Bureau of Customs and Border Protection CBP Decisions

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Read Liner Notes

Cover Photo: Paul Winter Consort, 1975 Somewhere in America (Clockwise from left: Ben Carriel, Tigger Benford, David Darling, Paul Winter, Robert Chappell) CONSORTING WITH DAVID A Tribute to David Darling Notes on the Music A Message from Paul: You might consider first listening to this musical journey before you even read the titles of the pieces, or any of these notes. I think it could be interesting to experience how the music alone might con- vey the essence of David’s artistry. It would be ideal if you could find a quiet hour, and avail yourself of your fa- vorite deep-listening mode. For me, it’s flat on the floor, in total darkness. In any case, your listening itself will be a tribute to David. For living music, With gratitude, Paul 2 1. Icarus Ralph Towner (Distant Hills Music, ASCAP) Paul Winter / alto sax Paul McCandless / oboe David Darling / cello Ralph Towner / 12-string guitar Glen Moore / bass Collin Walcott / percussion From the album Road Produced by Phil Ramone Recorded live on summer tour, 1970 This was our first recording of “Icarus” 2. Ode to a Fillmore Dressing Room David Darling (Tasker Music, ASCAP) Paul Winter / soprano sax Paul McCandless / English horn, contrabass sarrusophone David Darling / cello Herb Bushler / Fender bass Collin Walcott / sitar From the album Icarus Produced by George Martin Recorded at Seaweed Studio, Marblehead, Massachusetts, August, 1971 3 In the spring of 1971, the Consort was booked to play at the Fillmore East in New York, opening for Procol Harum. (50 years ago this April.) The dressing rooms in this old theatre were upstairs, and we were warming up our instruments there before the afternoon sound check. -

The Lawrence University New Music Ensemble, February 24, 2019 Lawrence University

Lawrence University Lux Conservatory of Music Concert Programs Conservatory of Music 2-24-2019 8:00 PM The Lawrence University New Music Ensemble, February 24, 2019 Lawrence University Follow this and additional works at: https://lux.lawrence.edu/concertprograms Part of the Music Performance Commons © Copyright is owned by the author of this document. Recommended Citation Lawrence University, "The Lawrence University New Music Ensemble, February 24, 2019" (2019). Conservatory of Music Concert Programs. Program 355. https://lux.lawrence.edu/concertprograms/355 This Concert Program is brought to you for free and open access by the Conservatory of Music at Lux. It has been accepted for inclusion in Conservatory of Music Concert Programs by an authorized administrator of Lux. For more information, please contact [email protected]. New Music Series 2018–19 The Lawrence University New Music Ensemble Michael Clayville, conductor 2 THE LAWRENCE UNIVERSITY NEW MUSIC ENSEMBLE Urban Sprawl Clint Needham (b. 1981) Sunday, February 24, 2019 Bianca Pratte, piccolo/flute Harper Hall Nora Lewis, oboe/English horn* 8 p.m. Abbey Atwater, E-flat clarinet Anthony Dare, clarinet/bass clarinet Stuart Young, bassoon Voices from the Killing Jar Kate Soper (b. 1981) Amos Egleston, trumpets I. Prelude: May Kasahara Julian Cohen, horn II. My Last Duchess: Isabel Archer Liam McDonald, bass trombone VII. The Owl and the Wren: Lady Macduff Michael Mizrahi, piano* VIII. Her Voice is Full of Money (A Deathless Song): Daisy Buchanan Alex Quade, percussion Daniel Green, drum set Sam Stone, voice/clarinet McKenzie Fetters, violin Erin Lesser, piccolo/flute/bass flute* Meghan Murphy, violin Daniel Whitworth, tenor saxophone Laura Vandenberg, viola Evangeline Werger, piano/recorder Horacio Contreras, cello* Alex Quade, percussion Mark Urness, bass* Alex Quinn, violin Ava Huebner, electronics Night of the Four Moons George Crumb (b. -

