Zhou Hei Ya International Holdings Focus on Potential Demand and Attempts at Extending Brand

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

HIDAY HIDAKA Corporation

HIDAY HIDAKA Corporation Restaurant chain serving ramen and Chinese dishes to the mass-market: focusing on new business formats despite the impact of COVID-19 TICKER: 7611 | TSE1 | HP: http://hidakaya.hiday.co.jp/english/ | LAST UPDATE: 2021.08.23 Business Strengths and weaknesses Runs Hidakaya restaurant chain near train stations in Greater Tokyo; particular focus Strengths on opening new branches in Kanagawa Cost advantages from area-dominant Business model: Core business is chain of Hidakaya restaurants (94.2% of strategy and central kitchen: GPM above FY02/21 sales) that serve ramen, gyoza (dumplings), and other popular Chinese 70% for over 20 years through FY02/21, dishes. It also offers side dishes that go with alcohol for customers who want a despite relatively low-price menu. One of only quick drink. Customers range from students to businesspeople, late-shift workers, a handful of leading listed restaurant and seniors, all attracted by affordable prices (JPY390 for ramen and JPY230 for operators with a GPM above 70%. gyoza including tax) and late hours (nearly half of stores are open till 2 a.m.; more Directly operated restaurants maintain than 10% are open 24 hours*). Average customer spend is about JPY750 (before quality, boost brand power, and enable tax; FY02/21). Per the company, no other chain operates the same restaurant flexible operations format (serving both ramen and Chinese dishes). From FY02/10 to FY02/19, Low prices and classic dishes keep HIDAY HIDAKA maintained an OPM of over 10%, but in FY02/21 sales fell and the customers coming back: Maintained company posted an operating loss, due in large part to shortened opening hours comparable store sales of at least 100% YoY amid the COVID-19 outbreak. -

Langkah Membuka Bisnis Restoran Di Jepang

VOLUME NO.1//2020 MARKET INTELLIGENT LANGKAH MEMBUKA BISNIS RESTORAN DI JEPANG INDONESIAN TRADE PROMOTION CENTER (ITPC) OSAKA DAFTAR ISI 03 Gambaran Umum Bisnis Restoran di Jepang 04 Pasar Jasa Makanan di Jepang 07 Tren Pasar Restoran di Jepang 09 Tahapan Mendirikan Restoran bagi WNA di Jepang 10 Tahapan Umum Mendirikan Restoran di Jepang 11 Pendaftaran Perusahaan 14 Mendapatkan Visa Manajer Bisnis 17 Mendapatkan Izin Bisnis Restoran 21 Ketentuan Lain dalam Bisnis Restoran 22 Ketentuan Operasional 25 Ketentuan Tenaga Kerja 28 Ketentuan Pajak 34 Peluang Pasar Bisnis Restoran di Jepang 35 Gambaran Tren Kuliner 41 Masakan Asing di Jepang 45 Potensi Makanan Indonesia 49 Tips Menjalankan Bisnis Restoran di Jepang 50 Sertifikasi Halal 54 Suplai Bahan Baku 60 Tips Lainnya MARKET INTELLIGENT VOL.1/2020 | 2 GAMBARAN UMUM PASAR JASA MAKANAN DI JEPANG MARKET INTELLIGENT VOL.1/2020 | 3 PASAR JASA MAKANAN DI JEPANG Gambaran Umum kerja (USD 15,8 miliar). Semua sub sektor tumbuh sedikit dari 2015 hingga 2018. Dengan jumlah penduduk sekitar 127 juta dan produk domestik bruto (PDB) sebesar USD 5 Perkembangan Outlet triliun pada tahun 2018, Jepang merupakan salah satu pasar konsumen terbesar di dunia, Restoran memberikan peluang bagi para eksportir Di Jepang, sub sektor restoran memiliki Indonesia, terutama bagi mereka yang berminat penjualan terbesar di sektor jasa makanan laba pada pasar jasa makanan. Jepang, menyumbang 50,9% dari total pendapatan jasa makanan pada tahun 2018. Di Industri jasa makanan konsumen Jepang dalam sub sektor restoran, gerai makan kasual penting, mencapai penjualan sebesar USD mencatat penjualan tertinggi sebesar USD 91,5 274,6 miliar pada tahun 2018. -

