Supply Chain Management : Strategy, Planning, and Operation / Sunil Chopra, Peter Meindl.—5Th Ed

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Project Managers Vs Operations Managers: a Comparison Based on the Style of Leadership

IOSR Journal of Business and Management (IOSR-JBM) e-ISSN: 2278-487X, p-ISSN: 2319-7668. Volume 12, Issue 5 (Jul. - Aug. 2013), PP 56-61 www.iosrjournals.org Project Managers Vs Operations Managers: A comparison based on the style of leadership Hadi Minavand1, Vahid Minaei2, Seyed Ehsan Mokhtari2, Nasrin Izadian2, Atefeh Jamshidian2 1&2International Business School / Universiti Teknologi Malaysia (UTM) Abstract: Within a century after the emergence of the initial theories in leadership area, several theories have tried to explain the different styles of leadership and the extent to which leaders’ styles can affect the overall success of the teams or the organizations being led by them. Regardless of the different ways in which these theories explain and address the styles of leadership, two concepts of ‘task’ and ‘individual’ are focused by most of them. Leaders, depending on their personal traits, attitudes, and situational considerations may show different levels of concern for tasks and individuals. Also, the environment in which a leader operates may affect the leader’s concern for tasks or individuals. Project environments, regarding the temporary nature of project- based activities, basically differ from operational environments in several aspects. Consequently, leadership in project environments may require a different style in comparison with operational environments. The current study has applied ‘concern for tasks’ and ‘concern for individuals’ as two dependent variables to make a comparison between project managers and operations managers based on the style of leadership. An online survey in a global context helped us to collect data from 159 project managers and 171 operations managers. The respondents were from different countries and various disciplines. -

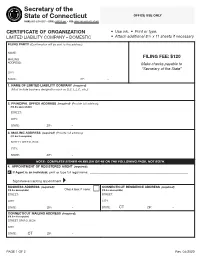

Certificate of Organization (LLC

Secretary of the State of Connecticut OFFICE USE ONLY PHONE: 860-509-6003 • EMAIL: [email protected] • WEB: www.concord-sots.ct.gov CERTIFICATE OF ORGANIZATION • Use ink. • Print or type. LIMITED LIABILITY COMPANY – DOMESTIC • Attach additional 8 ½ x 11 sheets if necessary. FILING PARTY (Confirmation will be sent to this address): NAME: FILING FEE: $120 MAILING ADDRESS: Make checks payable to “Secretary of the State” CITY: STATE: ZIP: – 1. NAME OF LIMITED LIABILITY COMPANY (required) (Must include business designation such as LLC, L.L.C., etc.): 2. PRINCIPAL OFFICE ADDRESS (required) (Provide full address): (P.O. Box unacceptable) STREET: CITY: STATE: ZIP: – 3. MAILING ADDRESS (required) (Provide full address): (P.O. Box IS acceptable) STREET OR P.O. BOX: CITY: STATE: ZIP: – NOTE: COMPLETE EITHER 4A BELOW OR 4B ON THE FOLLOWING PAGE, NOT BOTH. 4. APPOINTMENT OF REGISTERED AGENT (required): A. If Agent is an individual, print or type full legal name: _______________________________________________________________ Signature accepting appointment ▸ ____________________________________________________________________________________ BUSINESS ADDRESS (required): CONNECTICUT RESIDENCE ADDRESS (required): (P.O. Box unacceptable) Check box if none: (P.O. Box unacceptable) STREET: STREET: CITY: CITY: STATE: ZIP: – STATE: CT ZIP: – CONNECTICUT MAILING ADDRESS (required): (P.O. Box IS acceptable) STREET OR P.O. BOX: CITY: STATE: CT ZIP: – PAGE 1 OF 2 Rev. 04/2020 Secretary of the State of Connecticut OFFICE USE ONLY PHONE: 860-509-6003 • EMAIL: [email protected] -

