2014 NAND Flash Market Update -Supply, Demand and Beyond

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2013NAND Flash Market Annual Report

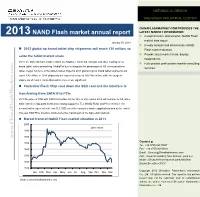

NATIONAL IC DESIGN SHENZHEN INDUSTRIAL CENTER CHINAFLASHMARKET.COM PROVIDES THE 2013 NAND Flash market annual report LATEST MARKET INFORMATION Comprehensive and accurate NAND Flash market data report January 10, 2014 Deeply analyze and demonstrate NAND Industry analysis report 2013 global no brand tablet chip shipments will reach 130 million, to Flash market situation Provide latest market trend, display seize the tablet market share newproducts 2013, the domestic tablet chip vendors as: Allwinner, Rockchip, Amlogic and other leading on no Fully provide professional market consulting brand tablet’ sales astonishing. MediaTek due to integrate the advantages of 3G communications services tablet, began full force in the tablet market. Expects 2013 global chip no brand tablet shipments will reach 130 million, in 2014 shipments are expected to rise to 160-180 million, while the surge in shipments of market competition will become more significant. Controller Flash Chip cost down the SSD cost and the interface is transferring from SATA III to PCIe 2013 the price of SSD with SATA III interface fell by 10% to 20% and in 2014 will continue to fell, while SSD controller chip plant in 2014 increasing support for TLC NAND Flash and PCIe interface, the second half is expected to be low TLC SSD enter the consumer market applications and at the end of this year SSD PCIe interface will become the mainstream in the high-end notebook. Market trend of NAND Flash market situation in 2013 2000 price index 1900 www.ChinaFlashMarket.com 1800 Contact : 1700 Tel:+86 0755-86133027 1600 Fax:+86 0755-86185012 Email:[email protected] 1500 Add:Room 6/F,Building No4.,Software park keji Middle 2 Road,Hi-tech Industrial park,NanShan 1400 Distrist.ShenZhen,P.R.C 1300 Copyright 2012 Shenzhen Flashmarket Information Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Co., Ltd . -

Phison's Resilient Business Model Generates Results Through

March 2020 Release EXECUTIVE SUMMARY Phison’s Resilient Business Phison’s diversified revenue contribution flows from a range of NAND applications including consumer, embedded, and Model Generates Results enterprise markets, making Phison less susceptible to global crisis incidents. through Challenging World During cyclical NAND price declines, Phison has demonstrated it can increase market share and unit shipments. Events During cyclical NAND price increases, Phison has demonstrated it can increase margin and revenue. _____________________________________ Over the past 20 years, Phison (TPEx: 8299) has endured the financial crisis of 2008, the cyclicality of NAND industry pricing related to supply and demand, and the introduction of new NAND technologies and emerging applications. Throughout these events, Phison maintained profitability while overcoming the challenges and generating business growth. Though the COVID-19 virus is currently impacting businesses worldwide, Phison continues to leverage its unique and resilient business model to generate results as it has successfully done in the past. PHISON’S BUSINESS MODEL Phison’s business model in Exhibit 1 is straightforward in simplicity but is underlined by massive engineering capability and flexible execution. Peer companies have attempted to study and replicate Phison’s model, but none have been successful to date. Exhibit 1: Phison’s unique business model of differentiated revenue and flexible execution. PHISON ELECTRONICS CORPORATION 1 March 2020 Release This model consists of 2 key elements: 1) NAND controller IC design, and 2) NAND storage module integration. Storage module integration is defined as manufacturing an entire functioning storage device including the controller, NAND and firmware under private labels for our valued customers. -