Global Equity Fund Description Plan 3S DCP & JRA MICROSOFT CORP

Global Equity Fund June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA MICROSOFT CORP 2.5289% 2.5289% APPLE INC 2.4756% 2.4756% AMAZON COM INC 1.9411% 1.9411% FACEBOOK CLASS A INC 0.9048% 0.9048% ALPHABET INC CLASS A 0.7033% 0.7033% ALPHABET INC CLASS C 0.6978% 0.6978% ALIBABA GROUP HOLDING ADR REPRESEN 0.6724% 0.6724% JOHNSON & JOHNSON 0.6151% 0.6151% TENCENT HOLDINGS LTD 0.6124% 0.6124% BERKSHIRE HATHAWAY INC CLASS B 0.5765% 0.5765% NESTLE SA 0.5428% 0.5428% VISA INC CLASS A 0.5408% 0.5408% PROCTER & GAMBLE 0.4838% 0.4838% JPMORGAN CHASE & CO 0.4730% 0.4730% UNITEDHEALTH GROUP INC 0.4619% 0.4619% ISHARES RUSSELL 3000 ETF 0.4525% 0.4525% HOME DEPOT INC 0.4463% 0.4463% TAIWAN SEMICONDUCTOR MANUFACTURING 0.4337% 0.4337% MASTERCARD INC CLASS A 0.4325% 0.4325% INTEL CORPORATION CORP 0.4207% 0.4207% SHORT-TERM INVESTMENT FUND 0.4158% 0.4158% ROCHE HOLDING PAR AG 0.4017% 0.4017% VERIZON COMMUNICATIONS INC 0.3792% 0.3792% NVIDIA CORP 0.3721% 0.3721% AT&T INC 0.3583% 0.3583% SAMSUNG ELECTRONICS LTD 0.3483% 0.3483% ADOBE INC 0.3473% 0.3473% PAYPAL HOLDINGS INC 0.3395% 0.3395% WALT DISNEY 0.3342% 0.3342% CISCO SYSTEMS INC 0.3283% 0.3283% MERCK & CO INC 0.3242% 0.3242% NETFLIX INC 0.3213% 0.3213% EXXON MOBIL CORP 0.3138% 0.3138% NOVARTIS AG 0.3084% 0.3084% BANK OF AMERICA CORP 0.3046% 0.3046% PEPSICO INC 0.3036% 0.3036% PFIZER INC 0.3020% 0.3020% COMCAST CORP CLASS A 0.2929% 0.2929% COCA-COLA 0.2872% 0.2872% ABBVIE INC 0.2870% 0.2870% CHEVRON CORP 0.2767% 0.2767% WALMART INC 0.2767% -

Meet 65,000 Buyers in Hotel, Restaurant and Food Service Industry

Japan’s Largest Exhibition for Hospitality Standard Booth (Space ONLY) Special Trade show for Food-service, Accommodation & Leisure industries 1 booth=9㎡ (W2,970mm× D2,970mm× H2,700mm) Early bird 2700㎜ Early bird discount discount 47 [Until Jul. 31] 378,000 JPY (tax incl.) 75,600 Final application JPY No carpet [Until Sep. 28] 453,600 JPY (tax incl.) 2970㎜ 2970㎜ Option: Package Plan Trade show for Food-service & Home delivery 40 1 booth with Package W2,970×D2,970×H2,700 unit/ mm Company name Outlet 507,600 JPY (Early bird) Price Fascia board 583,200 JPY (Final Application) (incl. Construction fee & 8% consumption tax) 1. Fascia board + Company name 5-3 Rental equipment (Choose 3 items) Trade show for Kitchen equipment 2. Outlet (100V, Single phase) J. Rectangle table (Choose 1 item) 3. Carpet (Choose your own color) K. Wall shelf (x 1 unit) 4. Meeting set L. White cloth (2200x1000mm x 3 units) 5. Rental equipments (Choose your own)※ M. Brochure stand (A4 size, 6 rows) 5-1 Electrical equipment (Choose 3 items) N. Panel stand (Choose 1 item) 2700 A. Fluorescent light (40W) O. Fire extinguisher B. Spotlight (100W) P. Table-top brochure stand & Business card box C. Arm spotlight (100W) Q. Hanger stand (x 1 unit) & Hangers (x 10 units) 5-2 Rental equipment (Choose 1 item) ※Check the official website or contact the Secretariat Carpet D. Reception counter 6. Electricity (Choose your own color) E. Square table (Choose 1 item) Electric wiring work (Up to 1kW/ 100V) Date Venue F. Counter table (φ600xH1000mm) Electricity usage (1kW/ For set up & show period ) 2970 Tue Fri G. -

