Annual Report 2013 Melco Crown Entertainment Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CULINARY OFFERINGS at STUDIO CITY Studio City Offers a Diverse Range of World-Class Restaurants, Cafes and a Number of Relaxed B

CULINARY OFFERINGS AT STUDIO CITY Studio City offers a diverse range of world-class restaurants, cafes and a number of relaxed bars and lounges. Over 20 food and beverage outlets are located throughout the property, from authentic traditional Cantonese, northern Chinese, South East Asian, Japanese, Italian, western and international cuisines to Macau local delicacies. Gourmet dining – unrivalled in Macau – is also on the menu at Studio City with a stellar range of signature restaurants including one-Michelin-starred ‘Pearl Dragon’; Michelin- recommended Bi Ying; Italian ‘Trattoria Il Mulino’ from New York; and Japanese ‘Hide Yamamoto’; Chinese Pearl Dragon Pearl Dragon, helmed by Chef de Cuisine Lam Yuk Ming, is a one-Michelin-starred Cantonese restaurant (2017-18) that offers a truly exquisite dining experience at Studio City. It also received a Four-Star Award from the prestigious Forbes Travel Guide (2018). With a dedication to perfection, Pearl Dragon offers a menu showcasing refined provincial Chinese flavors, innovative culinary creations and the finest delicacies to tempt your palate. Pearl Dragon was also named Top 20 Best Restaurants in the Hong Kong Tatler Best Restaurants Hong Kong & Macau Edition 2017 and received SCMP’s 100 Top Tables award in 2017-18. Location: Shop 2111, Level 2, Star Tower Operating Hours: Monday – Friday, 12 noon – 3pm / 6pm – 11pm Saturday, Sunday and Public Holidays, 11am – 3pm / 6pm – 11pm Bi Ying Bi Ying, which has been recommended in the Michelin Guide Hong Kong Macau 2017-18, invites guests to indulge in a culinary tour of China through dishes from the North and the South. Provincial favorites such as clay pot congee, tasty stir-fried dishes, as well as Cantonese and Northern style dim sum are made to order in the open kitchen. -

City of Dreams Resort and Casino, Grand Hyatt, Hard Rock and Crown Towers Hotels

City of Dreams Resort and Casino, Grand Hyatt, Hard Rock and Crown Towers Hotels The City of Dreams Resort includes four state-of-the-art casino hotel towers with 1,622 guest rooms: the 5-star, 970-key Grand Hyatt Hotel, the 5-star, 286-key Crown Towers; and the 4-star, 366-key Hard Rock Hotel. The development is designed to accommodate conventions and conferences. Its three-floor podium includes many large ballrooms, banquet halls, meeting rooms and business facilities; a mega-casino and over 200 shopping venues and hotel guest amenities. The development has 420,000 SF (39,000 m2) of gaming space with 550 gaming tables and 1500 gaming machines, over 20 restaurants and bars, including one of the largest in the city. Included within the property is 175,000 SF (16,300 m2) of high-end retail space spread across two levels. City of Dreams was designed to the highest quality in international standards, making it the premier development and destination in the Cotai Strip of Macau and the region for leisure and entertainment. Location: Macau, China Type: Hospitality, Master Planning, Mixed-Use, Retail / Entertainment, Waterfront Services: Master Planning, Architecture, Interiors, Landscape Size: 4,107,000 sf / 382,000 m2 Awards: * Society of American Registered Architects (SARA) | Design Award of Recognition * TTG China Travel Awards | “Best Luxury Hotel in Macau” for Grand Hyatt Hotel * World Luxury Spa Awards | “Best Luxury Hotel Spa” for Crown Towers * TTG Travel Awards | Best Integrated Resort * Forbes Travel Guide | Five-Star Hotel Award * International Gaming Awards | Best Casino Interior Design * International Gaming Awards | Best Casino Operator for the Asia Pacific Region * International Gaming Awards | Best Casino VIP Room * International Property Awards | Best Leisure Development in Asia Pacific * International Property Awards | Best Leisure Development in China * Macau Environmental Protection Bureau with the collaboration of Macao Government Tourist Office | Bronze Award 2010 Macao Green Hotel Award * SGS | Indoor Environmental Quality (IEQ) Certification. -

