Reliance on Comfort

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

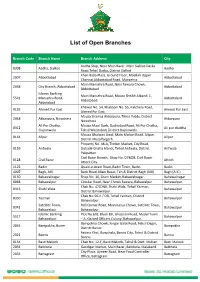

List of Open Branches

List of Open Branches Branch Code Branch Name Branch Address City Aadha Stop, Near Main Bazar, Main Sialkot-Daska 0308 Aadha, Sialkot Aadha Road,Tehsil Daska, District Sialkot Khan Baba Plaza, Ground Floor, Moallah Upper 2007 Abbottabad Abbottabad Channai,Abbottabad Road, Mansehra. Main Mansehra Road, Near Fawara Chowk, 2038 City Branch, Abbottabad Abbottabad Abbottabad Islamic Banking Main Mansehra Road, Mouza Sheikh Albandi 1, 5541 Mansehra Road, Abbottabad Abbotabad. Abbotabad Khewat No. 54, Khatooni No. 55, Katchery Road, 0193 Ahmed Pur East Ahmed Pur East Ahmed Pur East. Mauza Shamsa Akbarpura, Tehsil Pabbi, District 2048 Akbarpura, Nowshera Akbarpura Nowshera Ali Pur Chatha, Mauza Akaal Garh, Qadirabad Road, Ali Pur Chatha, 0312 Ali pur chattha Gujranwala Tehsil Wazirabad, District Gujranwala. Mouza Ghalwan Awal, Main Multan Road, Alipur, 0164 Alipur Alipur District Muzaffargarh. Property No. 48-A, Timber Market, City Road, 0159 Arifwala Outside Ghalla Mandi, Tehsil Arifwala, District Arifwala Pakpattan. Civil Bazar Branch, Shop No. D7&D8, Civil Bazar 0128 Civil Bazar Attock Attock City. 1122 Badin Quaid-e-Azam Road, Badin Town, Badin. Badin 4007 Bagh, AJK Bank Road, Main Bazar, Teh & District Bagh (AJK) Bagh (A.K.) 0150 Bahawalnagar Shop No. 10, Grain Market, Bahawalnagar. Bahawalnagar 0068 Bahawalpur Circular Road, Near Chowk Fawara, Bahawalpur Bahawalpur Chak No. 47/DNB, Shahi Wala, Tehsil Yazman, 0315 Shahi Wala Bahawalpur District Bahawalpur. Chak No.56-A / DB, Tehsil Yazman, District 0330 Yazman Bahawalpur Bahawalpur. Satellite Town, Rafi Qamar Road, Main Kanju Chowk, Satellite Town, 0341 Bahawalpur Bahawalpur Bahawalpur. Islamic Banking Plot No.6/B, Block B/I, Ghaznavi Road, Model Town 5517 Bahawalpur Bahawalpur – A, Gazted Officers Colony, Bahawalpur. -

(Winner)MCB Bank Limited Best Bank of the Year 2017 – Mid Size Banks

Banking: Best Bank of the year 2017 – Large Size Banks (Winner)MCB Bank Limited Best Bank of the year 2017 – Mid Size Banks (Winner) Bank Al Habib Limited Best Bank of the year 2017 – Small Size Banks Industrial and Commercial Bank of China (Winner) Limited Best Islamic Window of the year 2017 (Winner) Habib Bank Limited Best Islamic Bank of the year 2017 (Winner) Meezan Bank Limited Corporate Finance: Transaction of the year 2017 (Winner) Habib Bank Limited for Dasu Hydropower Project Best Corporate Finance House of the year (Fixed Income) 2017 United Bank Limited (Winner) Best Corporate Finance House of the year (Fixed Income) 2017Habib Bank Limited (Runner-up) Best Corporate Finance House of the year (Equity & Advisory) - Banks Bank Alfalah Limited 2017 (Winner) Best Corporate Finance House of the year (Equity & Advisory) - Banks United Bank Limited 2017 (Runner-up) Best Corporate Finance House of the year (Equity & Advisory) – Arif Habib Limited Security Firms 2017 (Winner) Best Corporate Finance House of the year (Equity & Advisory) – AKD Securities Limited Security Firms 2017 (Runner-up) Investor Relations: Best Investor Relations – Listed Companies 2017 (Winner) Bank Alfalah Limited Best Investor Relations – Listed Companies 2017 (Runner-up) Engro Fertilizers Limited Women in Finance Initiative: Gender Diversity at Workplace Award 2017 (Winner) Unilever Pakistan Limited Recognizing Gender Diversity Award – Special Recognition: Local National Foods Limited Industry 2017 (Winner) Recognizing Gender Diversity Award – Special Recognition: -