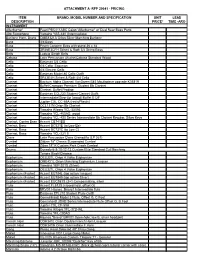

Attachment a -Rfp 20041 - Pricing

ATTACHMENT A -RFP 20041 - PRICING ITEM BRAND, MODEL NUMBER AND SPECIFICATION UNIT LEAD DESCRIPTION PRICE* TIME -ARO INSTRUMENT Afterburner' Pearl PBC411ABC Cajon 'Afterburner' w/ Dual Rear Bass Ports Alto Saxophone Yamaha YAS-480 (Intermediate) Baritone Horn, Brass OMB8321A Orion Silver Marching Baritone Bass 3/4 Bass Bass Pearn Concern Bass with stand 36 x 18 Bass SR46E3CFH Scheri & Roth 3/4 String Bass Bells Ludwig Sleigh Bells Cabasa Latin Percussion Afuche/Cabasa Standard Wood Cello Eastman 3/4 Cello Cello 4/4 Cello Eastman Cello 4/4 Electric Cello Cello Eastman Model 80 Cello Outfit Cello SR43E4H Scheri & Roth 4/4 Cello Clarinet Backum Alpha Clarinet/ VanDoren B45 Mouthpiece upgrade K35819 Clarinet Buffet Crampon Premium Student Bb Clarinet Clarinet Clarinet, Buffet Prodige Clarinet Eastman ECL230 Student Clarinet Outfit Clarinet Intermediate/Step-Up (wood) Buffet E12F Clarinet Jupiter CXL CC-65A (resin/Plastic) Clarinet OCL131N Orion Bb Clarinet Clarinet Yamaha Allegro YCL-550AL Clarinet Yamaha YCL-400AD, wood Clarinet Yamaha YCL-450 Series Intermediate Bb Clarinet Regular, Silver Keys Clarinet, Contra Base Accent CB741BB Clarinet, Base Accent BC531E (to Low Eb) Clarinet, Base Accent BC731C (to Low C) Clarinet, Base Yamaha YCL-221 II Clave Latin Percussion Clave Grenadilla (LP 261) Cymbal Zildjan 18" Classic Suspended Cymbal Cymbal Ziljan 18" K Custom Park Crash Cymbal Drums Dynasty 6-8-10-12-13 Custom Elite Standard Cut Marching Tenors Black/Chrome Euphonium OEU321L Orion 4 Valve Euphonium Euphonium OME421L Orion Marching Euphonium -

![Track Listing 1 No Wonder {RA} [3'33] Words & Music](https://docslib.b-cdn.net/cover/3450/track-listing-1-no-wonder-ra-333-words-music-2753450.webp)

Track Listing 1 No Wonder {RA} [3'33] Words & Music

Track listing 1 No Wonder {RA} [3’33] Words & Music: Elvis Costello Svante Henryson, cello; Steve Nieve, celesta, organ; Bengt Forsberg, piano, Hammond organ; Mats Schubert, piano; Johan Lindström, acoustic guitar; Magnus Persson, marimba, percussion; Michael Blair, bass drum, percussion An existing Elvis song rearranged for this album 2 Baby Plays Around {RA} [3’11] Words & Music: Cait O’Riordan & Declan Patrick Aloysius MacManus Elvis Costello, Lawery organ; Bergt Forsberg, Hammond organ; Pat White, flugelhorn; Svante Henryson, celtar; Mats Schubert, piano; Magnus Persson, vibraphone A song for which Elvis gives most of the credit to his wife Cait. 3 Go Leave {RA} [2’49] Words & Music: Anna McCarrigle Elvis Costello, baritone guitar; Kalle Moraeus, violin; Svante Henryson, cello; Mats Schubert, piano; Johan Lindström, acoustic guitar; Magnus Persson, bass drum, percussion This song is by Canadian Anna McGarrigle 4 Rope {RA} [3’54] Music: Fleshquartet / Words: Elvis Costello Fleshquartet: Jonas Lindgren, violin, electric 5-string violin · Örjan Högberg, viola, electric 5-string violin · Mattias Helldén, cello, electric cello · Sebastian Öberg, cello, electric cello; Christian Olsson, drums, percussion A song featuring music by the Fleshquartet with lyrics by Costello. 5 Don’t Talk (Put Your Head On My Shoulder) {RA} [3’11] Words & Music: Brian Wilson & Tony Asher Mats Schubert, piano; Johan Lindström, pedal steel guitar; Svante Henryson, double bass; Magnus Persson, vibraphone Taken from the much-lauded ”Pet Sounds” album of the Beach -