Phison Electronics Corporation 2016 ANNUAL REPORT

ި౻жዸǺ8299 ဂᖄႝηިҽԖज़Ϧљ Phison Electronics Corporation Ʉϖԃࡋ ԃ ൔ 2016 ANNUAL REPORT ԃൔ၌ᆛ֟ Ϧ໒ၗૻᢀෳઠᆛ֟Ǻhttp://mops.twse.com.tw ҁ Ϧ љ ᆛ ֟Ǻwww.phison.com т ӑ В ය Ǻ ύ ҇ ୯ Ʉ Ϥ ԃ ϖ Д Β Μ Ϥ В Ӝ/ᙍᆀ/ᖄ๎ႝ၉/ႝηແҹߞጃۉΓقz Ϧљว மדӜǺΪ ۉ ᙍ ᆀǺၗుձշ ႝ၉Ǻ(037) 586-896 ext.1019 ႝηແҹߞጃǺ[email protected] Ӝ/ᙍᆀ/ᖄ๎ႝ၉/ႝηແҹߞጃۉΓقz Ϧљжว ਁ۔ӜǺ ۉ ᙍ ᆀǺձշ ႝ၉Ǻ(037) 586-896 ext. 1029 ႝηແҹߞጃǺ[email protected] z ᕴϦљ/ϩϦљ/πቷϐӦ֟Ϸႝ၉ ᕴϦљ Ӧ ֟ǺཥԮᑜԮчѱൺᑫຉ 251 ဦ 10 ኴϐ 6 ႝ၉Ǻ(03)657-9299 ԮࠄϩϦљϷπቷ Ӧ ֟ǺभਪᑜԮࠄᙼဂကၡ 1 ဦϷभਪᑜԮࠄᙼဂကၡ 1-1 ဦ ႝ၉Ǻ(037)586-896 z ި౻ၸЊᐒᄬϐӜᆀ/Ӧ֟/ᆛ֟/ႝ၉ ҽԖज़Ϧљ ި୍жިچӜ ᆀǺֻᇻ Ӧ ֟ǺѠчѱεӼߞကၡѤࢤ 236 ဦ 3 ኴ ᆛ֟Ǻwww.honsec.com.tw ႝ၉Ǻ(02)2326-8818 Ӝᆀ/Ӧ֟/ᆛ֟/ႝ၉܌٣୍/Ӝۉz ന߈ԃࡋ୍ൔᛝीৣ ӜǺᔎߞᆢǵणԖۉीৣ ܌ӜᆀǺ༇ߞᖄӝीৣ٣୍܌٣୍ Ӧ ֟ǺѠчѱ҇ғܿၡΟࢤ 156 ဦ 12 ኴ ᆛ֟Ǻwww.deloitte.com.tw ႝ၉Ǻ(02)2545-9988 ၗૻϐБԄǺคǶچӜᆀϷ၌၀ੇѦԖሽ܌จວ፤ϐҬܰچz ੇѦԖሽ z Ϧљᆛ֟Ǻwww.phison.com ဂᖄႝηިҽԖज़Ϧљ Ʉϖԃࡋԃൔ Ҟ ᒵ ൘ǵठިܿൔਜ........................................................................................................... 1 ǵ 105 ԃࡋᔼ่݀.................................................................................................................... 1 Βǵ 106 ԃࡋᔼीჄཷा............................................................................................................ 3 ѦᝡݾᕉნǵݤೕᕉნϷᕴᡏᔼᕉნϐቹៜ ................... 4ډڙΟǵ ҂ٰϦљวౣǵ ມǵϦљᙁϟ................................................................................................................... 5 ǵ ҥВය................................................................................................................................... 5 Βǵ Ϧљݮॠ.................................................................................................................................. -

General Nvme FAQ

General NVMe FAQ 1. What is NVMe? NVMe, more formally NVM Express, is an interface specification optimized for PCI Express based solid state drives. The interface is defined in a scalable fashion such that it can support the needs of Enterprise and Client in a flexible way. 2. Is NVMe an industry standard? NVM Express has been developed by an industry consortium, the NVM Express Workgroup. Version 1.0 of the interface specification was released on March 1, 2011. Over 80 companies participated in the definition of the interface. 3. What is the legal framework of the NVM Express organization? The legal framework is structured as a Special Interest Group (SIG). To join a company executes a Contributor/Adopter agreement. There are 11 member companies who have board seats and provide overall governance. The Governing board is called the NVM Express Promoters Group. There are seven permanent seats and six seats filled by annual elections. Contributor companies are all free to participate in regularly scheduled workinG sessions that develop the interface. All Contributors have equal input into the development of the specification. 4. Who are the companies that form the NVM Express Promoters Group? The Promoters Group is composed of 13 companies, Cisco, Dell, EMC, IDT, Intel, Marvell, Micron, NetApp, Oracle, Samsung, SanDisk, SandForce (now LSI) and STEC. Two elected seats are currently unfilled. 5. Who are the permanent board members? Cisco, Dell, EMC, IDT, Intel, NetApp, and Oracle hold the seven permanent board seats. 6. How is the specification developed? Can anyone contribute? The specification is developed by the NVM Express Working Group. -