COMPARATIVE ANALYSIS of FINANCIAL PERFORMANCE and GROWTH of CONVENTIONAL and ISLAMIC BANKS of PAKISTAN Ishtiaq Khan, Sarhad University of Science & IT, Peshawar

COMPARATIVE ANALYSIS OF FINANCIAL PERFORMANCE AND GROWTH OF CONVENTIONAL AND ISLAMIC BANKS OF PAKISTAN Ishtiaq Khan, Sarhad University of Science & IT, Peshawar. Email: [email protected] Wali Rahman, Associate Professor, Sarhad University of Science & IT, Peshawar. Email: [email protected] Saeedullah Jan, Khushal Khan Khattak University, Karak. Email: [email protected] Mustaq Khan, Abasyn University of Science & IT, Peshawar Email: [email protected] Abstract. Various types of the banking system are operating in the world. The most commons are conventional and Islamic. Customers evaluate these systems before they decide in invest. The prime aim of this study is to assess and compare the financial performance and growth of conventional and Islamic banks operating in Pakistan. Banks offer different types of products and services for the satisfaction of customers for their financial needs. Conventional banking is based on interest while Islamic banking offers interest-free banking. To compare their respective performance financial ratios are applied. In Pakistan, Habib Bank Limited and Allied Bank Limited are typical examples of the conventional banking whereas Dubai Islamic Bank Limited and Meezan Bank Limited are operating as Islamic banking. Three (03) years data were obtained from the “Financial Statement Analysis of Financial Sector of Pakistan 2009-2011” State Bank of Pakistan publication. The analyses reflect that the liquidity ratio of Islamic banks appeared higher as compared to conventional banks, whereas the profitability and solvency ratios of conventional banks were comparatively higher than Islamic banks. Debt to asset ratio of Islamic banks seemed better than conventional banks due to low debt financing. Also, with regard to expansion, the growth rate of Islamic banks in Pakistan is comparatively higher than conventional banks. -

ANNUAL REPORT 2008 the Management Team Is Also Being Trained on Various Basel II Requirements

Contents Corporate Information......................................................................01 Director’s Report to the Shareholders........................................02 Statement of Compliance with the Code of Corporate Governance.......................................................07 Statement of Internal Control........................................................09 Notice of Annual General Meeting...........................................10 Review Report to the Members on Statement of the Compliance with Best Practices of Code of Corporate Governance...................................................................12 Auditor’s Report to Members.......................................................13 Balance Sheet......................................................................................15 Profit and Loss Account..................................................................16 Cash Flow Statement.......................................................................17 Statement Of Changes In Equity................................................18 Notes to Financial Statements.....................................................19 Six Years Key financial Data...........................................................62 Annexure - 1.........................................................................................63 Combined Pattern of CDC and Physical Share Holdings...................................................................64 Combined Pattern of CDC and Physical Share Holdings ..................................................................65 -