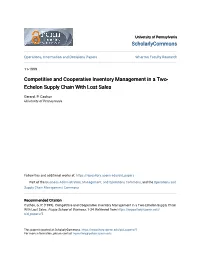

Competitive and Cooperative Inventory Management in a Two- Echelon Supply Chain with Lost Sales

University of Pennsylvania ScholarlyCommons Operations, Information and Decisions Papers Wharton Faculty Research 11-1999 Competitive and Cooperative Inventory Management in a Two- Echelon Supply Chain With Lost Sales Gerard. P. Cachon University of Pennsylvania Follow this and additional works at: https://repository.upenn.edu/oid_papers Part of the Business Administration, Management, and Operations Commons, and the Operations and Supply Chain Management Commons Recommended Citation Cachon, G. P. (1999). Competitive and Cooperative Inventory Management in a Two-Echelon Supply Chain With Lost Sales. Fuqua School of Business, 1-34. Retrieved from https://repository.upenn.edu/ oid_papers/5 This paper is posted at ScholarlyCommons. https://repository.upenn.edu/oid_papers/5 For more information, please contact [email protected]. Competitive and Cooperative Inventory Management in a Two-Echelon Supply Chain With Lost Sales Abstract This paper studies inventory management in a two echelon supply chain with stochastic demand and lost sales. The optimal policy is evaluated and compared with the competitive solution, the outcome of a game between a supplier and a retailer in which each firm attempts ot maximize its own profit. It is shown that supply chain profit in the competitive solution is always less than the optimal profit. However, the magnitude of the competition penalty is sometimes a trifle, sometimes enormous. Several contracts are considered to align the firms’ incentives so that they choose supply chain optimal actions. These contracts contain one or more of the following elements: a retailer holding cost subsidy (which acts like a buy-back/return policy), a lost sales transfer payment (which acts like a revenue sharing contract) and inventory holding cost sharing. -

Transforming the Retail Supply Chain Apparel, Fashion and Footwear GS1 Standards in Action

Transforming the Retail Supply Chain Apparel, Fashion and Footwear GS1 Standards in Action Collaborating in the dynamic retail industry In today’s omni-channel retail world, consumers are in control. They have embraced social media, online search and mobile apps—giving them instant access to product information to make buying decisions. Consumers are driving a retail environment where fast fashion translates to high-speed product turnover and a vast number of stock-keeping units that must be managed. On the supply side, retail production is complex and “ Implementing EPC-enabled truly global in scope where brands and manufacturers alike source materials and labour from a worldwide network of suppliers. RFID technology has been This dynamic retail industry calls for increased collaboration across the one of the most significant supply chain for improved speed-to-market capabilities and efficiencies. technological steps Partners in the apparel, fashion and footwear (AFF) sector are looking to inventory management and procurement processes to help drive Macy’s has taken toward these improvements. improving our supply Inventory Accuracy with EPC/RFID chain performance, and Industry leaders are starting to “tag at the source” by applying GS1 ultimately our customer EPC-enabled RFID tags on items at the point of manufacture. Using service, in the last 20 years. standards-based product identifiers—Serialised Global Trade Item Numbers (SGTINs) encoded into EPC tags, manufacturers can provide true visibility It is one of the keys to our of merchandise as it travels to distribution centres and stores. omni-channel success, and Brand owners utilise EPCs to easily verify the accuracy and completeness because we’ve already of shipments received—each identified by a GS1 Serial Shipping Container Code (SSCC)—and can track shipping processes to reduce counterfeits seen solid results, we from entering the supply chain. -

