Sparebank 1 SR-Bank Annual Report 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sustainability in Sparebank 1 SR-Bank

Sustainability in SpareBank 1 SR-Bank Sustainability in SpareBank 1 SR-Bank 1 1. SpareBank 1 SR-Bank’s approach to sustainability 1.1 SpareBank 1 SR-Bank is a responsible corporate citizen and a driving force behind the green shift ................................................................................................................................................................................................. 3 1.2 SpareBank 1 SR-Bank’s global responsibilities – organisations and international principles supported by the group ........................................................................................................................................................ 3 1.2.1 Global initiatives .................................................................................................................................................................................................. 3 1.3 Frameworks SpareBank 1 SR-Bank complies with: ............................................................................................................... 4 1.3.1 OECD Guidelines for Multinational Enterprises .......................................................................................................... 4 1.3.2 Global Reporting Initiative (GRI) ..................................................................................................................................................... 4 1.3.3 CDP reporting ...................................................................................................................................................................................................... -

Kulturminnegrunnlag

KULTURMINNEGRUNNLAG for Forvaltningsplan for Byfjellene Sør Smøråsfjellet, Stendafjellet og Fanafjellet Byantikvaren 2006 Byrådsavdeling for Byutvikling Bergen kommune Kulturminnegrunnlag for Byfjellene Sør 2006 FORORD For forvaltningsplan for Byfjellene Sør Smøråsfjellet, Stendafjellet og Fanafjellet Det foreliggende kulturminnegrunnlaget er en del av Byantikvarens arbeid med å kartfeste og sikre informasjon og kunnskap om det historiske kulturlandskapet i Bergen kommune. Kulturminnegrunnlaget er utarbeidet i forbindelse med forvaltningsplan for Byfjellene, og er ment å gi en sammenfatning av kulturminneverdiene i området. Kulturminnegrunnlagene ser generelt på hovedstrukturene i et område, og fokuserer i mindre grad på enkeltobjekter. For de fleste planer og konsekvensutredninger vil de foreligge et tilsvarende kulturminnegrunnlag med lik disposisjon og innholdsrekkefølge. Kulturminnegrunnlagene utarbeidet av Byantikvaren, Byrådsavdeling for Byutvikling, benyttes som underlagsmateriale for videre planarbeid. Det skal også ligge som vedlegg til disse planene frem til politisk behandling, og vil inngå som grunnlagsmateriale for senere saksbehandling innen planområdet. Byantikvaren benytter kulturminnegrunnlagene som underlag for kulturminneplanlegging og saksbehandling knyttet til vern av kulturminner og kulturmiljø. I dette kulturminnegrunnlaget er det i hovedsak fjellområdene som beskrives. Her har det vært en kraftig gjengroing som skyldes at skoggrensen kryper høyere, men også manglende uthogging. Derfor er mange av kulturminnestrukturene ikke lenger synlige og heller ikke registrert. Samtidig er det i fjellområdene relativt få spor etter menneskelig aktivitet, men likevel finnes der noen historiefortellende strukturer. Dette er ulike kulturminnestrukturer og spor etter menneskelig aktivitet som er avsatt i området, og som er med på å beskrive og forstå ulik bruk gjennom tidene. Disse sporene er en kilde til kunnskap og opplevelse, og er dermed med på å gi området en økt bruksverdi. -

Fjaler Kyrkjeblad Desember 2014

2 Kyrkjelydsblad for Fjaler Lyset skin i mørkret Den kjende målaren Rembrandt har laga eit bilete av stallen i mørke er at vi har mist kontakten med skaparen. Den Vonde Betlehem som har gjort eit sterkt inntrykk på meg. Biletet viser har fått oss til å tru at vi lever best når vi er våre eigne herrar, eit svært fattigsleg rom der det ikkje kjem inn lys utanfrå. Lyset utan Gud. Difor vert mørkret avslørt når skaparen sjølv stig som gjer at det er råd å skilja personane på biletet, kjem frå inn i vår verd. barnet som ligg i krubba og lyser. Maria og Josef, hyrdin- gane og dyra i stallen, får alle sitt lys frå barnet. “Han kom til sitt eige, og hans eigne tok ikkje i mot han”. Slik var det den fyrste julenatt. Juleevangeliet seier det slik: “Det var ikkje husrom for dei.” Men det store underet, som vi aldri vert ferdige med å undra oss over og gle oss over, er at han kom likevel. Han let seg ikkje stogga av våre stengde dører. Julenatt ligg han der i krubba og kastar sitt lys over oss, ved at han kjem sjølv inn i vår mørke verd som eit hjelpelaust menneskebarn. Han lyser for oss som frelsaren. Dette lyset opplevde mange sjuke, hjelpelause og utstøytte menneske som seinare møtte Jesus. Og det same lyset strålar frå Golgata, der Jesus andar ut på krossen med orda “Det er fullført” på leppene sine. Fyrst der anar vi den djupaste grunnen til at han kom. Han kom for å ta det store oppgjerd med vårt fråfall som ingen av oss er i stand til å ta. -