IBFT- Account Number Formats

IBFT- Account Number Formats Allied Bank Please enter Allied Bank Account Number by following the layout below: Total Digits of Account Number: 13 or 20 Digits Format Example: BBBBAAAAAAAAA or BBBBAAAAAAAAAAAAAAAA BBBB = 4 Digit Branch Code, AAAAAAAAA = 9 Digit Account Number, AAAAAAAAAAAAAAAA = 16 Digit Account Number Apna Microfinance Bank Please enter Apna Microfinance Bank Account Number by following the layout below: Total Digits of Account Number: 16 Digits Format Example: BBBBAAAAAAAAAAAA BBBB = 4 Digit Branch Code, AAAAAAAAA = 12 Digits Askari Bank Please enter Askari Bank Account Number by following the layout below: Total Digits of Bank Account Number: 14 Digits Format Example: BBBB = 4 Digit Branch Code, AAAAAAAAAA = 10 Digit Account Number Branchless Banking Account # Always consist of 11 digits Mobile Number. Al-Baraka Please enter Bank Al-Baraka total digits of account Number: Total Digits of Account Number: 13 Digits Bank Alfalah Please enter Bank Alfalah Account Number by following the layout below: Conventional A/C#: Total Digits of Account Number: 14 Format Example: BBBBAAAAAAAAAA BBBB = 4 Digit Branch Code, AAAAAAAAAA = 10 Digit Account Number Islamic A/C#: Total Digits of Account Number: 18 Digit Format Example: BBBBAAAAAAAAAAAAAA BBBB = 4 Digit Branch Code, AAAAAAAAAAAAAA = 14 Digit Account Number Branchless Banking Account # : Always consist of 11 digits Mobile Number. Bank Al-Habib Please enter Bank Al-Habib Account Number by following the layout below: Total Digits of Account Number: 17 Digit Format -

Debit Cards Visa Silver Clearing SMS Alerts Monthly ADC/Digital For

Key Fact Statement (KFS) for Deposit Accounts BANK AL HABIB LTD Date __________ branch IMPORTANT: Read this document carefully if you are considering opening a new account. It is available in English and Urdu. You may also use this document to compare different accounts offered by other banks. You have the right to receive KFS from other banks for comparison. Account Types & Salient Features: Fixed Term Deposit This information is accurate as of the date above. Services, fees and mark up rates may change on Quarterly basis. For updated fees/charges, you may visit our website at www.bankalhabib.com or visit our branches. • No penalty on Premature Encashment. Indicative Rates of Profit on Fixed Deposit Schemes 1 Month Deposit 5.50% p.a 3 Months Deposit 5.50% p.a 6 Months Deposit 5.50% p.a 1 Year Deposit 6.10% p.a 2 Year Deposit 6.30% p.a 3 Year Deposit 6.55% p.a 4 Year Deposit 6.55% p.a 5 Year Deposit 6.55% p.a On premature encashment, profit will be calculated as per rate of last nearest completed tenure while profit on the remaining number of days deposit held, will be calculated and paid on the Savings Account Profit Rate, applicable at the time of Booking of deposit Note: Kindly refer Schedule of Charges (SOC) for exemptions of service charges. Conventional Particulars Fixed Term Deposit Currency PKR Minimum Balance for To open 0 Account To keep 0 Account Maintenance Fee 0 Is Profit Paid on account Yes Subject to the applicable tax rate Indicative Profit Rate. -

