A Framework on Internet Banking Services for the Rationalized Generations

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Useful Information for Shareholders

useful information for shareholders Financial Calendar Particulars Date Twelfth Annual General Meeting April 17, 2008 First Extra-ordinary General Meeting April 17, 2008 Transfer of bonus shares May 07, 2008 Half-yearly Financial Statements (Un-audited) June 30, 2008 Record date for Bonus Shares March 01, 2009 Next half-yearly Financial Statements June 30, 2009 2nd Extra-ordinary General Meeting The 2nd Extra-ordinary General Meeting of the shareholders of the Bank will be held on March 23, 2009 at 10:00 a.m. at the “Hall of Fame” of Bangladesh-China Friendship Conference Center (BCFCC), Agargaon, Dhaka. 13th Annual General Meeting The 13th Annual General Meeting of shareholders of the Bank will be held on March 23,2009 at 10:30 a.m. at the “Hall of Fame” of Bangladesh-China Friendship Conference Center (BCFCC), Agargaon, Dhaka. Information on dividends Bonus share @3.94719 for existing 1 share of Taka 100 each for 2007 were declared in 2008. 50% bonus share i.e. 1 bonus share for existing 2 shares of Taka 100 each is proposed for 2008. Share transfer system The shares of Dutch-Bangla Bank Limited (DBBL) are being traded at the Stock Exchanges in Dematerialized form since June 15, 2004 through Central Depository Bangladesh Limited (CDBL) as per directive of Securities and Exchange Commission (SEC). Physical shares, which are not yet dematerialized, can be dematerialized with CDBL through BO account with Depository Participant (DP). Information relating to shareholdings Distribution of shares of DBBL and shareholdings by the Directors are given in Note 17 to Financial Statements of this Annual Report. -

Country Wise List of Our Foreign Correspondents Sonali Bank Limited

Country wise list of our Foreign correspondents as on 31-12-2018. Prepared bv : Sonali Bank limited Foreign Remittance Management Division Head office.Dhaka. Courtesv : Sonali Bank limited (Product Development Team) Business Development Division Head office,Dhaka. E mail-dgmb ddp dt@s on aliban k. co m.b d Md Mizanur Rahman Md Zillur Rahman Sikder Senior Principal officer Senior ofl.icer Product Development Team. Product Der elopment Team. mob-01708159313. mob-019753621 15. Corp Bank Country dents as on 3ut2na18 Sl.No. Name ofCountry No. o No. of SI. No. Name ofCountry No. of No. of Corp. RMA Corn. RMA 01. Afganistan J I 45. Malaysia t2 12 02. Australia 8 7 46. Monaco I I 03. Algeria J 1 41. Malta 2 04. Argentina I Z I 48. Netherlands 8 7 , 05. Albenia i 49. New Zealand J J 06. Austria 7 6 50. Nepal 2 2 07. Balrain J J 51. Norway 2 I 08. Belgium 9 7 52. Nigeria I ) 09. Bhutan 2 53. Oman I q 2 10. Bulgaria 4 4 54. Pakistan 18 18 ll Brunei I 55, Poland 3 1 12. Brazrl 4 2 56. Philippines 5 5 lJ. Republic ofBelarus I 57. Portugal 4 J 14. Canada 8 7 58. Qatar 6 5 15. China 4 l3 59. Romania 1 1 16. Chile I I 60 Russia 9 8 17. Croatia I 61. SaudiArabia l6 t5 18. Cyprus I I o/.. Senegal 1 1 t 19. CzechRepublic 6 J 63. Serbia + J ,1 20. Denmark J J 64. Srilanka 5 21. -

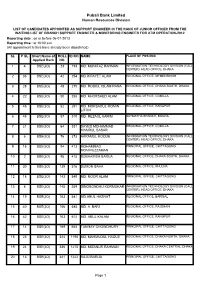

List of Candidates Appointed As Support Engineer in the Rank of Junior Officer From

