain 70 60 50 40 30 20 10 0 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 10-Year-Government Bond Yields UK-Spain 6 5.5 SPAIN 5 4.5 4 percent 3.5 UK 3 2.5 2 Nature of monetary union Members of monetary union issue debt in currency over which they have no control. It follows that: Financial markets acquire power to force default on these countries Not so in countries that are not part of monetary union, and have kept control over the currency in which they issue debt. Consider case of UK and Spain UK Case Suppose investors fear default of UK government They sell UK govt bonds (yields increase) Proceeds of sales are presented in forex market Sterling drops UK money stock remains unchanged maintaining pool of liquidity that will be reinvested in UK govt securities If not Bank of England can be forced to buy UK govt bonds Investors cannot trigger liquidity crisis for UK government and thus cannot force default (Bank of England is superior force) Investors know this: thus they will not try to force default. Spanish case Suppose investors fear default of Spanish government They sell Spanish govt bonds (yields increase) Proceeds of these sales are used to invest in other eurozone assets No foreign exchange market and floating exchange rate to stop this Spanish money stock declines; pool of liquidity for investing in Spanish govt bonds shrinks No Spanish central bank that can be forced to buy Spanish government bonds Liquidity crisis possible: Spanish government cannot fund bond issues at reasonable interest rate Can be forced to default Investors know this and will be tempted to try Situation of Spain is reminiscent of situation of emerging economies that have to borrow in a foreign currency. -

Nber Working Paper Series Monetary Policy in the Information Economy

NBER WORKING PAPER SERIES MONETARY POLICY IN THE INFORMATION ECONOMY Michael Woodford Working Paper 8674 http://www.nber.org/papers/w8674 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 December 2001 Prepared for the “Symposium on Economic Policy for the Information Economy,” Federal Reserve Bank of Kansas City, Jackson Hole, Wyoming, August 30-September 1, 2001. I am especially grateful to Andy Brookes (RBNZ), Chuck Freedman (Bank of Canada), and Chris Ryan (RBA) for their unstinting efforts to educate me about the implementation of monetary policy at their respective central banks. Of course, none of them should be held responsible for the interpretations offered here. I would also like to thank David Archer, Alan Blinder, Kevin Clinton, Ben Friedman, David Gruen, Bob Hall, Spence Hilton, Mervyn King, Ken Kuttner, Larry Meyer, Hermann Remsperger, Lars Svensson, Bruce White and Julian Wright for helpful discussions, Gauti Eggertsson and Hong Li for research assistance, and the National Science Foundation for research support through a grant to the National Bureau of Economic Research. The views expressed herein are those of the author and not necessarily those of the National Bureau of Economic Research. © 2001 by Michael Woodford. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full credit, including © notice, is given to the source. Monetary Policy in the Information Economy Michael Woodford NBER Working Paper No. 8674 December 2001 JEL No. E58 ABSTRACT This paper considers two challenges that improvements in private-sector information-processing capabilities may pose for the effectiveness of monetary policy. -

Explain How the Federal Reserve and the Banking System Create Money (I.E., the Supply of Money) Explain the Factors That Affect the Demand for Money.”

Macroeconomics Topic 6: “Explain how the Federal Reserve and the banking system create money (i.e., the supply of money) Explain the factors that affect the demand for money.” Reference: Gregory Mankiw’s Principles of Macroeconomics, 2nd edition, Chapter 15. The Banking System and the Money Supply The Federal Reserve System, also known simply as the Fed, is the central bank of the United State. The Fed has several important functions such as, supplying the economy with currency, holding deposits of banks, lending money to banks, regulating the money supply and supervising the banking system. Most modern economies are based on a fractional-reserve banking system. Fractional reserve banking is designed to assure that banks have enough liquid assets (reserves) on hand to satisfy the normal withdrawals made from checking account deposits. Actual Bank Reserves = Bank deposits held at the Fed. + Bank Vault Cash. Both of these assets are readily available to satisfy customer withdrawals or transfer to other banks as customers write checks. The Fed. establishes a Required Reserve Ratio which is the percentage of checkable account deposits that the banks are required to hold as reserves. Thus the Minimum required reserves = Required Reserve Ratio X Checkable deposits. Money Creation with Fractional-Reserve Banking The money supply is made up of the currency in circulation outside of banks, and the level of checkable deposits in the banking system. To see how banks create money, lets assume we have an economy without a banking system and this economy has $1000 in currency, so the total money supply is $1000. Now suppose someone opens a bank called First Local Bank (FLB) and people in this economy deposit all the money they have at FLB. -

