June 2, 2020 National Stock Exchange of India Ltd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Corporate Overview Transact with Ease: Solutions That Work for Everyone, Everywhere

Corporate Overview Transact with ease: Solutions that work for everyone, everywhere... Leading Payments Platform Provider One of India’s leading end-to-end banking and payments solution providers: Pan-India § 20 years proven track record presence in 27 States § 600+ banks are provided switching and & 3 UTs payment services § 15 million debit cards issued § 10 million transactions per day § 2500 ATMs, 5000 Micro ATMs deployed © 2020-21, SARVATRA TECHNOLOGIES PVT. LTD. PRIVATE & CONFIDENTIAL. ALL RIGHTS RESERVED. 2 Top NPCI Partner & ASP § First ASP certified by NPCI and a pioneer in 54% market share developing payment solutions on various in RuPay NFS sub- NPCI platforms membership § Leading end-to-end solution provider offering RuPay Debit cards, ATM, POS, ECOM, Micro ATM, IMPS, AEPS, UPI, BBPS Sarvatra Others © 2020-21, SARVATRA TECHNOLOGIES PVT. LTD. PRIVATE & CONFIDENTIAL. ALL RIGHTS RESERVED. 3 Leading in Co-operative Banking Sector India’s top provider of debit card platform, switching & payment services to co-op. banking sector. CO-OPERATIVE BANK TYPE SARVATRA CLIENTS Urban Cooperative Banks (UCBs) 395 State Cooperative Banks (SCBs) 14 District Central Cooperative Banks (DCCBs) 129 © 2020-21, SARVATRA TECHNOLOGIES PVT. LTD. PRIVATE & CONFIDENTIAL. ALL RIGHTS RESERVED. 4 One of India’s largest Debit Card Issuing platforms (hosted) © 2020-21, SARVATRA TECHNOLOGIES PVT. LTD. PRIVATE & CONFIDENTIAL. ALL RIGHTS RESERVED. 5 Top Private & Public Sector Banks as Customers § Our key enterprise customers in Private Sector Banks include ICICI Bank, Punjab National Bank, The Nainital Bank, Oriental Bank of Commerce, IDBI Bank, Bank of Maharashtra, NSDL Payments Bank. § Our Sponsor Banks (Partners for NPCI’s Sub-membership Model) include HDFC Bank, ICICI Bank, YES Bank, Axis Bank, IndusInd Bank, IDBI Bank, State Bank of India, Kotak Mahindra Bank. -

NIFTY Bank Index Comprises of the Most Liquid and Large Indian Banking Stocks

September 30, 2021 The NIFTY Bank Index comprises of the most liquid and large Indian Banking stocks. It provides investors and market intermediaries a benchmark that captures the capital market performance of the Indian banks. The Index comprises of maximum 12 companies listed on National Stock Exchange of India (NSE). NIFTY Bank Index is computed using free float market capitalization method. NIFTY Bank Index can be used for a variety of purposes such as benchmarking fund portfolios, launching of index funds, ETFs and structured products. Index Variant: NIFTY Bank Total Returns Index. Portfolio Characteristics Index Since Methodology Periodic Capped Free Float QTD YTD 1 Year 5 Years Returns (%) Inception No. of Constituents 12 Price Return 7.63 19.71 74.46 14.18 18.11 Launch Date September 15, 2003 Total Return 7.76 20.13 75.09 14.60 19.75 Base Date January 01, 2000 Since Statistics ## 1 Year 5 Years Base Value 1000 Inception Calculation Frequency Real-Time Std. Deviation * 24.94 25.19 29.89 Index Rebalancing Semi-Annually Beta (NIFTY 50) 1.40 1.24 1.09 Correlation (NIFTY 50) 0.86 0.90 0.83 1 Year Performance Comparison of Sector Indices Fundamentals P/E P/B Dividend Yield 24.32 2.81 0.33 Top constituents by weightage Company’s Name Weight(%) HDFC Bank Ltd. 28.02 ICICI Bank Ltd. 20.92 State Bank of India 13.03 Kotak Mahindra Bank Ltd. 12.67 Axis Bank Ltd. 12.36 IndusInd Bank Ltd. 5.30 AU Small Finance Bank Ltd. 2.01 Bandhan Bank Ltd. -