Pubali Bank Limited Human Resources Division LIST OF CANDIDATES APPOINTED AS SUPPORT ENGINEER IN THE RANK OF JUNIOR OFFICER FROM THE WAITING LIST OF BRANCH SUPPORT ENGINEER & MONITORING ENGINEER FOR ATM OPERATION-2012 Reporting date : on or before 06-01-2013 Reporting time : at 10:00 a.m. (All appointment letters have already been dispatched) SL P SL Short Name of ROLL ID NO. NAME PLACE OF POSTING Applied Rank NO. 1 4 BSE(JO) 23 193 MD. MONITAZ RAHMAN INFORMATION TECHNOLOGY DIVISION (CALL CENTER), HEAD OFFICE, DHAKA 2 33 BSE(JO) 42 254 MD.RIFAYET ALAM REGIONAL OFFICE, MYMENSINGH 3 28 BSE(JO) 48 270 MD. ROBIUL ISLAM RANA REGIONAL OFFICE, DHAKA SOUTH, DHAKA 4 22 BSE(JO) 50 285 MD. KHORSHED ALAM REGIONAL OFFICE, COMILLA 5 45 BSE(JO) 52 291 MD. MOKSADUL MOMIN REGIONAL OFFICE, RANGPUR LITON 6 48 BSE(JO) 57 310 MD. REZAUL KARIM SATMATHA BRANCH, BOGRA 7 21 BSE(JO) 64 331 SAYED MOHAMMAD REGIONAL OFFICE, COMILLA KHAIRUL BASAR 8 6 BSE(JO) 76 373 AKRAMUL HOQUE INFORMATION TECHNOLOGY DIVISION (CALL CENTER), HEAD OFFICE, DHAKA 9 15 BSE(JO) 94 413 MOHAMMAD PRINCIPAL OFFICE, CHITTAGONG MONIRUZZAMAN 10 2 BSE(JO) 95 415 SUBHASISH BARUA REGIONAL OFFICE, DHAKA SOUTH, DHAKA 11 30 BSE(JO) 139 516 SUMON SAHA REGIONAL OFFICE, KHULNA 12 18 BSE(JO) 143 549 MD. NOOR ALAM PRINCIPAL OFFICE, CHITTAGONG 13 8 BSE(JO) 145 559 DINOBONDHU KORMOKAR INFORMATION TECHNOLOGY DIVISION (CALL CENTER), HEAD OFFICE, DHAKA 14 19 BSE(JO) 153 581 MD.ABUL HASNAT REGIONAL OFFICE, BARISAL 15 40 BSE(JO) 156 585 MD. -

“E-Business and on Line Banking in Bangladesh: an Analysis”

“E-Business and on line banking in Bangladesh: an Analysis” AUTHORS Muhammad Mahboob Ali ARTICLE INFO Muhammad Mahboob Ali (2010). E-Business and on line banking in Bangladesh: an Analysis. Banks and Bank Systems, 5(2-1) RELEASED ON Wednesday, 07 July 2010 JOURNAL "Banks and Bank Systems" FOUNDER LLC “Consulting Publishing Company “Business Perspectives” NUMBER OF REFERENCES NUMBER OF FIGURES NUMBER OF TABLES 0 0 0 © The author(s) 2021. This publication is an open access article. businessperspectives.org Banks and Bank Systems, Volume 5, Issue 2, 2010 Muhammad Mahboob Ali (Bangladesh) E-business and on-line banking in Bangladesh: an analysis Abstract E-business has created tremendous opportunity all over the globe. On-line banking can act as a complementary factor of e-business. Bangladesh Bank has recently argued to introduce automated clearing house system. This pushed up- ward transition from the manual banking system to the on-line banking system. The study has been undertaken to ob- serve present status of the e-business and as its complementary factor on-line banking system in Bangladesh. The arti- cle analyzes the data collected from Bangladeshi banks up to February 2010 and also used snowball sampling tech- niques to gather answer from the five hundred respondents who have already been using on-line banking system on the basis of a questionnaire which was prepared for this study purpose. The study found that dealing officials of the banks are not well conversant about their desk work. The author observed that the country can benefit from successful utiliza- tion of e-business as this will help to enhance productivity. -

