Emerging Trends in Real Estate® 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Midvale City Council Meeting Agenda April 6, 2021

7505 South Holden Street Midvale, UT 84047 (801) 567-7200 www.midvalecity.org MIDVALE CITY COUNCIL MEETING AGENDA APRIL 6, 2021 PUBLIC NOTICE IS HEREBY GIVEN that the Midvale City Council will hold a meeting on the 6th day of April 2021 as follows: Electronic & In-Person City Council Meeting This meeting will be held electronically and in-person. Those choosing to attend the meeting in person will be required to wear a face mask (covering their mouth and nose) and practice social distancing. The City seeks to provide safe options for the public to participate in-person and electronically that comply with state and local regulations, as well as common sense. The meeting will be broadcast on the following: You Tube: www.MidvaleCity.org/YouTube If you would like to provide public comments electronically, please email your comments to [email protected] prior to the completion of the public comments portion of the meeting. You may also submit comments if the Mayor and City Council open a specific agenda item to public comment. These comments will be read aloud in the meeting and will be part of the public record. When commenting, please: • Limit your comments to 400 words (the equivalent of 3 minutes) • Include your first and last name • Include your city of residence (optional) • Include the name of the Agenda item 6:00 PM – WORKSHOP • Discuss Residential Planned Unit Developments [Alex Murphy, Planning Director] • Discuss FY 2022 Budget [Kyle Maurer, Administrative Services Director] 7:00 PM - REGULAR MEETING I. GENERAL BUSINESS A. WELCOME AND PLEDGE OF ALLEGIANCE B. -

JOB TITLE: Carpenter LOCATION: State College, PA COMPANY

JOB TITLE: Carpenter LOCATION: State College, PA COMPANY: Envinity is an energy conservation, efficiency and generation company that is rooted in the building science approach to green design, construction and energy management. Envinity’s Design and Construction group is seeking an experienced Carpenter to contribute to the group’s growth and service offerings. JOB SUMMARY: Envinity’s Residential Design + Build group focuses on creating high performance, energy efficient homes. Other important aspects of our work include the design and construction of home additions, custom woodworking, and other home improvements utilizing local resources and high performance building methods. Envinity has designed and constructed a wide range of energy savings projects from ENERGY STAR and Zero Energy Ready Homes rated new home construction to mechanical systems, home performance upgrades and alternative energy systems. To support and grow these efforts, Envinity is seeking a Carpenter with at least two years experience performing carpentry tasks. Qualified candidates should be versed in construction techniques, knowledge on how to safely use a wide variety of tools, experience in home construction and renovation projects, and a desire to improve your skills while working under some of the best carpenters in Centre County. This position requires some knowledge of building science and system interactions, strong communication skills, strong organizational skills, and a desire to make people’s homes more energy efficient. This position is primarily field-based performing all phases of carpentry and homebuilding on construction projects. JOB TASKS Perform basic rough and finish carpentry tasks. Read and interpret construction drawings and details. Understanding of home performance details such as air sealing and insulation techniques. -

Community Profile November 2017

COMMUNITY PROFILE NOVEMBER 2017 Acknowledgements Coming soon..... Table of Contents 1. Introduction..............................................1 2. The People of the Alisal..........................7 3. Land Use and Housing.........................15 4. Community Character.........................25 5. Quality of Life........................................51 6. Health......................................................57 7. Economic Development.......................71 8. Infrastructure and Mobility.................81 This page was intentionally left blank. CHAPTER 1: INTRODUCTION chapter one INTRODUCTION ALISAL VIBRANCY PLAN: COMMUNITY PROFILE 1 The Alisal Vibrancy Plan Plan Overview City was drafting its Downtown Vibrancy Plan What We Want to and Economic Development Element in 2013. The Alisal community and the City of Salinas are Through relationship building and partnerships Achieve undertaking an exciting planning process. Since with residents, other community groups, City 2013, residents and community organizers have staff, and elected officials, City Council allocated • Create a road map to a healthy and advocated for a community-driven plan to ensure the initial funding for a plan for the Alisal. environmentally sustainable Salinas for all residents a bright future for East Salinas. Through the Plan, the Alisal community will generate their vision for a thriving, safe, and • Confirm the community’s vision for the The Alisal is an eastern neighborhood in the future City of Salinas, generally bounded by Highway sustainable future, and strategies for getting 101 to the southwest, Madeira Avenue and St there. • Commit additional resources in areas of historic disinvestment that are in alignment Augustine Drive to the northwest, E Alisal Street Community participation and empowerment to the southeast, and Freedom Parkway to the with the community’s goals to ensure social are critical to ensure the Plan is responsive to equity northeast. -

Estimating Parking Utilization in Multi-Family Residential Buildings in Washington, D.C

