Final Assessment Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Social Screening & Me Framework

Himachal Pradesh State Road Project Feasibility Report Social Screening & ME Framework CHAPTER 11 – SOCIAL SCREENING & ME FRAMEWORK 11.1 NEED FOR SOCIAL SCREENING The Himachal Pradesh State Road Project primarily envisages improvement and rehabilitation of State Highway, Major District Roads of the state. The improvement works will consist mainly in raising the formation level, upgrading/improvement of road geometrics, widening, road stretches crossing urban areas may also require upgrading to a two-lane cross section, and/or provision for drains, sidewalks and parking where required. In some cases, new alignments (by- passes) and/or re-alignments may also be required. Improvement and rehabilitation work would entail land acquisition, adverse impact on structures, other assets and sources of earning, religious properties, impact on common properties such as bus stops, hand pumps, etc. The Government of India, the World Bank and the Government of Himachal Pradesh recognizes the need for addressing social issues at very beginning stage of any development project for minimizing adverse impacts and maximizing the benefits through equitable distribution. 11.2 CRITERIA FOR SOCIAL SCREENING Social screening of roads has been undertaken keeping in view the following parameters: (a) presence of number of residential, commercial and residential cum commercial properties within the direct impact zone (b) Existence of religious properties in project impact zone (c) likely Impact on public services (d) likely impact on public utilities (e) average land holding size (f) percentage of SC population (g) percentage of ST population. Under each parameter, relevant indicators have been identified for the screening purpose to arrive at a more meaningful screening result that would help in rational planning and selection of road. -

In Himachal Pradesh, India

Technical Report (PR-150) Population Status of Rhesus Macaque (Macaca mullata) in Himachal Pradesh, India Mewa Singh, H N Kumara and Avadhoot D Velankar Technical Report 2016 Population status of Rhesus Macaque (Macaca mullata) in Himachal Pradesh, India Technical Report : PR-150 Submitted to Himachal Pradesh Forest Department, Wildlife Wing Mewa Singh1, Honnavalli N. Kumara2 and Avadhoot D Velankar2 1Biopsychology Laboratory, University of Mysore, Mysore, Karnataka –570006 2 Sálim Ali Centre for Ornithology and Natural History, Anaikatti PO, Coimbatore, Tamil Nadu – 641108 Suggested Citation : Singh, M., Kumara H. N. and Velankar A. D. (2016). Population Status of Rhesus Macaque (Macaca mullata) In Himachal Pradesh, India. Technical Report (PR-150), Sálim Ali Centre for Ornithology and Natural History, India. Contents Acknowledgements ii No. Chapters Page No. 1 Introduction 1.1 Study Area and Species 1 1.2 Human – Rhesus Macaque Conflict 2 2 Methods 2.1 Survey technique 4 2.2 Analysis 4 2.2.1 Estimation of suitable habitat for rhesus macaques 4 2.2.2 Population Estimation 5 3 Results 3.1 Population Trends of Rhesus Macaques in Himachal Pradesh 8 3.2 Trends in Population of Rhesus Macaque in Shimla Urban region 16 4 Conclusion 18 5 References 20 6 Appendices I. Population status and extent of distribution in different wildlife 21 circles i Acknowledgements We are grateful to Hon PCCF Mr. S S Negi (IFS) and retired Hon PCCF Mr. J S Walia (IFS) of Himachal Pradesh Forest Department to give us this opportunity and put efforts to accomplish this report. We are also in debt to CCF Mr. -

