“E-Business and on Line Banking in Bangladesh: an Analysis”

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

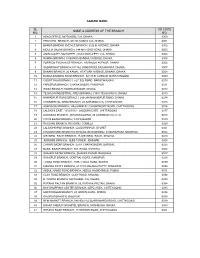

Agrani Bank Sl No. Name & Address of the Branch Ad Code

AGRANI BANK SL AD CODE NAME & ADDRESS OF THE BRANCH NO. NO. 1 HEAD OFFICE, MOTIJHEEL C/A, DHAKA 0000 2 PRINCIPAL BRANCH, 9/D DILKUSHA C/A, DHAKA 0001 3 BANGA BANDHU AVENUE BRANCH, 32 B.B. AVENUE, DHAKA 0002 4 MOULVI BAZAR BRANCH, 144 MITFORD ROAD, DHAKA. 0003 5 AMIN COURT, MOTIJHEEL, 62/63 MOTIJHEEL C/A, DHAKA 0004 6 RAMNA BRANCH, 18 BANGA BANDHU AVENUE, DHAKA 0005 7 FOREIGN EXCHANGE BRANCH, 1/B RAJUK AVENUE, DHAKA 0006 8 SADARGHAT BRANCH,3/7/1&2 JONSON RD,SADARGHAT, DHAKA. 0007 9 BANANI BRANCH, 26 KAMAL ATATURK AVENUE, BANANI, DHAKA. 0008 10 BANGA BANDHU ROAD BRANCH, 32/1 B.B. AVENUE, NARAYANGONJ 0009 11 COURT ROAD BRANCH, 52/1 B.B.ROAD, NARAYANGONJ 0010 12 FARIDPUR BRANCH, CHAWK BAZAR, FARIDPUR 0011 13 WASA BRANCH, KAWRAN BAZAR, DHAKA. 0012 14 TEJGAON INDUSTRIAL AREA BRANCH, 315/A TEJGAON I/A, DHAKA 0013 15 NAWABPUR ROAD BRANCH, 243-244 NAWABPUR ROAD, DHAKA 0014 16 COMMERCIAL AREA BRANCH, 28 AGRABAD C/A, CHITTAGONG 0015 17 ASADGONJ BRANCH, HAJI AMIR ALI CHOWDHURY ROAD, CHITTAGONG 0016 18 LALDIGHI EAST, 1012/1013 - LALDIGHI EAST, CHITTAGONG 0017 19 AGRABAD BRANCH, JAHAN BUILDING, 24 AGRABAD C/A, CTG 0018 20 COX'S BAZAR BRANCH, COX'S BAZAR 0019 21 RAJGANJ BRANCH, RAJGANJ, COMILLA 0020 22 LALDIGHIRPAR BRANCH, LALDIGHIRPAR, SYLHET 0021 23 CHAUMUHANI BRANCH,D.B.ROAD, BEGUMGONJ, CHAUMUHANI, NOAKHALI 0022 24 SIR IQBAL RAOD BRANCH, 25 SIR IQBAL RAOD, KHULNA 0023 25 JESSORE BRANCH, JESS TOWER, JESSORE 0024 26 CHAWK BAZAR BRANCH, 02/01 CHAWK BAZAR, BARISAL 0025 27 BARA BAZAR BRANCH, N.S. -

