ANNUAL REPORT 2008 the Management Team Is Also Being Trained on Various Basel II Requirements

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Introduction

INTRODUCTION Bank Alfalah Limited was incorporated in June 21st, 1997 as a public limited company under the Companies Ordinance 1984. Its banking operations commenced from November 1st, 1997. The bank is engaged in commercial banking and related services as defined in the Banking companies ordinance 1962. The Bank is listed on all the three stock exchanges of Pakistan. The Bank is engaged in banking services as described in the Banking Companies Ordinance, 1962 and is operating through 191 conventional banking branches, 32 Islamic banking branches and 7 overseas branches and 1 Offshore Banking Unit, with the registered office at B.A. Building, I.I. Chandigarh, Karachi. Since, its inception as the new identity of H.C.E.B after the privatization in 1997, the management of the bank has implemented strategies and policies to carve a distinct position for the bank in the market place. Strengthened with the banking of the Abu Dhabi Group and driven by the strategic goals set out by its board of management, the Bank has invested in revolutionary technology to have an extensive range of products and services. This facilitates their commitment to a culture of innovation and seeks out synergies with clients and service providers to ensure uninterrupted services to its customers. The bank perceived the requirements of customers and matches them with quality products and service solutions. During the past five years, bank has emerged as one of the foremost financial institution in the region endeavoring to meet the needs of tomorrow as well as today. To continually upgrade the quality of service to the customers, training of team members in all the integral aspects of banking, customer service and IT was specially focused. -

Annual Report 2011

SoneriBank Soneri B8nk Limited Regla11ered ortlce: Rupall House 241-242, - Upper Mall Scheme, Anand Road, Lahore - 54000, Pakistan Tel: (042) 35713101-04 Head Otnc:e: 90·8-C/11, Uberty Market, Gulberg Ill, LahcnJ • 54000, Pakistan Tal: (042) 35772362-65 Central Office: 51h FlOOr, AJ.Rahim Tower, 1.1. Chundrigar Road, Karachi ·74000, Pakistan J Tal: (021) 32439562-67 Webde: www.aonertbank.com 2417 Call C.ntre: 0800-00500 UAN: 111-80NERI Soneri Bank Limited nnnUHL REPORT 2U II An experience Beyond Banking Soneri Bank Limited R~~URl ~frO~T 2011 OUR MISSION To develop Soneri Bank into an aggressive and dynamic financial institution having the capabilities to provide personalized service to customers with cutting edge technology and a wide range of products, and during the process ensure maximum return on assets with the ultimate goal of serving the economy and the society. Soneri Bank Limited R~~URl ~frO~T 2011 Products and Services 07 Corporate Information 13 Board Committees 14 Management Committees 15 Key Performance Indicators 17 Six Years' Financial Summary 18 Six Years' Growth Summary 20 Six Years' Vertical Analysis 22 Six Years' Horizontal Analysis 24 Directors' Report to Shareholders 27 Statement of Value Addition 33 Statement of Internal Controls- by President 34 Statement of Internal Controls- by Chairman 35 Statement of Compliance with Best Practices of Code of Corporate Governance 36 Auditors' Review Report to The Members on Statement of Compliance with Best Practices of Code of Corporate Governance 38 Auditors' Report to The Members 39 Statement of Financial Position 40 Profit and Loss Account 41 Statement of Comprehensive Income 42 Cash Flow Statement 43 Statement of Changes in Equity 44 Notes to the Financial Statements 45 Shariah Advisor's Report 99 Notice of Annual General Meeting 101 Pattern of Shareholding 103 List of Branches 106 List of Foreign Correspondents 110 Soneri Bank Limited nnn ~Al ~Ero~r 2011 nnn~nl ~Ero~r 2011 As of 31 December 2011 Soneri Bank Limited was incorporated on September 28, 1991. -

