A Viga Ting Hin A

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

葡萄酒 House Pouring Wine

葡萄酒 House Pouring Wine 150ml 750ml 有气的葡萄酒 Sparkling Wine Glass Bottle SP101 Pol Remy Brut Nv (France) $12 $44 白葡萄酒 White Wine W201 Bellevie Pavillon Sauvignon Blanc (France) $11 $40 W202 Pierre Jean Colombard Chardonnay (France) $12 $44 W203 De Bortoli DB Family Selection $13 $50 Sauvignon Blanc (Australia) 红葡萄酒 Red Wine R301 Bellevie Pavillon Merlot (France) $11 $40 R302 Pierre Jean Merlot (France) $12 $44 R303 De Bortoli DB Family Selection $13 $50 Cabernet Sauvignon (Australia) 葡萄酒促销 Wine Promotion *Special deal with minimum purchase of 2 bottles house pouring wine to entitle to 15% discount off from the usual price listed above. Prices subjected to prevailing GST and Service Charge. 消费税与服务费另计。 All photos are meant for reference only. Presentation of dishes may vary without prior notice. 照片只供参考之用,摆设更改恕不作另行通知。 主酒单 Master Wine List 150ml 750ml 有气的葡萄酒 Sparkling Wine Glass Bottle SP101 Pol Remy Brut Nv (France) $12 $44 Pol Remy is produced in Burgundy, France from classic wine varieties perfect for the production of sparkling wine. It is light, fresh and fruity with aromas of apple and peach. With a delightfully easy-drinking style, it exudes aromas of creamy lemon and peach. The palate is gently off-dry and flows through to a satisfying finish. 香槟 Champagne CH102 Henri Abele Brut NV (France) $110 Pale golden colour with greenish highlights. Remarkably fine bubbles and a beautiful, persistent bead. Attractive and luscious, with hints of hawthorn and acacia blossoms as well as overtones of peach and apricot. Exceptional ripeness on the palate. Toasty, honey, and cinnamon flavours. This elegant cuvée has a full bodied, generous aftertaste. -

FTSE Publications

2 FTSE Russell Publications 01 October 2020 FTSE Value Stocks China A Share Indicative Index Weight Data as at Closing on 30 September 2020 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) Agricultural Bank of China (A) 4.01 CHINA Fuyao Glass Group Industries (A) 1.43 CHINA Seazen Holdings (A) 0.81 CHINA Aisino Corporation (A) 0.52 CHINA Gemdale (A) 1.37 CHINA Shanghai Fosun Pharmaceutical Group (A) 1.63 CHINA Anhui Conch Cement (A) 3.15 CHINA GoerTek (A) 2.12 CHINA Shenwan Hongyuan Group (A) 1.11 CHINA AVIC Investment Holdings (A) 0.61 CHINA Gree Electric Appliances Inc of Zhuhai (A) 7.48 CHINA Shenzhen Overseas Chinese Town Holdings 0.66 CHINA Bank of China (A) 2.23 CHINA Guangdong Haid Group (A) 1.24 CHINA (A) Bank Of Nanjing (A) 1.32 CHINA Guotai Junan Securities (A) 1.99 CHINA Sichuan Chuantou Energy (A) 0.71 CHINA Bank of Ningbo (A) 2 CHINA Hangzhou Hikvision Digital Technology (A) 3.56 CHINA Tbea (A) 0.86 CHINA Beijing Dabeinong Technology Group (A) 0.56 CHINA Henan Shuanghui Investment & Development 1.49 CHINA Tonghua Dongbao Medicines(A) 0.59 CHINA China Construction Bank (A) 1.83 CHINA (A) Weichai Power (A) 2.09 CHINA China Life Insurance (A) 2.14 CHINA Hengtong Optic-Electric (A) 0.59 CHINA Wuliangye Yibin (A) 9.84 CHINA China Merchants Shekou Industrial Zone 1.03 CHINA Industrial and Commercial Bank of China (A) 3.5 CHINA XCMG Construction Machinery (A) 0.73 CHINA Holdings (A) Inner Mongolia Yili Industrial(A) 6.32 CHINA Xinjiang Goldwind Science&Technology (A) 0.74 -