Pnabe336.Pdf

.,U. 1-4:Q, -;,!R,-I- SAT tgeonp A Cat log-, -Ir-A .0r.'T Atifm at 17 %_ Wt - Iw lk LV 'IS. 49 Citation: Remanandan, P., Sastry, D.V.S.S.R., and Mengesha, Melak H. 1988. ICRISAT information. Patancheru, A.P. 502 pigeonpea germplasm catalog: passport 324, India: International Crops Research Institute for the Semi-Arid Tropics. The International Crops Research Institute for the Semi-Arid Tropics is a nonprofit Consultative Group on International scientific educational institute Agricultural Research. Donors receiving support from donors through Germany. Finland. to ICRISAT include governments the France. India, Italy. Japan, Netherlands. and agencies of Australia, Belgium, Canada, and private Norway, Sweden. Switzerland, Federal Republicof organizations: Asian Development United Kingdom. United States of America, Bank. Deutsche Gesellschaft fur Technische and the following international international Fund for Agricultural Zusammenarbeit (GTZ). International Development. The European Economic Development Research Centre, Nations Development Community. The Opec Fund for Programme. Information and conclusions lnternational Development, The World and in this publication do not necessarily Bank, and United international reflect the position of the aforementioned and private organizations. governments, agencies, The designations employed and the presentation of the material in this publication concerning the legal do not imply the expression status of any country. territory, city. of any opinion whatsoever on the part or area. or of its authorities. or concerning ofICRISAT Where trade names are used this does the delimitation of its frontiers or boundaries. not constitute endorsement of or discrimination against any product by the Institute. ISBN 92-9066-153-4 Cover photo: High podding vegetable type identified during ICRISAT/NDFRC, Kenya joint landrace is now being tested under pigeonpea germplasm evaluation diverse agroclimatological enviro:tments in Kenya. -

Nukpa Dc 1111 1)14828

I fit^fnjF visT w tvut I NUKPA DC 1111 1)14828 MWII Documentation Ceo PREFACE The formulation of a pocket book of statistics is an important step in the direction of dissemination of useful socio economic data about the State. This publication which is 46*^ in the series fulfils the ever increasing demand for reliable facts and figures about the changes which are taking place in the economy of the State in a handy form. It is hoped that this publication will serve as a useful reference book for the general public, research workers and administrators. This office acknowledges with thanks the co-operation of various departments and organizations in making available the statistical data presented in this publication. This publication has been compiled by the Official Statistics Section of this Department. Pradeep Chauhan Economic Adviser Govt, of Himachal Pradesh. ABBREVIATIONS USED Sq.Kms ..Square kilometres % ..Percentage M.T. ..Metric ton Kg. ..Kilogram KWh. ..Kilowatt hour R.E. ..Revised Estimates B.E. ..Budget Estimates Km. ..Kilometre Hect. ..Hectare •• ..Not available - ..Nil/negligible P ..Provisional Q ..Quick Estimates A ' ..Actual UNITS OF MEASUREMENT One ounce (OZ) =28.3495grams One pound =0.4535924 Kilogram One maund =82-2/7lbs. =37.3242 Kilogram One ton =2240lbs. =1016.05 Kilograms =1.016 tonnes One bale =392 lbs.=177.1 kilograms approx. One acre =4840sq.yds. =0.0040468 sq. kilometre =0.40468 hectare One mile =1609.344 meters =1.609344kms OnQ square mile =640 acres =2.589988 sq. kilometres One imperial gallon =4.54596 litres Pne kilolitre =1000 litres Qne inch =2.54 centimetres One Square =100 hectares kilometre One hectare =2.47105 acres Two kanal =one bigha =20 biswas One biswa =45 sq.yards or 37.62 sq.metres ._______________ CONTENTS Table Page I GENERAL 1.1 Himachal at a glance. -

