Stranded Assets in Palm Oil Production: a Case Study of Indonesia Working Paper July 2016

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

How Dirty Palm Oil Is Feeding the Climate and Extinction

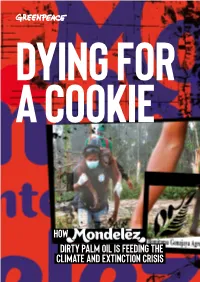

DYING FOR A COOKIE HOW DIRTY PALM OIL IS FEEDING THE CLIMATE AND EXTINCTION CRISIS ‘Wearetakingstepstoensurethatthepalmoilwebuyisproduced onlegallyheldland,doesnotleadtodeforestationorlossofpeat land,respectshumanrights,includinglandrights,anddoesnot useforcedorchildlabor.’ Mondelēz International Palm Oil Action Plan, June 2014 11 December 2016, PT Ladang Sawit Mas, 1°32’20.856”S 110°18’58.122”E: ©Ifansasti/Greenpeace Cover and right: March 2013, PT Ladang Sawit Mas:One of several orangutan rescue attempts by International Animal Rescue Indonesia in the Bumitama oil palm concession. ‘Theunsustainable useofnatural resourceshas causedadramatic declineofBornean orangutans[...]Our findingssuggest thatmorethan 100,000individuals havebeenlostinthe 16yearsbetween 1999and2015.’ Maria Voigt, researcher at the Max Planck Institute for Evolutionary Anthropology, September 2017 CONTENTS CALLING TIME ON MONDELēZ 1 EYES WIDE SHUT: HOW CONSUMER BRANDS AND THE RSPO SUPPORT THE TRADE IN DIRTY PALM OIL 2 BUMITAMA AND ITS DIRTY SECRETS 5 Bumitama’s ownership, structure and landbank 4 Quantifying Bumitama’s forest loss liability 7 Bumitama’s and IOI’s response 7 CRUNCH TIME FOR MONDELĒZ AND THE PALM OIL SECTOR 8 BUMITAMA’S LAUNDERING OF A TOXIC LEGACY 12 Associated parties 13 Citro Utomo 13 Djoni Rusmin and Tommy Santoso 14 Nita Gartika and Janta Halim 16 CASE STUDIES 20 PT Gunajaya Harapan Lestari (PT GHL), West Kalimantan 20 PT Hatiprima Agro (PT HPA), Central Kalimantan 22 PT Golden Youth Plantation Indonesia (PT GYP) and PT Ladang Sawit Mas (PT LSM), -

The Green Tigers

The Green Tigers Which Southeast Asian Companies Will Prosper in the New Age of Forest Conservation? SEPTEMBER 2014 Which Southeast Asian companies will prosper in the new age of forest conservation? © DeanBirinyi / istockphoto.com THE GREEN TIGERS Which Southeast Asian companies will prosper in the new age of forest conservation? By Glenn Hurowitz Southeast Asia’s economies are roaring. The rise of the so-called “Asian tiger” economies has been one of the most profound developments in global business over the past half-century. But even as the region grows, the manner of its growth is imperiling its future prosperity. Too much of Asia’s growth has relied upon defor- estation and pollution. Instead of pursuing lasting development, many countries and companies in the region have favored “spreadsheet development” that prioritizes goosing national gross domestic prod- uct numbers at the expense of making a positive impact on the communities where it occurs. Southeast Asia is by no means unique in pursuing this model, but it is possibly the place where it is followed most energetically—and with the most visible consequences. Too many companies are still putting the region’s environment and economy at risk through continued deforestation and other irresponsible practices. But some countries and companies are choosing a different path. They are adapting to the revolutionized global market by evolving to ensure that their growth does not come at the expense of forests. These are the Green Tigers – and they are set to roar for decades to come. There is great urgency behind this corporate evolution: Deforestation for palm oil and paper plantations has turned the region into a tinderbox. -