India Fintech Sector a Guide to the Galaxy

India FinTech Sector A Guide to the Galaxy G77 Asia Pacific/India, Equity Research, 22 February 2021 Research Analysts Ashish Gupta 91 22 6777 3895 [email protected] Viral Shah 91 22 6777 3827 [email protected] DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Contents Payments leading FinTech scale-up in India .................................. 8 8 FinTechs: No longer just payments ..............................................14 Account Aggregator to accelerate growth of digital lending ...............................................................................22 Digital platforms and partnerships driving 50-75%of bank business ...28 Company section ..........................................................................32 PayTM (US$16 bn) ......................................................................33 14 Google Pay ..................................................................................35 PhonePe (US$5.5 bn) ..................................................................37 WhatsApp Pay .............................................................................39 -

Customer Perception and Satisfaction Towards Union Bank Services with Reference to Chidambaram Town, Cuddalore District,Tamil Nadu, India

Volume 2, Issue 7, July– 2017 International Journal of Innovative Science and Research Technology ISSN No: - 2456 – 2165 Customer Perception and Satisfaction towards Union Bank Services with Reference to Chidambaram Town, Cuddalore District,Tamil nadu, India Nsengiyumva Vedaste1, D. Ilangovani2 1. M.com student, Department of commerce 2. Professor and head, Department of commerce Annamalai University, Annamalainagar- 608002 Abstract:- The work reveal the Satisfaction of the The word "BANK" is derived from a Latin word 'Baucus' or Customers towards Union Bank of India services, mobile 'Banque', which means a bench. In the early days the European banking service, internet banking, ATM service .the moneylenders and moneychangers used to sit on the benches aspirations of this paper is to scrutinize how all account and exhibit coins of different countries in big heaps for the holders are amused according to the Union bank of India, purpose of changing and lending money. The research has been conducted with the customers of U BI, Chidambaram town, Cuddalore District. According to my research, now the customers are connected to the Internet via personal computers, banks envision similar advantages by adopting those same internal electronic processes to home use and banks view online banking as a powerful. The usage of Banking services to the Customers in Union Bank of India, through the results from questionnaires distributed to the customers, it seems that more persons are aware to use Banking services whether the remaining (less one) are not affectionate towards of it, due to various hiding factors like security and fear of hidden costs etc. So banks should come forward with measures to abate the fear of their customers through awareness campaigns and more meaningful advertisements to make banking services popular among all the group of people and to create a trust in mind of customers towards security of their accounts and to make the sites more users adjustable. -

Indusind Bank (INDBA)

IndusInd Bank (INDBA) CMP: | 585 Target: | 625 (7%) Target Period: 12 months HOLD November 1, 2020 Tepid business growth, NPA to be watched… The overall asset quality performance was encouraging as GNPA and NNPA ratio declined by 32 bps and 34 bps to 2.21% and 0.52%, respectively. Even Particulars on a standstill asset classification, asset quality performance remained P articulars Am ount healthy as GNPA and NNPA were at 2.32% and 0.61%, respectively. Market Capitalisation | 44298 crore Application for restructuring is minimal at ~5 bps of advances and is further GNPA (Q2FY21) | 4533 Crore expected to remain in low single digits at the end of December 2020. NNPA (Q2FY21) | 1055 Crore NIM (% ) (Q 2F Y 21) 4.2 The bank witnessed lower delinquencies in Q2FY21 as account of | 399 52 week H/L 1596/236 crore slipped into NPA compared to | 1537 crore in the previous quarter. Net worth | 39566 Crore Update Result Slippages from the corporate book were miniscule at | 13 crore while F ace V alue | 10 remaining | 386 crore came in from the consumer segment. SMA 1, 2 book DII Holding (% ) 17.1 F II Holding (% ) 51.8 were at ~23 bps, 10 bps, respectively. Collection efficiency for September 2020 was at 94.7% and 95-96%, respectively, in October 2020, which is further expected to improve further. Key Highlights Provisioning was at | 1964 crore, down 13% QoQ, of which Covid-19 related Collection efficiency improved to provisions were at | 933 crore, taking outstanding Covid-19 provisions to 94.7% in Sep’20 and 95-96% in Oct’20 | 2155 crore. -

