Carbon Disclosure Project Transport Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

First Half of Fiscal Year Ending March 31, 2020 (FY2019) November 14, 2019 Results Presentation Keisei Electric Railway Co., Ltd

First Half of Fiscal Year Ending March 31, 2020 (FY2019) November 14, 2019 Results Presentation Keisei Electric Railway Co., Ltd. Contents 1. Consolidated Results for First Half of Fiscal Year Ending March 31, 2020 2. Consolidated Results Forecast for Fiscal Year Ending March 31, 2020 3. Progress in E4 Plan 4. Reference Material Copyright © Keisei Electric Railway Co., Ltd. 1 1-1. Overview of Results (Year on Year) Operating revenue, operating income, ordinary income, and net profit attributable to owners of parent posted record highs. FY2019 H1 FY2018 H1 % ■ Changes in operating revenue (by segment) Unit: million yen Million yen, % Change Result Result Change 3,353 327 Operating revenue 138,007 129,916 8,090 6.2 1,881 367 -514 3,078 Operating income 19,117 17,746 1,371 7.7 -403 138,007 (Operating income margin) 13.9 13.7 0.2pt - 129,916 Ordinary income FY2018FY2018 H1TransportationDistributionDistribution Real Leisure,Leisure, Construction OtherOther EliminationFY2019FY2019 H1 28,431 26,890 1,541 5.7 H1 Estate ServiceService H1 Share of profit of entities accounted for 9,770 9,799 -28 -0.3 using equity method ■ Changes in operating income (by segment) Unit: million yen Net profit attributable to owners of parent 21,176 20,520 655 3.2 277 67 1,165 -86 Depreciation 13,555 12,656 899 7.1 -46 151 19,117 -156 17,746 FY2018FY2018 TransportationH1 TransportationDistributionDistributionRealReal Estate Leisure,Leisure, Construction Construction OtherOther EliminationEliminationFY2019FY2019 H1 H1 Estate ServiceService H1 Copyright © Keisei Electric Railway Co., Ltd. 2 1-2. Overview of Results [Consolidated Balance Sheet/Consolidated Cash Flows] • The equity ratio increased due to an increase in shareholders’ equity. -

East Japan Railway Company Shin-Hakodate-Hokuto

ANNUAL REPORT 2017 For the year ended March 31, 2017 Pursuing We have been pursuing initiatives in light of the Group Philosophy since 1987. Annual Report 2017 1 Tokyo 1988 2002 We have been pursuing our Eternal Mission while broadening our Unlimited Potential. 1988* 2002 Operating Revenues Operating Revenues ¥1,565.7 ¥2,543.3 billion billion Operating Revenues Operating Income Operating Income Operating Income ¥307.3 ¥316.3 billion billion Transportation (“Railway” in FY1988) 2017 Other Operations (in FY1988) Retail & Services (“Station Space Utilization” in FY2002–2017) Real Estate & Hotels * Fiscal 1988 figures are nonconsolidated. (“Shopping Centers & Office Buildings” in FY2002–2017) Others (in FY2002–2017) Further, other operations include bus services. April 1987 July 1992 March 1997 November 2001 February 2002 March 2004 Establishment of Launch of the Launch of the Akita Launch of Launch of the Station Start of Suica JR East Yamagata Shinkansen Shinkansen Suica Renaissance program with electronic money Tsubasa service Komachi service the opening of atré Ueno service 2 East Japan Railway Company Shin-Hakodate-Hokuto Shin-Aomori 2017 Hachinohe Operating Revenues ¥2,880.8 billion Akita Morioka Operating Income ¥466.3 billion Shinjo Yamagata Sendai Niigata Fukushima Koriyama Joetsumyoko Shinkansen (JR East) Echigo-Yuzawa Conventional Lines (Kanto Area Network) Conventional Lines (Other Network) Toyama Nagano BRT (Bus Rapid Transit) Lines Kanazawa Utsunomiya Shinkansen (Other JR Companies) Takasaki Mito Shinkansen (Under Construction) (As of June 2017) Karuizawa Omiya Tokyo Narita Airport Hachioji Chiba 2017Yokohama Transportation Retail & Services Real Estate & Hotels Others Railway Business, Bus Services, Retail Sales, Restaurant Operations, Shopping Center Operations, IT & Suica business such as the Cleaning Services, Railcar Advertising & Publicity, etc. -