Odda 2-Dagars 2017 Resultat 3-Kamp

Odda 2-dagars 2017 Resultat 3-kamp Plass Namn Klubb Løype 1 Løype 2 Løype 3 Totaltid B-Open Løype 1 Løype 2 Løype 3 Totaltid 1 Ylva Svanberg Helle TIF Viking 02:42 03:20 02:49 08:51 2 Bjørg Kocbach Bergens TF 03:12 04:39 03:45 11:36 3 Kjetil Hjelle Fitjar IL 03:01 03:50 05:16 12:07 4 Trude Kyrkjebø TIF Viking 03:42 04:17 04:23 12:22 5 Kari Secher Bergens TF 04:17 05:54 04:47 14:58 6 Torild Myrli TIF Viking 07:35 05:19 04:16 17:10 C-Open Løype 1 Løype 2 Løype 3 Totaltid 1 Lisa Bakkejord IL Gular 01:57 02:22 02:26 06:45 2 Mette Fitjar Fitjar IL 02:02 03:00 03:38 08:40 3 Olve Hekland IL Gular 02:53 06:21 04:06 13:20 4 Ingrid Roll Fana IL 04:38 07:35 05:25 17:38 D11-12 Løype 1 Løype 2 Løype 3 Totaltid 1 Idun Hekland IL Gular 02:23 04:45 04:01 11:09 2 Karina Solheim Øyre Odda OL 05:00 05:02 02:44 12:46 D13-14 Løype 1 Løype 2 Løype 3 Totaltid 1 Marie Roll-Tørnquist Fana IL 02:11 02:50 03:33 08:34 2 Kristine Bog Vikane Fana IL 03:06 03:30 03:52 10:28 3 Oda Kjellevold Malde IL Gular 02:49 05:17 03:22 11:28 4 Guro Femsteinevik Varegg Fleridrett 02:29 03:08 06:09 11:46 D15-16 Løype 1 Løype 2 Løype 3 Totaltid 1 Mari Fjellbirkeland Johannesen IL Gular 02:18 03:03 03:24 08:45 2 Tora Aasheim Nymark TIF Viking 05:09 03:20 03:36 12:05 3 Ida Solheim Eide Odda OL 03:35 04:32 04:36 12:43 4 Tiril Olausen Haugesund IL 06:25 05:04 05:47 17:16 D17 Løype 1 Løype 2 Løype 3 Totaltid 1 Anne Kari Vikingstad Torvastad IL 02:18 02:43 02:47 07:48 2 Ingvild Paulsen Vie Haugesund IL 02:09 02:39 03:02 07:50 3 Kristina Voll Haugesund IL 02:12 02:47 02:53 07:52 4 Tonje -

District 104 C.Pdf

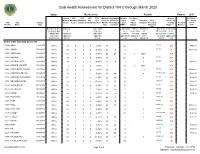

Club Health Assessment for District 104 C through March 2020 Status Membership Reports Finance LCIF Current YTD YTD YTD YTD Member Avg. length Months Yrs. Since Months Donations Member Members Members Net Net Count 12 of service Since Last President Vice Since Last for current Club Club Charter Count Added Dropped Growth Growth% Months for dropped Last Officer Rotation President Activity Account Fiscal Number Name Date Ago members MMR *** Report Reported Report *** Balance Year **** Number of times If below If net loss If no report When Number Notes the If no report on status quo 15 is greater in 3 more than of officers that in 12 within last members than 20% months one year repeat do not have months two years appears appears appears in appears in terms an active appears in in brackets in red in red red red indicated Email red Clubs more than two years old 19560 ARNA 11/13/1970 Active 10 0 0 0 0.00% 10 14 MC,SC N/R $400.65 19562 ASKØY 03/08/1967 Active 37 0 2 -2 -5.13% 38 7 4 MC,SC 24+ $1531.86 31071 AUSTEVOLL 07/01/1975 Active 51 1 3 -2 -3.77% 52 27 0 1 None N/R 19565 BERGEN 05/23/1951 Active 15 0 0 0 0.00% 15 16 7 MC,SC N/R 19561 BERGEN ÅSANE 07/01/1966 Active 24 1 2 -1 -4.00% 26 4 2 2 MC,SC N/R $328.86 88725 BERGEN STUDENT 06/23/2005 Active 2 0 0 0 0.00% 2 20 3 None N/R 19566 BERGEN/BERGENHUS 09/14/1966 Active 25 0 0 0 0.00% 26 9 13 MC,SC N/R $5683.62 31166 BERGEN/BJØRGVIN 09/10/1975 Active 18 0 1 -1 -5.26% 19 44 0 4 M,VP,MC,SC N/R $121.80 28228 BERGEN/LØVSTAKKEN 03/22/1974 Active 21 0 1 -1 -4.55% 22 30 5 MC,SC N/R $164.43 19567 BERGEN/ULRIKEN -