Luzhou Laojiao Co., Ltd. 2018 Annual Report April 2019

2018 Annual Report of Luzhou Laojiao Co.,Ltd. Luzhou Laojiao Co., Ltd. 2018 Annual Report April 2019 1 2018 Annual Report of Luzhou Laojiao Co.,Ltd. Section I Important Statements, Contents and Definitions The Board of Directors, Board of Supervisors, directors, supervisors and senior management guarantee that the information presented in this report is free of any false records, misleading statements or material omissions, and shall Individually and together be legally liable for truthfulness, accuracy and completeness of its contents. Mr. Liu Miao, responsible person for the Company, Ms. Xie Hong, responsible person for accounting work and Mr. Yan Li, responsible person for the Company’s financial affairs (Accounting Supervisor) have warranted that the financial statements in this report are true and complete. Other directors attended the board meeting to deliberate this report by themselves except the following directors. Name of directors who did not Position of directors who did not Reason for not attending Name of attend the meeting in person attend the meeting in person the meeting in person deputies Liu Miao Chairman of the Board work Lin Feng Shen Caihong Director work Jiang Yuhui Affected by risks, uncertainties and assumptions, the forward-looking statements concerning business objectives and future plans made in this report based on the subjective assumptions and judgments of the future policies and economic conditions may be significantly different from the actual results. Such statements shall not be considered as virtual promises of the Company to investors, and the investors and relevant persons shall maintain adequate risk awareness and shall understand the differences between plans, forecasts and commitments. -

China Consumer Close-Up

January 13, 2015 The Asian Consumer: A new series Equity Research China Consumer Close-up The who, what and why of China’s true consumer class Few investing challenges have proven more elusive than understanding the Chinese consumer. Efforts to translate the promise of an emerging middle class into steady corporate earnings have been uneven. In the first of a new series on the Asian consumer, we seek to strip the problem back to the basics: Who are the consumers with spending power, what drives their consumption and how will that shift over time? The result is a new approach that yields surprising results. Joshua Lu Goldman Sachs does and seeks to do business with +852-2978-1024 [email protected] companies covered in its research reports. As a result, Goldman Sachs (Asia) L.L.C. investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Sho Kawano Investors should consider this report as only a single factor +81(3)6437-9905 [email protected] Goldman Sachs Japan Co., Ltd. in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Becky Lu Appendix, or go to www.gs.com/research/hedge.html. +852-2978-0953 [email protected] Analysts employed by non- US affiliates are not registered/ Goldman Sachs (Asia) L.L.C. qualified as research analysts with FINRA in the U.S. January 13, 2015 Asia Pacific: Retail Table of contents PM Summary: A holistic view of the Asian consumer 3 China’s cohort in a regional context (a preview of India and Indonesia) 8 What they are buying and what they will buy next: Tracking 7 consumption desires 11 Seven consumption desires in focus 14 1. -

Value Partners Fund Series Value Partners China A-Share Select Fund

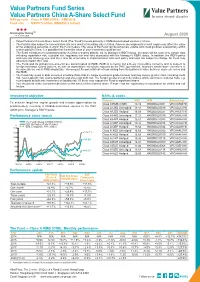

Value Partners Fund Series Value Partners China A-Share Select Fund NAV per unit : Class A RMB (CNH) – RMB19.19 Fund size : USD57.3 million (RMB393.2 million) HHH Morningstar RatingTM1 As at 31-08-2020 August 2020 • Value Partners China A-Share Select Fund (The “Fund”) invests primarily in RMB-denominated equities in China. • The Fund is also subject to concentration risk as a result of investing only in China. Adverse developments in such region may affect the value of the underlying securities in which the Fund invests. The value of the Fund can be extremely volatile and could go down substantially within a short period of time. It is possible that the entire value of your investment could be lost. • The Fund intends to invest predominantly in China A-shares directly, via its Manager’s RQFII quota. Investors will be subject to certain risks including repatriation risk, custodial risk, regulatory risk and risks associated with the Manager’s RQFII status. In addition, the RQFII policy and rules are relatively new and there may be uncertainty in implementation and such policy and rules are subject to change. All these may adversely impact the Fund. • The Fund and its primary investments are denominated in RMB. RMB is currently not a freely convertible currency and is subject to foreign exchange control policies, as well as repatriation restrictions imposed by the PRC government. Investors whose base currencies of investments are not in RMB should take into account the potential risk of loss arising from fluctuations in value between such currencies and the RMB. -