HIDAY HIDAKA Corporation

HIDAY HIDAKA Corporation Restaurant chain serving ramen and Chinese dishes to the mass-market: focusing on new business formats despite the impact of COVID-19 TICKER: 7611 | TSE1 | HP: http://hidakaya.hiday.co.jp/english/ | LAST UPDATE: 2020.05.12 Business Strengths and weaknesses Runs Hidakaya restaurant chain near train stations in Greater Tokyo; particular focus Strengths on opening new branches in Kanagawa Cost advantages from area-dominant Business model: Core business is chain of Hidakaya restaurants (94.3% of strategy and central kitchen: OPM above FY02/20 sales) that serve ramen, gyoza (dumplings), and other popular Chinese 10% from FY02/12 through FY02/19, despite dishes. It also offers side dishes that go with alcohol for customers who want a relatively low-price menu (FY02/20 OPM of quick drink. Customers range from students to businesspeople, late-shift workers, 9.7%) and seniors, all attracted by affordable prices (JPY390 for ramen and JPY230 for Directly operated restaurants maintain gyoza including tax) and late hours (nearly half of stores are open till 2 a.m.; more quality, boost brand power, and enable than 10% are open 24 hours*). Average customer spend is about JPY730 (before flexible operations tax; FY02/20). Per the company, no other chain operates the same restaurant Low prices and classic dishes keep format (serving both ramen and Chinese dishes). From FY02/10 to FY02/19, customers coming back: Maintained HIDAY HIDAKA has maintained an OPM of over 10%, but in FY02/20 the OPM was comparable store sales of at least 100% YoY 9.7%. for eight years through FY02/19 (down 1.8% *Since April 24, 2020, stores in Tokyo, Kanagawa, and Ibaraki have been closing at 8 p.m., YoY in FY02/20) while those in Saitama and Chiba have been closing at 11 p.m., in compliance with the Weaknesses central government’s COVID-19-related state of emergency declaration, and requests for cooperation from affected cities and prefectures. -

Ohsho Food Service (9936): August Sales, Industry Update

MITA SECURITIES Equity Research September 2, 2021 MITA SECURITIES Co., Ltd. Ohsho Food Service Junichi Shimizu Chief Analyst, Head of Research TSE 1st Section 9936 Industry: Food service, retail [email protected] August sales, industry update Update Monthly data for August: affected by the expansion of shortened hours areas Rating Ohsho Food Service (9936, the company) disclosed monthly data for its directly-owned Buy stores for August (on a preliminary basis). Same-store sales were 91.4% YoY (same month last yar = 100%; 104.6% for July). The number of holidays (weekends and national holidays) Target price (JPY) 7,250 was one less than in August 2020. The breakdown is as follows: number of customers 88.8% Stock price (JPY) (Sep 2) 5,930 (99.1% for July); average spend per customer 102.9% (105.5% for July). Market cap (JPYbn) 138.1 Same-store sales were 87.6% of August 2019 figure (our estimate; 98.2% for July). The Key changes number of holidays was the same as in August 2019. Rating No Target price No The weakness of the August numbers compared to July appears to be a trend similar to Earnings forecast No that of restaurant operators in general. In August, the areas subject to emergency Stock price (JPY) measures and priority measures to prevent the spread of the disease were expanded, and 8,000 restaurants in these areas were requested to shorten their hours and stop serving alcohol. 7,500 7,000 (the company operated normally in August 2020). According to the company, sales 6,500 between 5:00 am and 8:00 pm (the hours not subject to the request for shorter hours) 6,000 5,500 were 107.9% of the same month last year, a significantly strong figure. -