Sparebank 1 Nord-Norge Annual Report 2019 006

SPAREBANK 1 NORD-NORGE ANNUAL REPORT 2019 006 010 012 014 016 017 018 022 048 049 050 052 053 142 146 154 158 160 162 177 182 190 196 198 202 204 213 225 226 Table of contents NORD-NORGE 1 SPAREBANK 006 From the CEO SpareBank 1 Nord-Norge 010 Strategic compasss 012 Our history 014 Important events 016 Branches 017 Organization and company structure 018 Annual report 022 Annual report from the board ANNUAL ACCOUNTS ANNUAL Annual accounts 2019 048 Annual Report – Income statement 049 Annual Report – Balance Sheet 050 Annual Report – Changes in equity 052 Annual Report – Cash Flow Statement 053 Annual accounts – Notes 142 Statement from the Board of Directors and Chief Executive Officer 146 Auditor’s report Operations 154 Group Management 158 Board of Directors 160 Governing bodies OPERATIONS 162 Corporate governance 177 Risk management and internal control 182 Ownership 190 Operations 196 Markets 198 The SpareBank 1- alliansen CORPORATE SOCIAL RESPONSIBILITY SOCIAL CORPORATE 202 The foundations 204 Organisation and HR Corporate social responsibility 213 Sustainability 225 Samfunnsløftet 226 Index Global Reporting Intiative Continued Added Value Uncertainty dominated 2019. Trade wars, Brexit, esc- The financial results for SpareBank 1 Nord-Norge alating levels of conflict in the Middle East as well are affected by the economic temperature of the as climate change resulting in floods and wildfires. region. In addition, SpareBank 1 Nord-Norge have Paradoxically, Northern Norway, and SpareBank 1 gained a good effect by merging insurance compa- Nord-Norge profits from this uncertainty due to nies of SpareBank 1 and DNB. being an export driven region. -

Norway Maps.Pdf

Finnmark lVorwny Trondelag Counties old New Akershus Akershus Bratsberg Telemark Buskerud Buskerud Finnmarken Finnmark Hedemarken Hedmark Jarlsberg Vestfold Kristians Oppland Oppland Lister og Mandal Vest-Agder Nordre Bergenshus Sogn og Fjordane NordreTrondhjem NordTrondelag Nedenes Aust-Agder Nordland Nordland Romsdal Mgre og Romsdal Akershus Sgndre Bergenshus Hordaland SsndreTrondhjem SorTrondelag Oslo Smaalenenes Ostfold Ostfold Stavanger Rogaland Rogaland Tromso Troms Vestfold Aust- Municipal Counties Vest- Agder Agder Kristiania Oslo Bergen Bergen A Feiring ((r Hurdal /\Langset /, \ Alc,ersltus Eidsvoll og Oslo Bjorke \ \\ r- -// Nannestad Heni ,Gi'erdrum Lilliestrom {", {udenes\ ,/\ Aurpkog )Y' ,\ I :' 'lv- '/t:ri \r*r/ t *) I ,I odfltisard l,t Enebakk Nordbv { Frog ) L-[--h il 6- As xrarctaa bak I { ':-\ I Vestby Hvitsten 'ca{a", 'l 4 ,- Holen :\saner Aust-Agder Valle 6rrl-1\ r--- Hylestad l- Austad 7/ Sandes - ,t'r ,'-' aa Gjovdal -.\. '\.-- ! Tovdal ,V-u-/ Vegarshei I *r""i'9^ _t Amli Risor -Ytre ,/ Ssndel Holt vtdestran \ -'ar^/Froland lveland ffi Bergen E- o;l'.t r 'aa*rrra- I t T ]***,,.\ I BYFJORDEN srl ffitt\ --- I 9r Mulen €'r A I t \ t Krohnengen Nordnest Fjellet \ XfC KORSKIRKEN t Nostet "r. I igvono i Leitet I Dokken DOMKIRKEN Dar;sird\ W \ - cyu8npris Lappen LAKSEVAG 'I Uran ,t' \ r-r -,4egry,*T-* \ ilJ]' *.,, Legdene ,rrf\t llruoAs \ o Kirstianborg ,'t? FYLLINGSDALEN {lil};h;h';ltft t)\l/ I t ,a o ff ui Mannasverkl , I t I t /_l-, Fjosanger I ,r-tJ 1r,7" N.fl.nd I r\a ,, , i, I, ,- Buslr,rrud I I N-(f i t\torbo \) l,/ Nes l-t' I J Viker -- l^ -- ---{a - tc')rt"- i Vtre Adal -o-r Uvdal ) Hgnefoss Y':TTS Tryistr-and Sigdal Veggli oJ Rollag ,y Lvnqdal J .--l/Tranbv *\, Frogn6r.tr Flesberg ; \. -