Standard Settlement Instructions

Treasury & Financial Institutions Group STANDARD SETTLEMENT INSTRUCTIONS BANK ALFALAH LTD. - PAKISTAN CONVENTIONAL BANKING S. No. CURRENCY BANK / COUNTRY ACCOUNT NO. SWIFT CODE 1. ACU Dollar Bank Alfalah Limited 0701-32029040 ALFHBDDH 2. ACU Dollar Habib Bank Limited 2624032800618 HABBBDDH 3. ACU Dollar Union Bank of India 01003 UBININBB 4. ACU Dollar ICICI Bank Ltd. 000408000491 ICICINBB 5. ACU Dollar Hatton National Bank Ltd., 054010065847 HBLILKLX Mashreqbank PSC, 6. ACU Dollar Mumbai, India 61050949 MSHQINBB 7. ACU Euro Hatton National Bank Ltd 54010066822 HBLILKLX 8. ACU Euro MashreqBank PSC, Mumbai 61049703 MSHQINBB Bank Alfalah Limited 9. ACU Euro Bangladesh, Dhaka 0701-01660001 ALFHBDDH 10. AUD Westpac Banking Corporation ALF0001976 WPACAU2S 11. Canadian Dollar Bank of Montreal Account Number: 31691056928 BOFMCAM2 CNY (Chinese Yuan) Standard Chartered Bank 12. RMB (Renminbi) (China) Limited, Account Number:501510476874 SCBLCNSXSHA 3996019616 13. Danish Krone Danske Bank DK7230003996019616 DABADKKK IBAN: DE24 5004 0000 0880 7182 01; 14. Euro Commerzbank, A.G. Account Number: 400880718201 COBADEFF IBAN: AT79 1100 0010 1161 8400; 15. Euro Unicredit Bank Austria AG Account Number: 01011618400 BKAUATWW Account Number: 1149245009; IBAN: 16. Euro National Bank of Pakistan DE27 501 30000 1149245001 NBPADEFF Account Number: 100100004291; IBAN: 17. Euro Intesa Sanpaolo SpA IT05Z0306940101100100004291 BCITITMM 18. Euro SCB, Frankfurt 018080105 SCBLDEFX 19. Japanese Yen National Bank of Pakistan 21063 NBPAJPJT 20. Pound National Westminster Bank IBAN: GB84NWBK60000404625528; Sort Sterling plc Code: 60-00-04 NWBKGB2L Pound 01707999001 21. Sterling Standard Chartered Bank IBAN: GB87 SCBL 6091 0417 0799 90 SCBLGB2L Alawwal Bank ( Formerly 31002231021 22. Saudi Riyal Saudi Hollandi Bank) IBAN # SA2150000000031002231021 AAALSARI 23. Saudi Riyal Banque Saudi Fransi IBAN # SA5655000000000705900137 BFSRSARI Singapore 24. -

Bank Al Habib Branches Pdf

Bank al habib branches pdf Continue Plot #21, Gulzar Camera, Ware House, West Wharf, Karachi For other banks with similar names, see Habib Bank (disambiguation). This article may place undue reliance on sources too closely related to the subject, potentially preventing the article from being verifiable and neutral. Please help improve it by replacing them with more appropriate quotes in reliable, independent, third-party sources. (August 2020) (Learn how and when to delete this template message) This article is largely or completely dependent on a single source. The relevant discussion can be found on the conversation page. Please help improve this article by typing links to additional sources. Find sources: Al Habib Bank - News newspaper book scientist JSTOR (August 2020)Bank AL HabibTypePublicPSX: BAHLIndustryBanking,Capital Markets,Investment BankingFounded191FonderHamid D. HabibKhkvartersCaraci, PakistanNumber locations800 (2020)Key peopleAbbas D. Habib (Chairman)ProductsLoans, credit cards, savings, consumer bankingRevenuePKR 34.56 billion (2020) - total assets of PKR 1.36 trillion (2020) It is based in Karachi, Pakistan. Al Habib Bank plans to add another 200 branches by the end of 2020. Al Habib Bank has wholesale branches in Bahrain, Seychelles and Malaysia, as well as offices in the UAE, Istanbul, Beijing and Kenya. As of August 2020, the bank's assets have grown to 1.36 trillion rubles. Al Habib Bank decided to purchase a high-rise building in Karachi from TPL Properties, Centrepoint. The Habib Group's involvement in banking services dates back to the 1930s. Habib's original bank started modestly in Bombay in 1941, when he began fixed capital operations of 25,000 rupees. -