An Introduction to Us Monetary Policy

AN INTRODUCTION TO US MONETARY POLICY _____________________ Monetary policy is critical for policymakers to understand because their mistakes can cause enor- mous suffering. On one hand, not creating enough money to satisfy public demand can lead to mas- sive deflation, such as the kind that turned a recession in the early 1930s into the Great Depression. On the other hand, creating more money than the public demands can lead to serious inflation, like the inflation the United States experienced in the 1970s and early 1980s. In a study for the Mercatus Center at George Mason University, Senior Affiliated Scholar Steven Horwitz examines the history and evolution of the Federal Reserve System (Fed), as well as the tools it uses. The study also considers alternatives to the current discretionary monetary regime and evaluates their potential for providing a stable monetary framework. To read the entire study and learn more about its author, see “An Introduction to US Monetary Policy.” BACKGROUND Financial panics in the 1800s gave rise to a narrative that a lack of regulation led banks to engage in behavior that harmed customers and caused recessions. This view is incorrect: it was onerous state regulations that made small, underdiversified banks prone to failure in the face of an economic downturn. Even though this was a misperception, Congress passed the Federal Reserve Act of 1913, which created a “decentralized central bank” consisting of 12 districts and a weak oversight board. Over time, the Fed has evolved to play a critical role in managing the US money supply and acting as a lender of last resort to financial institutions. -

Unit 4 Practice Quiz #2 KEY

AP Macroeconomics Unit 4 Practice Quiz #2 KEY _ 1. When the price level falls, the number of dollars needed to buy a representative basket of goods a. increases, so the value of money rises. b. increases, so the value of money falls. c. decreases, so the value of money rises. d. decreases, so the value of money falls. 2. The supply of money is determined by a. the price level. b. the Treasury and Congressional Budget Office. c. the Federal Reserve System. d. the demand for money. 3. The velocity of money is a. the rate at which the Fed puts money into the economy. b. the same thing as the long-term growth rate of the money supply. c. the money supply divided by nominal GDP. d. the average number of times per year a dollar is spent. 4. According to the monetarist economists, which of the following is not influenced by monetary factors? a. nominal GDP and nominal interest rates b. real wages and real GDP c. the price level and nominal GDP d. None of the above is correct. 5. According to the equation of exchange (monetarism), (MV = PY) when the money supply doubles, which of the following also double? a. the price level and nominal wages b. the price level, but not the nominal wage c. the nominal wage, but not the price level d. neither the nominal wage nor the price level 6. The principle of monetary neutrality implies that an increase in the money supply will a. increase real GDP and the price level. -

Effects of Open Market Operations and Foreign Exchange Market Operations Under Flexible Exchange Rates

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: The International Transmission of Inflation Volume Author/Editor: Michael R. Darby, James R. Lothian and Arthur E. Gandolfi, Anna J. Schwartz, Alan C. Stockman Volume Publisher: University of Chicago Press Volume ISBN: 0-226-13641-8 Volume URL: http://www.nber.org/books/darb83-1 Publication Date: 1983 Chapter Title: Effects of Open Market Operations and Foreign Exchange Market Operations under Flexible Exchange Rates Chapter Author: Dan Lee Chapter URL: http://www.nber.org/chapters/c6134 Chapter pages in book: (p. 349 - 379) 12 Effects of Open Market Operations and Foreign Exchange Market Operations under Flexible Exchange Rates Dan Lee During the period of pegged exchange rates under the Bretton Woods Agreement, attention was directed to the problems of capital and reserve flows in the literature of international monetary economics. One relevant question was whether an individual country can conduct an independent monetary policy under fixed exchange rates. After the collapse of this system in the early seventies, attention was diverted to the determination of exchange rates and the workings of the flexible exchange-rate system. At least in theory, it seems that we finally have independent monetary policies. This chapter examines one of the topics in this still developing field, namely the relative effects of the two alternative instruments, open market operations (OMO) and foreign exchange market operations (FXO), in a small open economy. This topic is of great importance to policymakers who are faced with various policy targets and have two alternative instruments. -

Open Market Operations in English Central Banking

389 Open Market Operations in English Central Banking By R. S. Sayers London School of Economics I. The business of a central bank is to influence the behaviour of the country's financial institutions in the interest of the broad economic policy of the govern ment. The most appropriate way for it to function depends upon the nature of the financial institutions it is called upon to influence, and the economic policy whose furtherance is its ultimate purpose. There is consequently no standard pattern of central banking: indeed it is scarcely an exaggeration to say that there are as many kinds of central banks as there are countries. I make no attempt to describe a common pattern; still less to suggest that there is some ideal form to which all central banks should strive to conform. My purpose is simply to describe and comment upon a certain part of the work of the British central bank, bearing in mind that this central bank works in a highly-developed financial system, and that here in Switzerland also there is a highly-develop ed financial system but no parallel operations by the central bank1. The system of which the Bank of England is the centre consists of a small group of giant banks, having branches more or less throughout the country, together with an extensive fringe of smaller banks. Of these fringe banks, some are confined to parts of the U. K. but most of them have their principal interests in other parts of the Sterling Area. At the centre, that is to say in London, is a unique band of institutions which compose the London Discount Market.