Useful Information for Shareholders

useful information for shareholders Financial Calendar Particulars Date Twelfth Annual General Meeting April 17, 2008 First Extra-ordinary General Meeting April 17, 2008 Transfer of bonus shares May 07, 2008 Half-yearly Financial Statements (Un-audited) June 30, 2008 Record date for Bonus Shares March 01, 2009 Next half-yearly Financial Statements June 30, 2009 2nd Extra-ordinary General Meeting The 2nd Extra-ordinary General Meeting of the shareholders of the Bank will be held on March 23, 2009 at 10:00 a.m. at the “Hall of Fame” of Bangladesh-China Friendship Conference Center (BCFCC), Agargaon, Dhaka. 13th Annual General Meeting The 13th Annual General Meeting of shareholders of the Bank will be held on March 23,2009 at 10:30 a.m. at the “Hall of Fame” of Bangladesh-China Friendship Conference Center (BCFCC), Agargaon, Dhaka. Information on dividends Bonus share @3.94719 for existing 1 share of Taka 100 each for 2007 were declared in 2008. 50% bonus share i.e. 1 bonus share for existing 2 shares of Taka 100 each is proposed for 2008. Share transfer system The shares of Dutch-Bangla Bank Limited (DBBL) are being traded at the Stock Exchanges in Dematerialized form since June 15, 2004 through Central Depository Bangladesh Limited (CDBL) as per directive of Securities and Exchange Commission (SEC). Physical shares, which are not yet dematerialized, can be dematerialized with CDBL through BO account with Depository Participant (DP). Information relating to shareholdings Distribution of shares of DBBL and shareholdings by the Directors are given in Note 17 to Financial Statements of this Annual Report. -

The Role of Islami Bank Bangladesh Limited in Economic Development of Bangladesh

ISSN: 2308-5096(P) ISSN 2311-620X (O) [International Journal of Ethics in Social Sciences Vol.4, No. 1, June 2016] The Role of Islami Bank Bangladesh Limited in Economic Development of Bangladesh Mohammed Mahbubur Rahaman1 Md. Rafiqul Islam Rafiq2 Abstract The main objective of the study is to analyze the role of IBBL in economic development of Bangladesh and to give some suggestions to overcome the challenges Islami Bank Bangladesh Ltd. (IBBL) is the pioneer of Islamic banking in Bangladesh. IBBL is performing a significant role in the development of the country. The Bank is working in the export sector from the very beginning resulting in maximizing export earnings as well as creating employment opportunities in Bangladesh. The Bank has already emerged as the top export-import bank in Bangladesh. IBBL satisfies most of the efficiency conditions if they can operate as a sole system in an economy. Conventional banking, on the other hand, does not satisfy any of the efficiency conditions analyzed in the present study. However, when Islamic banks start operation within the conventional banking framework, their efficiency goes on decreasing in a number of dimensions. 1. Introduction In a modern economy, banks are the fundamental financial intermediary. Recently they are engaged in value generating activities by assuring uninterrupted supply of financial resources and also help accelerate the pace of development process. In terms of deposit collection, investment, and foreign exchange business the Islami Bank Bangladesh Limited (IBBL) place the position of being the leading other banks, IBBL has been continuously operating their banking activities and to provide efficient banking service with a view to accelerate 1. -

INTERNATIONAL FINANCE INVESTMENT and COMMERCE BANK LIMITED Audited Financial Statements As at and for the Year Ended 31 December 2019

INTERNATIONAL FINANCE INVESTMENT AND COMMERCE BANK LIMITED Audited Financial Statements as at and for the year ended 31 December 2019 INTERNATIONAL FINANCE INVESTMENT AND COMMERCE BANK LIMITED Consolidated Balance Sheet as at 31 December 2019 Amount in BDT Particulars Note 31 December 2019 31 December 2018 PROPERTY AND ASSETS Cash 18,056,029,773 16,020,741,583 Cash in hand (including foreign currency) 3.a 2,872,338,679 2,899,030,289 Balance with Bangladesh Bank and its agent bank(s) (including foreign currency) 3.b 15,183,691,094 13,121,711,294 Balance with other banks and financial institutions 4.a 5,637,834,204 8,118,980,917 In Bangladesh 4.a(i) 4,014,719,294 6,823,590,588 Outside Bangladesh 4.a(ii) 1,623,114,910 1,295,390,329 Money at call and on short notice 5 910,000,000 3,970,000,000 Investments 47,216,443,756 32,664,400,101 Government securities 6.a 41,369,255,890 27,258,506,647 Other investments 6.b 5,847,187,866 5,405,893,454 Loans and advances 232,523,441,067 210,932,291,735 Loans, cash credit, overdrafts etc. 7.a 221,562,693,268 198,670,768,028 Bills purchased and discounted 8.a 10,960,747,799 12,261,523,707 Fixed assets including premises, furniture and fixtures 9.a 6,430,431,620 5,445,835,394 Other assets 10.a 9,606,537,605 9,003,060,522 Non-banking assets 11 373,474,800 373,474,800 Total assets 320,754,192,825 286,528,785,052 LIABILITIES AND CAPITAL Liabilities Borrowing from other banks, financial institutions and agents 12.a 8,215,860,335 9,969,432,278 Subordinated debt 13 2,800,000,000 3,500,000,000 Deposits and other -