Annexure-V State/Circle Wise List of Post Offices Modernised/Upgraded

State/Circle wise list of Post Offices modernised/upgraded for Automatic Teller Machine (ATM) Annexure-V Sl No. State/UT Circle Office Regional Office Divisional Office Name of Operational Post Office ATMs Pin 1 Andhra Pradesh ANDHRA PRADESH VIJAYAWADA PRAKASAM Addanki SO 523201 2 Andhra Pradesh ANDHRA PRADESH KURNOOL KURNOOL Adoni H.O 518301 3 Andhra Pradesh ANDHRA PRADESH VISAKHAPATNAM AMALAPURAM Amalapuram H.O 533201 4 Andhra Pradesh ANDHRA PRADESH KURNOOL ANANTAPUR Anantapur H.O 515001 5 Andhra Pradesh ANDHRA PRADESH Vijayawada Machilipatnam Avanigadda H.O 521121 6 Andhra Pradesh ANDHRA PRADESH VIJAYAWADA TENALI Bapatla H.O 522101 7 Andhra Pradesh ANDHRA PRADESH Vijayawada Bhimavaram Bhimavaram H.O 534201 8 Andhra Pradesh ANDHRA PRADESH VIJAYAWADA VIJAYAWADA Buckinghampet H.O 520002 9 Andhra Pradesh ANDHRA PRADESH KURNOOL TIRUPATI Chandragiri H.O 517101 10 Andhra Pradesh ANDHRA PRADESH Vijayawada Prakasam Chirala H.O 523155 11 Andhra Pradesh ANDHRA PRADESH KURNOOL CHITTOOR Chittoor H.O 517001 12 Andhra Pradesh ANDHRA PRADESH KURNOOL CUDDAPAH Cuddapah H.O 516001 13 Andhra Pradesh ANDHRA PRADESH VISAKHAPATNAM VISAKHAPATNAM Dabagardens S.O 530020 14 Andhra Pradesh ANDHRA PRADESH KURNOOL HINDUPUR Dharmavaram H.O 515671 15 Andhra Pradesh ANDHRA PRADESH VIJAYAWADA ELURU Eluru H.O 534001 16 Andhra Pradesh ANDHRA PRADESH Vijayawada Gudivada Gudivada H.O 521301 17 Andhra Pradesh ANDHRA PRADESH Vijayawada Gudur Gudur H.O 524101 18 Andhra Pradesh ANDHRA PRADESH KURNOOL ANANTAPUR Guntakal H.O 515801 19 Andhra Pradesh ANDHRA PRADESH VIJAYAWADA -

World Bank Document

The World Bank Report No: ISR5708 Implementation Status & Results India PMGSY Rural Roads Project (P124639) Operation Name: PMGSY Rural Roads Project (P124639) Project Stage: Implementation Seq.No: 2 Status: ARCHIVED Archive Date: 26-Jun-2011 Country: India Approval FY: 2011 Public Disclosure Authorized Product Line:IBRD/IDA Region: SOUTH ASIA Lending Instrument: Specific Investment Loan Implementing Agency(ies): National Rural Roads Development Agency Key Dates Board Approval Date 20-Dec-2010 Original Closing Date 30-Nov-2015 Planned Mid Term Review Date 30-Jun-2013 Last Archived ISR Date 26-Jun-2011 Public Disclosure Copy Effectiveness Date 18-Feb-2011 Revised Closing Date 30-Nov-2015 Actual Mid Term Review Date Project Development Objectives Project Development Objective (from Project Appraisal Document) The project development objective is to support the strengthening of the systems and processes of the national PMGSY rural roads program for the expansion and maintenance of all-season rural access roads, resulting in enhanced road connectivity to economic opportunities and social services for beneficiary communities in the participating states. Has the Project Development Objective been changed since Board Approval of the Project? Public Disclosure Authorized Yes No Component(s) Component Name Component Cost PMGSY Program Financing 1440.00 Institutional Strengthening 60.00 Overall Ratings Previous Rating Current Rating Progress towards achievement of PDO Satisfactory Satisfactory Overall Implementation Progress (IP) Satisfactory Moderately Satisfactory Overall Risk Rating Moderate Moderate Public Disclosure Authorized Implementation Status Overview This is the third full implementation support mission since the project was made effective on February 18, 2011. Despite a slow start to the implementation progress all states have now had formal notification of their EC sanctions and started procurement of their civil works. -