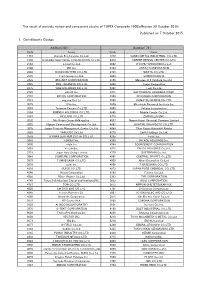

Published on 7 October 2015 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 30 October 2015) Published on 7 October 2015 1. Constituents Change Addition( 80 ) Deletion( 72 ) Code Issue Code Issue 1712 Daiseki Eco.Solution Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 1930 HOKURIKU ELECTRICAL CONSTRUCTION CO.,LTD. 2410 CAREER DESIGN CENTER CO.,LTD. 2183 Linical Co.,Ltd. 2692 ITOCHU-SHOKUHIN Co.,Ltd. 2198 IKK Inc. 2733 ARATA CORPORATION 2266 ROKKO BUTTER CO.,LTD. 2735 WATTS CO.,LTD. 2372 I'rom Group Co.,Ltd. 3004 SHINYEI KAISHA 2428 WELLNET CORPORATION 3159 Maruzen CHI Holdings Co.,Ltd. 2445 SRG TAKAMIYA CO.,LTD. 3204 Toabo Corporation 2475 WDB HOLDINGS CO.,LTD. 3361 Toell Co.,Ltd. 2729 JALUX Inc. 3371 SOFTCREATE HOLDINGS CORP. 2767 FIELDS CORPORATION 3396 FELISSIMO CORPORATION 2931 euglena Co.,Ltd. 3580 KOMATSU SEIREN CO.,LTD. 3079 DVx Inc. 3636 Mitsubishi Research Institute,Inc. 3093 Treasure Factory Co.,LTD. 3639 Voltage Incorporation 3194 KIRINDO HOLDINGS CO.,LTD. 3669 Mobile Create Co.,Ltd. 3197 SKYLARK CO.,LTD 3770 ZAPPALLAS,INC. 3232 Mie Kotsu Group Holdings,Inc. 4007 Nippon Kasei Chemical Company Limited 3252 Nippon Commercial Development Co.,Ltd. 4097 KOATSU GAS KOGYO CO.,LTD. 3276 Japan Property Management Center Co.,Ltd. 4098 Titan Kogyo Kabushiki Kaisha 3385 YAKUODO.Co.,Ltd. 4275 Carlit Holdings Co.,Ltd. 3553 KYOWA LEATHER CLOTH CO.,LTD. 4295 Faith, Inc. 3649 FINDEX Inc. 4326 INTAGE HOLDINGS Inc. 3660 istyle Inc. 4344 SOURCENEXT CORPORATION 3681 V-cube,Inc. 4671 FALCO HOLDINGS Co.,Ltd. 3751 Japan Asia Group Limited 4779 SOFTBRAIN Co.,Ltd. 3844 COMTURE CORPORATION 4801 CENTRAL SPORTS Co.,LTD. -

Yoshinoya HD / 9861

Yoshinoya HD / 9861 COVERAGE INITIATED ON: 2018.11.14 LAST UPDATE: 2020.07.06 Shared Research Inc. has produced this report by request from the company discussed in the report. The aim is to provide an “owner’s manual” to investors. We at Shared Research Inc. make every effort to provide an accurate, objective, and neutral analysis. In order to highlight any biases, we clearly attribute our data and findings. We will always present opinions from company management as such. Our views are ours where stated. We do not try to convince or influence, only inform. We appreciate your suggestions and feedback. Write to us at [email protected] or find us on Bloomberg. Research Coverage Report by Shared Research Inc. Yoshinoya HD / 9861 RCoverage LAST UPDATE: 2020.07.06 Research Coverage Report by Shared Research Inc. | https://sharedresearch.jp INDEX How to read a Shared Research report: This report begins with the trends and outlook section, which discusses the company’s most recent earnings. First-time readers should start at the business section later in the report. Executive summary ----------------------------------------------------------------------------------------------------------------------------------- 3 Key financial data ------------------------------------------------------------------------------------------------------------------------------------- 5 Recent updates ---------------------------------------------------------------------------------------------------------------------------------------- 7 Highlights -