Las Vegas Sands Corp. Annual Report 2018

Las Vegas Sands Corp. Annual Report 2018 Form 10-K (NYSE:LVS) Published: February 23rd, 2018 PDF generated by stocklight.com UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2017 or ¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission file number 001-32373 LAS VEGAS SANDS CORP. (Exact name of registrant as specified in its charter) Nevada 27-0099920 (State or other jurisdiction of (IRS Employer incorporation or organization) Identification No.) 3355 Las Vegas Boulevard South Las Vegas, Nevada 89109 (Address of principal executive offices) (Zip Code) Registrant's telephone number, including area code: (702) 414-1000 Securities registered pursuant to Section 12(b) of the Act: Title of Each Class Name of Each Exchange on Which Registered Common Stock ($0.001 par value) New York Stock Exchange Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. -

Marina Bay Sands

3Q19 Earnings Call Presentation October 23, 2019 Forward Looking Statements This presentation contains forward-looking statements made pursuant to the Safe Harbor Provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements involve a number of risks, uncertainties or other factors beyond the company’s control, which may cause material differences in actual results, performance or other expectations. These factors include, but are not limited to, general economic conditions, competition, new development, construction and ventures, substantial leverage and debt service, fluctuations in currency exchange rates and interest rates, government regulation, tax law changes and the impact of U.S. tax reform, legalization of gaming, natural or man- made disasters, terrorist acts or war, outbreaks of infectious diseases, insurance, gaming promoters, risks relating to our gaming licenses and subconcession, infrastructure in Macao, our subsidiaries’ ability to make distribution payments to us, and other factors detailed in the reports filed by Las Vegas Sands with the Securities and Exchange Commission. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date thereof. Las Vegas Sands assumes no obligation to update such information. Within this presentation, the company may make reference to certain non-GAAP financial measures including “adjusted net income,” “adjusted earnings per diluted share,” and “consolidated adjusted property EBITDA,” which have directly comparable financial measures presented in accordance with accounting principles generally accepted in the United States of America ("GAAP"), along with “adjusted property EBITDA margin,” “hold-normalized adjusted property EBITDA,” “hold-normalized adjusted property EBITDA margin,” “hold-normalized adjusted net income,” and “hold-normalized adjusted earnings per diluted share,” as well as presenting these or other items on a constant currency basis. -

MULTI/JOINT® a Solid Bet for Philippines' Okada Manila

MULTI/JOINT® a solid bet for Philippines’ Okada Manila integrated resort In February 2017, the casino resort and hotel complex Okada Manila, offi cially opened its doors. Japanese business man Kazuo Okada, who earned a big part of his fortune with the Japanese Pachinko machines, obtained a license back in 2008 to run a casino in the Manila Entertainment City. This prestigious gambling facility should compete with casinos in Macau and should turn Manila into a regional and international gambling destination. et in 45 hectares of picturesque oceanfront, the Okada Manila is one of the most iconic resorts of STiger Resort Leisure & Entertainment, Inc. (TRLEI). The hotel, consisting of 2 wings, each having 15 fl oors, is connected by two sky bridges and features 993 hotel rooms, more than 3,000 electronic gambling machines and 500 table games. In addition, the Okada Manila features a dancing fountain comparable to the Bellagio Fountains in Las Vegas, Asia’s fi rst nightclub and indoor beach club enclosed in a dome, a high-end retail area, a world-class 3,000-square-meter spa facility and several food and beverage outlets. A total of 8,000 staff has been hired to operate the resort. The fi ve-star Okada Manila hotel. More than 400 GF A collaboration with GF fi ttings have been The construction of the Okada resort, a $ 2.4 used for the hotel. billion project, required a total of 22,000 workers and took no less than 6 years. The main contractor was TransAsia Construction Development Corporation, where part of the plumbing work of the project was outsourced to Alpha Plumbing Works Inc. -