Fiscal Year 2020 Form 10-K

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K (Mark One) ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended February 1, 2020 or ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission file number 0-30877 Marvell Technology Group Ltd. (Exact name of registrant as specified in its charter) Bermuda 77-0481679 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) Canon’s Court, 22 Victoria Street, Hamilton HM 12, Bermuda (Address of principal executive offices) (441) 296-6395 (Registrant’s telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol Name of each exchange on which registered Common shares, $0.002 par value per share MRVL The Nasdaq Stock Market LLC Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒ Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

For Immediate Release

For Immediate Release Media Contact: Story Public Relations Michael Schoolnik [email protected] SandForce SSD Processors Transform Mainstream Data Storage Breakthrough DuraClass Technology Sets New Standards for SSD Reliability, Performance and Energy Efficiency SARATOGA, CA. – April 13, 2009 – SandForce™ Inc., the pioneer of SSD (Solid State Drive) Processors that enable commodity NAND flash deployment in enterprise and mobile computing applications, today emerged from stealth mode and unveiled its first product, the SF‐1000 SSD Processor family. These highly‐integrated silicon devices address the inherent endurance, reliability, and data retention issues associated with NAND flash memory, making it possible to build SSDs that deliver unprecedented performance over the life of the drive with orders‐of‐magnitude higher reliability than enterprise‐class HDDs (Hard Disk Drives). The SandForce patent‐pending DuraClass™ technology promises to accelerate mass‐market SSD adoption. Leading OEMs are expected to release both SLC (single level cell) and MLC (multi‐level cell) flash‐based SSDs using SandForce single‐chip SSD Processors later this year. IDC expects worldwide shipments of SSD's in the Enterprise and PC markets will exceed 40 million units in 2012, representing a CAGR of 171% from 2007‐20121. “The SF‐1000 SSD Processor Family promises to address key NAND flash issues allowing MLC flash technologies to be reliably used in broad based, mission critical storage environments,” said Mike Desens, Vice President for System Design, IBM. -

Press Release – 28 January 2019 Wibu-Systems Returns to Embedded

Press Release – 28 January 2019 The compound value of collaboration broadens the perspective on the digital transformation Wibu-Systems returns to Embedded World with an incredible lineup of solution partners Karlsruhe, Germany – Wibu-Systems will once again exhibit at Embedded World, the most iconic event for Europe’s embedded community, hosted in Nuremberg, Germany, from February 26th to 28th. The journey starts at Wibu-Systems’ principal booth (4/360) and continues at the OSADL, SD Association, Trusted Computing Group, and Wind River spaces for a fully engaging experience of the world of secure license management applied to electronic systems, distributed intelligence, the Industrial Internet of Things, e-mobility, and energy efficiency. At Wibu-Systems’ main space (Hall 4, booth 360), the company security experts will be focusing specifically on IP protection as a way to prevent attempts to pirate or reverse engineer crucial code and to ultimately ensure the lasting commercial success for businesses everywhere. They will also be sharing several case studies where IP protection was skillfully integrated into modern business models to multiply revenue streams. At the collective exhibit of OSADL, the Open Source Automation Development Lab (Hall 4, booth 168), embedded software developers will be laying out the importance of monetizing digital know-how and raising the quality of their code. Wibu-Systems, who affiliated with OSADL a couple of years ago, will join forces with them to provide their combined expertise and services to the entire OSADL community. Together with ATP, Delkin, GRL, Hagiwara, JMicron, Micron, Phison, Swissbit, Toshiba, and WD, Wibu-Systems will also present some of WIBU-SYSTEMS AG Page 1 Press Release – 28 January 2019 its many hardware secure elements at the SD Association’s group exhibit (Hall 3A, booth 524). -

Jim Handy [email protected] 105 Bacigalupi Drive, Los Gatos, CA 95032-5102, USA +1 (408) 356-2549