Unilever Palm Oil Mill List

2017 Palm Oil Mills No. Mill Name Parent Company RSPO Certified Country Province District Latitude Longitude 1 ABDI BUDI MULIA PKS 1 AATHI BAGAWATHI MANUFACTURING SDN BHD No Indonesia Sumatera Utara Labuhan Batu 2.0512694 100.252339 2 ABEDON OIL MILL KRETAM HOLDING BERHAD Yes Malaysia Sabah Kinabatangan 5.312106 117.9741 3 ACEITES CIMARRONES SAS ACEITES S.A. Yes Colombia Meta Puerto Rico 3.035593889 -73.11146556 4 ACEITES MANUELITA YAGUARITO CI BIOCOSTA Yes Colombia Meta San Carlos de Guaroa 3.882933 -73.341206 5 ACEITES MORICHAL CI BIOCOSTA No Colombia Meta San Carlos de Guaroa 3.92985 -73.242775 6 ADELA POM FELDA No Malaysia Johor Kota Tinggi 1.552768 104.1873 7 ADHYAKSA DHARMASATYA ADHYAKSA DHARMASATYA No Indonesia Kalimantan Tengah Kotawaringin Timur -1.588931 112.861883 8 ADITYA AGROINDO AGRINDO No Indonesia Kalimantan Barat Ketapang -0.476029 110.151418 9 ADOLINA PTPN IV No Indonesia Sumatera Utara Serdang Bedagai 3.568533 98.94805 10 ADONG MILL WOODMAN GROUP No Malaysia Sarawak Miri 4.541035 114.119098 11 AEK BATU WILMAR No Indonesia Sumatera Utara Labuhan Batu 1.850583 100.1457 12 AEK LOBA SOCFIN INDONESIA Yes Indonesia Sumatera Utara Asahan 2.651389 99.617778 13 AEK NABARA RAJA GARUDA MAS Yes Indonesia Sumatera Utara Labuhan Batu 1.999722222 99.93972222 14 AEK NABARA SELATAN PTPN III Yes Indonesia Sumatera Utara Labuhan Batu 2.058056 99.955278 15 AEK RASO PTPN III Yes Indonesia Sumatera Utara Labuhan Batu 1.703883 100.172217 16 AEK SIBIRONG MAJU INDO RAYA No Indonesia Sumatera Utara Tapanuli Selatan 1.409317 98.85825 17 AEK SIGALA-GALA -

NDPE Policies Cover 83% of Palm Oil Refineries; Implementation at 72%

NDPE Policies Cover 83% of Palm Oil Refineries; Implementation at 72% April 2020 Chain Reaction Research is a coalition Palm oil refiners are a strategic bottleneck in the global supply chain. Since of Aidenvironment, Profundo and Climate Advisers. 2014, the largest refiners have adopted No Deforestation, No Peat, No Exploitation (NDPE) policies, the strongest private instrument to cut the direct Contact: link between deforestation and palm oil. Refiners commit to NDPE policies that cover their own plantations and the plantations of their third-party suppliers. www.chainreactionresearch.com; This market mechanism functions best when the entire industry follows [email protected] commitments. However, non-cooperating refiners continue to leak unsustainable palm oil into the market. Authors: Albert ten Kate, Aidenvironment Key Findings: Barbara Kuepper, Profundo Matt Piotrowski, Climate Advisers • As of April 2020, NDPE policies cover 83 percent of palm oil refining With contributions from: capacity in Indonesia and Malaysia. In November 2017, this percentage Tim Steinweg, Aidenvironment stood at 74 percent. The increase is the result of six company groups with Gerard Rijk, Profundo large refining capacity adopting NDPE policies. • Because of weak implementation, effective NDPE coverage falls to 72 percent. Due to lagging transparency and grievance processes, three of the eleven largest refiners in Indonesia and Malaysia remain part of the leakage market. • The seven largest leakage refiners in Indonesia and Malaysia are FGV Holdings, Permata Hijau Group, Salim Group, BEST Group, Tunas Baru Lampung, Darmex Agro and the Wings Group. In India, the world’s largest importer of crude palm oil, there are three leakage refiners: Emami Agrotech, Patanjali Ayurved and Gokul Agro Resources. -