PERFORMER ROLE CODES Role Code

PERFORMER ROLE CODES To help calculate the share of revenues that individual performers should receive from use of a sound recording, a performer is assigned a contributor category and role code. Role codes are split into a number of types – not all of which are eligible for payment. Each type is further sorted into different instrumental, vocal or studio personnel performances, so that it is easy to identify what each performer contributed to a sound recording. Payable roles are generally ones which provide an audible contribution to the final sound recording. Non-payable roles are generally studio activities which add no audible contribution to the final sound recording. PAYABLE ROLES There are a number of payable roles. These are broken down into groups depending on the activity or instrument being played. See below all of the roles within each group. BRASS Role Code Alphorn ALP Alto Horn ALH Alto Trombone ATR Alto Valve Trombone AVT Bankia BKA Bass Trombone BTR Bass Trumpet BTP Bass Tuba BTB Brass Bass BRB Bugle BUE Cornet CTO Corno Da Caccia CDC Dung-Chen DUN Euphonium EUP FanfareTrumpet FFT Flugelhorn FLH French Horn FRH Horn HRN Horn HOR Hunting Horn (Valved) HHN Piccolo Trumpet PCT Sackbut SCK Slide Trumpet STP Sousaphone SOU Tenor Horn TNH Trombone TRM Trompeta TOA Trumpet TRU Trumpet (Eflat) TEF Tuba TUB ValveTrombone VTR ELECTRONICS Role Code Barrel Organ BRO Barrel Piano BPN Beat Box BBX DJ D_J DJ (Scratcher) SCT Emulator EMU Fairground Organ FGO Hurdy Gurdy HUR Musical Box BOX Ondioline OND Optigan OPG Polyphon PPN Programmer -

Medium of Performance Thesaurus for Music

A clarinet (soprano) albogue tubes in a frame. USE clarinet BT double reed instrument UF kechruk a-jaeng alghōzā BT xylophone USE ajaeng USE algōjā anklung (rattle) accordeon alg̲hozah USE angklung (rattle) USE accordion USE algōjā antara accordion algōjā USE panpipes UF accordeon A pair of end-blown flutes played simultaneously, anzad garmon widespread in the Indian subcontinent. USE imzad piano accordion UF alghōzā anzhad BT free reed instrument alg̲hozah USE imzad NT button-key accordion algōzā Appalachian dulcimer lõõtspill bīnõn UF American dulcimer accordion band do nally Appalachian mountain dulcimer An ensemble consisting of two or more accordions, jorhi dulcimer, American with or without percussion and other instruments. jorī dulcimer, Appalachian UF accordion orchestra ngoze dulcimer, Kentucky BT instrumental ensemble pāvā dulcimer, lap accordion orchestra pāwā dulcimer, mountain USE accordion band satāra dulcimer, plucked acoustic bass guitar BT duct flute Kentucky dulcimer UF bass guitar, acoustic algōzā mountain dulcimer folk bass guitar USE algōjā lap dulcimer BT guitar Almglocke plucked dulcimer acoustic guitar USE cowbell BT plucked string instrument USE guitar alpenhorn zither acoustic guitar, electric USE alphorn Appalachian mountain dulcimer USE electric guitar alphorn USE Appalachian dulcimer actor UF alpenhorn arame, viola da An actor in a non-singing role who is explicitly alpine horn USE viola d'arame required for the performance of a musical BT natural horn composition that is not in a traditionally dramatic arará form. alpine horn A drum constructed by the Arará people of Cuba. BT performer USE alphorn BT drum adufo alto (singer) arched-top guitar USE tambourine USE alto voice USE guitar aenas alto clarinet archicembalo An alto member of the clarinet family that is USE arcicembalo USE launeddas associated with Western art music and is normally aeolian harp pitched in E♭. -

Music: K-12 Instruments, Supplies Accs. (%)