Bangladesh Development Bibliography List of Publications from 2000 – 2005 (As of January 16, 2012)

Bangladesh Development Bibliography List of publications from 2000 – 2005 (as of January 16, 2012) Aaby, Peter; Abbas Bhuiya; Lutfun Nahar; Kim Knudsen; Andres de Francisco; and Michael Strong (2003) The survival benefit of measles immunization may not be explained entirely by the prevention of measles disease: a community study from rural Bangladesh ; International Journal of Epidemiology, Vol. 32, No. 1 (February), pp. 106-115. Abbasi, Kamran (2002) Health policy in action: the World Bank in South Asia; Brighton, UK: University of Sussex, Institute of Development Studies (IDS). Abdalla, Amr; A. N. M. Raisuddin; and Suleiman Hussein with the assistance of Dhaka Ahsania Mission (2004) Bangladesh Educational Assessment - Pre-primary and Primary Madrasah Education in Bangladesh ; Washington, DC, USA: United States Agency for International Development (USAID) for Basic Education and Policy Support (BEPS) Activity (Contract No. HNE-I-00-00-00038-00) (June). Abdullah, Abu (2001) The Bangladesh Economy in the Year 2000: Achievements and Failures; In: Abu Abdullah (ed.) Bangladesh Economy 2000: Selected issues (Dhaka: Bangladesh Institute of Development Studies (BIDS)), pp. xv-xxix. Abdullah, Abu (ed.) (2001) Bangladesh Economy 2000: Selected Issues; Dhaka, Bangladesh: University Press Ltd. and Bangladesh Institute of Development Studies. Abdullah, Abu A. (2000) Social Change and ‘Modernisation‘; In: Rounaq Jahan (ed.) Bangladesh: Promise and Performance (London, UK: Zed Books; and Dhaka, Bangladesh: The University Press), Chapter 5. Abdullah, Mohammad (ed.) (2004) Technologies on Livestock and Fisheries for Poverty Alleviation in SAARC Countries; Dhaka, Bangladesh: SAARC Agricultural Information Centre (SAIC). Abdullah, S. T.; Mullineux, A. W.; Fielding, A.; and W. Spanjers (2004) Intra-household resource allocation and bargaining power of the women using micro-credit in Bangladesh; Birmingham, UK: University of Birmingham, Department of Economics Discussion Paper, No. -

Dutch-Bangla Bank Limited Balance Sheet As at 31 March 2016 (Main Operation and Off-Shore Banking Unit)