The Case of Malaysian Palm Oil

Agro-Commodity Global Value Chains and Upgrading: The Case of Malaysian Palm Oil Yee Siong Tong Queens’ College University of Cambridge This dissertation is submitted for the degree of Doctor of Philosophy August 2018 Agro-Commodity Global Value Chains and Upgrading: The Case of Malaysian Palm Oil Yee Siong Tong Summary This dissertation consists of three closely related essays on upgrading in agro-commodity value chains, which is an important issue for many developing countries that produce and export commodities in mostly unprocessed form. The essays are based on fieldwork in Malaysia and focus on its palm oil, which is the world’s largest oils and fats product by production and export volumes. The first essay examines the suitability of vertical specialisation for participation and upgrading in agro-commodity value chains based on the case of Malaysian palm oil. It uses data from interviews, site visits, and industry and economic statistics to analyse upgrading at the sector and firm levels. The essay suggests that upgrading is prone to sectoral linkage development and vertical integration at local lead firms. The development is driven by production characteristics, sectoral dynamics, eco-historical settings that are unique to agro-commodity value chains, as well as firm motives seeking resources, markets, efficiency gains, and strategic assets. The second essay studies Malaysia’s industrial policy for its palm oil sector through three distinct stages of development. The findings show that resource-based industrialisation (RBI) requires selective state intervention targeting macroeconomic conditions, infrastructure, business climate, and human capital. The Malaysian experience also highlights the importance of local firms in driving RBI investments, contrary to the emphasis in the literature which either overplays the importance of foreign linkages or dismisses nationality of firms as a non-factor for industrialisation. -

RM New Entries 2016 Mar.Pdf

International Plant Nutrition Institute Regional Office • Southeast Asia Date: March 31, 2016 Page: 1 of 88 New Entries to IPNI Library as References Roberts T. L. 2008. Improving Nutrient Use Efficiency. Turkish Journal of Agriculture and Forestry, 32:177-182. Reference ID: 21904 Notes: #21904e Abstract: Public interest and awareness of the need for improving nutrient use efficiency is great, but nutrient use efficiency is easily misunderstood. Four indices of nutrient use efficiency are reviewed and an example of different applications of the terminology show that the same data set might be used to calculate a fertilizer N efficiency of 21% or 100%. Fertilizer N recovery efficiencies from researcher managed experiments for major grain crops range from 46% to 65%, compared to on-farm N recovery efficiencies of 20% to 40%. Fertilizer use efficiency can be optimized by fertilizer best management practices that apply nutrients at the right rate, time, and place. The highest nutrient use efficiency always occurs at the lower parts of the yield response curve, where fertilizer inputs are lowest, but effectiveness of fertilizers in increasing crop yields and optimizing farmer profitability should not be sacrificed for the sake of efficiency alone. There must be a balance between optimal nutrient use efficiency and optimal crop productivity. Souza L. F. D.and D. H. Reinhardt. 2015. Pineapple. Pages 179-201 IPO. Reference ID: 21905 Notes: #21905e Abstract: Pineapple is one of the tropical fruits in greatest demand on the international market, with world production in 2004 of 16.1 million mt. Of this total, Asia produces 51% (8.2 million mt), with Thailand (12%) and the Philippines (11%) the two most productive countries. -

