Divisibility, Technology, and the Competitive Potential of Regional Airlines

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fairchild Aviation Corporation, Factory No. 1) MD-137 851 Pennsylvania Avenue Hagerstown Washington County Maryland

KREIDER-REISNER AIRCRAFT COMPANY, FACTORY NO. 1 HAER MD-137 (Fairchild Aviation Corporation, Factory No. 1) MD-137 851 Pennsylvania Avenue Hagerstown Washington County Maryland PHOTOGRAPHS HISTORIC AMERICAN ENGINEERING RECORD National Park Service U.S. Department of the Interior 1849 C Street NW Washington, DC 20240-0001 ADDENDUM TO: HAER MD-137 KREIDER-REISNER AIRCRAFT COMPANY, FACTORY NO. 1 MD-137 (Fairchild Aviation Corporation, Factory No. 1) 851 Pennsylvania Avenue Hagerstown Washington County Maryland WRITTEN HISTORICAL AND DESCRIPTIVE DATA HISTORIC AMERICAN ENGINEERING RECORD National Park Service U.S. Department of the Interior 1849 C Street NW Washington, DC 20240-0001 HISTORIC AMERICAN ENGINEERING RECORD KREIDER-REISNER AIRCRAFT COMPANY, FACTORY NO. 1 (FAIRCHILD AVIATION CORPORATION, FACTORY NO. 1) HAER No. MD-137 LOCATION: 881 Pennsylvania Avenue (Originally 1 Park Lane), Hagerstown, Washington County, Maryland Fairchild Factory No. 1 is located at latitude: 39.654706, longitude: - 77.719042. The coordinate represents the main entrance of the factory, on the north wall at Park Lane. This coordinate was obtained on 22 August, 2007 by plotting its location on the 1:24000 Hagerstown, MD USGS Topographic Quadrangle Map. The accuracy of the coordinate is +/- 12 meters. The coordinate’s datum is North American Datum 1927. The Fairchild Factory No. 1 location has no restriction on its release to the public. DATES OF CONSTRUCTION: 1929, 1931, 1935, 1941, 1965, 1987 BUILDER: Kreider-Reisner Aircraft Company, a subsidiary of Fairchild Aviation Corporation PRESENT OWNER: Vincent Groh PRESENT USE: Light industry, storage SIGNIFICANCE: Kreider-Reisner Factory No. 1 (also known as Fairchild No. 1) was built as a result of a partnership between upstart airplane builders Ammon H. -

Aircraft Tire Data

Aircraft tire Engineering Data Introduction Michelin manufactures a wide variety of sizes and types of tires to the exacting standards of the aircraft industry. The information included in this Data Book has been put together as an engineering and technical reference to support the users of Michelin tires. The data is, to the best of our knowledge, accurate and complete at the time of publication. To be as useful a reference tool as possible, we have chosen to include data on as many industry tire sizes as possible. Particular sizes may not be currently available from Michelin. It is advised that all critical data be verified with your Michelin representative prior to making final tire selections. The data contained herein should be used in conjunction with the various standards ; T&RA1, ETRTO2, MIL-PRF- 50413, AIR 8505 - A4 or with the airframer specifications or military design drawings. For those instances where a contradiction exists between T&RA and ETRTO, the T&RA standard has been referenced. In some cases, a tire is used for both civil and military applications. In most cases they follow the same standard. Where they do not, data for both tires are listed and identified. The aircraft application information provided in the tables is based on the most current information supplied by airframe manufacturers and/or contained in published documents. It is intended for use as general reference only. Your requirements may vary depending on the actual configuration of your aircraft. Accordingly, inquiries regarding specific models of aircraft should be directed to the applicable airframe manufacturer. -

History of Aircraft Designation Systems

UNITED STATES NAVAL AVIATION 1910–1995 451 APPENDIX 5 Aircraft Designations and Popular Names Background on the Evolution of Aircraft Designations Aircraft model designation history is very complex. by a number to indicate the individual plane of that In order to fully understand the designations, it is type-manufacturer. Under this system: important to know the factors that played a role in developing the different missions that aircraft have been “A” was used for Curtiss hydroaeroplanes “B” for Wright hydroaeroplanes called upon to perform. Technological changes affect- “C” for Curtiss flying boats ing aircraft capabilities have resulted in corresponding “D” for Burgess flying boats changes in the operational capabilities and techniques “E” for Curtiss amphibian flying boats employed by the aircraft. Prior to World War I, the Navy tried various schemes for designating aircraft. This system had been established in 1911 by Captain In the early period of naval aviation a system was Washington I. Chambers, Director of Naval Aviation. developed to designate an aircraft’s mission. Different The following is a list of the types of aircraft and their aircraft class designations evolved for the various types designations in existence from 1911–1914: of missions performed by naval aircraft. This became known as the Aircraft Class Designation System. Aircraft Designation System 1911–1914 Numerous changes have been made to this system since the inception of naval aviation in 1911. A-1 Curtiss hydroaeroplane (originally an amphib- While reading this section various references will be ian, and the Navy’s first airplane) made to the Aircraft Class Designation System, A-2 Curtiss landplane (rebuilt as a hydroaeroplane) Designation of Aircraft, Model Designation of Naval A-3 Curtiss hydroaeroplane Aircraft, Aircraft Designation System, and Model A-4 Curtiss hydroaeroplane Designation of Military Aircraft. -