Standards Monitoring and Enforcement Division List Of

DEPARTMENT OF TOURISM OFFICE OF TOURISM STANDARDS AND REGULATION - STANDARDS MONITORING AND ENFORCEMENT DIVISION LIST OF OPERATIONAL HOTELS AS OF MARCH 26, 2020, 09:00 AM NATIONAL CAPITAL REGION COUNT NAME OF ESTABLISHMENT ADDRESS 1 Ascott Bonifacio Global City 5th ave. Corner 28th Street, BGC, Taguig 2 Ascott Makati Glorietta Ayala Center, San Lorenzo Village, Makati City 3 Cirque Serviced Residences Bagumbayan, Quezon City 4 Citadines Bay City Manila Diosdado Macapagal Blvd. cor. Coral Way, Pasay City 5 Citadines Millenium Ortigas 11 ORTIGAS AVE. ORTIGAS CENTER, PASIG CITY 6 Citadines Salcedo Makati 148 Valero St. Salcedo Village, Makati city Asean Avenue corner Roxas Boulevard, Entertainment City, 7 City of Dreams Manila Paranaque #61 Scout Tobias cor Scout Rallos sts., Brgy. Laging Handa, Quezon 8 Cocoon Boutique Hotel City 9 Connector Hostel 8459 Kalayaan Ave. cor. Don Pedro St., POblacion, Makati 10 Conrad Manila Seaside Boulevard cor. Coral Way MOA complex, Pasay City 11 Cross Roads Hostel Manila 76 Mariveles Hills, Mandaluyong City Corner Asian Development Bank, Ortigas Avenue, Ortigas Center, 12 Crowne Plaza Manila Galleria Quezon City 13 Discovery Primea 6749 Ayala Avenue, Makati City 14 Domestic Guest House Salem Complex Domestic Road, Pasay City 15 Dusit Thani Manila 1223 Epifanio de los Santos Ave, Makati City 16 Eastwood Richmonde Hotel 17 Orchard Road, Eastwood City, Quezon City 17 EDSA Shangri-La 1 Garden Way, Ortigas Center, Mandaluyong City 18 Go Hotels Mandaluyong Robinsons Cybergate Plaza, Pioneer St., Mandaluyong 19 Go Hotels Ortigas Robinsons Cyberspace Alpha, Garnet Road., San Antonio, Pasig City 20 Gran Prix Manila Hotel 1325 A Mabini St., Ermita, Manila 21 Herald Suites 2168 Chino Roces Ave. -

Nov 13, 2019 Melco Announces Macau-First Pop-Up Store Initiative Exclusively for Local Small

FOR IMMEDIATE RELEASE Melco announces Macau-first pop-up store initiative exclusively for local Small and Medium Enterprises Macau, Wednesday, November 13, 2019 – Melco Resorts & Entertainment announces it will host a Macau-first pop-up store initiative exclusively for local Small and Medium Enterprises (SMEs) at Studio City in 2020. It serves as a continuation of the Melco philosophy to create and support the growth of local SMEs. Demonstrating Melco’s ongoing and steadfast commitment to SMEs, the scheme provides rent-free retail spaces and essential operational resources to participating SMES subsidized by Melco for optimized revenues through the marketing and selling of their products and services directly to Studio City’s visitors, tourists and shoppers. Mr. Geoff Andres, Property President of Studio City, said, “Melco is firmly committed to supporting local SME business development in Macau. As announced earlier this year, we have been planning a series of further initiatives to continue establishing detailed dialogue and understanding between ourselves and local SME businesses. We are pleased to introduce the forthcoming Macau-first pop-up store initiative at our Studio City property to provide support and contribute to the advancement of local small and medium-scale businesses and look forward to working in collaboration with our local vendors towards the sustainable development of Macau.” Melco continues to plan and implement numerous campaigns to support local SME development, including the forthcoming Studio City Christmas Bazaar, Macau-first pop-up store initiative, and the ‘Knowing You, Knowing Us’ campaign. Each of these initiatives aim to create a communications platform between SMEs and Melco, to help SMEs get to know Melco as a company, its management team and employees, as well as the Company’s operational requirements and standards, and for Melco to get to know Macau’s local suppliers, their businesses, services and offerings, and serve as a catalyst for the development of a sustainable Macau. -