Bumitama Agri Ltd. MEDIUM RISK

INITIATING COVERAGE 15 October 2014 Bumitama Agri Ltd. MEDIUM RISK Oil palm plantation ISIN: SG2E67980267| SGX: P8Z | Bloomberg: BAL:SP BUMITAMA AGRI LTD. MEDIUM RISK Summary Warding off Sustainability Risk This Chain Reaction Research (CRR) report analyzes the financial risk profile of Bumitama Agri Ltd. (BAL:SP), a rapidly growing palm oil company. We looked at sustainability risks associated with the group’s 204,000 hectare (ha) land bank in Kalimantan, Indonesia – an area that the company identifies as available for plantation development. Detailed analysis of 16 of the group’s 18 plantation subsidiaries shows that Bumitama has been involved in significant deforestation, peatland development and legal irregularities since the group entered the plantation business in 1998. Continuation of such practices places the group at serious risk of losing its two major customers. Wilmar International and Golden Agri-Resources (GAR) together purchase approximately 90 percent of Bumitama’s palm oil supply. As of early 2014, both companies have adopted stringent sourcing policies that disqualify third-party suppliers who engage in deforestation, peat development and social exploitation. In the months since, Bumitama has taken several steps that may mitigate some of the worst risks. In this report, CRR reviews how Bumitama accumulated its sustainability risk profile over the years, and assesses the potential financial consequences should the group fail to duly address its sustainability risk exposure. An earlier version of this report was sent to Bumitama Agri for review, and this final report integrates information from its response. Contested Land Bank: 41% At the core of our Sustainability Risk Assessment (SRA) is an analysis of how much of a company’s land bank may be “contested land” – i.e. -

PRINCIPLES and CRITERIA for Sustainable Palm Oil Production 2018

RSPO Roundtable on Sustainable Palm Oil PRINCIPLES AND CRITERIA For Sustainable Palm Oil Production 2018 The Indonesia National Interpretation 1 Draft 1 – National Interpretation RSPO Principles & Criteria 2018 Preface Sustainable palm oil production comprises legal, economically viable, environmentally appropriate and socially beneficial management and operations. This is delivered through the application of the following set of Principles and Criteria ("P&C") herein and the accompanying Indicators and Guidance. The first set of RSPO P&C, Indicators and Guidance (RSPO P&C 2007) have been applied since November 2007. These had been subject to trial implementation from November 2005 to November 2007 and, in a number of countries, to a subsequent process of National Interpretation process (NI). After five years of application by RSPO members, RSPO P&C 2007 were reviewed in 2012-2013, leading to the RSPO P&C 2013. After a five years of application, RSPO P&C 2013 were reviewed and revised in 2017-2018 by the RSPO Principles and Criteria Review Task Force. The objective of each review and revision is to improve the relevance and effectiveness of the Principles and Criteria for RSPO members, and in achieving the shared vision and mission to make sustainable palm oil the norm. More specifically, this most recent revision sought to align the Principles and Criteria with the RSPO Theory of Change (ToC) and increase accessibility by making so these Principles and Criteria are more relevant and practical. The review process went beyond International Social and Environmental Accreditation and Labelling (ISEAL) best practices, including two public consultation periods of 60 days each, and with 17 physical consultation workshops in 10 countries around the world, as well as 6 physical Task Force meetings. -