Aircraft Manufacturers Partie 4 — Constructeurs D’Aéronefs Parte 4 — Fabricantes De Aeronaves Часть 4

4-1 PART 4 — AIRCRAFT MANUFACTURERS PARTIE 4 — CONSTRUCTEURS D’AÉRONEFS PARTE 4 — FABRICANTES DE AERONAVES ЧАСТЬ 4. ИЗГОТОВИТЕЛИ ВОЗДУШНЫХ СУДОВ COMMON NAME COMMON NAME NOM COURANT NOM COURANT NOMBRE COMERCIAL NOMBRE COMERCIAL CORRIENTE MANUFACTURER FULL NAME CORRIENTE MANUFACTURER FULL NAME ШИРОКО NOM COMPLET DU CONSTRUCTEUR ШИРОКО NOM COMPLET DU CONSTRUCTEUR РАСПРОСТРАНЕННОЕ FABRICANTE NOMBRE COMPLETO РАСПРОСТРАНЕННОЕ FABRICANTE NOMBRE COMPLETO НАИМЕНОВАНИЕ ПОЛНОЕ НАИМЕНОВАНИЕ ИЗГОТОВИТЕЛЯ НАИМЕНОВАНИЕ ПОЛНОЕ НАИМЕНОВАНИЕ ИЗГОТОВИТЕЛЯ A (any manufacturer) (USED FOR GENERIC AIRCRAFT TYPES) AERO ELI AERO ELI SERVIZI (ITALY) AERO GARE AERO GARE (UNITED STATES) 3 AERO ITBA INSTITUTO TECNOLÓGICO DE BUENOS AIRES / PROYECTO PETREL SA (ARGENTINA) 328 SUPPORT SERVICES 328 SUPPORT SERVICES GMBH (GERMANY) AERO JAEN AERONAUTICA DE JAEN (SPAIN) AERO KUHLMANN AERO KUHLMANN (FRANCE) 3XTRIM ZAKLADY LOTNICZE 3XTRIM SP Z OO (POLAND) AERO MERCANTIL AERO MERCANTIL SA (COLOMBIA) A AERO MIRAGE AERO MIRAGE INC (UNITED STATES) AERO MOD AERO MOD GENERAL (UNITED STATES) A-41 CONG TY SU'A CHU'A MAY BAY A-41 (VIETNAM) AERO SERVICES AÉRO SERVICES GUÉPARD (FRANCE) AAC AAC AMPHIBIAM AIRPLANES OF CANADA (CANADA) AERO SPACELINES AERO SPACELINES INC (UNITED STATES) AAK AUSTRALIAN AIRCRAFT KITS PTY LTD (AUSTRALIA) AEROALCOOL AEROÁLCOOL TECNOLOGIA LTDA (BRAZIL) AAMSA AERONAUTICA AGRICOLA MEXICANA SA (MEXICO) AEROANDINA AEROANDINA SA (COLOMBIA) AASI ADVANCED AERODYNAMICS AND STRUCTURES INC AERO-ASTRA AVIATSIONNYI NAUCHNO-TEKHNICHESKIY TSENTR (UNITED STATES) AERO-ASTRA -

Type Rating of an Aircraft, Compare the Aircraft Model from Block 2 of the Airworthiness Certificate to the Civil Model Designation Column Below