Pdf/Rosen Eng.Pdf Rice fields) Connnecting Otsuki to Mt.Fuji and Kawaguchiko

Iizaka Onsen Yonesaka Line Yonesaka Yamagata Shinkansen TOKYO & AROUND TOKYO Ōu Line Iizakaonsen Local area sightseeing recommendations 1 Awashima Port Sado Gold Mine Iyoboya Salmon Fukushima Ryotsu Port Museum Transportation Welcome to Fukushima Niigata Tochigi Akadomari Port Abukuma Express ❶ ❷ ❸ Murakami Takayu Onsen JAPAN Tarai-bune (tub boat) Experience Fukushima Ogi Port Iwafune Port Mt.Azumakofuji Hanamiyama Sakamachi Tuchiyu Onsen Fukushima City Fruit picking Gran Deco Snow Resort Bandai-Azuma TTOOKKYYOO information Niigata Port Skyline Itoigawa UNESCO Global Geopark Oiran Dochu Courtesan Procession Urabandai Teradomari Port Goshiki-numa Ponds Dake Onsen Marine Dream Nou Yahiko Niigata & Kitakata ramen Kasumigajo & Furumachi Geigi Airport Urabandai Highland Ibaraki Gunma ❹ ❺ Airport Limousine Bus Kitakata Park Naoetsu Port Echigo Line Hakushin Line Bandai Bunsui Yoshida Shibata Aizu-Wakamatsu Inawashiro Yahiko Line Niigata Atami Ban-etsu- Onsen Nishi-Wakamatsu West Line Nagaoka Railway Aizu Nō Naoetsu Saigata Kashiwazaki Tsukioka Lake Itoigawa Sanjo Firework Show Uetsu Line Onsen Inawashiro AARROOUUNNDD Shoun Sanso Garden Tsubamesanjō Blacksmith Niitsu Takada Takada Park Nishikigoi no sato Jōetsu Higashiyama Kamou Terraced Rice Paddies Shinkansen Dojo Ashinomaki-Onsen Takashiba Ouchi-juku Onsen Tōhoku Line Myoko Kogen Hokuhoku Line Shin-etsu Line Nagaoka Higashi- Sanjō Ban-etsu-West Line Deko Residence Tsuruga-jo Jōetsumyōkō Onsen Village Shin-etsu Yunokami-Onsen Railway Echigo TOKImeki Line Hokkaid T Kōriyama Funehiki Hokuriku -

Keisei Electric Railway Co., Ltd. Incident Type

Railway serious incident investigation report Railway operator : Keisei Electric Railway Co., Ltd. Incident type : Violating closure section for construction, the railway serious incident related with the situation that train ran in the section under construction works, while the construction work or the maintenance work that should be implemented to stop train operation was implemented, prescribed in Number 5, Clause 1, Article 4, of the Ordinance on Report on Railway Accidents, etc. Date and time : About 00:55, July 27, 2016 Location : At around 46,062 m from the origin at Keisei-Ueno station, between Keisei-Usui station and Keisei-Sakura station, double track, Keisei Main Line, Sakura City, Chiba Prefecture SUMMARY On July 27, 2016, the assistant manager of Sogo Branch Office of the Conductor's Office of Keisei Electric Railway Co., Ltd., accepted the request to start construction work in the down track between Keisei-Usui station and Sogosando station, from the person in charge of the closed track construction work. The assistant manager confirmed that the outbound 2345 train, the last train bound for Keisei-Narita station departing from the down track of Sogosando station, had departed from Sogosando station, and approved to start construction works at about 00:51. On the other hand, the outbound 2373K train, the last train bound for Keisei-Sakura station, departed from Keisei-Usui station about one minute behind schedule, at about 00:55, and went into the closed track section after the start of the construction works was approved. PROBABLE CAUSES It is highly probable that the serious incident had occurred as the 2373K train ran in the closed track section after the approval of the construction works that should be implemented to stop train operation, because the request to start the closed track construction works was approved without confirmed arrival of the 2373K train at Keisei-Sakura station, the last train bound for Keisei-Sakura station. -