Global Trade and Supply Chain Management Sector Economic

Connecting Industry, Education & Training Sam Kaplan, Director, Center of Excellence for Global Trade & Supply Chain Management The Mission of the Center of Excellence for Global Trade & Supply Chain Management is to build a skilled workforce for international trade, supply chain management, and logistics. 2 Defining the Supply Chain Sector “If you can’t measure it, you can’t improve it.” “You can't miss what you can't measure.” – Peter Drucker —George Clinton, Funkadelic 3 Illustrative Companies Segment Subsector/Activity Description and Organizations Domestic and international freight vessels, Marine cargo shipping e.g., Tote, as well as supporting operations Tote Maritime, Foss Maritime such as tugs. Movement of cargo from one mode to another BNSF, UP, SSA Marine, Transloading & Intermodal and consolidation and repackaging of goods, MacMillan-Piper, Oak Harbor including between container sizes. Freight Lines. Transportation, Distribution Air cargo jobs at Alaska & Logistics Freight airlines (e.g., Air China) and air cargo Air cargo shipping Airlines and Delta, Hanjin ground-handling operation. Global Logistics, Swissport. Freight forwarding Freight arrangement and 3rd Party Logistics Expeditors International Warehousing & storage Dry and cold storage facilities and packaging. Couriers Express delivery services DHL, FedEx, UPS Procurement and supply chain management Procurement, sales, import and export of Supply chain and Supply Chain Management across local manufacturers, wholesalers, finished and/or intermediate goods and procurement units within local shippers materials, customer service. manufacturers. Letters of credit and other short-term lending U.S. Bank, Bank of America, Trade finance for exporters and importers. Washington Trust Supply Chain Services Compliance ITAR and other regulatory compliance issues. -

Wolfsberg Group Trade Finance Principles 2019

Trade Finance Principles 1 The Wolfsberg Group, ICC and BAFT Trade Finance Principles 2019 amendment PUBLIC Trade Finance Principles 2 Copyright © 2019, Wolfsberg Group, International Chamber of Commerce (ICC) and BAFT Wolfsberg Group, ICC and BAFT hold all copyright and other intellectual property rights in this collective work and encourage its reproduction and dissemination subject to the following: Wolfsberg Group, ICC and BAFT must be cited as the source and copyright holder mentioning the title of the document and the publication year if available. Express written permission must be obtained for any modification, adaptation or translation, for any commercial use and for use in any manner that implies that another organization or person is the source of, or is associated with, the work. The work may not be reproduced or made available on websites except through a link to the relevant Wolfsberg Group, ICC and/or BAFT web page (not to the document itself). Permission can be requested from the Wolfsberg Group, ICC or BAFT. This document was prepared for general information purposes only, does not purport to be comprehensive and is not intended as legal advice. The opinions expressed are subject to change without notice and any reliance upon information contained in the document is solely and exclusively at your own risk. The publishing organisations and the contributors are not engaged in rendering legal or other expert professional services for which outside competent professionals should be sought. PUBLIC Trade Finance Principles -

Why Procurement Professionals Should Be Engaged in Supply Chain

business solutions for a sustainable world WBCSD Future Leaders Team (FLT) 2011 Why procurement professionals should be engaged in supply chain sustainability “The Future Leaders Team is an unparalleled of common challenges – across sectors – and learning experience for young managers of WBCSD shared best practices. Above all, they experienced member companies. They have the opportunity to what is recommended here: engaging people in understand the benefits of why sustainability matters sustainability. I am convinced that they brought back to business and to develop a solid international valuable knowledge and information to their jobs.“ and professional network. Sustainability is complex subject is some cases, and it is therefore crucial for Congratulations to Eugenia Ceballos, John Zhao, multinational companies to enrich their work with Baptiste Raymond, and to all participants of the other companies’ experiences through collaboration. Future Leaders Team 2011! FLT 2011’s theme was sustainability in the supply chain, which is increasingly considered as an area of direct responsibility for companies. The following report reflects FLTs’ peer learning experience and team work. This is not the work of experts or consultants. Rather, the three managers from DuPont China, Holcim and Lafarge, took this opportunity Kareen Rispal, to engage with key people across functions and Lafarge Senior Vice President, geographies within their companies. In doing Sustainable Development so, they have deepened their understanding and Public Affairs I. Why procurement functions all stakeholders involved in bringing products and services to market. should be engaged in sustainability for their We believe that a sustainable supply chain can drive supply chain: competition and profit, and is a great opportunity to make a difference to companies, communities 1. -