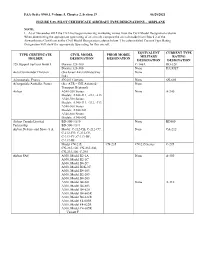

FAA Order 8900.1, Volume 5, Chapter 2, Section 19 06/28/2021 FIGURE 5-88, PILOT CERTIFICATE AIRCRAFT TYPE DESIGNATIONS – AIRPLANE NOTE: 1. As of November 2015 the FAA has begun removing marketing names from the Civil Model Designation column. When determining the appropriate type rating of an aircraft, compare the aircraft model from Block 2 of the Airworthiness Certificate to the Civil Model Designation column below. The column titled Current Type Rating Designation will show the appropriate type rating for this aircraft. EQUIVALENT CURRENT TYPE TYPE CERTIFICATE CIVIL MODEL PRIOR MODEL MILITARY RATING HOLDER DESIGNATION DESIGNATION DESIGNATION DESIGNATION 328 Support Services GmbH Dornier 328-100 C-146A DO-328 Dornier 328-300 None D328JET Aero Commander Division (See Israel Aircraft Industries None Ltd.) Aérospatiale, France SN 601 Corvette None SN-601 Aérospatiale/Aeritalia, France (See ATR – GIE Avions de None Transport Régional) Airbus A340-200 Series: None A-340 Models: A340-211, -212, -213 A340-300 Series: Models: A340-311, -312, -313 A340-500 Series: Models: A340-541 A340-600 Series: Models: A340-642 Airbus Canada Limited BD-500-1A10 None BD500 Partnership BD-500-1A11 Airbus Defense and Space S.A. Model: C-212-CB, C-212-CC, None CA-212 C-212-CD, C-212-CE, C-212-CF, C-212-DF, C-212-DE Model CN-235, CN-235 CN-235 Series C-295 CN-235-100, CN-235-200, CN-235-300, C-295 Airbus SAS A300, Model B2-1A None A-300 A300, Model B2-1C A300, Model B4-2C A300, Model B2K-3C A300, Model B4-103 A300, Model B2-203 A300, Model B4-203 A300, Model B4-601 -

United States Army Air Forces Primary Trainers, 1939-1945

United States Army Air Forces Primary Trainers, 1939-1945 by Stephen G. Craft A Stearman PT-17 fl ies over Carlstrom Field in Arcadia, Fla., where thousands of United States Army Air Corps cadets received primary fl ight training. (Photo by Charles C. Ebbets, courtesy of Ebbets Photo-Graphics, LLC) WII aviation enthusiasts and Hollywood tend over 60 civilian schools were responsible for providing primary to remember speci c ghters, such as the P-51 training to all army ying cadets. WMustang or the P-47 Thunderbolt, and bombers, When Arnold formulated his plan, the civilian contractors such as the B-17 Flying Fortress or the B-29 Superfortress. had xed-base operations or ight schools with air elds and Often forgotten or misunderstood are the much smaller and facilities, years of commercial and military aviation experience, slower monoplane and biplane piston-engine aircraft that were and the ight instructors and mechanics in place, but they used to train thousands of United States Army Air Corps and Air lacked the aircraft necessary to carry out ight training. In Forces pilots. These aircraft, built mostly by such companies as January 1939, the original eight contractors possessed a total of Stearman, Fairchild and Ryan, were used in what some deemed 24 planes. Even then, the USAAC could only make 86 planes the most important stage of a cadet’s training career: primary. available with another 81 projected to arrive later in the year. Each possessed certain strengths and weaknesses. Some of This was far short of the 400 primary trainers proposed for the these aircraft can still be seen ying out of small airports in 4,500 Pilot Plan. -

Dornier 328 Maintenance Manual

Dornier 328 Maintenance Manual If searched for the ebook Dornier 328 maintenance manual in pdf form, then you've come to the loyal website. We present the utter release of this ebook in PDF, DjVu, ePub, doc, txt formats. You can read Dornier 328 maintenance manual online or download. Too, on our site you can reading instructions and another art eBooks online, or load their as well. We wish to draw on note what our website not store the eBook itself, but we provide reference to the site whereat you may downloading or read online. If have must to load Dornier 328 maintenance manual pdf, in that case you come on to faithful website. We own Dornier 328 maintenance manual PDF, doc, txt, DjVu, ePub formats. We will be pleased if you get back again. dornier 228 manual normal procedures - Dornier 228 Manual Normal Procedures Dornier found that Flight Manual Dornier 328 procedures dornier 328-300, g-cjab 09-09.pdf - cabinet - SERIOUS INCIDENT Aircraft Type and Registration: Dornier 328-300, G-CJAB Approved Maintenance Manual requirements for long- dornier 328 aircraft maintenance manual - Dornier 328 Aircraft Maintenance Manual aircraft maintenance | 328.eu Dornier 328; service matrix; aircraft for sale; SNCORP; we offer comprehensive services on fsims document viewer - FAIRCHILD/DORNIER DO-328-100 Turboprop AND DO-328-300 Turbojet -- Date 06/15/1999 free dornier 328 jet flight manual download - - Free download dornier 328 jet flight manual Files at Software Informer - PowerCheck provides home electrical safety inspections for owners of older homes -