SEBL Financial Statements As on 31

Southeast Bank Limited Report and Consolidated & Separate Financial Statements as at and for the year ended 31 December 2016 Rahman Rahman Huq Telephone +880 (2) 988 6450-2 Chartered Accountants Fax +880 (2) 988 6449 9&5Mohakhali C/A E-mail [email protected] Dtaka 1212 lnternet www.kpmg.com/bd Bangladesh independent auditoris report to the shareholders of Southeast Bank lJ■ lited Report on the financiat statements We have audited the accompanying consolidated financial statements ol Southeast Bank Limited and its subsidiaries (the "Group') as well as the separate financial statements of Southeast Bank Limited (the "Bank'), which comprise the consolidated balance sheet and the separate balance sheet as at 3l December 2016, and the consolidated and separate profit and loss accounts, consolidated and separate statements of changes in equity and consolidated and separate cash ffow statements for the year then ended, and a summary of significant accounting policies and other explanatory information. Management's responslbility for the financial statements and internal controls Management is responsible for the preparation of consolidated financial statements of the Group and also separate 'linancial statements of the Bank that give a true and lair view in accordance with Bangladesh Financial Reporting Standards as explained in note 2 and for such intemal control as management determines is necessary to enable the preparation of consolidated financial statements of the Group and also separate financial statements of the Bank that are lree from matedal mi$statement, whether due to traud or eror. The Bank Company Act, 1991 and the Bangladesh Bank Regulations require the Management to ensure etf€ctive intemal audit, intemal control and risk management functions of the Bank. -

Dutch-Bangla Bank Limited Balance Sheet As at 31 March 2016 (Main Operation and Off-Shore Banking Unit)

Dutch-Bangla Bank Limited Balance Sheet As at 31 March 2016 (Main Operation and Off-shore Banking Unit) PROPERTY AND ASSETS Notes 31-Mar-16 31-Dec-15 31-Mar-15 Taka (Un-audited) Taka (Audited) Taka (Un-audited) Main Operation Off-shore Total Total Total Cash In hand (including foreign currencies) 4 8,687,307,386 - 8,687,307,386 8,296,998,632 7,020,803,945 Balance with Bangladesh Bank and its agent bank (s) (including foreign currencies) 5 17,414,308,363 - 17,414,308,363 14,555,926,865 15,178,783,055 26,101,615,749 - 26,101,615,749 22,852,925,497 22,199,587,000 Balance with other banks and financial institutions 6 In Bangladesh 23,883,193,400 2,052,052,493 25,935,245,893 27,591,599,177 13,010,752,944 Outside Bangladesh 804,409,204 - 804,409,204 1,154,177,150 1,840,924,301 24,687,602,604 2,052,052,493 26,739,655,097 28,745,776,327 14,851,677,245 Money at call and short notice 7 1,980,000,000 - 1,980,000,000 5,270,000,000 1,100,000,000 Investments 8 Government 19,187,552,263 - 19,187,552,263 19,405,280,474 25,193,823,649 Others 564,983,434 - 564,983,434 804,983,434 885,283,434 19,752,535,697 - 19,752,535,697 20,210,263,908 26,079,107,083 Loans and advances 9 Loans, cash credits, overdrafts, etc. -