Supplementary Information Q2 2017

Chief Executive, CEO Arne Austreid For further information, please contact Inge Reinertsen, Chief Financial Officer [email protected] +47 909 95 033 Stian Helgøy, VP Investor Relations [email protected] +47 906 52 173 Address SpareBank 1 SR-Bank, Postboks 250, 4066 Stavanger Visiting address: Bjergsted Terrasse 1, 4001 Stavanger SpareBank 1 SR-Bank Switchboard: +47 915 02002 Information on the Internet SpareBank 1 SR-Bank’s homepage www.sr-bank.no Financial Calendar Second quarter 2017 9 August Third quarter 2017 27 October Table of Contents 1. SpareBank 1 SR-Bank ASA .............................................................................. 1 1.1 Financial highlights ....................................................................................... 1 1.2 Business description: leading financial institution in Rogaland, Hordaland and Agder ........................................................................................................................ 3 Retail Market ................................................................................................................................................. 3 Corporate Market .......................................................................................................................................... 3 Capital Market ............................................................................................................................................... 3 Vision and strategy ....................................................................................................................................... -

Annual Report 2020 2 SPAREBANK 1NORD-NORGE Table of Contents

Annual Report 2020 2 SPAREBANK 1 NORD-NORGE 1 SPAREBANK Table of contents SPAREBANK 1 NORD-NORGE 04 From the CEO 08 Strategic compass 10 Our history 12 Timeline 14 Important events 16 Branches 20 Organisation chart 22 Company structure 23 Annual report 24 Group profit analysis 27 Annual report of the Board 28 ANNUAL ACCOUNTS 2020 60 Income statement 62 Balance sheet 63 Changes in equity 64 Cash flow statement 66 Notes 67 Statement by the Bord og Directors and the Group CEO 160 Alternative performance measures 161 Auditor’s report 164 3 Table of contents NORD-NORGE 1 SPAREBANK OPERATIONS 170 Group Management 172 Board of Directors 174 Governing bodies 176 Corporate governance 180 Risk management and internal control 198 Ownership 204 Operations 210 SpareBank1 Nord-Norge Capital markets 218 The SpareBank 1-alliansen 221 The foundations 224 Organisation and HR 226 CORPORATE SOCIAL RESPONSIBILITIY 234 Sustainability in SpareBank 1 Nord-Norge 236 Climate risk (TCFD) 241 Annex 1: Global reporting initiative (GRI) index 256 Annex 2: Carbon exposure in the credit portfolio 262 Annex 3: Stakeholder analysis 2020 264 Annex 4: ‘Samfunnsløftet’s’ contribution to the UN sustainability goals 266 Samfunnsløftet across all Northern Norway 268 4 SPAREBANK 1 NORD-NORGE 1 SPAREBANK Sparebank 1 Nord-Norge SpareBank 1 Nord-Norge is the leading finance house in Northern Norway. The group is part of SpareBank 1-alliansen, an alliance of 14 independent savings banks across the entire country. 5 SPAREBANK 1 NORD-NORGE 1 SPAREBANK Photo: Marius Fiskum DIGITALISATION 2020 was the year that video meetings – up to then meeting between people remains at centre-stage. -

Administrative and Statistical Areas English Version – SOSI Standard 4.0

Administrative and statistical areas English version – SOSI standard 4.0 Administrative and statistical areas Norwegian Mapping Authority [email protected] Norwegian Mapping Authority June 2009 Page 1 of 191 Administrative and statistical areas English version – SOSI standard 4.0 1 Applications schema ......................................................................................................................7 1.1 Administrative units subclassification ....................................................................................7 1.1 Description ...................................................................................................................... 14 1.1.1 CityDistrict ................................................................................................................ 14 1.1.2 CityDistrictBoundary ................................................................................................ 14 1.1.3 SubArea ................................................................................................................... 14 1.1.4 BasicDistrictUnit ....................................................................................................... 15 1.1.5 SchoolDistrict ........................................................................................................... 16 1.1.6 <<DataType>> SchoolDistrictId ............................................................................... 17 1.1.7 SchoolDistrictBoundary ........................................................................................... -