Sr.No Ifsc Code Branch Zone Status

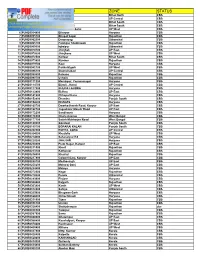

SR.NO IFSC CODE BRANCH ZONE STATUS 1 PUNB0032600 Munger Bihar North CBS 2 PUNB0047900 Siyana UP Central CBS 3 PUNB0049300 Piro Bihar South CBS 4 PUNB0050200 Aurangabad Bihar South CBS 5 PUNB0051200 Amin Nagar Sarai UP West CBS 6 PUNB0054800 Bilaspur Haryana CBS 7 PUNB0055700 Bhupal Sagar Rajasthan CBS 8 PUNB0062500 Devprayag Uttranchal CBS 9 PUNB0065700 Fatehpur Shekhawati Rajasthan CBS 10 PUNB0069600 Iqbalpur Uttranchal CBS 11 PUNB0070100 Jhinjhak UP East CBS 12 PUNB0070600 Jhinjhana UP West CBS 13 PUNB0072500 Koilwar Bihar South CBS 14 PUNB0073800 Kumher Rajasthan CBS 15 PUNB0079700 Kaul Haryana CBS 16 PUNB0082100 Parikshitgarh UP West CBS 17 PUNB0086100 Shamshabad UP Central CBS 18 PUNB0090600 Palsana Rajasthan CBS 19 PUNB0090700 Uchain Rajasthan CBS 20 PUNB0111300 Manakpur, Yamunanagar Haryana CBS 21 PUNB0114700 Bijauli, Jhansi UP Central CBS 22 PUNB0117200 KHUDA LAHORA Haryana CBS 23 PUNB0123800 Bidhnu UP East CBS 24 PUNB0141900 Chhaparthana Haryana CBS 25 PUNB0152800 Dhandra Punjab South CBS 26 PUNB0154200 DHANAS Haryana CBS 27 PUNB0160700 Dwarkadheesh Road, Kanpur UP East CBS 28 PUNB0162700 Jageshwar Mandir Road UP East CBS 29 PUNB0172200 Sandhaura Haryana CBS 30 PUNB0176900 Charu Avenue West Bengal CBS 31 PUNB0177100 Satish Mukherjee Road West Bengal CBS 32 PUNB0180000 Gondwal Punjab South CBS 33 PUNB0180700 BOPARAI KALAN Punjab South CBS 34 PUNB0202300 ROHTA, AGRA UP Central CBS 35 PUNB0204200 Khudalia UP West CBS 36 PUNB0214000 Saharanpur Rd Haryana CBS 37 PUNB0220200 JHAJJAR Haryana CBS 38 PUNB0230800 Prem Nagar, Kanpur UP East -

Diversity in Fossil Fungal Spores Article

Mycosphere 12(1): 670–874 (2021) www.mycosphere.org ISSN 2077 7019 Article Doi 10.5943/mycosphere/12/1/8 Diversity in fossil fungal spores Saxena RK1, Wijayawardene NN2,3, Dai DQ3, Hyde KD4 and Kirk PM5 1Birbal Sahni Institute of Palaeosciences, 53 University Road, Lucknow–226007, India 2State Key Laboratory of Functions and Applications of Medicinal Plants, Guizhou Medical University, Guiyang 550014, P.R. China 3Center for Yunnan Plateau Biological Resources Protection and Utilization, College of Biological Resource and Food Engineering, Qujing Normal University, Qujing, Yunnan 655011, P.R. China 4Center of Excellence in Fungal Research, Mae Fah Luang University, Chiang Rai 57100, Thailand 5Royal Botanic Gardens, Kew, Richmond, Surrey TW9 3DS, UK Saxena RK, Wijayawardene NN, Dai DQ, Hyde KD, Kirk PM 2021 – Diversity in fossil fungal spores. Mycosphere 12(1), 670–874, Doi 10.5943/mycosphere/12/1/8 Abstract Diverse types of fungal spores, exhibiting a variety of morphological variations, have been added to the fossil records from time to time. These may be unicellate (unicellular), dicellate, tricellate, tetracellate, multicellate, muriform, filiform, spirally coiled and star-like. Similarly, these may be inaperturate, monoaperturate, diaperturate, triaperturate and multiaperturate. The present paper documents all published fossil fungal spore genera and species. Assignment of fossil fungal spores to extant fungal taxa is seldom possible. These are therefore placed into artificial supra- generic taxa based on morphological characters, -

Statistical Abstract of Himachal Pradesh 2018-19” Presents the Latest Statistical Data on Various Socio-Economic Aspects of Himachal Pradesh