Keisei Electric Railway Co., Ltd. June 4, 2020 MEETING AGENDA

Securities Code: 9009 Keisei Electric Railway Co., Ltd. June 4, 2020 NOTICE OF THE 177th ORDINARY GENERAL MEETING OF SHAREHOLDERS Dear Shareholder: You are cordially notified of the 177th Ordinary General Meeting of Shareholders of Keisei Electric Railway Co., Ltd. (the “Company”), which will be held on Friday, June 26, 2020, at 10:00 a.m. (reception will open at 9:00 a.m.) in the Rose Room on the sixth floor of KEISEI HOTEL MIRAMARE, 15-1 Honchiba-cho, Chuo-ku, Chiba-city, Chiba. The agenda is as shown below. If you do not attend the meeting in person, you may exercise your voting rights in writing or by the Internet. Please review the attached Reference Materials for General Meeting of Shareholders, then refer to Instructions on the Exercise of Your Voting Rights on pages 3 to 4, and exercise your voting rights by 6:00 p.m. on the day before the meeting (June 25, 2020). Faithfully yours, Toshiya Kobayashi, President and Representative Director Keisei Electric Railway Co., Ltd. 3-3-1 Yawata, Ichikawa-city, Chiba, Japan MEETING AGENDA Items to be Reported: 1: The Business Report, Consolidated Financial Statements for the 177th term, extending from April 1, 2019 to March 31, 2020, the Report of Accounting Auditors, and the Report of the Audit & Supervisory Board concerning the results of the audit of the Consolidated Financial Statements will be reported at the meeting. 2: The Non-consolidated Financial Statements for the 177th term, extending from April 1, 2019 to March 31, 2020, will be reported at the meeting. -

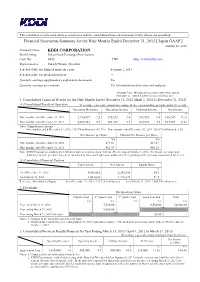

Financial Statements Summary for the Nine Months Ended

This translation is to be used solely as a reference and the consolidated financial statements in this release are unaudited. Financial Statements Summary for the Nine Months Ended December 31, 2012 [ Japan GAAP ] January 28, 2013 Company Name KDDI CORPORATION Stock Listing Tokyo Stock Exchange-First Section Code No. 9433 URL http://www.kddi.com Representative Takashi Tanaka, President Scheduled date for filing of quarterly report February 1, 2013 Scheduled date for dividend payment - Quarterly earnings supplementary explanatory documents: Yes Quarterly earnings presentation: Yes (for institutional investors and analysts) (Amount Unit : Millions of yen, unless otherwise stated) (Amounts are rounded down to nearest million yen) 1. Consolidated Financial Results for the Nine Months Ended December 31, 2012 (April 1, 2012 to December 31, 2012) (1) Consolidated Results of Operation (Percentage represents comparison change to the corresponding previous quarterly period) Operating Revenues Operating Income Ordinary Income Net Income %% % % Nine months ended December 31, 2012 2,710,577 2.5 395,573 3.0 393,955 8.0 180,247 (7.3) Nine months ended December 31, 2011 2,645,412 2.9 384,227 3.3 364,671 4.3 194,354 (4.1) Note: Comprehensive Income Nine months ended December 31, 2012: 183,570 million yen; (10.7%) Nine months ended December 31, 2011: 205,573 million yen; 5.6% Net Income per Share Diluted Net Income per Share Yen Yen Nine months ended December 31, 2012 471.63 431.87 Nine months ended December 31, 2011 462.79 460.25 Note: KDDI Corporation conducted a 1:100 stock split on common stock, with an effective date of October 1, 2012. -