Lagsblad for Leikanger Skyttarlag • Desember 2020 Meir Fart, Meir Moro! 2

LAGSBLAD FOR LEIKANGER SKYTTARLAG • DESEMBER 2020 MEIR FART, MEIR MORO! 2 FIBERNETT på arbeid, heime og hytta Kontakt oss for meir informasjon: sognenett.no | [email protected] | 9519 2222 SKYTELAPPEN LAGSBLAD FOR LEIKANGER SKYTTARLAG 2020 Leikanger skyttarlag sender også i år lagsbladet sitt Skytelappen til alle innbyggarar i gamle Leikanger kommune. Gjennom eit slikt blad får me orientera om tilboda og aktiviteten vår, og dei ulike ANSVARLEG UTGIVAR. årgangane kan vera gode å ha om me vil Leikanger skyttarlag v/styret. Postadresse: 6863 Leikanger sjå tilbake på tidlegare hendingar, bilete og * resultat. BANK: Sparebanken Sogn og Fjordane Konto nr.: 3781.07.31045 Første utgåve av Skytelappen kom i 1984, Heimeside: www.dfs.no/leikanger så dette blir vel 37. årgang. e-post: [email protected] SATS, MONTASJE OG TRYKK: INGVALD HUSABØ PRENTEVERK, LEIKANGER De finn alle blada på laget si heimeside www.dfs.no/leikanger under fana Klasseførde «Om Leikanger». skyttarar i 2021 Skyttarlaget rettar stor takk til Ingvald Tala i klamme gjeld klassesetting for 15 meter innandørs. Husabø Prenteverk for støtte, deira Klasse 5 Arnhild Eiken, Svein Kåre Furre profesjonelle hjelp gjer det muleg å få eit Klasse 4 Vidar Skarsbø Dale, Stine Njøs Eikeland (5), Gaute blad med så høg teknisk kvalitet. Eliassen Hamre, Oliver Karelius Prøven, Eivind Yttri. Klasse 3 Jomar Skarsbø Dale, Atle Henning Lunde (4), Helena Sæbø Nes (4), Malin Sæbø Nes, Janne Humlestøl Njøs (4), Trine Humlestøl Njøs (4), Ørjan Næss, Redaksjonen ynskjer alle ei god jul Jostein Odd, Gabriel Skjulhaug Yttri, Torbjørn Aase. Klasse 2 og eit godt nytt år! Janne Marita Bergheim (3), Gunnar Hamre, Steinar 3 Husabø, Ivar Husum, Linda Furre Lunde, Eirik Håland Moen (3), Håkon Nesse, Camilla Njøs, Jørn Njøs (3), Kjell Nornes, Linn Marita Næss, Yngve Næss, Helsing Leif Arne Stadheim, Odd Rune Våge, Arve Yttri, Siv Kristin Laberg Yttri, Frode Ølmheim, Nils Olav Øy. -

Second Opinion

Fana Sparebank Green Finance Framework Second Opinion 11.12.2019 Fana Sparebank is a local savings bank based in Bergen, Norway, holding a SHADES OF GREEN substantial share in the regional retail market. Based on our review, we rate the Fana Sparebank’s The Fana Sparebank green finance framework provides a framework for green finance framework investments into projects that align with the Green Bond and Green Loan CICERO Medium Green. Principles. Eligible projects include financing or refinancing investments in green buildings, clean transport and renewable energy. Fana Sparebank excludes fossil energy generation, research and/or development within weapons and defense, Included in the overall potentially environmentally negative resource extraction, gambling or tobacco. shading is an assessment of from its use of proceeds. the governance structure of the green finance Fana Sparebank expects to allocate the majority of net proceeds to green buildings, which cover both new and existing buildings. In addition to new and framework. CICERO existing green buildings, project categories include clean transport and renewable Shades of Green finds the energy. Investors should be aware that buildings that fall within the “green” zones governance procedures in defined by the Bergen municipality can qualify automatically for green funding. Fana Sparebank’s This includes that buildings only following regulation at the time of construction, framework to be good. meeting energy efficiency requirements similar to EPC rating C will qualify according to the framework. Direct fossil fuel heating is however excluded and for new buildings requirements are more stringent than regulation. Fana Sparebank’s governance policy and framework meet the Green Bond and Green Loans Principles.