MUSIC: K-12 INSTRUMENTS, SUPPLIES ACCS. (%) BID ID 7951 *NOTE: Specific vendors require PO Mailing and Remittance to be selected on Requisition prior to releasing* Begins: April 2, 2021 Refer to Vendors section for important reference information Ends: April 1, 2022 Description Commodity Code Vendor(s) Discount Item No.: 1 - All Classrooms: Supplies and Accessories 4600500-2014396 Mel Owen Music, Inc. 35.00% Includes music stands, metronome, tuner, etc. Old Town Violins, LLC 30.00% Doo Wop Shop 20.00% K&S Music 20.00% Washington Music Center 20.00% Music and Arts Centers* 5.00% Woodwind & Brasswind, Inc. 3.00% Item No.: 2 - Concert/Marching Band: Wind Instruments 4600500-2014397 K&S Music 45.00% Includes clarinet, saxophone, trumpet, euphonium, etc. Mel Owen Music, Inc. 35.00% Washington Music Center 20.00% Doo Wop Shop 10.00% Music and Arts Centers* 5.00% Woodwind & Brasswind, Inc. 3.00% Item No.: 3 - Concert/Marching Band: Wind Instrument 4600500-2014398 Mel Owen Music, Inc. 30.00% Supplies and Accessories Doo Wop Shop 20.00% Includes reed, ligature, mouthpiece, swab, snake, disinfectant, instrument K&S Music 20.00% stand, instrument case, etc. Washington Music Center 20.00% Music and Arts Centers* 5.00% Woodwind & Brasswind, Inc. 3.00% Item No.: 4 - Concert/Marching Band: Large Percussion 4600500-2014399 Mel Owen Music, Inc. 35.00% Instruments & Drums Washington Music Center 20.00% Includes concert bass drum, marimba, chime, snare drum, etc. Doo Wop Shop 10.00% K&S Music 10.00% Music and Arts Centers* 5.00% Woodwind & Brasswind, Inc. 3.00% Description Commodity Code Vendor(s) Discount Item No.: 5 - Concert/Marching Band: Small & Hand-Held 4600500-2014400 Mel Owen Music, Inc. -

Request for Proposal # 20041

Request for Proposal # 20041 Addendum I May 21, 2020 Questions Marimba- Adams 4.2 Octave Marimba: Could this be a 4.3 octave? (4.2 not made) Also…is this with a concert frame (Voyager) or field frame (Endurance)? Answer: 4.3 Concert Violin- 41E15H-Scherl & Roth 15” Violin outfit: Is this a violin or viola outfit? Referenced as a violin but 15” refers to a viola size. Violins are measured in ½, ¾, and 4/4. Violas are measured in inches as 14”, 15”, 15.5”, etc. Answer: Viola Violin- Acoustic/Electric Violin Serial # 17013002: What is the brand and model number requested? Answer: Glasser, Model AEX Cello- 4/4 Electric Cello: Is there a preferred brand & model? Answer: Model 110, Cecillio, Tulsa Violin brand Drums- Dynasty 6-8-10-12-13 Custom Elite Standard Cut Marching Tenors Black/Chrome: Should this be priced w/ a carrier and case? Or simply the drums only? Answer: Drums and Carrier; No case. Bass ¾ Bass – no brand or model no. listed Answer: Model K61, Tulsa Violin brand Bass – Pearl Concert Bass Drum with stand 36X18 – no model listed (there are many) for the drum and stand Answer: Model PBE3618/CBS Pearl Concert Bass Drum with direct stand mount Flute Gemeinhardt – Gemeinhardt Model 3 flute – there is no model by that number Answer: Model 3shb Flute - - Jupiter CXL CF50A – no flute by that model Answer: Jupiter CXL CF-50A Trumpet – Jupiter CXL CTR60A – no trumpet by that model Answer: Jupiter JTR700 Viola – Model 80 viola outfit – no Brand listed Answer: Eastman Violin – Model 105 Violin outfit – no brand listed Answer: Eastman Mouthpiece – Vandoren BLC Baritone Sax mouthpiece – not enough information Answer: Vandoren SM731 BL3 Optimum Series Baritone Saxophone Mouthpiece RESPECTFULLY Proposal responses must include a copy of this page, signed by the vendor, confirming receipt of same. -