Air-Rail Links in Japan 35 Years Old and Healthier Than Ever Ryosuke Hirota

Feature Railways and Air Transport Air-Rail Links in Japan 35 Years Old and Healthier than Ever Ryosuke Hirota tic and 860,000 international passengers. grown. Three airports: Haneda, Narita, Air-Rail Links in Japan Today In the same year, the monorail carried and Kansai International, each have two about 2.74 million people, including ARLs, using mostly conventional tracks During 1998, in many different parts of some non-flying passengers who used it (urban/suburban heavy rail, subways, or the world, getting to the airport became as a transit system. In 1978, airline traffic main line railways), while Haneda and easier due to construction of new air-rail in Japan grew to such an extent that a new Itami use monorails as one of their ARLs. links (ARLs). Three airports: Hong Kong airport serving Tokyo was opened for in- Japan was the first country to build a high- International Airport at Chek Lap Kok, ternational flights. This was the New To- speed train (the shinkansen), but the Copenhagen Airport at Kastrup, and Oslo kyo International Airport at Narita. honour of having the first high-speed train International Airport at Gardermoen, Haneda basically became Tokyo’s domes- serving an airport went to France when opened their first ARLs, while two other tic airport, but passenger traffic for both its TGV began linking Charles de Gaulle airports: London Heathrow and Haneda the airport and monorail continued to Airport to Paris. Unlike Frankfurt Airport Airport in Tokyo each gained a second rail grow. According to the ACI (Airports in Germany, Japan has no plans to bring link. -

Alma Eikoh Japan Large Cap Equity Fund a Sub-Fund of Alma Capital Investment Funds SICAV

FOR PROFESSIONAL INVESTORS ONLY Alma Eikoh Japan Large Cap Equity Fund A sub-fund of Alma Capital Investment Funds SICAV As of 31 March 2020 Eikoh Fund description • Investment objective: seek long-term capital growth by investing generally in Japanese large cap stocks (with market capitalisation in excess of US$ 1bn) • Investment process: analyse long term company fundamentals through extensive in-house bottom up research with a strong risk management ethos • Portfolio of around 25-30 companies which are well managed, profitable and with good prospects. Portfolio managers believe that Cash Flow Return on Investment and value creation are key Investment manager: ACIM (Alma Capital Investment Management) • Alma Capital Investment Management is a Luxembourg based asset management company and holds a branch office in London • ACIM manages assets of $4bn and is regulated by the Luxembourg regulator the CSSF • The portfolio managers, led by James Pulsford, worked together at Eikoh Research Investment Management managing the portfolio before joining ACIM in January 2020 • Naohiko Saida based in Tokyo at Milestone Asset Management provides a dedicated research service to the team at ACIM, Naohiko and James have worked together for the last twenty years Cumulative performance (%) 1 M 3 M 6 M YTD 1Y 3Y ITD ITD (annualized) I GBP Hedged C shares -11.76 -20.99 -13.03 -20.99 -2.38 -0.33 47.40 6.91 I GBP C shares -7.05 -15.14 -12.80 -15.14 6.39 3.99 - - I EUR Hedged C shares -11.94 -21.46 -13.42 -21.46 -3.31 -3.02 - - I JPY C shares -11.28 -20.69 -12.20 -20.69 -1.46 0.28 - - I EUR C shares -10.76 -18.65 -13.08 -18.65 2.95 - - - I EUR D shares -10.79 -18.68 -13.11 -18.68 2.79 - - - I USD Hedged C shares -12.21 -21.26 -12.49 -21.26 -0.58 5.03 53.11 7.61 Topix (TR) -5.99 -17.45 -10.37 -17.45 -9.50 -0.43 29.23 4.52 Fund launched on 12 June 2014 (I USD Hedged C and I GBP Hedged C shares) Portfolio characteristics Performance (Indexed - Base 100) Main indicators Fund Index Alma Eikoh Japan Large Cap Equity Fund Topix TR No. -