Jim Handy [email protected] 105 Bacigalupi Drive, Los Gatos, CA 95032-5102, USA +1 (408) 356-2549 Experience • Experienced in Trial & Deposition Testimony, Expert Reports, etc. • Highly published and widely quoted as a key semiconductor industry analyst. • 44-year semiconductor industry veteran. • Honorary Member: Storage Networking Industry Association (SNIA) • Deep technical understanding and design background. • Highly analytical. • Excellent communications skills: oral, written, and presentation. • Author of key reference design work: “The Cache Memory Book” Harcourt Brace, 1993 • Patent holder in cache memory design Expert Experience Trial Testimony In Re: Spansion et al Federal Bankruptcy Court of Delaware Docket No: 09-10690, (Hon. Kenneth Carey). 11/30/09 Netlist, Inc. (Plaintiff) vs. Diablo Technologies, Inc. (Defendant), US District Court, Northern District of CA, Case No. 13-CV-05962 YGR, (Hon. Yvonne Gonzalez Rogers), 3/13/15 Deposition Testimony In Re: Spansion et al Federal Bankruptcy Court of Delaware Docket No: 09-10690, (Hon. Kenneth Carey). 11/24/09 In Re: SRAM, 07-CV-1819-CW (N.D. Cal.), 3/25/10 Expert Reports Expert Rebuttal Report - In Re: Spansion et al Federal Bankruptcy Court of Delaware Docket No: 09-10690, (Hon. Kenneth Carey). 11/20/09 (8 pages) Expert Report - In Re: SRAM, 07-CV-1819-CW (N.D. Cal.), 1/25/10 (13 pages) Expert Report - In Re: Qimonda Richmond, LLC, et al., Case No. 09-10589 (MFW) 2/6/12 (30 pages) Expert Report - Netlist, Inc. (Plaintiff) vs. Diablo Technologies, Inc. (Defendant), US District Court, Northern District of CA, Case No. 13-CV-05962 YGR, (Hon. -

FOR IMMEDIATE RELEASE Wibu‐Systems to Expand Its Presence

FOR IMMEDIATE RELEASE Wibu‐Systems to Expand its Presence at Embedded World 2019 in Close Collaboration with Solution Partners The company to focus on secure license management and IP protection January 24, 2019 ‐ Edmonds, WA – Wibu‐Systems will exhibit at Embedded World 2019, the iconic event for Europe’s embedded community, hosted in Nuremberg, Germany, from February 26 to 28. The company will focus on secure license management applied to electronic systems, distributed intelligence, the Industrial Internet of Things, e‐mobility, and energy efficiency. Wibu‐Systems’ will exhibit in its main booth (Hall 4/Booth 360) in addition to a presence at the Open Source Automation Development Lab (OSADL), SD Association, Trusted Computing Group, and Wind River exhibits. At Wibu‐Systems’ main stand, company security experts will focus specifically on IP protection as a way to prevent attempts to pirate or reverse engineer crucial code and to ultimately ensure the lasting commercial success for global businesses. They will also share several case studies where IP protection was skillfully integrated into modern business models to multiply revenue streams. At the collective exhibit of OSADL, (Hall 4, booth 168), embedded software developers will lay out the importance of monetizing digital know‐how and raise the quality of their code. Wibu‐Systems, who affiliated with OSADL a couple of years ago, will join forces with them to provide their combined expertise and services to the entire OSADL community. Together with ATP, Delkin, GRL, Hagiwara, JMicron, Micron, Phison, Swissbit, Toshiba, and WD, Wibu‐ Systems will also present some of its many hardware secure elements at the SD Association’s group exhibit (Hall 3A, booth 524). -

4 Cos. Don't Infringe Sandisk Flash Patents: ITC

Portfolio Media, Inc. | 648 Broadway, Suite 200 | New York, NY 10012 | www.law360.com Phone: +1 212 537 6331 | Fax: +1 212 537 6371 | [email protected] 4 Cos. Don't Infringe SanDisk Flash Patents: ITC By Ryan Davis Law360, New York (April 13, 2009) -- An administrative law judge for the U.S. International Trade Commission has ruled that flash memory products made by Silicon Motion Technology Corp., Phison Electronics Corp., Skymedi Corp and Imation Corp. do not infringe two patents held by SanDisk Corp., a setback for SanDisk in a patent case it originally brought against dozens of competitors. In an initial determination issued Friday, Administrative Law Judge Charles E. Bullock ruled that the four companies did not infringe the asserted claims of SanDisk's patents, and that one claim of one of the patents was invalid for obviousness. Both patents involve methods for storing and organizing data in portable flash memory devices. “SanDisk tried to coerce the flash memory industry to pay unwarranted license fees on patents of limited value,” said Mike Bettinger, an attorney for Taiwan-based Silicon Motion. “We said from the beginning that the SanDisk patents don’t cover Silicon Motion products. We are pleased with the fact that Silicon Motion came away with a complete victory.” E. Earle Thompson, SanDisk's vice president and chief intellectual property counsel, said in a statement that the company was disappointed by the ruling. “We will continue to vigorously pursue actions against companies that use SanDisk’s patented technology without a license,” Thompson said. “SanDisk expects that the Initial Determination will not adversely impact existing licensing agreements or the royalties expected from those agreements.” The patents-at-issue in the ruling are U.S. -