China Weigao Reducer Success Case (Large Enterprise Version) Serial Company Name Serial Company Name

China Weigao reducer success case (large enterprise version) serial Company Name serial Company Name 1 Shanghai Automobile Group Co., Ltd. 231 Chongqing Textile Holding (Group) Company 2 Dongfeng Motor Corporation 232 Aoyang Group Co., Ltd. 3 Huawei Investment Holdings Co., Ltd. 233 Guangxi Shenglong Metallurgy Co., Ltd. 4 China Ordnance Equipment Group Corporation 234 Lingyuan Iron and Steel Group Co., Ltd. 5 China Minmetals Corporation 235 Futong Group Co., Ltd. 6 China FAW Group Corporation 236 Yongfeng Group Co., Ltd. 7 China Ordnance Industry Corporation 237 Shandong Taishan Iron and Steel Group Co., Ltd. 8 Beijing Automobile Group Co., Ltd. 238 Xinjiang Zhongtai (Group) Co., Ltd. 9 Shandong Weiqiao Venture Group Co., Ltd. 239 Guangdong Haida Group Co., Ltd. 10 China Aviation Industry Corporation 240 Jiangsu Yangzijiang Shipbuilding Group Corporation 11 Zhengwei International Group Co., Ltd. 241 Shenzhen Oufeiguang Technology Co., Ltd. 12 China Baowu Iron and Steel Group Co., Ltd. 242 Dongchen Holding Group Co., Ltd. 13 Lenovo Holdings Co., Ltd. 243 Xinjiang Goldwind Technology Co., Ltd. 14 China National Chemical Corporation 244 Wanji Holding Group Co., Ltd. 15 Hegang Group Co., Ltd. 245 Tsingtao Brewery Co., Ltd. 16 China Shipbuilding Industry Corporation 246 Tasly Holding Group Co., Ltd. 17 Guangzhou Automobile Industry Group Co., Ltd. 247 Wanfeng Auto Holding Group Co., Ltd. 18 Aluminum Corporation of China 248 Wuhan Institute of Posts and Telecommunications 19 China National Building Material Group Co., Ltd. 249 Red Lion Holdings Group Co., Ltd. 20 Hengli Group Co., Ltd. 250 Xinjiang Tianye (Group) Co., Ltd. 21 CRRC Corporation Limited 251 Juhua Group Company 22 Xinxing Jihua Group Co., Ltd. -

Luzhou Laojiao Co., Ltd. 2020 Interim Report

2020 Interim Report of Luzhou Laojiao Co., Ltd. Luzhou Laojiao Co., Ltd. 2020 Interim Report August 2020 1 2020 Interim Report of Luzhou Laojiao Co., Ltd. Section I Important Statements, Contents and Definitions The Board of Directors, Board of Supervisors, as well as directors, supervisors and senior management other than the following directors, supervisors and senior management that have expressed dissent against this report guarantee that the information presented in this report is free of any false records, misleading statements or material omissions, and shall individually and together be legally liable for truthfulness, accuracy and completeness of its contents. Liu Miao, responsible person for the Company, Xie Hong, responsible person for accounting work and Yan Li, responsible person for the Company’s financial affairs (Accounting Supervisor) have warranted that the financial statements in this report are true and complete. All the directors attended the board meeting to deliberate this report by themselves. Affected by risks, uncertainties and assumptions, the forward-looking statements concerning business objectives and future plans made in this report based on the subjective assumptions and judgments of the future policies and economic conditions may be significantly different from the actual results. Such statements shall not be considered as virtual promises of the Company to investors, and the investors and relevant persons shall maintain adequate risk awareness and shall understand the differences between plans, forecasts and commitments. The Company has no interim dividend plan, either in the form of cash or stock. This Report has been prepared in both Chinese and English. Should there be any discrepancies or misunderstandings between the two versions, the Chinese version shall prevail. -