Companies Listed On

Companies Listed on KSE SYMBOL COMPANY AABS AL-Abbas Sugur AACIL Al-Abbas CementXR AASM AL-Abid Silk AASML Al-Asif Sugar AATM Ali Asghar ABL Allied Bank Limited ABLTFC Allied Bank (TFC) ABOT Abbott (Lab) ABSON Abson Ind. ACBL Askari Bank ACBL-MAR ACBL-MAR ACCM Accord Tex. ACPL Attock Cement ADAMS Adam SugarXD ADMM Artistic Denim ADOS Ados Pakistan ADPP Adil Polyprop. ADTM Adil Text. AGIC Ask.Gen.Insurance AGIL Agriautos Ind. AGTL AL-Ghazi AHL Arif Habib Limited AHSL Arif Habib Sec. AHSM Ahmed Spining AHTM Ahmed Hassan AIBL Asset Inv.Bank AICL Adamjee Ins. AJTM Al-Jadeed Tex AKDCL AKD Capital Ltd AKDITF AKD Index AKGL AL-Khair Gadoon ALFT Alif Tex. ALICO American Life ALNRS AL-Noor SugerXD ALQT AL-Qadir Tex ALTN Altern Energy ALWIN Allwin Engin. AMAT Amazai Tex. AMFL Amin Fabrics AMMF AL-Meezan Mutual AMSL AL-Mal Sec. AMZV AMZ Ventures ANL Azgard Nine ANLCPS Azg Con.P.8.95 Perc.XD ANLNCPS AzgN.ConP.8.95 Perc.XD ANLPS Azgard (Pref)XD ANLTFC Azgard Nine(TFC) ANNT Annoor Tex. ANSS Ansari Sugar APL Attock Petroleum APOT Apollo Tex. APXM Apex Fabrics AQTM Al-Qaim Tex. ARM Allied Rental Mod. ARPAK Arpak Int. ARUJ Aruj Garments ASFL Asian Stocks ASHT Ashfaq Textile ASIC Asia Ins. ASKL Askari Leasing ASML Amin Sp. ASMLRAL Amin Sp.(RAL) ASTM Asim Textile ATBA Atlas Battery ATBL Atlas Bank Ltd. ATFF Atlas Fund of Funds ATIL Atlas Insurance ATLH Atlas Honda ATRL Attock Refinery AUBC Automotive Battery AWAT Awan Textile AWTX Allawasaya AYTM Ayesha Textile AYZT Ayaz Textile AZAMT Azam Tex AZLM AL-Zamin Mod. -

Bank Alfalah Limited SHELF PROSPECTUS for THE

ADVICE FOR INVESTORS INVESTORS ARE STRONGLY ADVISED IN THEIR OWN INTEREST TO CAREFULLY READ THE CONTENTS OF THIS PROSPECTUS ESPECIALLY THE RISK FACTORS GIVEN AT PART 6 OF THIS PROSPECTUS BEFORE MAKING ANY INVESTMENT DECISION. SUBMISSION OF FALSE AND FICTITIOUS APPLICATIONS IS PROHIBITED AND SUCH APPLICANT’S MONEY MAY BE FORFEITED UNDER SECTION 87(8) OF THE SECURITIES ACT, 2015 Bank Alfalah Limited SHELF PROSPECTUS FOR THE ISSUANCE OF RATED, SECURED, LISTED, REDEEMABLE TERM FINANCE CERTIFICATES OF PKR 50,000 MILLION (Under shelf registration over a period of 3-years) Date and Place of Incorporation: Karachi, June 21st, 1992, Incorporation Number: 0027580, Registered and Corporate Office: B.A. Building, I.I Chundrigar Road, Karachi, Contact Person: Muhammad Zeeshan, Contact Number: +92 21 3312 2126, Website: https://www.bankalfalah.com/, Email: [email protected] Type of Issue and Total Approved Issue Size: The Issue consists of Rated, Secured, Listed, Redeemable Term Finance Certificates (TFCs) having a Total Approved Issue Size of up to PKR 50,000 million. Time Period of Shelf Registration: The TFCs shall be issued in multiple tranches over a period of three (3) years from the date of publication of this prospectus. Size of Current Tranche Series A: Issue Size of Current Tranche Series A is PKR 11,000 million (inclusive of Green Shoe Option of PKR 1,000 million), out of which TFCs of PKR 9,000 million (82% of Issue Size) have been issued to and subscribed by Pre-IPO investors and TFCs of PKR 2,000 million (18% of Issue Size), inclusive of a Green Shoe Option of PKR 1,000 million, are being offered to the general public by way of an Initial Public Offering through this Shelf Prospectus. -