Historical Evolution of Management Accounting

1990's: Value Based Management Focus shifted to include the creation of customer value, strategy, balanced scorecards, EVA, and other related concepts. 1980's: Lcan Enterprise CA M-I Cost Management Focus shifted to the reduction of waste, JTT, teamwork, ABC, target costing, quality, investment & product life cycle management. 1951 - 1980's: Managerial Accounting Focus shifted to providinginformation for management planning & control. 1920 - 1950: Cost Accounting Matching concept developed. Focus on cost determination and financial control. 1812 - 1920: Accountingfor Processes Prior to the matching concept. Focus on operating cost and efficiency of processes. Shah Kamal Historical Evolution of Assistant Relationship Manager Management Accounting Bank Alfalah [email protected] Abstract The obsolescence of most companies' cost accounting and management control systems is particularly unfortunate for the global competition of the 1980s (Johnson & Kaplan, 1987). During the past two decades, conventional cost and management accounting practices have been under extensive criticism for their malfunction to instigate change and their inability to support management accounting innovations in coping with the requirements of a changing environment. The academic literature has been crucial of conventional management accounting systems particularly for their lack of efficiency and capability to present comprehensive and the latest information and to assure decision makers and potential users of such information. Focusing on this debate, current study reviews the evolution of cost and management accounting innovations over the past century around the world and to examine whether there has been a significant impact of management accounting in the organization. The analyses suggest that management accounting is changing. However, these changes do not have much bearing upon the type of management accounting techniques. -

Trade Management Guidelines

Trade Management Guidelines TRADE MANAGEMENT TASK FORCE Theodore R. Aronson, CFA, Chairman Aronson + Partners Gregory H. Bokach, CFA Damian Maroun American Century Investment Management G.E. Asset Management Corporation Eugene K. Bolton Jean Margo Reid G.E. Asset Management Corporation Paul Richards* Michael H. Buek, CFA Financial Services Authority The Vanguard Group H. Paul Reynolds Richard A. Carriuolo Frank Russell Securities, Inc. R.M. Davis, Inc. George U. Sauter Gene A. Gohlke, Ph.D., CPA* The Vanguard Group U.S. Securities and Exchange Commission Erik R. Sirri Paul S. Gottlieb Babson College Merrill Lynch Wayne H. Wagner Joanne M. Hill Plexus Group Goldman, Sachs & Co. Jessica L. Mann, CFA Donald B. Keim CFA Institute The Wharton School Maria J. A. Clark, CFA Anthony J. Leitner CFA Institute Goldman, Sachs & Co. Ananth Madhavan ITG, Inc. * Observer. 1 CFA INSTITUTE TRADE MANAGEMENT GUIDELINES Recognizing the ambiguities and complexities surrounding the concept of Best Execution,1 CFA Institute Trade Management Task Force has developed the CFA Institute Trade Management Guidelines (Guidelines) for investment management firms (Firms). The recommendations contained herein stem from the obligations Firms have to clients regarding the execution of their trades and provide Firms with a demonstrable framework from which to make consistently good trade-execution decisions over time. The Guidelines formalize processes, disclosures, and record-keeping suggestions that, together, form a systematic, repeatable, and demonstrable approach to seeking Best Execution. It is important to note that the Guidelines are a compilation of recommended practices and not standards. CFA Institute encourages Firms worldwide to adopt as many of the recommendations as are appropriate to their particular circumstances. -