Buku Prospektus Astra Agro Lestari (Indonesia).Pdf

PENAWARAN UMUM TERBATAS (PUT I) PT ASTRA AGRO LESTARI TBK KEPADA PARA PEMEGANG SAHAM PERSEROANDALAM RANGKA PENERBITAN HAK MEMESAN EFEK TERLEBIH DAHULU (HMETD) TAHUN 2016 HAK MEMESAN EFEK TERLEBIH DAHULU (HMETD) TAHUN PENERBITAN PEMEGANG SAHAM PERSEROANDALAM RANGKA PARA TBK KEPADA AGRO LESTARI ASTRA (PUT I) PT UMUM TERBATAS PENAWARAN JADWAL Tanggal Rapat Umum Pemegang Saham Luar Biasa (RUPSLB) : 11 April 2016 'LVWULEXVL6HUWL¿NDW%XNWL+0(7' : 10 Juni 2016 7DQJJDO3HUQ\DWDDQ3HQGDIWDUDQ+0(7'PHQMDGL(IHNWLI : 0HL 7DQJJDO3HQFDWDWDQ6DKDPGL%XUVD(IHN,QGRQHVLD : 13 Juni 2016 7DQJJDO7HUDNKLU3HQFDWDWDQ Recording Date XQWXNPHPSHUROHK+0(7' : 9 Juni 2016 3HULRGH3HUGDJDQJDQ+0(7' : 13 - 17 Juni 2016 7DQJJDO7HUDNKLU3HUGDJDQJDQ6DKDP'HQJDQ+0(7' &XP5LJKW 3HULRGH3HQGDIWDUDQ3HPED\DUDQGDQ3HODNVDQDDQ+0(7' : 13 - 17 Juni 2016 3DVDU5HJXOHUGDQ3DVDU1HJRVLDVL : 6 Juni 2016 3HULRGH3HQ\HUDKDQ6DKDP+DVLO3HODNVDQDDQ+0(7' : 15 - 21 Juni 2016 Pasar Tunai : 9 Juni 2016 7DQJJDO7HUDNKLU3HPED\DUDQ3HPHVDQDQ6DKDP7DPEDKDQ : 21 Juni 2016 7DQJJDO0XODL3HUGDJDQJDQ6DKDP7DQSD+0(7' ([5LJKW 7DQJJDO3HQMDWDKDQ : 22 Juni 2016 3DVDU5HJXOHUGDQ3DVDU1HJRVLDVL : 7 Juni 2016 7DQJJDO3HPEHOL6LDJD0HODNVDQDNDQ.HZDMLEDQQ\D : 23 Juni 2016 Pasar Tunai : 10 Juni 2016 Tanggal Pengembalian Uang Pemesanan : 24 Juni 2016 OTORITAS JASA KEUANGAN (“OJK”) TIDAK MEMBERIKAN PERNYATAAN MENYETUJUI ATAU TIDAK MENYETUJUI EFEK INI, TIDAK JUGA MENYATAKAN KEBENARAN ATAU KECUKUPAN ISI PROSPEKTUS INI. SETIAP PERNYATAAN YANG BERTENTANGAN DENGAN HAL-HAL TERSEBUT ADALAH PERBUATAN MELANGGAR HUKUM. PROSPEKTUS INI PENTING DAN PERLU -

No Less an Authority Than the Highest Court in the Land Has Now Confirmed That Palm Oil Producer Bumitama Agri Ltd. Violated

These trees were felled illegally to make room for oil palm plantations. “No less an authority than the highest court in the land has now confirmed that palm oil producer Bumitama Agri Ltd. violated Indonesian law when it let its subsidiary PT. HPA clear 7,000 hectares of rainforest”, writes Nordin, an activist with our Indonesian partner organization Save our Borneo. The Indonesian Supreme Court ruled in a two-year dispute between the country’s Forestry Ministry and Bumitama Agri Ltd. The court confirmed that the company did not have a valid permit to clear-cut Central Kalimantan’s unique primary forests for palm oil plantations. “We won!” Nordin writes. “This verdict is a great success for our campaign work.” Nordin became aware of the illegal deforestation in March 2012 and filed a complaint, whereupon the company threatened him and had him repeatedly interrogated by the police for making what it claimed were “false accusations in public”. Rainforest Rescue supported Nordin’s work by collecting 45,000 signatures in an online petition to the plantation operators and their corporate customers in the West. Bumitama Agri Ltd. is a major player in the palm oil business. According to its own figures, the Indonesian company owns or uses 204,052 hectares of land in Borneo and Sumatra, of which more than two thirds are now occupied by oil palm monocultures. Bumitama Agri Ltd. is listed on the Singapore Stock Exchange, and the influential IOI Group of Malaysia holds 33 percent of its shares. IOI supplies multinational corporations such as Nestlé and Unilever and the biofuel producer Neste Oil – thus putting conflict palm oil on our dinner tables and in our fuel tanks. -