IBFT Guideline

MCB Bank Limited IBFT- Guidelines 1. Al Baraka Bank (Pakistan) Limited Please enter Bank Al-Baraka total digits of account Number: Total Digits of Account Number: 13 Digits Format Example: AAAAAAAAAAAAA Note: A = Account Number 2. Allied Bank Limited Please enter Allied Bank Account Number by following the layout below: Total Digits of Account Number: 13 or 20 Digits Format Example: BBBBAAAAAAAAA or BBBBAAAAAAAAAAAAAAAA Note: B = Branch Code, A = Account Number 3. APNA Microfinance Bank Please enter APNA Microfinance Bank Account Number by following the layout below: Total Digits of Account Number: 16 Digits Format Example: BBBBAAAAAAAAAAAA Note: B = Branch Code, A = Account Number 4. Askari Bank Limited Please enter Askari Bank Account Number by following the layout below: For Branch Banking: Total Digits of Bank Account Number: 14 Digits Format Example: BBBBAAAAAAAAAA Note: B = Branch Code, A = Account Number For Branchless Banking: Total Digits of Bank Account Number: 11 Digits Format Example: 03XXXXXXXXX 5. Bank Al-Habib Limited Please enter Bank Al-Habib Account Number by following the layout below: Total Digits of Account Number: 17 Digits Format Example: BBBBTTTTBBBBBBRRC Note: B = Branch Code, A = Account Number, T = Account Type, BBBB= Base Number, RR = Digit Running Number, C = Check Digit 111 000 622 mcb.com.pk /MCBBankPk Over 1350 Branches & ATMs 6. Bank Al-Falah Limited Please enter Bank Al-Falah Account Number by following the layout below: For Conventional Banking: Total Digits of Account Number: 14 Digits Format Example: BBBBAAAAAAAAAA Note: B = Branch Code, A = Account Number For Islamic Banking: Total Digits of Account Number: 18 Digits Format Example: BBBBAAAAAAAAAAAAAA Note: B = Branch Code, A = Account Number For Branchless Banking: Total Digits of Account Number: 11 Digits Format Example: 03XXXXXXXXX 7. -

Terms and Conditions for Bank AL Habib

Terms and Conditions for Bank AL Habib Debit Card /Bank AL Habib ATM Card The Cardholder / Account Holder understands that by signing this application form, the Cardholder / Account Holder agrees to all the terms and conditions contained herein relating to the Bank AL Habib Debit Card and/or ATM Card, as applicable (“Terms and Conditions”) issued by Bank AL Habib Limited (hereinafter referred to as "the Bank"). These Terms and Conditions are in addition to and not in substitution for any other agreements, mandates, terms and conditions relating to the Cardholder's / Account Holder’s account(s) with the Bank including the General Terms and Conditions. These Terms and Conditions are to be read in conjunction with (i) the Account opening terms and conditions as shall be applicable to the Account from time to time (ii) the general terms and conditions and any other specific applicable terms and conditions for bank accounts and banking services from time to time (“General Terms and Conditions”). The Cardholder confirms having read and understood the General Terms and Conditions relating to all the services mentioned herein, as issued by the Bank from time to time and posted on the corporate website of the Bank, and agrees to be bound by such General Terms and Conditions. 1. Definitions 1.1 "Account" shall mean the bank account held with the Bank in the name of the Cardholder / Account Holder (whether solely or jointly with another person), the number of which account is or shall be specified in the application form for the Card; 1.2 “Account