Sl. Correspondent / Bank Name SWIFT Code Country

International Division Relationship Management Application( RMA ) Total Correspondent: 156 No. of Country: 36 Sl. Correspondent / Bank Name SWIFT Code Country 1 ISLAMIC BANK OF AFGHANISTAN IBAFAFAKA AFGHANISTAN 2 MIZUHO BANK, LTD. SYDNEY BRANCH MHCBAU2S AUSTRALIA 3 STATE BANK OF INDIA AUSTRALIA SBINAU2S AUSTRALIA 4 KEB HANA BANK, BAHRAIN BRANCH KOEXBHBM BAHRAIN 5 MASHREQ BANK BOMLBHBM BAHRAIN 6 NATIONAL BANK OF PAKISTAN NBPABHBM BAHRAIN 7 AB BANK LIMITED ABBLBDDH BANGLADESH 8 AGRANI BANK LIMITED AGBKBDDH BANGLADESH 9 AL-ARAFAH ISLAMI BANK LTD. ALARBDDH BANGLADESH 10 BANGLADESH BANK BBHOBDDH BANGLADESH 11 BANGLADESH COMMERCE BANK LIMITED BCBLBDDH BANGLADESH BANGLADESH DEVELOPMENT BANK 12 BDDBBDDH BANGLADESH LIMITED (BDBL) 13 BANGLADESH KRISHI BANK BKBABDDH BANGLADESH 14 BANK ASIA LIMITED BALBBDDH BANGLADESH 15 BASIC BANK LIMITED BKSIBDDH BANGLADESH 16 BRAC BANK LIMITED BRAKBDDH BANGLADESH 17 COMMERCIAL BANK OF CEYLON LTD. CCEYBDDH BANGLADESH 18 DHAKA BANK LIMITED DHBLBDDH BANGLADESH 19 DUTCH BANGLA BANK LIMITED DBBLBDDH BANGLADESH 20 EASTERN BANK LIMITED EBLDBDDH BANGLADESH EXPORT IMPORT BANK OF BANGLADESH 21 EXBKBDDH BANGLADESH LTD 22 FIRST SECURITY ISLAMI BANK LIMITED FSEBBDDH BANGLADESH 23 HABIB BANK LTD HABBBDDH BANGLADESH 24 ICB ISLAMI BANK LIMITED BBSHBDDH BANGLADESH INTERNATIONAL FINANCE INVESTMENT 25 IFICBDDH BANGLADESH AND COMMERCE BANK LTD (IFIC BANK) 26 ISLAMI BANK LIMITED IBBLBDDH BANGLADESH 27 JAMUNA BANK LIMITED JAMUBDDH BANGLADESH 28 JANATA BANK LIMITED JANBBDDH BANGLADESH 29 MEGHNA BANK LIMITED MGBLBDDH BANGLADESH 30 MERCANTILE -

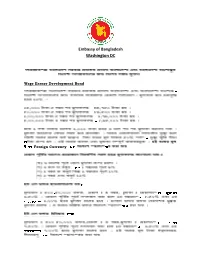

Procedure of Open Foreign Currency Account.Pdf

Embassy of Bangladesh Washington DC Wage Earner Development Bond Foreign Currency Foreign Currency Accounts Specimern Signature Specimern Signature FC Account Opening Form and Specimen Signature Extension [email protected] Diplomatic Bag /DHL/Fedex English Version The Government of the People’s Republic of Bangladesh have introduced special saving facilities for Non Resident Bangladeshis and also foreigner’s of Bangladeshi decent. Wage Earner Development Bond : Most profitable fixed deposit investment “Wage Earner Development Bond” for Non Resident Bangladeshi’s and Foreigners of Bangladeshi decent introduced by the Government of the People’s Republic of Bangladesh. Compound rate of profit is 12.00% per annum. Tk. 25,000 become Tk. 44,750 with profit after 5 years Tk. 50,000 become Tk. 89,500 with profit after 5 years Tk. 1,00,000 become Tk. 1,79,000 with profit after 5 years Tk. 5,00,000 become Tk. 8,95,000 with profit after 5 years Profits could be withdrawn at a rate of Tk. 1000.00 per month for every Tk. 100000.00. For withdrawal of profit simple rate is applicable. Nominee is entitled to 30% to 50% of invested amount as a death risk insurance at no extra charge in case of death of the bond owner. No income tax is levied on the initial investment or profits thereof. Initial investment amount could be transferred back in foreign currency. If encashed before maturity you will get interest at following rate : a. Before six month no interest b. After six month and before 1 year : 9% c. After 1 year and before 2 years : 10% d. -