Keisei Electric Railway Co., Ltd. June 7, 2017 MEETING AGENDA

Securities Code: 9009 Keisei Electric Railway Co., Ltd. June 7, 2017 NOTICE OF THE 174th ORDINARY GENERAL MEETING OF SHAREHOLDERS Dear Shareholder: You are cordially invited to attend the 174th Ordinary General Meeting of Shareholders of Keisei Electric Railway Co., Ltd. (the “Company”), which will be held on Thursday, June 29, 2017, at 10:00 a.m. in the Rose Room on the sixth floor of KEISEI HOTEL MIRAMARE, 15-1 Honchiba-cho, Chuo-ku, Chiba-city, Chiba. The agenda is as shown below. If you are unable to attend the meeting in person, you may exercise your voting rights in writing or by the Internet. Please review the attached Reference Materials for General Meeting of Shareholders, then refer to Instructions on the Exercise of Your Voting Rights on pages 3 to 4, and exercise your voting rights by 6:00 p.m. on the day before the meeting (June 28, 2017). Faithfully yours, Norio Saigusa, President and Representative Director Keisei Electric Railway Co., Ltd. 3-3-1 Yawata, Ichikawa-city, Chiba, Japan MEETING AGENDA Items to be Reported: 1: The Business Report, Consolidated Financial Statements for the 174th term, extending from April 1, 2016 to March 31, 2017, the Report of Accounting Auditors, and the Report of the Audit & Supervisory Board concerning the results of the audit of the Consolidated Financial Statements will be reported at the meeting. 2: The Non-consolidated Financial Statements for the 174th term, extending from April 1, 2016 to March 31, 2017, will be reported at the meeting. Items to be Resolved: Item 1: Approval of the appropriation of surplus for the 174th term (from April 1, 2016 to March 31, 2017) Item 2: Election of sixteen (16) Directors Item 3: Election of one (1) Audit & Supervisory Board Member 1 Decisions, etc. -

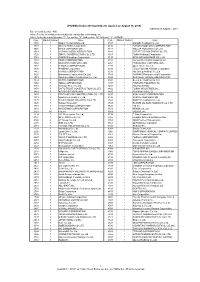

"JPX-Nikkei Index 400"

JPX-Nikkei Index 400 Constituents (applied on August 30, 2019) Published on August 7, 2019 No. of constituents : 400 (Note) The No. of constituents is subject to change due to de-listing. etc. (Note) As for the market division, "1"=1st section, "2"=2nd section, "M"=Mothers, "J"=JASDAQ. Code Market Divison Issue Code Market Divison Issue 1332 1 Nippon Suisan Kaisha,Ltd. 3107 1 Daiwabo Holdings Co.,Ltd. 1333 1 Maruha Nichiro Corporation 3116 1 TOYOTA BOSHOKU CORPORATION 1605 1 INPEX CORPORATION 3141 1 WELCIA HOLDINGS CO.,LTD. 1719 1 HAZAMA ANDO CORPORATION 3148 1 CREATE SD HOLDINGS CO.,LTD. 1720 1 TOKYU CONSTRUCTION CO., LTD. 3167 1 TOKAI Holdings Corporation 1721 1 COMSYS Holdings Corporation 3197 1 SKYLARK HOLDINGS CO.,LTD. 1801 1 TAISEI CORPORATION 3231 1 Nomura Real Estate Holdings,Inc. 1802 1 OBAYASHI CORPORATION 3254 1 PRESSANCE CORPORATION 1803 1 SHIMIZU CORPORATION 3288 1 Open House Co.,Ltd. 1808 1 HASEKO Corporation 3289 1 Tokyu Fudosan Holdings Corporation 1812 1 KAJIMA CORPORATION 3291 1 Iida Group Holdings Co.,Ltd. 1820 1 Nishimatsu Construction Co.,Ltd. 3349 1 COSMOS Pharmaceutical Corporation 1821 1 Sumitomo Mitsui Construction Co., Ltd. 3360 1 SHIP HEALTHCARE HOLDINGS,INC. 1824 1 MAEDA CORPORATION 3382 1 Seven & I Holdings Co.,Ltd. 1860 1 TODA CORPORATION 3391 1 TSURUHA HOLDINGS INC. 1861 1 Kumagai Gumi Co.,Ltd. 3401 1 TEIJIN LIMITED 1878 1 DAITO TRUST CONSTRUCTION CO.,LTD. 3402 1 TORAY INDUSTRIES,INC. 1881 1 NIPPO CORPORATION 3405 1 KURARAY CO.,LTD. 1893 1 PENTA-OCEAN CONSTRUCTION CO.,LTD. 3407 1 ASAHI KASEI CORPORATION 1911 1 Sumitomo Forestry Co.,Ltd. -

Around Tokyo from Narita Airport Model Course Depart Narita Airport ➡ Nikko ➡ Chichibu ➡ Narita ➡ Arrive Narita Airport (A Model Course)