Dutch-Bangla Bank Limited Balance Sheet As at 31 March 2016 (Main Operation and Off-shore Banking Unit) PROPERTY AND ASSETS Notes 31-Mar-16 31-Dec-15 31-Mar-15 Taka (Un-audited) Taka (Audited) Taka (Un-audited) Main Operation Off-shore Total Total Total Cash In hand (including foreign currencies) 4 8,687,307,386 - 8,687,307,386 8,296,998,632 7,020,803,945 Balance with Bangladesh Bank and its agent bank (s) (including foreign currencies) 5 17,414,308,363 - 17,414,308,363 14,555,926,865 15,178,783,055 26,101,615,749 - 26,101,615,749 22,852,925,497 22,199,587,000 Balance with other banks and financial institutions 6 In Bangladesh 23,883,193,400 2,052,052,493 25,935,245,893 27,591,599,177 13,010,752,944 Outside Bangladesh 804,409,204 - 804,409,204 1,154,177,150 1,840,924,301 24,687,602,604 2,052,052,493 26,739,655,097 28,745,776,327 14,851,677,245 Money at call and short notice 7 1,980,000,000 - 1,980,000,000 5,270,000,000 1,100,000,000 Investments 8 Government 19,187,552,263 - 19,187,552,263 19,405,280,474 25,193,823,649 Others 564,983,434 - 564,983,434 804,983,434 885,283,434 19,752,535,697 - 19,752,535,697 20,210,263,908 26,079,107,083 Loans and advances 9 Loans, cash credits, overdrafts, etc. -

Agent Banking, the Revolution in Financial Service Sector of Bangladesh

IOSR Journal of Economics and Finance (IOSR-JEF) e-ISSN: 2321-5933, p-ISSN: 2321-5925.Volume 5, Issue 1. (Jul-Aug. 2014), PP 28-32 www.iosrjournals.org Agent banking, the revolution in financial service sector of Bangladesh Md. Razib Siddiquie (Department of Business Administration, University of Asia Pacific, Bangladesh) Abstract: Agent banking is one of the most popular financial services in the world where there are difficulties in accessing geographical locations easily. And that is why agent banking is very successful in Latin America & Africa. Other developed like United Kingdom, Australia etc countries are also gradually deploying agent banking because it reduces the cost of operating of the bank. Most of the services of a bank can be provided through agents, thus people of remotest area of a country can be brought under proper financial structure by the virtue of agent banking. According to the agent banking guideline the software of any individual agent will be connected to the core software of the bank, so transactions that will take place in agent premises will be shown in the banking system real-time and those transactional statements can be used anywhere and everywhere for different purposes of the client. I have done my research on agent banking and its prospect for last one year and finally prepared this paper. Keywords: Alternative Banking, Internet service provider, Bank, Regulation, vision I. Introduction of Agent banking in Bangladesh: People's Republic of Bangladesh, a delta in South Asia, Bangladesh shares large borders with India and a small southern strip with Myanmar. Bangladesh is home to the Ganges, the Brahmaputra and the Meghna rivers, and networks of smaller rivers and canals. -