The Great Palm Oil Scandal Labour Abuses Behind Big Brand Names

THE GREAT PALM OIL SCANDAL LABOUR ABUSES BEHIND BIG BRAND NAMES Under strict embargo until 00:01 GMT 30 November 2016 Amnesty International is a global movement of more than 7 million people who campaign for a world where human rights are enjoyed by all. Our vision is for every person to enjoy all the rights enshrined in the Universal Declaration of Human Rights and other international human rights standards. We are independent of any government, political ideology, economic interest or religion and are funded mainly by our membership and public donations. CONTENTS 1. EXECUTIVE SUMMARY 4 2. METHODOLOGY 13 3. BACKGROUND 17 4. QUOTAS FOR EXPLOITATION 22 5. CASUAL WORKERS, DISCRIMINATION, AND ABUSES OF THE RIGHT TO HEALTH 51 6. WILMAR AND ITS SUPPLIERS: ABUSING HUMAN RIGHTS 70 7. ENABLING ABUSES: GAPS IN LAWS AND ENFORCEMENT IN INDONESIA 81 8. TRACING THE MOVEMENT OF PALM OIL FROM THE PLANTATIONS TO THE BUYERS 88 9. WILMAR’S BUYERS AND THEIR FAILURE TO RESPECT HUMAN RIGHTS 93 10. CONCLUSION AND RECOMMENDATIONS 105 THE GREAT PALM OIL SCANDAL LABOUR ABUSES BEHIND BIG BRAND NAMES Under strict embargo until 00:01 GMT 30 November 2016 1. EXECUTIVE SUMMARY Palm oil and palm-based ingredients are found in approximately 50% of common consumer products. Besides its use as a cooking oil, palm oil is found in many food products such as packaged bread, breakfast cereals, margarine, chocolate, ice cream, biscuits, and snack food. It is also used in household detergents, shampoos, creams, soap, lipsticks and in biofuels for cars and power plants. Global production of palm oil has doubled over the last decade and experts estimated that it will have doubled again by 2020. -

Sustainable Palm Oil

ROUNDTABLE ON SUSTAINABLE PALM OIL IMPACT REPORT 2014 CONTENTS Welcome by RSPO Secretary General 02 Impact Report Highlights 04 Facts about palm oil 06 The Roundtable on Sustainable Palm Oil 10 Certified Sustainable Palm Oil 17 Measuring our impact 24 Partnering with leading experts 26 People 28 Better livelihoods 28 Protecting the rights of local communities 34 Planet 40 Protecting biodiversity 40 Reducing greenhouse gas (GHG) emissions 48 Soil and water 54 Profit 58 Improving yields for smallholders 58 Driving market transformation 68 References 74 Base data and notes 76 Glossary 79 01 RSPO IMPACT REPORT RSPO IMPACT Photo credit: New Britain Palm Oil Ltd Edited by Helikonia Design by Meta Fusion Pte Ltd WELCOME BY RSPO is a voluntary standard and in itself conjures the impression RSPO SECRETARY GENERAL that companies willingly commit to making the shift to responsible practices, steered by their own conscience and integrated into their business operations and mission. IMPACT REPORT PRESENTED BY DARREL WEBBER RSPO SECRETARY GENERAL When the RSPO was first established a decade ago – all it Herein –the significance in presenting, for the first time, We are pleased that despite the challenges we continue had to its name was a small group of enthusiastic pioneers the in-depth 2014 Impacts Report outlining the social; to be confronted with in the transformation to making envisioning to eradicate some of the world’s most intense environmental and economic progress of the RSPO to date sustainable palm oil the norm – the commitment by both dilemmas in the palm oil sector. These issues range from as a result of the commitment from all the players in the the private sector and civil society including governments deforestation, extinction of wildlife, unethical practices, sector, not precluding the collaboration received from has not abated - in fact as we witness in this report, it has opaque business operations and land conflicts, to name a few.