Aircraft Designations and Popular Names

Chapter 1 Aircraft Designations and Popular Names Background on the Evolution of Aircraft Designations Aircraft model designation history is very complex. To fully understand the designations, it is important to know the factors that played a role in developing the different missions that aircraft have been called upon to perform. Technological changes affecting aircraft capabilities have resulted in corresponding changes in the operational capabilities and techniques employed by the aircraft. Prior to WWI, the Navy tried various schemes for designating aircraft. In the early period of naval aviation a system was developed to designate an aircraft’s mission. Different aircraft class designations evolved for the various types of missions performed by naval aircraft. This became known as the Aircraft Class Designation System. Numerous changes have been made to this system since the inception of naval aviation in 1911. While reading this section, various references will be made to the Aircraft Class Designation System, Designation of Aircraft, Model Designation of Naval Aircraft, Aircraft Designation System, and Model Designation of Military Aircraft. All of these references refer to the same system involved in designating aircraft classes. This system is then used to develop the specific designations assigned to each type of aircraft operated by the Navy. The F3F-4, TBF-1, AD-3, PBY-5A, A-4, A-6E, and F/A-18C are all examples of specific types of naval aircraft designations, which were developed from the Aircraft Class Designation System. Aircraft Class Designation System Early Period of Naval Aviation up to 1920 The uncertainties during the early period of naval aviation were reflected by the problems encountered in settling on a functional system for designating naval aircraft. -

8900.1 05/31/2012 Figure 5-88, Pilot Certificate Aircraft

8900.1 05/31/2012 FIGURE 5-88, PILOT CERTIFICATE AIRCRAFT TYPE DESIGNATIONS - AIRPLANE MANUFACTURER MODEL PRIOR CURRENT DESIGNATION DESIGNATION DESIGNATION Aero Commander Division 1121 Jet Commander AC-1121 IA-JET (Also See North American Rockwell Commodore Jet 1123 CJ-1123 Corporation, USA) Aérospatiale, France SN 601 Corvette SN-601 Aérospatiale/Aeritalia, France ATR-42, ATR-72 ATR-42, ATR-72 Airbus (formerly known as Groupement A-300B Airbus A-300 d’Inerte Economique Airbus Industires, France) A-300-600R, A-310 Airbus A-310 A-319, A-320, A-321 Airbus A-320 A-330-200/300 Series A-330 A-340 200/300 Series Airbus A-340 A-380-800 A-380 Armstrong Whitworth Aircraft Co., Ltd., Argosy AW 650 Armstrong Whitworth AW-650 UK AW-650 Avions Dassault, General Aéronautique Falcon 7X DA-7X Marcel, Dassault, France Mystère 10 Falcon DA-10 Mystère 20 Falcon, Fan Jet GAMD/SUD-20 DA-20 Falcon 50-A, DA 900, DA-50 DA 900C, DA 900EX Fan Jet Model 200 DA-200 Falcon DA-2000, DA-2000 Dassault 2000EX DA-900DX, DA-EASY DA-900EX EASY DA-900LX DA-2000EX-EASY DA-2EASY Beech Aircraft Corporation, USA BE-200T/200TC, RC/FWC BE-200 BE-300, BE-B300, BE-300FF BE-300F BE-300 BE-300LW, BE-350, RC-12K, RC-12N, RC-12P, RC-12Q Diamond I, MU-300, MU-300 MU-300, BE-400 MU-300-10, BE-400, and 400T (USAF T-1A Jayhawk) BE-400-A BE-1900, BE-1900C, BE-1900 BE-1900D, C-12J (Military) BE-2000 Starship BE-2000 (SIC Required) BE-2000S Starship (Single Pilot) BE-2000S Boeing Co., USA B-17 Boeing B-17, B-B17 B-17 247-D Boeing 247 B-247 S-307, SA-307 Boeing 307 B-307 314 Boeing 314 B-314 -