Customer Charter 1

Dutch-Bangla Bank Limited YOUR TRUSTED PARTNER TABLE OF CONTENT Article Number Topic Page Number 1.1 Introduction 1 1.2 Objectives of Customer Charter 1 1.3 Legal basis of the Customer Charter 1 1.4 Application of the Customer Charter 1 1.5 Impact of the violation of the Charter 1 2 Head Office Communication 2 3 Statistics of DBBL Branches , Offices and outlets etc 2 4 Office and Transaction Time Table 3 5 DBBL Service Desk 3 6 Common Areas Of DBBL Services 3-16 7 Service Charges 16 8 Rate of Interest 16 9 Customers Rights/Bankers Obligations 17 10 Customers Obligations/Bankers Right 18 11 Customer Complaints lodgment Process 19 12 Tips for Customers 20 13 How to protect yourself when banking online 21 14 Helping us serve you better 22 1.1 Introduction Customer Charter is a general statement of commitments for providing banking services and necessary information to our customers. It also aims at making our Customers conscious about their rights and obligations to bank as well. It outlines the types of services we will endeavor to provide and the various channels for customers to share feedback. The main objectives of the Customer Charter are to make the customers conscious about their general rights, obligations, grievance approach process so as to enable them in taking their own decision on banking matters. 1.2 Objectives of Customer Charter The Charter is intended to: 1. Define the standards of good practice and service; 2. Promote disclosure of information relevant and useful to Customers; 3. Promote informed and effective relationships between the Bank and its Customers; and 4. -

District Bank Branch Location Bank Bank Branch Address DLI Office

DLI Bank Branch DLI District Bank Bank Branch Address A/C Location Office No. Bagerhat Bagerhat Agrani Bank Ltd Bagerhat, Khulna Khulna 737 Bagerhat Bagerhat Pubali Bank Ltd Bagerhat-9300 Khulna 9 Bagerhat Chakshree Bazar Bangladesh Krishi Bank Chakshree Bz. Rampal, Bagerhat Khulna 110 Bagerhat Chital Mari Bazar Bangladesh Krishi Bank Chitalmari Bz.,Bagerhat-9360 Khulna 214 Bagerhat Fakirhat Bangladesh Krishi Bank Fakirhat, Bagerhat-9370 Khulna 293 Bagerhat Mongla Pubali Bank Ltd Mongla Bazar,MadrasaRd.,Bagerhat-9351 Khulna 5 Bagerhat Morelgonj Bangladesh Krishi Bank Morelgonj, Bagerhat-9320 Khulna 281 Bagerhat Raindabazar Bangladesh Krishi Bank Raindabazar,Sarankhola, Bagerhat-9330 Khulna 263 Bagerhat Rampal Bangladesh Krishi Bank Rampal, Bagerhat-9340 Khulna 211 Bagerhat Doiboghohati Bangladesh Krishi Bank Morelgonj, Bagerhat-9320 Khulna 44 Bagerhat Foltita Bangladesh Krishi Bank Kolkolia, Fakirhat, Bagerhat Khulna 30 Bagerhat Mollahat Bangladesh Krishi Bank Mollahat, Bagerhat-9380 Khulna 243 Bagerhat Sannayashibazar Bangladesh Krishi Bank Morelgonj, Bagerhat-9321 Khulna 1 Bagerhat Town Noapara Bangladesh Krishi Bank Town Noapara, Fakirhat, Bagerhat-9370 Khulna 45 Bandarban Baishari Bangladesh Krishi Bank Baishari, Naikhagchari, Bandarban-4660 Chittagong 81 Bandarban Bandarban Pubali Bank Ltd Bandarban-4600 Chittagong 16 Bandarban Lama Bangladesh Krishi Bank Lama, Bandarban Chittagong 453 Barguna Amtoli Bangladesh Krishi Bank Amtoli, Borguna-8710 Barisal 149 Barguna Barguna Pubali Bank Ltd Barguna-8700 Barisal 9 Barguna Betagi Bangladesh -

