3Q18 Earnings Call Presentation October 24, 2018

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

UBS AG (Incorporated with Limited Liability in Switzerland) Acting Through Its London Branch

3 June 2021 Hong Kong Exchanges and Clearing Limited (“HKEX”), The Stock Exchange of Hong Kong Limited (the “Stock Exchange”) and Hong Kong Securities Clearing Company Limited take no responsibility for the contents of this document, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this document. This document, for which we accept full responsibility, includes particulars given in compliance with the Rules Governing the Listing of Securities on the Stock Exchange of Hong Kong Limited (the “Rules”) for the purpose of giving information with regard to us. We, having made all reasonable enquiries, confirm that to the best of our knowledge and belief the information contained in this document is accurate and complete in all material respects and not misleading or deceptive, and there are no other matters the omission of which would make any statement herein or this document misleading. This document is for information purposes only and does not constitute an invitation or offer to acquire, purchase or subscribe for the Warrants. The Warrants are complex products. Investors should exercise caution in relation to them. Investors are warned that the price of the Warrants may fall in value as rapidly as it may rise and holders may sustain a total loss of their investment. Prospective purchasers should therefore ensure that they understand the nature of the Warrants and carefully study the risk factors set out in the Base Listing Document (as defined below) and this document and, where necessary, seek professional advice, before they invest in the Warrants. -

Proposed Re-Election of Retiring Directors and Proposed Granting of General Mandates to Repurchase Shares and to Issue New Shares and Notice of Annual General Meeting

475754 \ (Sands) \ 23/03/2018 \ M51 P.1 THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt as to any aspect of this circular or as to the action to be taken, you should consult a stockbroker or other registered dealer in securities, a bank manager, solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares in Sands China Ltd., you should at once hand this circular, together with the enclosed form of proxy, to the purchaser or transferee or to the bank, stockbroker or other agent through whom the sale or transfer was effected for transmission to the purchaser or transferee. Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this circular, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. SANDS CHINA LTD. 金沙中國有限公司 (Incorporated in the Cayman Islands with limited liability) (Stock Code: 1928) PROPOSED RE-ELECTION OF RETIRING DIRECTORS AND PROPOSED GRANTING OF GENERAL MANDATES TO REPURCHASE SHARES AND TO ISSUE NEW SHARES AND NOTICE OF ANNUAL GENERAL MEETING A notice convening the Annual General Meeting of Sands China Ltd. to be held at The Venetian Macao-Resort-Hotel, Florence 2201 to 2302, Level 1, Estrada da Baia de N. Senhora da Esperanca, s/n, Taipa, Macao on Friday, May 25, 2018, at 11:00 a.m. -

2020 Annual Report

Stock Code: 1928 and Note Stock Codes: 5140, 5141, 5142, 5725, 5727, 5733, 40246, 40247, 40584, 40585 www.sandschina.com From Luxury Duty Free Shopping, Exciting Entertainment and Fabulous Dining to World-Class Hotel Suites and MICE, Come and Discover Everything at Sands China. SANDS CHINA LTD. CONTENTS 1. OVERVIEW 4 1.1 Financial Results Summary 4 1.2 Highlights of 2020 5 1.3 Directors and Senior Management 11 2. BUSINESS REVIEW 18 2.1 Chairman’s Statement 18 2.2 Business Overview and Outlook 20 2.3 Our Properties 26 2.4 Management Discussion and Analysis 33 2.5 Priority Risk Factors 47 2.6 Stakeholder Information 59 3. CORPORATE GOVERNANCE 66 REPORT 3.1 Introduction 66 3.2 Corporate Governance Code Compliance 66 3.3 Board Governance Structure 67 3.4 The Board 68 3.5 Audit Committee 74 3.6 Remuneration Committee 76 3.7 Nomination Committee 78 3.8 Capex Committee 81 3.9 Risk Management and Internal Control 82 3.10 Shareholders 87 3.11 Compliance Disclosures and Other Matters 90 3.12 Directors’ Report 92 4. FINANCIAL STATEMENTS 113 4.1 Independent Auditor’s Report 113 4.2 Financial Statements 117 4.3 Notes to the Consolidated Financial Statements 123 4.4 Financial Summary 193 5. CORPORATE INFORMATION 194 6. CONTACT US 195 7. GLOSSARY 196 In case of any inconsistency between the English version and the Chinese version of this Annual Report, the English version shall prevail. SANDS CHINA LTD. 1.1 FINANCIAL HIGHLIGHTS 2 ANNUAL REPORT 2020 SANDS CHINA LTD. 1.1 FINANCIAL HIGHLIGHTS our Luxurious Hotel Rooms and Suites await you. -