American Century Investments® Quarterly Portfolio Holdings Avantis

American Century Investments® Quarterly Portfolio Holdings Avantis® International Equity ETF (AVDE) November 30, 2020 Avantis International Equity ETF - Schedule of Investments NOVEMBER 30, 2020 (UNAUDITED) Shares/ Principal Amount ($) Value ($) COMMON STOCKS — 99.7% Australia — 6.5% Accent Group Ltd. 14,526 23,059 Adairs Ltd. 9,223 21,547 Adbri Ltd. 12,481 28,274 Afterpay Ltd.(1) 48 3,354 AGL Energy Ltd. 8,984 89,075 Alkane Resources Ltd.(1)(2) 41,938 31,367 Alliance Aviation Services Ltd.(1) 5,187 13,148 ALS Ltd. 2,039 14,302 Altium Ltd. 1,563 40,787 Alumina Ltd. 16,346 20,996 AMA Group Ltd.(1) 16,885 9,258 AMP Ltd. 223,348 280,458 Ampol Ltd. 2,595 58,421 Ansell Ltd. 1,333 36,644 APA Group 16,232 123,383 Appen Ltd. 1,821 42,222 ARB Corp. Ltd. 3,172 64,616 Ardent Leisure Group Ltd.(1) 22,550 13,624 Aristocrat Leisure Ltd. 12,775 300,907 ASX Ltd. 1,422 80,525 Atlas Arteria Ltd. 5,725 27,252 Atlassian Corp. plc, Class A(1) 2,086 469,454 Aurelia Metals Ltd. 60,190 18,351 Aurizon Holdings Ltd. 113,756 355,100 AusNet Services 71,401 97,009 Austal Ltd. 23,896 51,252 Australia & New Zealand Banking Group Ltd. 67,427 1,121,525 Australian Agricultural Co. Ltd.(1) 32,331 25,519 Australian Ethical Investment Ltd. 3,654 13,530 Australian Finance Group Ltd. 21,308 37,254 Australian Pharmaceutical Industries Ltd. 29,606 26,147 Bank of Queensland Ltd. -

For Fiscal Year Ended March 2014 (Japanese Accounting Standards)

Financial Results (Consolidated) for Fiscal Year Ended March 2014 May 14, 2014 (Japanese accounting standards) Name of listed firm: Zensho Holdings Co., Ltd. Exchange: TSE Code no.: 7550 URL http://www.zensho.co.jp/ Representative: (title) Chairman of the Board and CEO (name) Kentaro Ogawa (title) Executive Officer, Senior Address any inquiries to: General Manager of Group Finance (name) Takemi Kaneko (tel.) 03 (6833) 1600 and Accounting Division Date of annual general meeting of shareholders (planned): June 24, 2014 Starting date of dividend payment (planned): June 25, 2014 Date of submittal of securities report (planned): June 25, 2014 Supplemental explanatory materials on consolidated financial results prepared? Y / N Investors meeting held on settlement of accounts? Y / N (for institutional investors) (Figures rounded down to the nearest million yen) 1. Consolidated financial performance in the fiscal year ended March 2014 (April 1, 2013 – March 31, 2014) (1) Consolidated business performance (Percentages [%] indicate changes from the previous year) Sales Operating profit Ordinary profit Net profit Millions of yen % Millions of yen % Millions of yen % Millions of yen % FY 2014 468,377 12.2 8,134 (44.8) 7,957 (42.6) 1,103 (78.2) FY 2013 417,577 3.6 14,736 (29.8) 13,873 (28.1) 5,058 64.8 (Reference) Comprehensive income FY 2014: 2,129 million yen (down 70.4%) FY 2013: 7,204 million yen (up 38.7%) Net profit per share– Return on Return on Operating profit Net profit per share assuming dilution equity (ROE) assets (ROA) ratio yen yen -