Nikko Area Nikko Area *Please be aware that transport and the time required for a model course may vary depending on the weather and/or traffic conditions *Please note that Chichibu 2-Day Pass does not cover the Red Arrow Limited Express fare Around Tokyo from Narita Airport Model course Depart Narita Airport ➡ Nikko ➡ Chichibu ➡ Narita ➡ Arrive Narita Airport (A model course) Keisei Skyliner & Tokyo Subway Ticket NIKKO ALL AREA PASS Keisei Skyliner & Tokyo Subway Ticket Chichibu 2-Day Pass Keisei Skyliner & Tokyo Subway Ticket Narita-Kaiun Pass Keisei Tokyo Metro Tobu Limited Express Tobu Limited Express Tokyo Metro Ginza Line / Tozai Line / Red Arrow Red Arrow Tokyo Metro Marunouchi Line / Tozai Line / Keisei Skyliner Ginza Line SPACIA, Revaty SPACIA, Revaty Marunouchi Line Limited Express Limited Express Ginza Line Skyliner Keisei Main Line Keisei Main Line Narita Airport Ueno Sta. Asakusa Sta. Tobu Nikko Sta. Asakusa Sta. Ikebukuro Sta. Seibu Chichibu Sta. Ikebukuro Sta. Ueno Sta. Narita Airport Keisei Narita Sta. Narita Airport About 44 minutes About 5 minutes About 110 minutes About 110 minutes About 29 minutes About 78 minutes About 78 minutes About 16 minutes About 44 minutes About 10 minutes About 10 minutes Nikko Area Narita Area Chichibu Area Narita Area Chichibu Area Use the Use the Use the Chichibu 2-Day pass Narita-Kaiun pass Experience the mysterious charm of Nikko NIKKO ALL AREA PASS Try Sanja Meguri (visiting three shrines) to feel nature and history for sightseeing in Chichibu! Multifarious places well worth visiting near the airport! for sightseeing in Narita! for sightseeing in Nikko! Please refer to the back of the brochure for details. -

![Corporate Information [PDF/1.01MB]](https://docslib.b-cdn.net/cover/8791/corporate-information-pdf-1-01mb-1508791.webp)

Corporate Information [PDF/1.01MB]

Corporate Information 088 JR East: Domestic and International Perspectives 101 Glossary 102 Consolidated Subsidiaries and Equity-Method Affiliated Companies 104 Corporate Data 105 Stock Information Annual Report 2010 087 Corporate Information JR East: Domestic and International Perspectives PEER GROUP COMPARISONS In this section, several key performance indicators illustrate how JR East compares with selected well- known companies. Total Stock Market Value Millions of U.S. Dollars International Domestic JR East 27,647 JR East 27,647 British Airways 4,233 ANA 7,196 Lufthansa 7,210 Tokyu 5,249 Union Pacific 32,288 TEPCO 36,142 FedEx 17,259 NTT 56,058 UPS 56,957 • Data in these graphs have been computed from each company’s share price and shares outstanding at the end of the previous fiscal year. Operating Revenues Millions of U.S. Dollars International Domestic JR East 27,674 JR East 27,674 British Airways 12,071 ANA 13,208 Lufthansa 29,859 Tokyu 13,227 Union Pacific 14,143 TEPCO 53,938 FedEx 35,497 NTT 109,477 UPS 45,297 Net Income (Loss) Millions of U.S. Dollars International Domestic JR East 1,293 JR East 1,293 British Airways –642 ANA –617 Lufthansa –150 Tokyu 160 Union Pacific 1,898 TEPCO 1,438 FedEx 98 NTT 5,293 UPS 2,152 088 East Japan Railway Company Cash Flows from Operating Activities Millions of U.S. Dollars International Domestic JR East 5,152 JR East 5,152 British Airways 500 ANA 892 Lufthansa 2,668 Tokyu 1,623 Union Pacific 3,234 TEPCO 10,627 FedEx 2,753 NTT 30,299 UPS 5,285 Return on Average Equity (ROE) % International Domestic JR East 6.9 JR East 6.9 British Airways –21.5 ANA –14.4 Lufthansa –1.8 Tokyu 4.0 Union Pacific 11.7 TEPCO 5.5 FedEx 0.7 NTT 6.5 UPS 29.9 Average equity is the average of equity at the end of the previous and applicable fiscal years.