Attachment A

Attachment A RFP 20022 - MUSICAL INSTRUMENTS PROPOSAL PRICING Note: Pricing is to be firm through June 30, 2021. Unit Extended Lead Delivery QTY Description Part Number/MFR. Price Price Time Loc. 1 Flute Accent FL512S (closed hold, offset G) Memorial/ Band 1 Flute (intermediate Haynes "Bravo" BRV01 Open-hole; low B, silver head joint Memorial/ Band 1 Bass Clarinet Accent BC531E (to Low Eb) Memorial/ Band 1 Bass Clarinet Accent BC731C (to Low C) Memorial/ Band 1 Trumpet - Silver-plate Accent TR781S Memorial/ Band 1 Trumpet - Silver-plate Accent TR0942SK Memorial/ Band 1 Trombone (F-attachment) Accent TB783LF Memorial/ Band 1 Euphonium (4valve) Accent EU784L (top action: lacquer) Memorial/ Band 1 Euphonium (4valve) Accent EU7849 (top action: silver) Memorial/ Band 1 Euphonium (4valve) Accent EUC981S (3+1 Compensating, silver Memorial/ Band 1 Contra-Bass Clarinet BBb Accent CB741BB Memorial/ Band 2 Tuba OBB221L Orion 3/4 Tuba Edison Preparatory 3 Euphonium OEU321L Orion 4 Valve Euphonium Edison Preparatory 2 Mellophone OMM422MS Orion Silver Marching Mellophone Edison Preparatory 3 Brass Baritone Horn OMB8321A Orion Silver Marching Baritone Edison Preparatory 3 Trumpet Orion Student Trumpet Edison Preparatory 15 Violin SR41E4H Sheri & Roth 4/4 Violin Rogers College 5 Viola ST42E152H Scheri & Roth 15.5" Viola Rogers College 8 Cello SR43E4H Scheri & Roth 4/4 Cello Rogers College 5 Bass SR46E3CFH Scheri & Roth 3/4 String Bass Rogers College 1 Saxophone JBS1000 Jupiter Baritone Saxophone East Central HS 2 Saxophone JAS710GNA Jupiter Alto Saxophone -

Hope's Dream (2009) by Mark Dresser And

SARAH WEAVER LIST OF COMPOSITIONS HOPE’S DREAM (2009) By Mark Dresser and Sarah Weaver for telematic large ensemble Dedicated to Dr. Hope P. White-Davis (b. 1952 d. 2009) , Founder and President Emeritus of the World Association of Former United Nations Internes and Fellows Premiere: November 20, 2009 at United Nations Headquarters in New York, University of California San Diego, Banff Center for the Arts (Canada), Queen's University Belfast, Dongguk University (Seoul, Korea) via Internet Performers: United Nations Headquarters in New York - Joan La Barbara, voice, Yoon Sun Choi, voice, Robert Dick, flute, Jane Ira Bloom, soprano saxophone, Marty Ehrlich, woodwinds, Oliver Lake, saxophone, Dave Taylor, trombone, Tomas Ulrich, cello, Samir Chatterjee, tabla, Sarah Weaver, conductor and composer. San Diego - Mark Dresser, contrabass, conductor, composer Banff, Canada - Lee Heuermann, soprano, Charles Nichols, electric violin, Sam Davidson, clarinet and electronics, Chris Chafe, electric cello and composer, Geoff Shoesmith, tuba and electronics, Knut Eric Jensen, piano Belfast - Pedro Rebelo, composer and piano, Franziska Schroeder, saxophone, Manuela Meier, accordion, Steve Davis, drums/percussion, Justin Yang, saxophone/electronics Seoul - Jun Kim, composer, SeungHee Lee, haegeum, Euy-shick Hong, saxophone, Woon Seung Yeo, visuals, Quartet X: Yoonbhum Cho, 1st violin, Soyeon Park, 2nd violin, Heejun Kim, viola, Saelan Oh, cello Program Note: Telematic ensemble piece co-composed and co-conducted by Mark Dresser and Sarah Weaver for the -