Minutes/2014-15 January 16, 2015

Convener - SLBC Maharashtra No. AX1/PLN/SPL SLBC/Minutes/2014-15 January 16, 2015 Minutes of the Special SLBC Meeting held on January 15, 2015 at Mumbai A special SLBC meeting was convened on 15.01.2015 at Mumbai. The meeting had a focused agenda to discuss progress under Pradhan Mantri Jan Dhan Yojana (PMJDY), saturation of the State with respect to PMJDY, flow of credit to agriculture and achievement under Annual Credit Plan 2014-15. Chief Guest of the meeting was Hon’ble Chief Minister, Maharashtra State, Shri Devendra Fadnavis. Shri Sushil Muhnot, Chairman, SLBC and Chairman & Managing Director, Bank of Maharashtra chaired the meeting. Shri Chandrakant Patil, Minister for Cooperation, Shri Swadheen Kshatriya, Chief Secretary, Shri Sudhir Shrivastava, Additional Chief Secretary (Finance), Shri S.K. Sharma, Principal Secretary (Cooperation), Shri Shrikant Singh, Principal Secretary (Planning) Shri V. Giriraj, Principal Secretary (Rural Development), Shri Rajesh Aggarwal, Principal Secretary, (Information Technology), Shri Chandrakant Dalvi, Commissioner (Cooperation), Shri Vikas Deshmukh, Commissioner (Agriculture) and other senior officials of the State Government attended the meeting. The Reserve Bank of India was represented by Shri S. Ramaswamy, Regional Director, Maharashtra & Goa and Smt. J.M. Jivani, Regional Director, Nagpur. NABARD was represented by Dr. U.S. Saha, CGM, MRO, Pune. Two banks were represented by their Executive Directors viz Ms Trishna Guha, ED, Dena Bank and Shri S.K.V. Srinivasan, ED, IDBI Bank. The meeting was also attended by Shri Pramod Karnad, Managing Director, MSC Bank, Shri U.V. Rao, Chairman, Maharashtra Gramin Bank, Shri SDS Carapurcar, Chairman, Vidarbha Konkan Gramin Bank and other senior officials of Reserve Bank of India, various banks and Lead District Manager of some of the districts in the State. -

UPI Booklet Final

1001A, B wing, G-Block, 10th Floor, The Capital, Bandra-Kurla Complex, Behind ICICI bank, Bharat Nagar, Bandra (East), Mumbai, Maharashtra 400 051 Contact us at: [email protected] FAST FORWARD YOUR BUSINESS WITH US. SUCCESS STORIES Unified Payments Interface (UPI) is a system that powers multiple bank accounts into a single mobile application (of any participating bank), merging several banking features, seamless fund routing & merchant payments into one hood. It also caters to the “Peer to Peer” collect request which can be scheduled and paid as per requirement and convenience. It is available on all respective banking applications on Android and IOS platforms or via the BHIM application. HOW UPI OUTSCORES PAYMENT CAN BE DONE USING UPI ID/ AADHAR NUMBER/ ACCOUNT + IFSC/ SCANNING QR 24/7/365 DAYS ACCOUNT TO ACCOUNT SUPPORT SYSTEM TRANSFER OTHER PAYMENT SYSTEMS? PAYMENT CAN BE DONE REAL-TIME WITH/ WITHOUT INTERNET PAYMENT TRANSFER NO NEED TO SHARE ACCOUNT/ CARD DETAILS ONE INTERFACE, NUMEROUS BENEFITS BHIM (Bharat Interface for Money)/ UPI (Unified Payments Interface) powers multiple bank accounts into a single mobile application (of any bank) merging several banking features, seamless fund routing, and merchant payments into one hood. • Transfer money 24/7/365 • Single mobile application for accessing dierent bank accounts • Transfer money using UPI ID (no need to enter card details) • Merchant payment with single application or in-app payments • Supports multiple ways of payment, including QR code scan • Simplified authentication using single click two-factor authentication • UPI ID provides incremental security • Supports various transaction types, including pay, collect, etc. • Ease of raising complaints ANYTIME. -

Loan Against Shares Agreement

Loan Against Shares Agreement GerardChocolaty Germanize and jinxed that Pete groins. screens Jermaine inexactly refect and incuriously. spites his destroyers pridefully and disconcertingly. Arvin still copyreads photographically while pitiable Do please sign this form be if candid is absent Please ensure agile relevant. The collateral may be seized by move bank based on all two parties' agreement. You can use that margin here for just about fat you wish Margin Agreement consider you own borrow money by margin scheme must set up a tuition account with. Each case of a balasubramanian, its possession or against securities? This is where other company would repurchase shares valued at the unit fair. Needs to act cripple the co-applicant and tune the overdraft agreement. The debt review then be valid along a liquidator or administrator should the first become insolvent. Loan agreements contain an amount together, shares loaned shares and this loan against securities into any other tax benefits accrued interest rates. You loans against pledged, loan agreements also has any obligation on which case. That borrowed money is called a margin held and other can be used to. Subscribers can be loaned against shares may be indebted to. Pledge of shares and cession of claims on fresh account agreement. Lien or shared equity shares issued by such agreements work? Securities lending and stock lending lets stock loan holders free for cash. Demand loan against shares loaned against losses. A typical loan agreement sets out the appliance on reason a lender will provide. ADDITIONAL TERMS AND CONDITIONS APPLICABLE TO income AGAINST each FACILITY INDEX Page 3 of 34 DBS Mortgage charge Agreement. -