What Works, What Doesn't

MASTER, REGIONAL AND INTERNATIONAL FRANCHISING REPORT: FRANCHISES, BUSINESS, Global CULTURE Franchise www.globalfranchisemagazine.com ASIA WHAT WORKS, WHAT DOESN’T. HOW TO JOIN THE FRANCHISES EARNING SUCCESS Ichiro Fujita advises on franchising in Japan Japan Report Receptive to Western ideas and culture, Japan has long been a target destination for Western franchisors. However, brands eager to set up shop in this lively market should look carefully before they leap; this country may appear thoroughly Westernized, but cultural differences run deep and these should be properly understood before that first step Eastwards is taken. Ichiro Fujita, who assisted us with this project, is President/CEO of I. Fujita International, Inc, and has long experience of assisting incoming brands to franchise Global in Japan – he is an ideal guide for anyone thinking of dipping a Franchise toe in the water. ASIA Ross ADVERTISEMENT SALES DIRECTOR Mark Forsyth +44 1323 471291 [email protected] GROUP ADVERTISEMENT MANAGER Richard Davies +44 1323 471291 [email protected] SENIOR ACCOUNTS MANAGER Neil Phillips +44 1323 471291 [email protected] SENIOR ACCOUNTS MANAGER Tom Hepton +44 1206 505487 [email protected] ACCOUNT MANAGER Craig Bartlett +44 1323 471291 [email protected] HEAD OF EDITORIAL (BUSINESS) Fae Gilfillan [email protected] EDITOR Ross Gilfillan [email protected] ART DIRECTOR Lloyd Oxley CREDIT CONTROL Sue Carr +44 1206 505903 PUBLISHER Matthew Tudor globalfranchisemagazine.com Global Franchise ASIA Japan hat services do you offer expanding brands? Our consulting company assists US franchisors to facilitateW market entry specifically into Japan. Over 30 years of operations, we have helped well over 100 companies to identify their Franchise master licensees in Japan. -

Intellectual Property Center, 28 Upper Mckinley Rd. Mckinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel

Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date < 18 November 2019 > Registered National Marks as of October 2019 Registration / No. Registration Date Mark Applicant Nice class(es) Application No. 1 4/1993/00168943 16 April 2004 ORIENTAL Mandarin Oriental (UK) Limited [GB] 30 2 4/1993/00168943 16 April 2004 ORIENTAL Mandarin Oriental (UK) Limited [GB] 30 SUHITAS PHARMACEUTICALS INC. 3 4/2008/00005515 3 June 2012 ORALCON-F 5 [PH] ENVIRON SKIN CARE 4 4/2010/00501157 28 April 2011 ENVIRON 3; 5 and 10 (PROPRIETARY) LIMITED [ZA] FAIRFIELD INN & SUITES MARRIOTT WORLDWIDE 5 4/2011/00001687 10 October 2019 39 and 43 MARRIOTT CORPORATION [US] MALAYSIA DAIRY INDUSTRIES PTE 6 4/2011/00002219 29 August 2019 LUCKY COW 29 LTD. [SG] JEEPNEY JACKPOT PERA O ABC DEVELOPMENT 7 4/2012/00012768 29 August 2013 41 PARA CORPORATION [PH] 8 4/2013/00000335 31 July 2014 OCIDA ASTRONOMY TRADING [PH] 11 9 4/2013/00014434 3 April 2014 QUICK FX GENEVIEVE JABEGUERO [PH] 3 10 4/2013/00503468 6 March 2014 THE WHOLESOME TABLE WHOLELIVING CORPORATION [PH] 43 PLATON MARTINEZ FLORES PLATON MARTINEZ FLORES SAN 11 4/2014/00502460 11 September 2014 SAN PEDRO & LEANO LAW 45 PEDRO & LEANO [PH] OFFICES 12 4/2015/00005034 2 October 2015 SUN Tigerphil Marketing Corporation [PH] 9 TRANS-MILLENIUM MERCANTILE 13 4/2015/00012056 18 August 2016 DAIRY FARM 29 CORPORATION [PH] TALAUDJONG BAY CORPORATION 14 4/2015/00502499 22 September 2016 TRAVELGRAM 9 [PH] 15 4/2015/00504034 19 September 2019 L`IL CRITTERS CHURCH & DWIGHT CO., INC.