STATISTICAL ABSTRACT OF HIMACHAL PRADESH 2018-19 DEPARTMENT OF ECONOMIC AND STATISTICS GOVERNMENT OF HIMACHAL PRADESH SHIMLA PREFACE Rapid changes in economic scenario emphasis the need for sensitizing the data collection system in the state. The Department of Economic and Statistics is playing an active role in generation and dissemination of various kinds of data of Himachal Pradesh. The publication “Statistical Abstract of Himachal Pradesh 2018-19” presents the latest Statistical Data on various Socio-Economic aspects of Himachal Pradesh. Tables presented in this publication indicate the development trend and progress under various sectors of State’s economy. I thank all the departments and data source/providing agencies in the state for supplying the data required for this publication. I also put on record my appreciation for the sincere and hard work done by the officers and officials of Official Statistics Section of the department in bringing out this Publication. I hope the publication will be very useful to various planners and policy makers, research scholars and Economists/Statisticians. Suggestions for improvement of the publication will be highly appreciated. Dr.Vinod Kumar Rana Economic Adviser Himachal Pradesh. ABBREVIATIONS Sq.Kms - Square kilometres % - Percentage M.T. - Metric ton Kg. - Kilogram KWh. - Kilowatt hour R - Revised B - Budget Km. - Kilometre Hect. - Hectare .. - Not available - - Nil/negligible P - Provisional Q - Quick Estimates A - Actual Ad - Advance CONVERSION FACTORS Area 1 Acre = 0.404686 Hectares 1 Square Mile = 2.590 Sq.Kilometres 1 Square Mile = 640 Acres =259 Hectares 1 Square Yard = 0.84 Sq. Metres 1 Hectare = 2.47105 Acres 1 Sq. Kilometre = 0.38610 Sq.Mile 1 Sq. -

Mega E-Auction Sale Notice

MEGA E-AUCTION Regional Office, SCO 62-63, First / Second Floor, Bank Square, Sector 17-B, Chandigarh, Ph.: 0172-5007292 SALE NOTICE E-Auction Sale Notice for Sale of Movable/Immovable Assets under the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 read with proviso to Rule 6(2), 8(6) and 9 of the Security Interest (Enforcement) Rules, 2002 Notice is hereby given to the public in general and in particular to the Borrower(s) and Guarantor(s) that the below described Movable/Immovable properties hypothecated/pledged/mortgaged/charged to the Bank of Baroda, the possession of which has been taken by the respective Authorised Officers of the Bank, will be sold on "AS IS WHERE IS", "WHATEVER THERE IS" AND "WITHOUT RECOURSE BASIS” under the Rule No. 9 of the Security Interest (Enforcement) Rules, 2002 (hereinafter referred to as the Rules): Nature of Date of Dues Reserve EMD EMD Collection IFSC Code Minimum Bid Name of the Owner / Description of Sr. Property Demand Price Account Increment contact person Branch Borrower Guarantor of the immoveable/ No. (Freehold / Notice U/s Amount and contact Property Movable Property Lease hold) 13 (2) number 1. ROSARB M/s Jai Maa Bala (1) Sh. Jaswinder Property-I: All that part and parcel of the property Residential 15.01.2018 Rs. Rs. 82.00 Rs. 8.20 A/C No. BARB0SARCHA Rs. Chandigarh Sundri Polymers Singh (2) Sh. consisting of House constructed on Khata / Khatauni No. House (Freehold) 47,81,770.65P Lacs + GST Lacs 60450013201006 (Fifth Character 20,000/- and Partners Sh. -