Xiaomi Sews up Deals for Smart Homes

16 BUSINESS Thursday, November 29, 2018 CHINA DAILY HONG KONG EDITION Xiaomi sews Shenzhen firms hike investment up deals for in R&D sector By ZHOU MO in Shenzhen, Guangdong smart homes [email protected] 20 percent of Shenzhenregistered list Tech tieups with Ikea, Microsoft and Nearly 20 percent of ed companies devoted more Shenzhenregistered listed than 10 percent of their iKongjian ‘to create better life for people’ companies devoted more operating revenue to R&D than 10 percent of their oper By OUYANG SHIJIA shortly after Ikea, the world’s ating revenue to research ouyangshijia@ largest furniture retailer, said and development last year, a chinadaily.com.cn last week that it would acceler level on par with globally ate its transformation to fully leading hightech enterpris the sector that took the lead. Chinese technology giant embrace new technologies and es like Google and Apple, Of the 10 listed companies Xiaomi Corp announced on offer better user experiences. according to a report. with the biggest R&D invest Wednesday it has teamed up Bjorn Block, business leader In all, 256 companies cov ment, eight were IT compa with Sweden’s furniture titan for Ikea’s Home Smart divi Lei Jun, founder and CEO of Xiaomi Corp, delivers a speech on Wednesday during the MIDC Xiaomi ered in the Shenzhenregis nies. Ikea to offer smart home prod sion, told during the confer AIoT Developer Conference in Beijing. PROVIDED TO CHINA DAILY tered Listed Companies The R&D investment of ucts. ence that the new partnership Development Report dis Tencent Holdings Ltd, the The tieup is part of its larg marked a key step in creating a closed their R&D spending world’s largest game maker er efforts to expand into the seamless experience for cus partnership would benefit home renovation service plat in their 2017 annual reports. -

Annual Report 2017 1

CONTENTS Key Performance Indicators 14 Corporate Profile 16 Corporate Structure 17 Chairman & CEO’s Statement 18 Management Discussion and Analysis 20 Management Profile 34 Environmental, Social and Governance Report 38 Corporate Governance Report 54 Report of the Directors 63 Independent Auditor’s Report 93 Consolidated Statement of Profit or Loss and Other Comprehensive Income 98 Consolidated Statement of Financial Position 100 Consolidated Statement of Changes in Equity 102 Consolidated Statement of Cash Flows 105 Notes to Consolidated Financial Statements 107 Five Years Financial Summary 207 Corporate Information 208 Melco International Development Limited | Annual Report 2017 1 A TRUE LANDMARK FOR ALL OF MACAU Constantly upping its ante in the Macau integrated resort scene, our flagship property City of Dreams is heralding the start of a new era of hospitality sophistication in Macau. With the launch of the Forbes 5-Star hotel Nüwa, the rebranding and redevelopment of The Countdown, and the eagerly awaited opening of Morpheus, the cornerstone of the final phase of development for City of Dreams, the property sets a new benchmark for luxury and entertainment in Macau. A SPARKLING ENTERTAINMENT WONDERLAND Combining electrifying entertainment with Forbes 5-Star hotel, Michelin-starred dining and designer brand shopping, the cinematically-themed resort Studio City takes thrilling entertainment to a whole new level in Asia. Studio City is further embarking on a series of property upgrades to refine the entertainment offerings and improve accessibility into the resort, striving for bringing the biggest, boldest and most exciting attractions to Macau. THE WINNING HAND IN THE PHILIPPINE ENTERTAINMENT SCENE Featuring 3 luxurious hotel brands, various premium dining outlets and one-of-a-kind entertainment, the dynamic and innovative resort City of Dreams Manila is playing a key role in strengthening the depth and diversity of the Philippines’ leisure, business and tourism offerings. -