12. BANKING 12.1 Scheduled Banks Operating in Pakistan Pakistani Banks

12. BANKING 12.1 Scheduled Banks Operating in Pakistan Pakistani Banks Public Sector Banks Nationalized Banks 1. First Women Bank Limited 2. National Bank of Pakistan Specialized Banks 1. Industrial Development Bank of Pakistan (IDBP) 2. Punjab Provincial Co-operative Bank Limited (PPCB) 3. Zarai Traqiati Bank Limited 4. SME Bank Ltd. Provincial Banks 1. The Bank of Khyber 2. The Bank of Punjab Private Domestic Banks Privatized Bank 1. Allied Bank of Pakistan Limited 2. Muslim Commercial Bank Limited 3. United Bank Limited 4. Habib Bank Ltd. Private Banks 1. Askari Commercial Bank Limited 2. Bank Al-Falah Ltd. 3. Bank Al-Habib Ltd. 4. Bolan Bank Ltd. 5. Faysal Bank Ltd. 6. KASB Bank Limited 7. Meezan Bank Ltd. 8. Metropolitan Bank Ltd 9. Prime Commercial Bank Ltd. 10. PICIC Commercial Bank Ltd. 11. Saudi-Pak Commercial Bank Limited 12. Soneri Bank Ltd. 13. Union Bank Ltd. Contd. 139 12.1 Scheduled Banks Operating in Pakistan Private Banks 14. Crescent Commercial Bank Ltd. 15. Dawood bank Ltd. 16. NDLC - IFIC Bank Ltd. Foreign Banks 1. ABN AMRO Bank NV 2. Al-Baraka Islamic Bank BSC 3. American Express Bank Ltd. 4. Citi Bank NA 5. Deutsche Bank AE 6. Habib Bank AG Zurich 7. Oman International Bank SAOG 8. Rupali Bank Ltd 9. Standard Chartered Bank Ltd. 10. The Bank of Tokyo-Mitsubishi Ltd. 11. The Hong Kong & Shanghai Banking Corporation Ltd. Source: SBP Note: Banks operating as on 30th June, 2004 140 12.2 State Bank of Pakistan - Assets of the Issue Department (Million Rupees) Last Day of June Particulars 2003 2004 2005 Total Assets 522,891.0 611,903.7 705,865.7 1. -

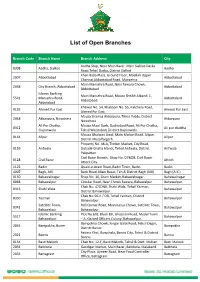

List of Open Branches

List of Open Branches Branch Code Branch Name Branch Address City Aadha Stop, Near Main Bazar, Main Sialkot-Daska 0308 Aadha, Sialkot Aadha Road,Tehsil Daska, District Sialkot Khan Baba Plaza, Ground Floor, Moallah Upper 2007 Abbottabad Abbottabad Channai,Abbottabad Road, Mansehra. Main Mansehra Road, Near Fawara Chowk, 2038 City Branch, Abbottabad Abbottabad Abbottabad Islamic Banking Main Mansehra Road, Mouza Sheikh Albandi 1, 5541 Mansehra Road, Abbottabad Abbotabad. Abbotabad Khewat No. 54, Khatooni No. 55, Katchery Road, 0193 Ahmed Pur East Ahmed Pur East Ahmed Pur East. Mauza Shamsa Akbarpura, Tehsil Pabbi, District 2048 Akbarpura, Nowshera Akbarpura Nowshera Ali Pur Chatha, Mauza Akaal Garh, Qadirabad Road, Ali Pur Chatha, 0312 Ali pur chattha Gujranwala Tehsil Wazirabad, District Gujranwala. Mouza Ghalwan Awal, Main Multan Road, Alipur, 0164 Alipur Alipur District Muzaffargarh. Property No. 48-A, Timber Market, City Road, 0159 Arifwala Outside Ghalla Mandi, Tehsil Arifwala, District Arifwala Pakpattan. Civil Bazar Branch, Shop No. D7&D8, Civil Bazar 0128 Civil Bazar Attock Attock City. 1122 Badin Quaid-e-Azam Road, Badin Town, Badin. Badin 4007 Bagh, AJK Bank Road, Main Bazar, Teh & District Bagh (AJK) Bagh (A.K.) 0150 Bahawalnagar Shop No. 10, Grain Market, Bahawalnagar. Bahawalnagar 0068 Bahawalpur Circular Road, Near Chowk Fawara, Bahawalpur Bahawalpur Chak No. 47/DNB, Shahi Wala, Tehsil Yazman, 0315 Shahi Wala Bahawalpur District Bahawalpur. Chak No.56-A / DB, Tehsil Yazman, District 0330 Yazman Bahawalpur Bahawalpur. Satellite Town, Rafi Qamar Road, Main Kanju Chowk, Satellite Town, 0341 Bahawalpur Bahawalpur Bahawalpur. Islamic Banking Plot No.6/B, Block B/I, Ghaznavi Road, Model Town 5517 Bahawalpur Bahawalpur – A, Gazted Officers Colony, Bahawalpur. -