DOLE-NCR for Release AEP Transactions As of 7-16-2020 12.05Pm

DOLE-NCR For Release AEP Transactions as of 7-16-2020 12.05pm Company Address Transaction No. 3M SERVICE CENTER APAC, INC. 17TH, 18TH, 19TH FLOORS, BONIFACIO STOPOVER CORPORATE CENTER, 31ST STREET COR., 2ND AVENUE, BONIFACIO GLOBAL CITY, TAGUIG CITY TNCR20000756 3O BPO INCORPORATED 2/F LCS BLDG SOUTH SUPER HIGHWAY, SAN ANDRES COR DIAMANTE ST, 087 BGY 803, SANTA ANA, MANILA TNCR20000178 3O BPO INCORPORATED 2/F LCS BLDG SOUTH SUPER HIGHWAY, SAN ANDRES COR DIAMANTE ST, 087 BGY 803, SANTA ANA, MANILA TNCR20000283 8 STONE BUSINESS OUTSOURCING OPC 5-10/F TOWER 1, PITX KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000536 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000554 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000569 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000607 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000617 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000632 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000633 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000638 8 STONE BUSINESS OUTSOURCING OPC 5-10/F TOWER 1, PITX KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000680 8 STONE BUSINESS OUTSOURCING OPC 5-10/F TOWER 1, PITX KENNEDY -

Hotel Address Contact Number Email

HOTEL ADDRESS CONTACT NUMBER EMAIL Astoria Bohol Baranggay Taguihon, Baclayon, Bohol 335-1111 [email protected] 036-2881111/ Astoria Boracay Station 1, Boracay Island, Malay, Aklan [email protected] 036-2883536 Km 62 North National Highway, Brgy. San Rafael, Puerto Princesa Astoria Palawan 335-1111 [email protected] City, Palawan Astoria Plaza 15 J. Escriva Drive, Ortigas Business District, Pasig City 335-1131 to 35 [email protected] 2107 Prime Street, Madrigal Business Park, Ayala Alabang, B Hotel Alabang 828-8181 Muntinlupa City B Hotel Quezon City 14 Scout Rallos Street, Brgy. Laging Handa, Quezon City 990-5000 Chardonnay by Astoria 352 Captain Henry P. Javier, Brgy. Oranbo, Pasig City 335-1131 to 35 [email protected] Asean Avenue corner Roxas Boulevard, Entertainment City, City of Dreams Manila 800-8080 [email protected] Paranque Conrad Manila Seaside Boulevard, Coral Way, Pasay City 833-9999 Seascapes Resort Town, Soong, Lapu-Lapu City, Mactan Island, 032-4019999/ Crimson Resort & Spa Mactan [email protected] Cebu 239-3900 Ortigas Avenue corner Asian Development Bank Ave, Ortigas Crowne Plaza Manila Galleria 633-7222 Center, Quezon City Diamond Hotel Roxas Boulevard corner Dr. J. Quintos Street, Manila 528-3000/ 305-3000 [email protected] Discovery Suites 25 ADB Avenue, Ortigas Center, Pasig City 719-8888 [email protected] Dusit Thani Manila Ayala Center, Makati City 238-8888 [email protected] Eastwood Richmonde Hotel 17 Orchard Road, Eastwood City, Bagumbayan, Quezon City 570-7777 [email protected] F1 Hotel Manila 32nd Street, Bonifacio Global City, Taguig City 928-9888 Fairmont Makati 1 Raffles Drive, Makati Avenue, Makati City 795-1888 [email protected] Las Casas Filipinas de Acuzar Brgy. -

Lrwc 2018 Annual Report

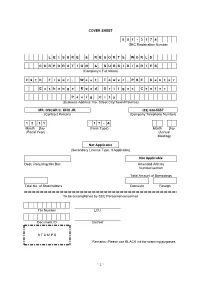

COVER SHEET 0 0 1 - 3 1 7 4 SEC Registration Number L E I S U R E & R E S O R T S W O R L D C O R P O R A T I O N & S U B S I D I A R I E S (Company’s Full Name) 2 6 t h F l o o r , W e s t T o w e r , P S E C e n t e r E x c h a n g e R o a d O r t i g a s C e n t e r P a s i g C i t y (Business Address: No. Street City/Town/Province) MR. OSCAR C. KHO JR. (02) 638-5557 (Contract Person) (Company Telephone Number) 1 2 3 1 1 7 - A Month Day (Form Type) Month Day (Fiscal Year) (Annual Meeting) Not Applicable (Secondary License Type, If Applicable) Not Applicable Dept. Requiring this Doc. Amended Articles Number/section Total Amount of Borrowings Total No. of Stockholders Domestic Foreign To be accomplished by SEC Personnel concerned File Number LCU Document ID Cashier S T A M P S Remarks: Please use BLACK ink for scanning purposes. ~ 1 ~ SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF THE CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended December 31, 2018 2. Commission identification number 13174 3. BIR tax identification number 321-000-108-278 LEISURE & RESORTS WORLD CORPORATION 4. -