Melco Presents Celine Dion in Concert for the First Time in Cyprus

Press Release [For Immediate Publication] 18 October 2019 Melco presents Celine Dion in concert for the first time in Cyprus Demonstrating Melco’s commitment to bringing world-class entertainment to the region as the event’s sole presenter Melco announces it will soon present Cyprus’ first ever Celine Dion concert as the event’s main sponsor, demonstrating the Company’s commitment to bringing world-class entertainment to the region. The award-winning French-Canadian singer’s “Celine Dion Courage World Tour, Cyprus, presented by Melco Resorts and Entertainment” will take place at GSP Stadium, Nicosia on 2 August 2020. Mr. Craig Ballantyne, Property President of City of Dreams Mediterranean and Cyprus Casinos “C2”, said: “Melco has long been dedicated to presenting world-class entertainment offerings that go beyond gaming for the premium travel segment. Achieving this through continuous collaborations with outstanding partners, we are pleased to support Celine Dion in concert for the first time in Cyprus. In alignment with the mission of the forthcoming City of Dreams Mediterranean, the first and largest Integrated Casino Resort (ICR) in Europe, to attract and excite customers from all over the world, we anticipate the concert will enthuse and draw fans from around the region, for the chance to enjoy the singer’s thrilling performance which will further enhance the local tourism industry’s appeal. We look forward to presenting many more world-class experiences and attractions when the ICR’s doors officially open in 2021.” “Courage World Tour” is the fourteenth concert tour by Celine Dion and the artist’s first world tour in over a decade. -

Oct 8, 2019 Melco Chairman & CEO Visits Zhuhai with Team of Senior

FOR IMMEDIATE RELEASE Melco Chairman & CEO visits Zhuhai with team of senior executives Part of ‘Splendors of China’ initiative, visit is the first in a series to develop in-depth understanding of the Greater Bay Area for management team Macau, Tuesday, October 8, 2019 – Melco Resorts & Entertainment Chairman & Chief Executive Officer Mr. Lawrence Ho recently paid a visit to the city of Zhuhai with a team of the company’s senior executives as part of the Melco initiative ‘Splendors of China’. The visit is the first in a series to enhance and strengthen Melco management team’s understanding of the Greater Bay Area, with further trips being planned to Shenzhen and Guangzhou in the coming months. Mr. Lawrence Ho and the team of twelve senior executives from Melco met with representatives from the Liaison Office of the Central People’s Government in the Macao SAR (Liaison Office), including Mr. Zuo Xianghua, Director of Economic Affairs Department; and Mr. Yang Yi, Deputy Director of Economic Affairs Department, as well as Zhuhai officials including Ms. Zou Hua, Director of Zhuhai Municipal Affairs Bureau of Taiwan, Hong Kong and Macao; Mr. Huang Yuan Peng; Deputy Director of Zhuhai Municipal Affairs Bureau of Taiwan, Hong Kong and Macao; Mr. Xie Liang, Director of Zhuhai Foreign Investment Service Center; and Ms. Su Cuizhu, Divison Chief of Municipal Affairs Bureau of Taiwan, Hong Kong and Macao; and was introduced to Zhuhai’s unique positioning within the Greater Bay Area and its relationship with Macau. The Melco team visited the Hengqin integrated tourism and entertainment project Novotown, visiting Lionsgate Entertainment World and National Geographic Ultimate Explorer within the complex. -