Le Chevalier Errant

期 49 总第 JUILLET 2018 | MAGAZINE CULTUREL EN CHINOIS ET FRANÇAIS ISSN : 16749715 CN115961/C N°49 二零一八年七月刊 《孔子学院》中法文对照版 武侠 Le chevalier errant Le chevalier 孔 子 学 院 INSTITUT CONFUCIUS N.49 | JUILLET 2018 WWW.CIM.CHINESECIO.COM RMB 16 / EURO 5,99 NEOMA CONFUCIUS INSTITUTE FOR BUSINESS Le seul centre accrédité par Hanban en France et dans les pays francophones pour la formation et l’examen de CTCSOL (Certificate for Teachers of Chinese to Speakers of Other Languages). Le CTCSOL est un certificat international, délivré par Hanban, aux candidats ayant réussi l’examen de qualification professionnelle en tant que professeurs de chinois internationaux. PROCHAINES SESSIONS DE FORMATION ET D’EXAMEN L’INSTITUT CONFUCIUS DE Examen oral Formation à l’examen oral • Session 2018 : • 1re session : 2–4 janv. 2019 L’UNIVERSITÉ DE LORRAINE 5–6 janv. ; 13–14 janv. 2019 • 2e session : 3–5 juil. 2019 Situé à Metz, chef-lieu de l’ancienne région de Lorraine, • 1re session 2019 : • 3e session : 11–13 déc. 2019 l’institut Confucius de l’Université de Lorraine est une structure 6–7 juil. ; 13–14 juil. 2019 universitaire de coopération franco-chinoise (Université de Lorraine, e • 2 session 2019 : Formation à l’examen écrit Université de Technologie de Wuhan et Hanban). Il est également re 14–15 déc. ; 21–22 déc. 2019 • 1 session : 5–8 janv. 2019 soutenu par les autorités territoriales. Depuis sa création en 2011, • 2e session : 6–9 juil. 2019 il reste fidèle à sa vocation d’être un lieu d’échange et de découverte Examen écrit • 3e session : 14–17 déc. -

“Eight-Point Regulation” and “Chinese

vv Clinical Group Archives of Nursing Practice and Care DOI http://dx.doi.org/10.17352/anpc.000016 CC By Xianglong Xu1-3, Runzhi Zhu1-3, Sha Deng1-3, Sheng Liu1-3, Dengyuan Liu1-3, Research Article Cesar Reis4, Manoj Sharma5 and Yong Effects of “Eight-Point Regulation” Zhao1-3* 1School of Public Health and Management, and “Chinese Military Bans Luxury Chongqing Medical University, Chongqing 400016, China 2Research Center for Medicine and Social Banquets” on Price, Sale, and Development, Chongqing Medical University, Chongqing 400016, China Consumption of High-End Alcohol 3The Innovation Center for Social Risk Governance in Health, Chongqing Medical University, Chongqing Products in China 400016, China 4Loma Linda University Medical Center, Department of Preventive Medicine 24785 Stewart Street, Suite 204 Loma Linda, CA 92354 5Department of Behavioral and Environmental Health, Abstract Jackson State University, Jackson 39213, USA Background: Alcohol use disorder was linked to corruption, abuse of power, and bureaucratic Dates: Received: 20 June, 2016; Accepted: 02 ineffi ciency in mainland China. The Communist Party of China issued the “Eight-Point Regulation” and December, 2016; Published: 05 December, 2016 “Luxury Banquets Ban for Chinese Military” in December 2012 to eliminate extravagance and corruption. This study aimed to probe the effects of “Eight-point regulation” and “Chinese military bans luxury *Corresponding author: Yong Zhao, Department banquets” on price, sale, and consumption of high-end alcohol products in China. of Nutrition and Food Hygiene, School of public health and management, Chongqing Medical Methods: We collected and analyzed secondary data to derive refl ections on the infl uence of the University. -