Dutch Bangla Bank Limited & HSBC

P a g e | 1 Jatiya Kabi Kazi Nazrul Islam University Trishal, Mymensingh Course Title: Research Methodology Course Code: 403 TITLE OF RESEARCH PROPOSAL: Dutch Bangla Bank Limited & HSBC Products “Life Line” A comparative study on the loan Evaluator: Shakhawat Hossain Sarkar Lecturer, Dept. of Accounting & Information Systems, Jatiya Kabi Kazi Nazrul Islam University. Submitted By: KAWSAR ALAM SHIHAB ID NO. : 08132536 SESSION: 2007-08 DEPTRTMENT OF AIS J.K.K.N.I.U [email protected] Date of Submission: 23rd October, 2012. P a g e | 2 Table of Contents 1. Abstract Page 03 2. Introduction Page 04 3. Source of Data and Methodology Page 05 a) Primary data: Page 05 b) Secondary data: Page 05 4. Research Output & Findings: Page 06 5. Conclusion: Page 06 6. Reference: Page 07 P a g e | 3 A comparative study on the loan Products “Life Line” Dutch Bangla Bank Limited & HSBC 1. Abstract: There is possibly nothing more important to a bank than the loans they make. Loans are the way a bank makes money. When loans go bad, it can be fatal to a bank. Loans are the lifeblood of a bank. All businesses sell products, and a bank's product is money. Banks make money by taking in funds from depositors and other sources and then lending money out to customers. The bank spread is the difference between what the interest a bank must pay to obtain the funds and the rate the bank charges on the loan. For example, a bank might pay two percent interest to a depositor and charge a customer six percent interest on a loan. -

Dutch - Bangla Bank Limited

DUTCH - BANGLA BANK LIMITED UN-AUDITED FINANCIAL STATEMENTS For the Third Quarter ended 30 September 2019 Dutch-Bangla Bank Limited Consolidated Balance Sheet As at 30 September 2019 PROPERTY AND ASSETS Notes 30-Sep-19 31-Dec-18 30-Sep-18 Taka (Un-audited) Taka (Audited) Taka (Un-audited) Cash In hand (including foreign currencies) 4 13,588,077,031 17,419,869,741 13,424,335,615 Balance with Bangladesh Bank and its agent bank (s) (including foreign currencies) 5 21,515,865,165 32,728,425,040 25,272,773,773 35,103,942,197 50,148,294,781 38,697,109,388 Balance with other banks and financial institutions 6 In Bangladesh 13,775,674,405 6,715,668,728 19,872,111,450 Outside Bangladesh 138,592,298 656,896,195 2,646,119,188 13,914,266,703 7,372,564,923 22,518,230,638 Money at call on short notice 7 13,170,000,000 - 2,670,000,000 Investments 8 Government 43,878,875,002 31,457,164,331 25,593,984,526 Others 1,411,283,434 751,283,434 251,283,434 45,290,158,436 32,208,447,765 25,845,267,960 Loans and advances 9 Loans, cash credits, overdrafts, etc. 228,437,319,738 209,463,408,465 196,168,533,474 Bills purchased and discounted 17,168,958,714 22,090,531,874 21,013,792,031 - - 245,606,278,452 231,553,940,339 217,182,325,505 Fixed assets including land, building, furniture and fixtures 10 5,483,822,895 5,737,308,593 5,129,942,207 Other assets 11 21,613,894,320 19,448,234,568 19,350,180,886 Non-banking assets - - - TOTAL ASSETS 380,182,363,003 346,468,790,969 331,393,056,584 LIABILITIES AND CAPITAL Liabilities Borrowings from other banks, financial institutions