Sl. Correspondent / Bank Name SWIFT Code Country

International Division Relationship Management Application( RMA ) Total Correspondent: 156 No. of Country: 36 Sl. Correspondent / Bank Name SWIFT Code Country 1 ISLAMIC BANK OF AFGHANISTAN IBAFAFAKA AFGHANISTAN 2 MIZUHO BANK, LTD. SYDNEY BRANCH MHCBAU2S AUSTRALIA 3 STATE BANK OF INDIA AUSTRALIA SBINAU2S AUSTRALIA 4 KEB HANA BANK, BAHRAIN BRANCH KOEXBHBM BAHRAIN 5 MASHREQ BANK BOMLBHBM BAHRAIN 6 NATIONAL BANK OF PAKISTAN NBPABHBM BAHRAIN 7 AB BANK LIMITED ABBLBDDH BANGLADESH 8 AGRANI BANK LIMITED AGBKBDDH BANGLADESH 9 AL-ARAFAH ISLAMI BANK LTD. ALARBDDH BANGLADESH 10 BANGLADESH BANK BBHOBDDH BANGLADESH 11 BANGLADESH COMMERCE BANK LIMITED BCBLBDDH BANGLADESH BANGLADESH DEVELOPMENT BANK 12 BDDBBDDH BANGLADESH LIMITED (BDBL) 13 BANGLADESH KRISHI BANK BKBABDDH BANGLADESH 14 BANK ASIA LIMITED BALBBDDH BANGLADESH 15 BASIC BANK LIMITED BKSIBDDH BANGLADESH 16 BRAC BANK LIMITED BRAKBDDH BANGLADESH 17 COMMERCIAL BANK OF CEYLON LTD. CCEYBDDH BANGLADESH 18 DHAKA BANK LIMITED DHBLBDDH BANGLADESH 19 DUTCH BANGLA BANK LIMITED DBBLBDDH BANGLADESH 20 EASTERN BANK LIMITED EBLDBDDH BANGLADESH EXPORT IMPORT BANK OF BANGLADESH 21 EXBKBDDH BANGLADESH LTD 22 FIRST SECURITY ISLAMI BANK LIMITED FSEBBDDH BANGLADESH 23 HABIB BANK LTD HABBBDDH BANGLADESH 24 ICB ISLAMI BANK LIMITED BBSHBDDH BANGLADESH INTERNATIONAL FINANCE INVESTMENT 25 IFICBDDH BANGLADESH AND COMMERCE BANK LTD (IFIC BANK) 26 ISLAMI BANK LIMITED IBBLBDDH BANGLADESH 27 JAMUNA BANK LIMITED JAMUBDDH BANGLADESH 28 JANATA BANK LIMITED JANBBDDH BANGLADESH 29 MEGHNA BANK LIMITED MGBLBDDH BANGLADESH 30 MERCANTILE -

AGRANI BANK LIMITED Notes to the Financial Statements As at and for the Year Ended December 31, 2011

ACNABIN Howladar Yunus & Co. Chartered Accountants Chartered Accountants AGRANI BANK LIMITED Notes to the Financial Statements As at and for the year ended December 31, 2011 1. BACKGROUND INFORMATION 1.1 Establishment and status of the Bank Agrani Bank Limited (the Bank) has been incorporated as a Public Limited Company on May 17, 2007 Vide Certificate of Incorporation # C-66888(4380)/07. The Bank has taken over the business of Agrani Bank (emerged as a Nationalized Commercial Bank in 1972, pursuant to Bangladesh Bank (Nationalization) Order # 1972 (P.O. # 26 of 1972)) on a going concern basis through a Vendor Agreement signed between the Ministry of Finance of the People’s Republic of Bangladesh on behalf of Agrani Bank and the Board of Directors on behalf of Agrani Bank Limited on November 15, 2007 with a retrospective effect from July 01, 2007. The Bank’s current shareholdings comprise Government of the People’s Republic of Bangladesh and other 12 (Twelve) shareholders nominated by the Government. The Bank has 876 branches as on December 31, 2011. The Bank has four wholly-owned subsidiary Companies named (a) Agrani Exchange House (Pvt.) Ltd. in Singapore, (b) Agrani Remittance House SDN, BHD in Malaysia, (c) Agrani Equity and Investment Limited and (d) Agrani SME Financing Company Limited. 1.2 Nature of business The principal activities of the Bank are providing all kinds of commercial banking services to it’s customers and the principal activities of it’s subsidiaries are: a) To carry on the remittance business and to undertake and participate in any or all transactions, and operations commonly carried or undertaken by remittance and exchange houses established in Singapore and Malaysia. -