1 Estimating Parking Utilization in Multi-Family Residential Buildings in Washington, D.C. 2 3 Jonathan Rogers 4 Corresponding Author 5 District Department of Transportation 6 55 M Street SE 7 Washington, DC 20003 8 Tel: 202-671-3022; Fax: 202-671-0617; Email: [email protected] 9 10 Dan Emerine 11 D.C. Office of Planning 12 1100 4th Street SW, Suite E560 13 Washington, DC 20024 14 Tel: 202-442-8812; Fax: 202-442-7638 ; Email: [email protected] 15 16 Peter Haas 17 Center for Neighborhood Technology 18 2125 W. North Ave. 19 Chicago, Il 60647 20 Tel.: 773-269-4034; Fax: 773-278-3840; Email: [email protected] 21 22 David Jackson 23 Cambridge Systematics, Inc. 24 4800 Hampden Lane, Suite 800 25 Bethesda, MD 20901 26 Tel: 301-347-9108; Fax: 301-347-0101; Email: [email protected] 27 28 Peter Kauffmann 29 Gorove/Slade Associates, Inc. 30 1140 Connecticut Avenue, NW, Suite 600 31 Washington, DC 20036 32 Tel: 202-296-8625; Fax: 202-785-1276; Email: [email protected] 33 34 Rick Rybeck 35 Just Economics, LLC 36 1669 Columbia Rd., NW, Suite 116 37 Washington, DC 20009 38 Tel: 202-439-4176; Fax: 202-265-1288; Email: [email protected] 39 40 Ryan Westrom 41 District Department of Transportation 42 55 M Street SE 43 Washington, DC 20003 44 Tel: 202-671-2041; Fax: 202-671-0617; Email: [email protected] 45 46 Word count: 5,468 words text + 8 tables/figures x 250 words (each) = 7,468 words 1 Submission Date: November 13, 2015 1 ABSTRACT 2 The District Department of Transportation and the District of Columbia Office of Planning 3 recently led a research effort to understand how parking utilization in multi-family residential 4 buildings is related to neighborhood and building characteristics. -

Fair Housing Information Brochure

Fair Housing Information (Includes Landlord-Tenant Information) Prepared by Housing Development Division 2014 Contents Introduction ........................................................................................ 1 Section I - Fair Housing .................................................................... 2 What Fair Housing Laws Apply in Colorado? ...................................... 2 Fair Housing Act .................................................................................. 2 Colorado Anti-Discrimination Act of 1957, Housing Practices: ............ 2 What Housing Is Covered?.................................................................. 2 What Is Prohibited? ............................................................................. 2 If You Have a Disability ........................................................................ 3 Where Do You Go For Help? ............................................................... 4 Mortgage Lending................................................................................ 5 Predatory Lending ............................................................................... 5 What is Predatory Lending? ................................................................ 6 What Tactics Do Predators Use? ......................................................... 6 11 Tips on Being a Smart Consumer ................................................... 7 Section II – Landlord /Tenant Rights Information ........................... 9 Application Process ............................................................................ -

Predicting Long-Term Trends & Market Cycles in Commercial Real Estate

PREDICTING LONG-TERM TRENDS & MARKET CYCLES IN COMMERCIAL REAL ESTATE by Glenn R. Mueller Working Paper #388 10/24/01 Land, together with labor and capital, is one of the three major factors of production. As population grows, additional people need places to work, sleep, eat, shop and be entertained. Historically the supply of buildings to meet these needs has been “lumpy,” with too little space available during times of rapid growth and too much supply when growth slows This lag between demand growth and supply response is the major cause of volatility in real estate market cycles. Real estate cycles can be separated into four distinct phases based upon the rate of change in both demand and supply. Figure 1 depicts the market cycle in terms of occupancy rates. Occupancy is the difference between total supply (including newly constructed space) and effective demand as measured by absorption. Markets are defined as having two up-cycles (recovery and expansion) when demand growth rates are higher than supply growth rates, and two down-cycles (hypersupply and recession) when demand Figure 1 1 Phase 2 - Expansion M ar ket Cycle Quadr ants Long Term Occupancy Average Occupancy Demand/Supply Equilibrium Point D eclining Vacancy Phase 3 - Hypersupply Declining Vacancy No New N Phase 1 - Recovery Construct New Construction e ion w C I V n o a c n c r s a t e r nc a u s growth rates are lower than supply growth rates. In reality, markets always have either c i y t ng i o M n demand growing faster than supply or supply growing faster than demand. -