Investment Daily

Investment Daily 12 August 2020 Major Market Indicators Market Overview 11 Aug 10 Aug 7 Aug Mkt. Turn.(mn) 141,400 135,300 177,800 HK stock will retreat today, resistance at 25,000; Eye on Tencent Stock Advances 1,015 741 577 Result Stock Declines 857 1,054 1,242 Overnight US equities performed well. Hang Seng Index significantly rebounded 513 points to 24,890 HSI 24,891 24,377 24,532 after dropping two days in a row. H-share Index rose 162 points to 10,153. Market turnover was Change +531 -154 -399 HK$141.4 billion. Heavyweight blue chips boosted market. Tencent(700) rose 2.3% before result announcement. AIA(1299) also rose 2.5%. Macau will resume issuing tourist visas. Gaming stocks HSI Turn.($bn) 41.50 44.96 56.02 HSCEI 10,153 9,991 10,063 rose. Sands(1928)surged 9.8% while Galaxy Entertainment(27) advanced 5.5%. Change +163 -73 -139 President Trump said he was considered a capital gain tax cut, together with newly daily confirmed HSCEI Turn.($bn) 34.63 41.20 54.31 COVID 19 cases decline in US, support the US stock market to rise on early Tuesday, the Dow once rose 360 points on Tuesday. However, Senate Majority Leader Mitch McConnell confirmed that talks between the Democrats and the White House were at a stalemate, triggered late selling pressure. US HSI Technical Indicators stock finished lower. 10-days MA 24,743 The three major US stock index fell 0.4-1.7% respectively on Tuesday, of which, the Nasdaq index fell 50-days MA 24,885 the most and closed below the 10 Day SMA. -

UNO Template

04 December 2013 Asia Pacific/Australia Equity Research Casinos & Gaming (Casino & Gaming (AU)) Crown (CWN.AX / CWN AU) Rating (from Outperform) UNDERPERFORM* DOWNGRADE RATING Price (04 Dec 13, A$) 16.65 Target price (A$) 16.40¹ Market cap. (A$mn) 12,127.76 Pause in the rally Yr avg. mthly trading (A$mn) 433 Last month's trading (A$mn) 448 Projected return: ■ We believe Crown will UNDERPERFORM in the short-term as Macau Capital gain (%) -1.5 gaming stocks have become expensive. We lower our rating from Dividend yield (net %) 2.2 Outperform. We upgrade our FY14 NPAT 8% on a strong MPEL 3Q. Our Total return (%) 0.72 DCF-based target price remains unchanged as the uplift in our MPEL 52-week price range 17.2 - 10.1 * Stock ratings are relative to the relevant country benchmark. valuation was offset by weakness in the domestic casinos as reported at ¹Target price is for 12 months. CWN’s AGM. CWN reported that main floor gaming across its Australia casinos was in-line with the prior year for the 17 weeks ending October 27. It Research Analysts was implied from the AGM language that VIP was running below the pcp. Larry Gandler 61 3 9280 1855 ■ For calendar 2014 we factor 6% gaming revenue growth for MPEL – a [email protected] somewhat slower pace than the 22% for 2013E. Our US$32.50 MPEL DCF Kenny Lau, CFA equates to 12.1x 2014E EBITDA. Currently, MPEL is trading at 13.1x 2014E 852 2101 7914 EBITDA. Also, the margin expansion phase may be slowing as mass market [email protected] table hold rates rose from the low-20s to the low-30s by 2013E. -

1Q19 Results in Line, Maintain "Buy" 2019 年第 1 季度业绩符合预期,维持“买入”