Trade Deficit Everyone at Least for a Time Being

The Business | EDITORIAL/OPINISOunday N , June 130, 24021 Budget 2021-22: A story Chief Editor of uncatchable dreams out of which 369 billion will be from in - disappointed as development spending do not address the issues of lack of Irfan Athar Qazi ternational financial institutions. The has been hiked by more than 40 percent water, huge price hike of inputs and no E-mail: [email protected] tragedy is we are deep down muddled marked as Rs 1370 billion. The ex - subsidy on inputs. Therefore, more im - into circular debts already and we never penses planned to be incurred on the ports of food items which by the way [email protected] able to cut down debt servicing but we armed services constitute 16 percent of will face increased excise duties as well. are again planning to hike the load of the total outlay of the budget, which is So practically the expenditures without debts. Rs 8.48 trillion. Moreover, the alloca - revenues like dreams without outcomes. Tijarat House, 14-Davis Road, Lahore In terms of real growth the deficit tion is 2.54 percent of the GDP. The The aim behind such exemptions is to should be financed by growth not by debt servicing has been marked as of Rs promote the assembly of mobile phones 0423-6312280, 6312480, 6312429, 6312462 loans and we don’t see the practical poli - 3060 billion which comprised 38 per - as well as encourage investments in re - Cell # 0321-4598258 cies to implement growth since this gov - cent of the GDP. The PSDP budget is of fineries. -

Bilingual / Bi-Annual Pakistan Studies, English / Urdu Research Journal

I ISSN: 2311-6803 PAKISTAN STUDIES Bilingual / Bi-annual Pakistan Studies, English / Urdu Research Journal Vol. 03 Serial No. 1 January - June 2016 Editor: Dr.Mohammad Usman Tobawal PAKISTAN STUDY CENTER, UNIVERSITY OF BALOCHISTAN, QUETTA. II III MANAGING COMMITTE Patron Prof. Dr. Javaid Iqbal Vice Chancellor Editor Inchief Prof. Dr. Naheed Anjum Chishti Editor Dr. Muhammad Usman Tobawal Assistant Editors Dr. Noor Ahmed Prof. Dr. Kalimullah Prof. Dr. Ain ud Din Prof. Ghulam Farooq Baloch Prof. Yousuf Ali Rodeni Prof. Surriya Bano Associate Editors Prof. Taleem Badshah Mr. Qari Abdul Rehman Miss. Shazia Jaffar Mr. Nazir Ahmed Miss. Sharaf Bibi Composing Section Mr. Manzoor Ahmed Mr. Bijar Khan Mr. Pervaiz Ahmed IV EDITORIAL BOARD INTERNATIONAL Dr. Yanee Srimanee, Ministry of Commerce, Thailand. Prof. M. Aslam Syed Harvard University, Cambridge, Massachusetts. Dr. Jamil Farooqui Dept. of Sociology and Anthropology, International Islamic University, Kaula Lumpur Prof. Dr. Shinaz Jindani, Savannah State University of Georgia, USA Dr. Elina Bashir, University of Chicago. Dr. Murayama Kazuyuki, #26-106, Hamahata 5-10, Adachi-ku, Tokyo 1210061, Japan. Prof. Dr. Fida Muhammad, State University of New York Oneonta NY 12820 Dr. Naseer Dashti, 11 Sparows Lane, New Elthaw London, England SEQ2BP. Dr. Naseeb Ullah, International Correspondent, Editor & Political Consultant, The Montreal Tribune, Montreal, Quebec, Canada. Johnny Cheung Institute of Culture & Language Paris, France. V EDITORIAL BOARD NATIONAL Prof. Dr.Abdul Razzaq Sabir, Vice Chancellor, Turbat University. Dr. Fakhr-ul-Islam University of Peshawar. Dr. Abdul Saboor Pro Vice Chancellor, University of Turbat. Syed Minhaj ul Hassan, University of Peshawar. Prof. Dr. Javaid Haider Syed, Gujrat University. -