The Postwar Pattern of Mortgage Interest Rates

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: The Postwar Residential Mortgage Market Volume Author/Editor: Saul B. Klaman Volume Publisher: Princeton University Press Volume ISBN: 0-870-14106-6 Volume URL: http://www.nber.org/books/klam61-1 Publication Date: 1961 Chapter Title: The Postwar Pattern of Mortgage Interest Rates Chapter Author: Saul B. Klaman Chapter URL: http://www.nber.org/chapters/c2341 Chapter pages in book: (p. 74 - 98) CHAPTER 4 The Postwar Pattern of Mortgage Interest Rates THE course of mortgage interest rates and its relationship to the flow of mortgage funds are referred to in most chapters of this report. Separate treatment is given here to that subject, so fundamentally important to an understanding of postwar market developments. The influence of shifting market forces on mortgage flows has often been transmitted through changes in mortgage interest rates and yields and in their relationship to yields of other capital market securities.'Little current information on these points has been available, and obtaining data is difficult because of the complexities of interrelationships between mortgage interest rates, other mortgage terms, and the demand and supply of mortgage funds. Obviously, such gaps in our knowledge of this important area- cannot be filled by what follows. We may hope that a future broad-scaled study of interest rates, as suggested by the National Bureau, will include the mortgage field. Meanwhile, a beginning is made here by presentation of new data on conventional mortgage interest rates, by examination of the effects of discounts on FHA and VA loans, and by analysis of the relationship of changes in mortgage yields to changes in the flow of mortgage funds. -

Real Estate Agents Will Lose Value As Digital Peer-To-Peer Exchange Platforms Couple Exponentially with Technological Advancements by Cusumano, L

Real Estate Agents Will Lose Value as Digital Peer-to-Peer Exchange Platforms Couple Exponentially with Technological Advancements by Cusumano, L. A Thesis Submitted to REALTOR® University In Partial Fulfillment for the Degree of Master of Real Estate Professor, Dr. Sullivan April 24, 2017 Abstract As technology collides with disruptive innovation, residential buyers and sellers will no longer want or need some or all services offered by a traditional real estate brokerage. Consumers are frequently becoming self-serving as they can now find a vast amount of housing information and apps through their mobile devices. Today’s consumers are more cognizant of the fact that many brokerages throughout the US are now limiting their liabilities to protect their own company and maximize their profits through earning both sides of the commission thus eliminating undivided loyalty, protection, and full representation to the consumer. Furthermore, tech savvy buyers and sellers have watched numerous home programs and videos, have easy access to MLS and many other real estate websites, and will continually seek out money saving solutions while buying and selling their home. Like Uber and Airbnb, digital peer to peer exchange platforms coupled with built in algorithms and artificial intelligence will gain allegiance among future home buyers and sellers, thus creating new real estate models and fewer agents in the industry. Keywords: algorithms, artificial intelligence, augmented reality, autonomous vehicles, buyer agent, designated agency, drones, dual agency, exclusive buyer agent, facilitator, FSBO, for sale by owner, listing agent, peer-to-peer, transaction brokerage, single agent, Uber, virtual reality, wearable technology. i Table of Contents Abstract. -

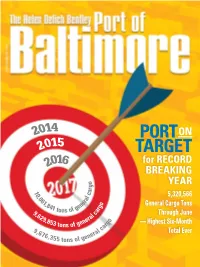

Porton Target

2014 PORT ON 2015 TARGET 2016 for RECORD BREAKING o YEAR g r 1 a 0 c 5,320,566 ,0 l 61 ra , e o General Cargo Tons 84 n g 1 t f ge r 9 ons o a Through June ,6 l c 29 ra ,85 ne o — Highest Six-Month 3 tons of ge rg ca 9,6 al Total Ever 76 ner ,355 tons of ge Celebrating 100 Years! Our Foundation’s Legacy is Always With Us: Uncommon Dedication and Integrity John S. Connor 1890-1940 Husband, Father, Friend, Merchant Founder, 1917: John S. Connor, Inc Frank Burkhardt BalTerm employee for 11 years One of our most important assets. Cleanliness, and the employees who keep it but its that kind of attention to detail that puts that way. Partner with the company BalTerm in a class by itself. Our that’s cleaning up when it comes warehouse floors are as polished to forest products warehousing, as our reputation. And if our floors stevedoring and cargo handling. BALTIMORE FOREST PRODUCTS TERMINALSget this much attention, imagine Of course, some might consider us the attention we give to everything a bit obsessive about keeping our else. At BalTerm, our assets are warehouses and equipment clean, your assets�. BALTIMORE FOREST PRODUCTS TERMINALS www.BalTerm.com South Locust Point Marine Terminal 2001 East McComas St. Baltimore, MD 21230 410.752.9981 BALTIMORE FOREST PRODUCTS TERMINALS ™ MARYLAND DEPARTMENT OF TRANSPORTATION’S MARYLAND PORT ADMINISTRATION World Trade Center Baltimore, 401 E. Pratt St. Baltimore, MD 21202 | Toll Free 1-800-638-7519 GOVERNOR LIEUTENANT Larry Hogan GOVERNOR Executive Director General Manager of Intermodal / Boyd Rutherford James J. -