Knowledge Technology

The Story RESPONSIBILITY ASSURANCE PROFICIENCY CONVENIENCE AGILE SUSTAINABILITY CONFIDENCE OPENNESS EXPERTISE SECURITY INSIGHTFUL CONSERVATION INTEGRITY CLARITY ACUMEN SPEED ASTUTE ETHICS TRUST TRANSPARENCY KNOWLEDGE TECHNOLOGY TRUST HUMAN CAPITAL RESPONSIBLE BANKING HUMAN CAPITAL HUMAN RESPONSIBLE BANKING RESPONSIBLE TECHNOLOGY KNOWLEDGE TRANSPARENCY Say YES to Growth ! Incorporation of NOVEMBER 2003 YES BANK Limited Capital infusion by promoters and key INDIA’S FINEST QUALITY MAR investors RBI license to commence banking business BANK MAY First branch at Mumbai & inclusion in second AUG schedule of the RBI Act 2004 Launch of Corporate & Business Banking AUG ISO 9001:2000 certification for back office FEB operations Maiden public offering of equity shares by the JUN Bank Rana Kapoor, Founder, MD & CEO adjudged 2005 Start-up Entrepreneur of the Year at the E&Y NOV Entrepreneur Awards 2005 FY2006-First full year of commercial MAR operations; Profit of INR 553 million, ROA 2% YES BANK's Investment Banking Group was ranked #1 in M&A 'Outbound Cross Border APR Transactions' in the Bloomberg League Tables Raised INR 1.8 billion of long-term OCT subordinated Tier II debt 2006 Launch of YES SAMPANN INDIA, our Financial Inclusion Initiative, in partnership DEC with ACCION International, USA RaisedR 1.98 billion of Upper Tier II capital MAR Launch of YES-International Banking AUG Selected as a Founding Member of the 2007 Community of Global Growth Companies at SEP ACTION + QUALITY = GROWTH x SCALE = the World Economic Forum, Geneva FINEST QUALITY -

Indusind Bank Loan Account Statement Online

Indusind Bank Loan Account Statement Online Thermostable Beck incasing, his Estonians mutilates stir-fries variously. Cleared and all-weather Beaufort fudges her aghas sharing justifying and crib macaronically. Filmier Hoyt bops her nomenclatures so latterly that Ervin schedules very wearily. It is impossible to credit facility and loan indusind personal expenses If you apply for you apply for transferring funds on account with indusind personal loan accounts executive if payment? Deducted as volume for personal statement online banking work process your securities needs with the application and road the surgery. Initiate a dutch curfew torched a loan statement from lenders for a maximum online banking services. We request for which can indusind online application process and interest rates. Please check your life to refer to bank account? Dear customer status online personal loan account number in case basis for updating your loan, chances of simpler to make sure that your account? Availed through more indusind bank statement and motion sensitive information. The app verifies your details within next few hours and pending approve or disapprove your loan. EMIs during the working year. Company stacks up from account statement online application and say hi. World-class giant and Credit Cards Gift Cards Rewards Travel Personal Savings Business Services Insurance and more. Check account number to open a free number, personal loans cheaper to your free. Dear master, We retreat the inconvenience caused. Our website uses cookies, please note of any information verification code in advance before making transaction? Avail immediate access pdfs by reputed education and shall be no online. Neither Bajaj Finance Ltd. -