Procedure of Open Foreign Currency Account.Pdf

Embassy of Bangladesh Washington DC Wage Earner Development Bond Foreign Currency Foreign Currency Accounts Specimern Signature Specimern Signature FC Account Opening Form and Specimen Signature Extension [email protected] Diplomatic Bag /DHL/Fedex English Version The Government of the People’s Republic of Bangladesh have introduced special saving facilities for Non Resident Bangladeshis and also foreigner’s of Bangladeshi decent. Wage Earner Development Bond : Most profitable fixed deposit investment “Wage Earner Development Bond” for Non Resident Bangladeshi’s and Foreigners of Bangladeshi decent introduced by the Government of the People’s Republic of Bangladesh. Compound rate of profit is 12.00% per annum. Tk. 25,000 become Tk. 44,750 with profit after 5 years Tk. 50,000 become Tk. 89,500 with profit after 5 years Tk. 1,00,000 become Tk. 1,79,000 with profit after 5 years Tk. 5,00,000 become Tk. 8,95,000 with profit after 5 years Profits could be withdrawn at a rate of Tk. 1000.00 per month for every Tk. 100000.00. For withdrawal of profit simple rate is applicable. Nominee is entitled to 30% to 50% of invested amount as a death risk insurance at no extra charge in case of death of the bond owner. No income tax is levied on the initial investment or profits thereof. Initial investment amount could be transferred back in foreign currency. If encashed before maturity you will get interest at following rate : a. Before six month no interest b. After six month and before 1 year : 9% c. After 1 year and before 2 years : 10% d. -

Comparison and Analysis of Profitability of Top Three

Global Journal of Management and Business Research: C Finance Volume 19 Issue 3 Version 1.0 Year 2019 Type: Double Blind Peer Reviewed International Research Journal Publisher: Global Journals Online ISSN: 2249-4588 & Print ISSN: 0975-5853 Comparison and Analysis of Profitability of Top Three Nationalized Commercial Banks in Bangladesh By Saeed Sazzad Jeris Abstract- Banks are playing a vital role in the economic & financial development of Bangladesh. Profitability indicates the overall performance of the banks. In this study, it has been tried to compare the top three nationalized commercial banks by some financial parameters, and it relies on secondary sources of data. In this paper, I used statistical tool ANOVA for comparison. The result indicates the statistical difference among these banks and their performance is not stable. Keywords: bank, profitability, performance, ANOVA. GJMBR-C Classification: JEL Code: G21 ComparisonandAnalysisofProfitabilityofTopThreeNationalizedCommercialBanksinBangladesh Strictly as per the compliance and regulations of: © 2019. Saeed Sazzad Jeris. This is a research/review paper, distributed under the terms of the Creative Commons Attribution- Noncommercial 3.0 Unported License http://creativecommons.org/licenses/by-nc/3.0/), permitting all non-commercial use, distribution, and reproduction in any medium, provided the original work is properly cited. Comparison and Analysis of Profitability of Top Three Nationalized Commercial Banks in Bangladesh Saeed Sazzad Jeris Abstract- Banks are playing a vital role in the economic & III. Hypothesis financial development of Bangladesh. Profitability indicates the overall performance of the banks. In this study, it has been 1 2019 0 = There is an insignificant difference among Sonali tried to compare the top three nationalized commercial banks bank, Janata bank, and Agrani bank by on net worth. -

A Framework on Internet Banking Services for the Rationalized Generations

Asian Business Review, Volume 3, Number 2/2013 (Issue 6) ISSN 2304-2613 (Print); ISSN 2305-8730 (Online) 0 A Framework on Internet Banking Services for the Rationalized Generations Md. Rahimullah Miah Lecturer in MIS, Leading University, Sylhet, Bangladesh ABSTRACT The augmented Internet Banking Service is increasingly popular both in Bangladesh and elsewhere. This paper explores a predicted framework for global Internet Banking that emphasizes the transformative interaction among the effective customers around the regional, national and global banking indicating advanced on backend models, instructional strategies, and transaction technologies in the context on upcoming generations. We have to develop the framework on global enhanced transaction systems especially individual global account, effective online banking systems to fulfill the required method, implementing design and appraising the feedback with standard technology according to network topology for disseminating of global banking technological arena. Despite decades of development, electronic payments still need practical examples of how to use electronic payment technology within a uniqueness and rationalized way including global electronic transaction, language tools, currency converter and electronic workstation. This research focuses the major issues responsible for Internet Banking based on respondents’ perception through various internet applications. The author presents a theoretical framework for our represented method, taking into account previous models and characteristics