Hunan Sanhong Pharmaceutical Company Limited “True Tiger Wine” Project

Hunan Sanhong Pharmaceutical Company Limited “True Tiger Wine” Project Feasibility Studies Report December 2005 Table of Content Chapter 1 General Introduction ................................................................................................................................................................................... 7 1.1 Project Summary ......................................................................................................................................................................................... 7 1.1.1 Project Title ....................................................................................................................................................................................... 7 1.1.2 Project Construction Contractor and Corporation ............................................................................................................................. 7 1.1.3 General Competent Authority of Project ............................................................................................................................................ 7 1.1.4 Nature of Project ................................................................................................................................................................................ 7 1.1.5 Specific Competent Authority of Project ............................................................................................................................................ 7 1.1.6 Project Construction Location and Area -

Luzhou Laojiao Co., Ltd. 2020 Annual Report April 2021

2020 Annual Report of Luzhou Laojiao Co., Ltd. Luzhou Laojiao Co., Ltd. 2020 Annual Report April 2021 1 2020 Annual Report of Luzhou Laojiao Co., Ltd. Section I Important Statements, Contents and Definitions The Board of Directors, Board of Supervisors, directors, supervisors and senior management guarantee that the information presented in this report is free of any false records, misleading statements or material omissions, and shall individually and together be legally liable for truthfulness, accuracy and completeness of its contents. Liu Miao, responsible person for the Company, Xie Hong, responsible person for accounting work and Yan Li, responsible person for the Company’s financial affairs (Accounting Supervisor) have warranted that the financial statements in this report are true, accurate and complete. Other directors attended the board meeting to deliberate this report by themselves except the following directors. Position of directors who Name of directors who did not Reason for not attending did not attend the meeting Name of deputies attend the meeting in person the meeting in person in person Wang Hongbo Director Work Lin Feng Tan Lili Independent Director Work Xu Guoxiang Qian Xu Director Work Liu Miao Ying Hanjie Director Work Liu Miao Affected by risks, uncertainties and assumptions, the forward-looking statements concerning business objectives and future plans made in this report based on the subjective assumptions and judgments of the future policies and economic conditions may be significantly different from the actual results. Such statements shall not be considered as virtual promises of the Company to investors, and the investors and relevant persons shall maintain adequate risk awareness and shall understand the differences between plans, forecasts and commitments. -

Research and Analysis Report of Kweichow Moutai Company

Academic Journal of Business & Management ISSN 2616-5902 Vol. 3, Issue 7: 1-5, DOI: 10.25236/AJBM.2021.030701 Research and Analysis Report of Kweichow Moutai Company Yinglin Qian School of Economics, Northwest University for Nationalities, Qujing, Yunnan 655000, China Abstract: Fiedler mentioned "does not exist a kind of is suitable for various situation of universal principles and methods of management, management can only act according to the circumstances of the specific", moutai company is the most influential brand in China and to achieve a monopoly in the competition and development, based on the fundamental analysis and technical analysis, maotai company for the industry analysis, company analysis and technical analysis, This paper probes into the development prospect of Maotai Company, obtains some problems existing in the development and puts forward corresponding investment suggestions for investors. Keywords: industry analysis, technical analysis, investment advice 1. Overview of Kweichow Moutai Company 1)Company business summary and analysis of capital ownership structure Since its establishment, the company has been engaged in a variety of businesses, including the production, sales and service of Maotai liquor, the production and sales of beverage, food and packaging materials, the development of anti-counterfeiting technology and the research and development of related products of the information industry. It belongs to the beverage manufacturing industry in the food and beverage industry, and is the typical representative of maotai-flavor liquor in China. It wants to have a famous reputation both at home and abroad, and it is the only liquor industry in China that has won the title of "green food" and "organic food".