Extensions of Remarks

October 5, 1970 EXTENSIONS OF REMARKS 34:953 EXTENSIONS OF REMARKS GOVERNOR ROCKEFELLER SPEAKS Around this State there are nine other We need a unified system for financing AT THE OLDER AMERICAN WHITE meetings of this conference; and my voice is medical care, like Universal Health Insur going out to each meeting over a special ance. HOUSE FORUM telephone hookup. I've tried to get it In our State, I'll keep I want all of you out there and here to trying. HON. JACOB K. JAVITS know that what you tell me Is just as im But, Universal Health Insurance would portant as what I'm going to tell you; be work better on a national basis. OF NEW YORK cause this is your conference. I hope that the State and regional com IN THE SENATE OF THE UNITED STATES What you say will determine the shape mittees that Will be working on recommenda of this State's recommendations at next Monday, October 5, 1970 tions for the White House Conference on year's White House Conference on Aging. Aging Will give Universal Health Insurance Mr. JAVITS. Mr. President, on Sep But it all begins here and now. a strong recommendation. tember 23, the New York State Office for So my real job today Is not so much to Another thing some older people want to the Aging officially launched our State's talk. do or need to do is work. preparations for the 1971 White House It's to listen to you. Yet, the Federal Social Security law penal Conference on Aging with 10 Regional And one way we'll be listening is by izes work, in a sense. -

TRANSFORM YOUR CUSTOMER MARKETING Improve Engagement, Reach, and Advocacy with Online Community 1

TRANSFORM YOUR CUSTOMER MARKETING Improve engagement, reach, and advocacy with online community 1 INTRODUCTION Customer marketers have a tough job. They’re tasked with keeping customers interested after the initial sales push, opening the door for sales to convince customers to buy more from the company, and finding customers who are happy enough to advocate for the organization. All of this requires you to be in tune with your customers' needs, which is a monumental task. The organizations who win at engagement make those customers feel like next-door neighbors. How can you reach the right customers when they're spread out across devices, interests, and locations? CUSTOMER MARKETERS, MEET ONLINE COMMUNITIES When so much of the world is digital, it should be easy to reach customers, and online community software makes that a reality. You can bring your customers together, all in one place online, where they can talk and exchange ideas. Engagement is its natural outcome. And even more than that, you can use online community to help, curate, and create. TRANSFORM YOUR CUSTOMER MARKETING ©HIGHER LOGIC. ALL RIGHTS RESERVED 2 HOW CAN AN ONLINE COMMUNITY TRANSFORM THE CUSTOMER MARKETER'S ROLE? Transformation is a big concept, but online communities can deliver. They’re a growing channel for customer marketing teams because they can transform your day-to-day, no matter the size of your team. With an online community, customer marketers have a comprehensive platform to engage customers, with multiple tools at their disposal, such as: » Automation rules to encourage participation » User-generated content promoting upsell opportunities » Gamification to pique interest and keep interactions both fun and organic Customer marketers can use a myriad of online community tools to get customers more engaged, reach customers for upsell opportunities, and scale advocacy programs. -

Organizational Culture Model

A MODEL of ORGANIZATIONAL CULTURE By Don Arendt – Dec. 2008 In discussions on the subjects of system safety and safety management, we hear a lot about “safety culture,” but less is said about how these concepts relate to things we can observe, test, and manage. The model in the diagram below can be used to illustrate components of the system, psychological elements of the people in the system and their individual and collective behaviors in terms of system performance. This model is based on work started by Stanford psychologist Albert Bandura in the 1970’s. It’s also featured in E. Scott Geller’s text, The Psychology of Safety Handbook. Bandura called the interaction between these elements “reciprocal determinism.” We don’t need to know that but it basically means that the elements in the system can cause each other. One element can affect the others or be affected by the others. System and Environment The first element we should consider is the system/environment element. This is where the processes of the SMS “live.” This is also the most tangible of the elements and the one that can be most directly affected by management actions. The organization’s policy, organizational structure, accountability frameworks, procedures, controls, facilities, equipment, and software that make up the workplace conditions under which employees work all reside in this element. Elements of the operational environment such as markets, industry standards, legal and regulatory frameworks, and business relations such as contracts and alliances also affect the make up part of the system’s environment. These elements together form the vital underpinnings of this thing we call “culture.” Psychology The next element, the psychological element, concerns how the people in the organization think and feel about various aspects of organizational performance, including safety.