Composition Portfolio Thomas Mcveety

University of New Mexico UNM Digital Repository Music ETDs Electronic Theses and Dissertations 6-9-2016 Composition Portfolio Thomas McVeety Follow this and additional works at: https://digitalrepository.unm.edu/mus_etds Recommended Citation McVeety, Thomas. "Composition Portfolio." (2016). https://digitalrepository.unm.edu/mus_etds/13 This Thesis is brought to you for free and open access by the Electronic Theses and Dissertations at UNM Digital Repository. It has been accepted for inclusion in Music ETDs by an authorized administrator of UNM Digital Repository. For more information, please contact [email protected]. Thomas G. McVeety Candidate Music Department This thesis is approved, and it is acceptable in quality and form for publication: Approved by the Thesis Committee: Peter Gilbert , Chairperson Jose--Luis Hurtado Karola Obermulller i COMPOSITION PORTFOLIO by THOMAS G. MCVEETY BACHELOR OF MUSIC, CELLO PERFORMANCE UNIVERSITY OF NEW MEXICO, DECEMBER 1985 BACHELOR OF ART, MUSIC UNIVERSITY OF NEW MEXICO, MAY 2007 BACHELOR OF SCIENCE, ELECTRICAL ENGINEERING UNIVERSITY OF NEW MEXICO, MAY 2007 THESIS Submitted in Partial Fulfillment of the Requirements for the Degree of Master of Music The University of New Mexico Albuquerque, New Mexico May 2016 ii DEDICATION I dedicate this work to my wonderful parents, Raymond and Abigail McVeety. iii ACKNOWLEDGMENTS I want to thank the following individuals for their inspiration, guidance and patience: Karola Obermulller, Peter Gilbert, Jose--Luis Hurtado, Richard Hermann and David Bashwiner. I am grateful for their insight and suggestions, for thoroughly challenging my abilities, and for opening new paths of thinking and hearing. Others who brought knowledge and understanding to my studies include William Wood, Scott Wilkinson, Chris Schultis, Joanna de Keyser, and David Schepps. -

Ogoun Badagris for Percussion Ensemble

CLASSICAL SERIES FRIDAY & SATURDAY, MAY 18 & 19, AT 8 PM NASHVILLE SYMPHONY GIANCARLO GUERRERO, conductor JOHANNES MOSER, cello CLASSICAL SERIES PRESENTING PARTNER CHRISTOPHER ROUSE Ogoun Badagris for Percussion Ensemble PIOTR ILYICH TCHAIKOVSKY Variations on a Rococo Theme for Cello and Orchestra, Opus 33 Johannes Moser, cello CONCERT PARTNERS – INTERMISSION – ENRICO CHAPELA Magnetar, Concerto for Electric Cello Johannes Moser, cello AARON COPLAND Symphony for Organ and Orchestra Prelude: Andante BMW OF NASHVILLE Scherzo: Allegro molto Finale: Lento This concert will run approximately one hour MEDIA PARTNER and 50 minutes, including a 20-minute intermission. INCONCERT 31 TONIGHT’S CONCERT AT A GLANCE CHRISTOPHER ROUSE Ogoun Badagris • A major figure in contemporary American orchestral music, Rouse is a professor at the Juilliard School in New York, and his work will be the subject of a forthcoming Nashville Symphony release on Naxos. • Written in 1976 and scored exclusively for percussion, Ogoun Badagris conjures a scene from a Haitian Voodoo ritual. The title of the piece refers to a Voodoo deity, and the various percussion instruments, including cabasa and conga drums, imitate those used in the actual ritual. PYOTR ILYICH TCHAIKOVSKY Variations on a Rococo Theme for Cello and Orchestra, Op. 33 • Though viewed as the epitome of Russian Romanticism, Tchaikovsky also had a strong inclination toward Neoclassicism, as exemplified in this work. • Cello soloist Wilhelm Fitzhagen asked the composer’s permission to make adjustments to the demanding solo part — and wound up taking even greater liberties, making numerous edits and cuts to the piece, to Tchaikvosky’s chagrin. • Fitzhagen’s revisions became the standard version of the Rococo Variations until the 1950s, when a Soviet musicologist published a reconstruction of the original score.