Emerging Trends in Real Estate®

FRANCIS ZERA FRANCIS Emerging Trends in Real Estate® United States and Canada 2018 Emerging Trends in Real Estate® 2018 A publication from: Emerging Trends in Real Estate® 2018 Contents 1 Notice to Readers 71 Chapter 4 Property Type Outlook 72 Industrial 3 Chapter 1 Navigating at Altitude 76 Apartments 4 Long Glide Path to a Soft Landing 80 Single-Family Homes 6 Working Smarter and Working Harder 83 Office 9 Procession of the Generations 87 Hotels 10 But Don’t Forget the Baby Boomers 89 Retail 11 It’s Different This Time . Isn’t It? 13 Housing at a Technological Tipping Point? 93 Chapter 5 Emerging Trends in Canadian 15 Retail Transforms and Stores Remain Real Estate 16 Tax Reform: It’s Going to Take Some Time 93 Rebalancing Portfolios to Create Advantage This Time 94 Rethinking How to Address Affordability 17 Replacing the Yardstick 96 Transit to Transform Cities 19 Staying on the Radar 97 The Rise of Placemaking 21 Expected Best Bets for 2018 97 Making the 18-Hour City a Canadian Reality 97 Reinventing Real Estate through Technology 23 Chapter 2 Capital Markets 99 The Global War for Talent 24 The Debt Sector 99 Property Type Outlook 29 The Equity Sector 105 Markets to Watch in 2018 35 Summary 109 Expected Best Bets for 2018 36 Chapter 3 Markets to Watch 110 Interviewees 36 2018 Market Rankings 37 Market Summaries Emerging Trends in Real Estate® 2018 i Editorial Leadership Team Emerging Trends Chairs PwC Advisers and Contributing Researchers Mitchell M. Roschelle, PwC Aakriti Sondhi* Haley Anderson Nicholas Mitchell Patrick L. -

Ontario Quiz

Ontario Quiz Try our Ontario Quiz & see how well you know Ontario. Answers appear at the bottom. 1. On Ontario’s Coat of Arms, what animal stands on a gold and green wreath? A) Beaver B) Owl C) Moose D) Black Bear 2. On Ontario’s Coat of Arms, the Latin motto translates as: A) Loyal she began, loyal she remains B) Always faithful, always true C) Second to none D) Liberty, Freedom, Truth 3. Which premier proposed that Ontario would have its own flag, and that it would be like the previous Canadian flag? A) Frost B) Robarts C) Davis D) Rae 4. Ontario’s Progressive Conservative government under right wing leader Mike Harris espoused what kind of revolution? A) Law and order B) Tax deductions C) People first D) Common sense 5. Which of the following was not an Ontario Liberal leader? A) Jim Bradley B) Robert Nixon C) Mitch Hepburn D) Cecil Rhodes 6. Which of the following is not a recognized political party in Ontario? A) White Rose B) Communist C) Family Coalition D) Libertarian 7. Tim Hudak, leader of Ontario’s PC party is from where? A) Crystal Beach B) Fort Erie C) Welland D) Port Colborne 8. Former Ontario Liberal leader, Dalton McGuinty was born where? A) Toronto B) Halifax C) Calgary D) Ottawa 9. The first Ontario Provincial Police detachment was located where? A) Timmins B) Cobalt C) Toronto D) Bala 10. The head of the OPP is called what? A) Commissioner B) Chief C) Superintendent D) Chief Superintendent 11. Which of the following was not a Lieutenant Governor of Ontario? A) Hillary Weston B) John Aird C) Roland Michener D) William Rowe 12. -

Commercial Occupancy Agreement

2615 Park Avenue Associates Cooperative Commercial Occupancy Agreement Table of Contents ARTICLE 1 Monthly Assessments ..............................................................................................2 ARTICLE 2 When Payment of Assessments Commence ..........................................................4 ARTICLE 3 Patronage Refund ....................................................................................................4 ARTICLE 4 Shareholder’s Option for Automatic Renewal......................................................4 ARTICLE 5 Commercial Units for Commercial use Only .......................................................5 ARTICLE 6 Shareholder’s Right to Peaceable Possession ........................................................5 ARTICLE 7 No Subleasing Without the Cooperative’s Consent ..............................................5 ARTICLE 8 Transfers ..................................................................................................................6 ARTICLE 9 Management, Taxes and Insurances ......................................................................6 ARTICLE 10 Utilities ....................................................................................................................7 ARTICLE 11 Repair, Maintenance and Replacement Obligations ..........................................8 ARTICLE 12 Alterations and Additions ...................................................................................10 ARTICLE 13 Definition and Effect of Shareholder’s Default.................................................11