(IEM) in the MONTH of OCTOBER 2018 (Investment in Rs Cror

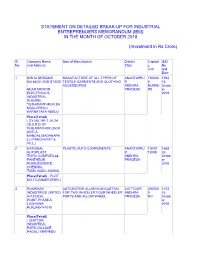

STATEMENT ON DETAILED BREAK-UP FOR INDUSTRIAL ENTREPRENUERS MEMORANDUM (IEM) IN THE MONTH OF OCTOBER 2018 (Investment in Rs Crore) Sl. Company Name Item of Manufacture District Capacit IEM No and Address State y No Unit and Date 1 NISHA DESIGNS MANUFACTURE OF ALL TYPES OF ANANTAPPU 150000 1593 NO.86-D1,2ND STAGE TEXTILE GARMENTS AND CLOTHING R 0 15 , ACCESSORIES ANDHRA NUMBE Octob NEAR MICRON PRADESH RS er ELECTRICALS, 2018 INDUSTRIAL SUBURB, YESHWANTHPUR,BA NGALORE(U) KARNATAKA-560022 Place(Tehsil) : SY.NO.191-1,1A 2A 2B,S R D OF CHILAMATHUR,(GOR ANTLA MANDAL,MADANAPA LLI PANCHAYAT & VILL,) 2 NATIONAL PLASTIC AUTO COMPONENTS ANANTAPPU 10000 1668 AUTOPLAST R TONS 26 THIRU COMPLEX,44, ANDHRA Octob PANTHEON PRADESH er ROAD,EGMORE, 2018 CHENNAI, TAMIL NADU-600008 Place(Tehsil) : PLOT NO.10,(ANANTAPUR,) 3 ROCKMAN AUTOMOTIVE ALUMINIUM CASTING CHITTOOR 200000 1673 INDUSTRIES LIMITED FOR TWO WHEELER FOUR WHEELER ANDHRA 0 26 A-7,FOCAL PARTS AND ALLOW WHEEL PRADESH NO Octob POINT,PHASE-5, er LUDHIANA 2018 PUNJAB-141010 Place(Tehsil) : CHITTOR INDUSTRIAL PARK,(VILLAGE PAGALI YERPEDU MANDAL,) 4 VISHNU BARIUM BARIUM CARBONATE CHITTOOR 65000 1598 PVT.LTD. ANDHRA METRI 15 PLOT NO.C-23,FILM PRADESH C TON Octob NAGAR, er ROAD NO.8,JUBILEE 2018 HILLS, HYDERABAD, TELANGANA-500033 Place(Tehsil) : SY.NO.27/1A,URAND PUR VILLAGE,(SRI KALAHASTHI MANDAL,) 5 SHALOM PAPER AND MANUFACTURING OF KRAFT PAPER CHITTOOR 24000 1528 BOARDS PRIVATE BOARDS ANDHRA METRI 05 LIMITED PRADESH C TON Octob D.NO.14,SRIKRISHNA er NAGAR, 2018 2ND STREET,MADIPAKKA M, KEELKATTALAI,CHEN -

Directory Establishment

DIRECTORY ESTABLISHMENT SECTOR :RURAL STATE : HIMACHAL PRADESH DISTRICT : Bilaspur Year of start of Employment Sl No Name of Establishment Address / Telephone / Fax / E-mail Operation Class (1) (2) (3) (4) (5) NIC 2004 : 0121-Farming of cattle, sheep, goats, horses, asses, mules and hinnies; dairy farming [includes stud farming and the provision of feed lot services for such animals] 1 GOVT LIVESTOCK FARM KOTHIPURA P. O. KOTHIPURA TEH SADAR DITT. BILASPUR MIMACHAL PRADESH PIN CODE: 174001, STD 1972 10 - 50 CODE: 01978, TEL NO: 280034, FAX NO: NA, E-MAIL : N.A. NIC 2004 : 0122-Other animal farming; production of animal products n.e.c. 2 TARA CHAND VILLAGE GARA PO SWAHAN TEH SH NAINA DEVI DISTT. BILAS PUR HP PIN CODE: 174310, 1990 10 - 50 STD CODE: NA , TEL NO: NA , FAX NO: NA, E-MAIL : N.A. NIC 2004 : 1410-Quarrying of stone, sand and clay 3 GAMMUNINDIALIMITED GAMMONHOUSEVSMARGPRABHADEVIDADARMUMBAI NTPCKOLDAMBARMANADISTT. 1954 10 - 50 BILASPURHP PIN CODE: 400025, STD CODE: NA , TEL NO: NA , FAX NO: NA, E-MAIL : N.A. NIC 2004 : 2102-Manufacture of corrugated paper and paperboard and of containers of paper and paperboard 4 RAJVANSHI CORRUGATING PACKAGING GOALTHAI PO GOALTHRI DISTT BILASPOR HP , PIN CODE: 174201, STD CODE: 98160, TEL 2005 10 - 50 INDUSTRY NO: 48623, FAX NO: NA, E-MAIL : N.A. NIC 2004 : 2411-Manufacture of basic chemicals except fertilizers and nitrogen compounds 5 ROSIN AND TARPIN FACTORY VILL RAGUNATHPURA P.O .RAGUNATHPURA TEH SADAR DISTT. BILASPUR HP PIN CODE: 1969 101 - 500 174005, STD CODE: 01978, TEL NO: 222464, FAX NO: 222464, E-MAIL : N.A.