AAHS Fightline

AAHS FLIGHTLINE No. 174, First Quarter 2011 American Aviation Historical Society www.aahs-online.org Fairchild FC-2-W2, N13934, s/n 531, owned by Yellowstone Aviation out of Jackson, Wyo. (All photos by Charles E. Stewart) Antique Aircraft Association 2010 National Fly-in The theme of Antique Aircraft of the Kreider-Reisner company. And these were just the marquee Association (AAA) annual National Fly- Fairchild produced a varied line of aircraft. As usual, this fl y-in is the place to in held September 1-6, 2010, was “Iowa’s civilian and military aircraft from 1926 go to get up close and personal with many Centenary of Flight.” To complement this up until 1987. With excellent weather of the remaining antique aircraft still theme, Fairchild aircraft were selected as during the period, AAA was able to operating in the United States. Held every the marquee aircraft. attract a wide variety of Fairchild models year in early September at Blakesburg, Fairchild was founded in 1920 to to the fl y-in. Among those attending Iowa, this members-only event is well support an aerial photography business types represented were an FC-2-W2, a worth the annual membership. Around and expanded in 1929 with the absorption Model 71, and variety of F-22s, F-24s 175 aircraft attended this year’s fl y- and PT-19s. in. Waco, Luscombe and Stearman Highlights of What’s Inside In addition, the AAA hosted the were well represented with other types 2003 National Air Tour Reunion of the including Piper, Command-Aire, pilots and aircraft that participated in the Howard, Beechcraft, Hatz, Aeronca, - Antique Aircraft Association re-enactment of the Ford Air Tours of the Cessna and Curtiss being in attendance 2010 National Fly-in 1920s and early 1930s. -

Pegasus Flyer

Pegasus Flyer Preserving Hagerstown’s Aviation Heritage Issue 3 DOME HANGAR SPECIAL EDITION! November 2020 Welcome to the Hagerstown Aviation Museum's third issue of tory of Hagerstown's aviation industry. It is with your contin- the Pegasus Flyer. This newsletter is published periodically to ued support that the museum will be able to renovate it’s new keep the museum's members, donors, volunteers and friends home in the historic 1943 Fairchild Aircraft Flight Test Han- informed about museum acquisitions, preservation projects, gar. You can support these efforts by making a dona- events and interesting museum activities. tion by mail or online. The museum is extremely grateful to every person, organiza- tion and corporation who over the years has provided the Thank you! support necessary for the museum to continue it’s mission of John Seburn, President, preserving and presenting to the public the century long his- Hagerstown Aviation Museum Hagerstown Aviation Museum’s First Home! - 25 Years in the Making! Concept illustration of a museum event in the Dome Hangar, By Nick Rotondo Museum aircraft moved into Dome Hangar. October, 2020 The Hagerstown Aviation Museum is dedicated to preserving museum facility to showcase the collection, the museum has and presenting the over 100 year aviation history of the held outdoor events at the Hagerstown Regional Airport Hagerstown, Maryland region. Over the past 25 years the drawing thousands of visitors each year. During these out- museum has grown from a concept to a collection of 23 his- door events, rides in the museum’s Fairchild PT-19 aircraft toric aircraft and is the world’s largest collection of historic were offered providing a memorable living history flight ex- aircraft built in Hagerstown. -

![Dornier 328 Maintenance Manual.PDF [Online Books] Dornier 328 Maintenance Manual](https://docslib.b-cdn.net/cover/5431/dornier-328-maintenance-manual-pdf-online-books-dornier-328-maintenance-manual-3065431.webp)

Dornier 328 Maintenance Manual.PDF [Online Books] Dornier 328 Maintenance Manual

[Online Books] Free Download Dornier 328 maintenance manual.PDF [Online Books] Dornier 328 Maintenance Manual If you are searched for a ebook Dornier 328 maintenance manual in pdf format, then you have come on to the loyal site. We furnish the complete release of this ebook in txt, doc, ePub, DjVu, PDF formats. You can reading Dornier 328 maintenance manual online or load. As well as, on our site you may read the manuals and diverse artistic books online, either download them as well. We want draw on your regard what our site not store the book itself, but we grant reference to website where you may downloading either read online. So that if need to load pdf Dornier 328 maintenance manual , then you have come on to loyal website. We own Dornier 328 maintenance manual doc, PDF, txt, DjVu, ePub forms. We will be happy if you go back more. We have made sure that you find the PDF Ebooks without unnecessary research. And, having access to our ebooks, you can read Dornier 328 maintenance manual online or save it on your computer. To find a Dornier 328 maintenance manual, you only need to visit our website, which hosts a complete collection of ebooks. Dornier 328 aircraft maintenance manual Dornier 328 Aircraft Maintenance Manual aircraft maintenance | 328.eu Dornier 328; service matrix; aircraft for sale; SNCORP; we offer comprehensive services on Dornier 328-300, g-cjab 09-09.pdf - cabinet SERIOUS INCIDENT Aircraft Type and Registration: Dornier 328-300, G-CJAB Approved Maintenance Manual requirements for long- Dornier 228 engine manual dornier