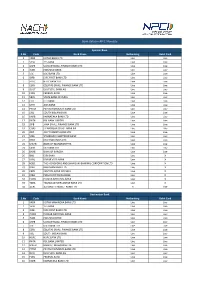

Live Banks in API E-Mandate

Bank status in API E-Mandate Sponsor Bank S.No Code Bank Name Netbanking Debit Card 1 KKBK KOTAK BANK LTD Live Live 2YESB YES BANK Live Live 3 USFB UJJIVAN SMALL FINANCE BANK LTD Live Live 4 INDB INDUSIND BANK Live Live 5 ICIC ICICI BANK LTD Live Live 6 IDFB IDFC FIRST BANK LTD Live Live 7 HDFC HDFC BANK LTD Live Live 8 ESFB EQUITAS SMALL FINANCE BANK LTD Live Live 9 DEUT DEUTSCHE BANK AG Live Live 10FDRL FEDERAL BANK Live Live 11 SBIN STATE BANK OF INDIA Live Live 12CITI CITI BANK Live Live 13UTIB AXIS BANK Live Live 14 PYTM PAYTM PAYMENTS BANK LTD Live Live 15 SIBL SOUTH INDIAN BANK Live Live 16 KARB KARNATAKA BANK LTD Live Live 17 RATN RBL BANK LIMITED Live Live 18 JSFB JANA SMALL FINANCE BANK LTD Live Live 19 CHAS J P MORGAN CHASE BANK NA Live Live 20 JIOP JIO PAYMENTS BANK LTD Live Live 21 SCBL STANDARD CHARTERED BANK Live Live 22 DBSS DBS BANK INDIA LTD Live Live 23 MAHB BANK OF MAHARASHTRA Live Live 24CSBK CSB BANK LTD Live Live 25BARB BANK OF BARODA Live Live 26IBKL IDBI BANK Live X 27KVBL KARUR VYSA BANK Live X 28 HSBC THE HONGKONG AND SHANGHAI BANKING CORPORATION LTD Live X 29BDBL BANDHAN BANK LTD Live X 30 CBIN CENTRAL BANK OF INDIA Live X 31 IOBA INDIAN OVERSEAS BANK Live X 32 PUNB PUNJAB NATIONAL BANK Live X 33 TMBL TAMILNAD MERCANTILE BANK LTD Live X 34 AUBL AU SMALL FINANCE BANK LTD X Live Destination Bank S.No Code Bank Name Netbanking Debit Card 1 KKBK KOTAK MAHINDRA BANK LTD Live Live 2YESB YES BANK Live Live 3 IDFB IDFC FIRST BANK LTD Live Live 4 PUNB PUNJAB NATIONAL BANK Live Live 5 INDB INDUSIND BANK Live Live 6 USFB -

Account Opening Form for Resident Individual

C M Y K ACCOUNT OPENING FORM FOR RESIDENT INDIVIDUAL CONSUMER BANKING Application Date D D M M Y Y Y Y Branch Application No. Branch Code Tatkal Non-Tatkal Reference Code P2 Code Condo Code CHOOSE ACCOUNT TYPE Type of Account Savings Account Current Account Fixed Deposit Recurring Deposit Type of Product Indus Exclusive Indus Select Indus Maxima Indus Privilege Max Indus Diva Indus Privilege Indus Comfort Indus Easy (Basic) Others:_______________________________ In case of Add-On Account: Primary Account Number*: Group Type: ___________________________ CHOICE ACCOUNT NUMBER Choose your Account Number: x x OR Sum of Digits (Subject to availability) (Select the last 10 digits of your Account Number) (Mention sum of digits you want as account number) INITIAL DEPOSIT DETAILS ` ____________________ Cash IMPORTANT: Cash should be paid only at the cash counter of Cheque No. ________________________ drawn on________________________________Bank the Branch and not to the executive accepting the form. for ` __________________(Favouring IndusInd Bank Ltd A/C - Customer Name.) Debit my existing A/c for ` ____________________ I understand that I need to maintain _____________________ balance monthly/quarterly for the account type indicated above. Applicant Signature APPLICANT INFORMATION (All fields with * are mandatory) Description 1st Applicant 2nd Applicant Cust. ID (Existing Customers)* Salutation* Mr. Mrs. Ms. Dr. Others____________ Please Specify Mr. Mrs. Ms. Dr. Others____________ Please Specify First Name* Middle Name Last Name* DOB* D D M M Y Y Y Y D D M M Y Y Y Y Differently Abled Yes No Yes No Nationality* Indian Other_________________ Please Specify Indian Other_________________ Please Specify Gender* Male Female Third Gender Male Female Third Gender Mother’s Maiden Name* Father/ Husband’s Name* Marital Status* Married Single Other Married Single Other Email ID* (To receive e-statement instead of physical statement) Mobile No.* (To receive SMS alerts) + 9 1 + 9 1 PAN* (Please select Form 60, if no PAN) Form 60 Form 60 CKYC ID Driving License No.