Manual 417045 OCZ VTX3-25SAT3-480G

OCZ Solid State Drive Breakdown Delivering performance, versatility, and reliability that other SSD lines cannot offer 2.5 inch SATA III Capacity Max Read Max Write Random 4K Write Technology NAND Vector Series – groundbreaking storage performance Product Page VTR1-25SAT3-128G 128GB 550MB/s 400MB/s 90,000 IOPS Indilinx Barefoot 3 VTR1-25SAT3-256G 256GB 550MB/s 530MB/s 95,000 IOPS Advanced suite of NAND flash Sync VTR1-25SAT3-512G 512GB 550MB/s 530MB/s 95,000 IOPS management for reliability MLC Idle time garbage collection Vertex 4 Series - Rethinking storage performance and endurance with a cutting-edge new architecture Product Page VTX4-25SATA3-64G 64GB 460MB/s 220MB/s 70,000 IOPS Indilinx Everest 2 VTX4-25SATA3-128G 128GB 560MB/s 430MB/s 90,000 IOPS Ndurance™ 2.01 Sync VTX4-25SATA3-256G 256GB 560MB/s 510MB/s 90,000 IOPS Latency reduction MLC VTX4-25SATA3-512G 512GB 560MB/s 510MB/s 95,000 IOPS Up to 1GB cache Vertex 3 Max IOPS Series - Maximizes data throughput with increased random IOPS performance Product Page VTX3MI-25SAT3-120G 120GB 550MB/s 500MB/s 75,000 IOPS SandForce 2200 Toggle VTX3MI-25SAT3-240G 240GB 550MB/s 500MB/s 65,000 IOPS MLC Vertex 3 Series - Excellent performance & endurance for write-intensive applications Product Page 7mm Product Page VTX3-25SAT3-60G 60GB 535MB/s 480MB/s 60,000 IOPS VTX3-25SAT3-90G 90GB 550MB/s 500MB/s 60,000 IOPS VTX3-25SAT3-120G 120GB 550MB/s 500MB/s 60,000 IOPS VTX3-25SAT3-128G 128GB 550MB/s 500MB/s 60,000 IOPS SandForce 2200 Sync VTX3-25SAT3-240G 240GB 550MB/s 500MB/s 60,000 IOPS MLC VTX3-25SAT3-256G -

Sandforce® SF3500 Family

SandForce® SF3500 Family CLIENT FLASH CONTROLLERS Data Sheet Rapidly evolving NAND flash memory that leverages new flash types and Key Features and Benefits technologies delivers benefits in a form of higher density and lower cost per GB. At • Optimized for client SSD the same time, as NAND flash memory geometries shrink, delivering the endurance applications and reliability that customers demand becomes more challenging. • Scalable and flexible SF3000 The Seagate® SandForce SF3500 family of flash controllers is engineered to solve architecture the challenges of evolving NAND flash memory, and enable SSD manufacturers to • Native SATA and PCIe NVMe build robust SATA and PCIe NVMe SSDs with a greater capacity using the most interfaces in a single ASIC design advanced NAND flash memory for cost-sensitive client SSD applications. • Up to 1TB capacity • Supports the latest 10nm-class Performance and Power Optimizations MLC, TLC and 3D NAND flash SF3500 flash controllers deliver exceptional, consistent performance in real-world • DRAM support for improved applications with balanced read/write speeds and low predictable latency even latency with high entropy data. The SF3500 family is optimized for low-power environments • Award-winning DuraClass™ and supports ultra-low power sleep modes to maximize battery life and meet the technology delivers enhanced aggressive power requirements in the latest laptop and Ultrabook systems. performance, endurance, reliability and power efficiency Endurance and Reliability • SHIELD™ advanced error correction combines LDPC and DSP for The SF3500 family combines several techniques to extend flash memory life higher data reliability and longer and maintain data integrity. Enhanced DuraWrite™ data reduction lowers write endurance amplification and P/E cycles to maximize SSD endurance.