For Immediate Release City of Dreams Manila Temporarily

FOR IMMEDIATE RELEASE CITY OF DREAMS MANILA TEMPORARILY SUSPENDS ITS CASINO, HOTEL AND RESTAURANT OPERATIONS (UPDATED) Manila, March 17, 2020 - Following the earlier announcement of City of Dreams Manila of the temporary closure of all its casino operations effective March 15 in full compliance with PAGCOR’s order to suspend all gaming operations, its three luxury hotels: Nuwa, Nobu and Hyatt Regency and all restaurants and guest facilities on property will also temporarily suspend operations effective March 18, in adherence with the Enhanced Community Quarantine guidelines in Metro Manila and Luzon. “In these extraordinary times that call for extraordinary measures, we rally behind President Rodrigo Duterte in the actions he has implemented to curb the spread of the Coronavirus, and we fully support PAGCOR under the leadership of Chairman Andrea Domingo in its order to temporarily suspend gaming operations in the best interest of all,” says City of Dreams Manila Chief Operating Officer Kevin Benning. “We are also one with our industry colleagues who in this time of need have prioritized the safety of our colleagues and guests over economic goals,” he continues. In implementing the Enhanced Community Quarantine, the management is extending beneficial schemes for affected colleagues to tide them over the period. The property remains vigilant while installing stringent protocols and precautionary measures for the protection and well-being of its colleagues and guests from COVID-19. During the integrated resort’s closure, guests are encouraged to check on the service advisory updates on its website, Facebook and social media channels. Stringent social distancing and application of sanitation and hygiene protocols continue to be implemented for the skeletal workforce involved in the maintenance of the property. -

Annual Report 2017 1

CONTENTS Key Performance Indicators 14 Corporate Profile 16 Corporate Structure 17 Chairman & CEO’s Statement 18 Management Discussion and Analysis 20 Management Profile 34 Environmental, Social and Governance Report 38 Corporate Governance Report 54 Report of the Directors 63 Independent Auditor’s Report 93 Consolidated Statement of Profit or Loss and Other Comprehensive Income 98 Consolidated Statement of Financial Position 100 Consolidated Statement of Changes in Equity 102 Consolidated Statement of Cash Flows 105 Notes to Consolidated Financial Statements 107 Five Years Financial Summary 207 Corporate Information 208 Melco International Development Limited | Annual Report 2017 1 A TRUE LANDMARK FOR ALL OF MACAU Constantly upping its ante in the Macau integrated resort scene, our flagship property City of Dreams is heralding the start of a new era of hospitality sophistication in Macau. With the launch of the Forbes 5-Star hotel Nüwa, the rebranding and redevelopment of The Countdown, and the eagerly awaited opening of Morpheus, the cornerstone of the final phase of development for City of Dreams, the property sets a new benchmark for luxury and entertainment in Macau. A SPARKLING ENTERTAINMENT WONDERLAND Combining electrifying entertainment with Forbes 5-Star hotel, Michelin-starred dining and designer brand shopping, the cinematically-themed resort Studio City takes thrilling entertainment to a whole new level in Asia. Studio City is further embarking on a series of property upgrades to refine the entertainment offerings and improve accessibility into the resort, striving for bringing the biggest, boldest and most exciting attractions to Macau. THE WINNING HAND IN THE PHILIPPINE ENTERTAINMENT SCENE Featuring 3 luxurious hotel brands, various premium dining outlets and one-of-a-kind entertainment, the dynamic and innovative resort City of Dreams Manila is playing a key role in strengthening the depth and diversity of the Philippines’ leisure, business and tourism offerings.