股 票 研 [Table_Title] Company Report: Melco Resorts & Entertainment (MLCO US) Noah Hudson 究 (86755) 2397Hudson 6684 Equity Research 公司报告: 新濠博亚 (MLCO US) [email protected] 4 June 2019 [Table_Summary] 1Q19 Results In Line, Maintain "Buy" 2019 年第 1 季度业绩符合预期,维持“买入” 1Q19 luck-normalized adjusted property EBITDA was US$362 mn [Table_Rank] 公 (-12.0% yoy, -2.3% qoq), in line with market and our expectations. Total Rating: Buy VIP turnover declined sharply (-22.6% yoy, -15.1% qoq), while total mass Maintained 司 GGR recorded below-industry-average growth (+5.0% yoy, +0.9% qoq). 报 评级: 买入 (维持) We have adjusted upward our forecasts for Melco's 2019-2021 adjusted 告 property EBITDA by 2.5%, 1.9% and 3.4%, respectively. We expect that property enhancements at City of Dreams as well as the roll out of new 6[Table_Price-18m TP 目标价] : US$23.70 Company Report Company Revised from 原目标价: US$26.50 non-gaming attractions at Studio City will increase the Company's competitiveness and further drive growth. We have adjusted downward ADR price ADR价格: US$18.810 slightly our revenue forecasts as we expect some negative impact to operations while property renovations are being undertaken. However, we expect higher EBITDA margin as Melco's non-VIP segments now contribute Stock performance more than 90% of Melco's luck-adjusted EBITDA (excluding Philippines). We 股价表现 forecast 2019-2021 adjusted property EBITDA of US$1.6 bn, US$1.7 bn and [Table_QuotePic] US$1.8 bn, respectively, representing 7.1% CAGR. 20 % change We lower our target price from US$26.50 to US$23.70 on lower sector 10 valuation and maintain our "Buy" investment rating. -

Issue of Senior Notes

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. This announcement is for informational purposes only and is not an offer to sell or the solicitation of an offer to buy securities in the United States or in any other jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. Neither this announcement nor anything herein forms the basis for any contract or commitment whatsoever. Neither this announcement nor any copy hereof may be taken into or distributed in the United States. The securities referred to herein have not been and will not be registered under the United States Securities Act of 1933, as amended, and may not be offered or sold in the United States absent registration or an applicable exemption from registration. No public offer of securities is to be made by the Company in the United States. SANDS CHINA LTD. 金沙中國有限公司 (Incorporated in the Cayman Islands with limited liability) (Stock Code: 1928 and Note Stock Codes: 5140, 5141, 5142, 5725, 5727, 5733) INSIDE INFORMATION ISSUE OF SENIOR NOTES This announcement is issued pursuant to Part XIVA of the SFO and Rule 13.09(2)(a) of the Listing Rules. INTRODUCTION Reference is made to the announcement of the Company dated June 2, 2020 in relation to the proposed issuance of senior notes. -

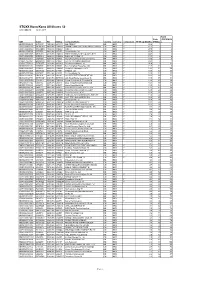

STOXX Hong Kong All Shares 50 Last Updated: 02.01.2018

STOXX Hong Kong All Shares 50 Last Updated: 02.01.2018 Rank Rank (PREVIOUS ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) ) HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 85.6 1 1 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 65.7 2 2 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 47.5 3 4 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 47.2 4 3 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 44.6 5 5 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 31.1 6 6 HK0388045442 6267359 0388.HK 626735 Hong Kong Exchanges & Clearing HK HKD Y 29.6 7 8 KYG217651051 BW9P816 0001.HK 619027 CK HUTCHISON HOLDINGS HK HKD Y 29.1 8 7 KYG2177B1014 BYZQ077 1113.HK HK50CI CK Asset Holdings Ltd HK HKD Y 26.9 9 12 HK0016000132 6859927 0016.HK 685992 Sun Hung Kai Properties Ltd. HK HKD Y 21.8 10 9 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 19.5 11 10 HK0883013259 B00G0S5 0883.HK 617994 CNOOC Ltd. CN HKD Y 19.0 12 13 HK0002007356 6097017 0002.HK 619091 CLP Holdings Ltd. HK HKD Y 18.9 13 11 HK0027032686 6465874 0027.HK 646587 GALAXY ENTERTAINMENT GP. HK HKD Y 18.0 14 15 HK0823032773 B0PB4M7 0823.HK B0PB4M Link Real Estate Investment Tr HK HKD Y 17.0 15 14 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 15.6 16 16 HK2388011192 6536112 2388.HK 653611 BOC Hong Kong (Holdings) Ltd.