Pakistan in the Danger Zone a Tenuous U.S

Pakistan in the Danger Zone A Tenuous U.S. – Pakistan Relationship Shuja Nawaz The Atlantic Council promotes constructive U.S. leadership and engagement in international affairs based on the central role of the Atlantic community in meeting the international challenges of the 21st century. The Council embodies a non-partisan network of leaders who aim to bring ideas to power and to give power to ideas by: 7 stimulating dialogue and discussion about critical international issues with a view to enriching public debate and promoting consensus on appropriate responses in the Administration, the Congress, the corporate and nonprofit sectors, and the media in the United States and among leaders in Europe, Asia, Africa and the Americas; 7 conducting educational and exchange programs for successor generations of U.S. leaders so that they will come to value U.S. international engagement and have the knowledge and understanding necessary to develop effective policies. Through its diverse networks, the Council builds broad constituencies to support constructive U.S. leadership and policies. Its program offices publish informational analyses, convene conferences among current and/or future leaders, and contribute to the public debate in order to integrate the views of knowledgeable individuals from a wide variety of backgrounds, interests, and experiences. The South Asia Center is the Atlantic Council’s focal point for work on Afghanistan, Pakistan, India, Bangladesh, Sri Lanka, Nepal and Bhutan as well as on relations between these countries and China, Central Asia, Iran, the Arab world, Europe and the U.S. As part of the Council’s Asia program, the Center seeks to foster partnerships with key institutions in the region to establish itself as a forum for dialogue between decision makers in South Asia, the U.S. -

Research and Development

Annual Report 2010-11 Research and Development RESEARCH AND DEVELOPMENT FACULTY OF ARTS & HUMANITIES DEPARTMENT OF ARCHAEOLOGY Projects: (i) Completed UNESCO funded project ―Sui Vihar Excavations and Archaeological Reconnaissance of Southern Punjab” has been completed. Research Collaboration Funding grants for R&D o Pakistan National Commission for UNESCO approved project amounting to Rs. 0.26 million. DEPARTMENT OF ENGLISH LANGUAGE & LITERATURE Publications Book o Spatial Constructs in Alamgir Hashmi‘s Poetry: A Critical Study by Amra Raza Lambert Academic Publishing, Germany 2011 Conferences, Seminars and Workshops, etc. o Workshop on Creative Writing by Rizwan Akthar, Departmental Ph.D Scholar in Essex, October 11th , 2010, Department of English Language & Literature, University of the Punjab, Lahore. o Seminar on Fullbrght Scholarship Requisites by Mehreen Noon, October 21st, 2010, Department of English Language & Literature, Universsity of the Punjab, Lahore. Research Journals Department of English publishes annually two Journals: o Journal of Research (Humanities) HEC recognized ‗Z‘ Category o Journal of English Studies Research Collaboration Foreign Linkages St. Andrews University, Scotland DEPARTMENT OF FRENCH LANGUAGE AND LITERATURE R & D-An Overview A Research Wing was introduced with its various operating desks. In its first phase a Translation Desk was launched: Translation desk (French – English/Urdu and vice versa): o Professional / legal documents; Regular / personal documents; o Latest research papers, articles and reviews; 39 Annual Report 2010-11 Research and Development The translation desk aims to provide authentic translation services to the public sector and to facilitate mutual collaboration at international level especially with the French counterparts. It addresses various businesses and multi national companies, online sales and advertisements, and those who plan to pursue higher education abroad. -

KFS Current Accounts Silkbank (Final).FH11

Key Fact Statement for Deposit Accounts Silkbank Limited, Date ___- ___-____ IMPORTANT: Read this document carefully if you are considering opening a new account. It is available in English and Urdu. You may also use this document to compare different accounts offered by other banks. You have the right to receive KFS from other banks for comparison. Branch, City Account Types & Salient Features: This information is accurate as of the date above. Services, fees and mark-up rates may change on a bi-annual basis. For updated fees/charges, you may visit our website or visit our branches. Conventional Particulars All in One Account Business Value Business Value Online Express Basic Banking Asaan Account Salary Premium Salary Premium Pensioner Account Foreign Currency Account Account Plus Account Plus Account Currency PKR PKR PKR PKR PKR PKR PKR PKR PKR USD, GBP, EUR To open Rs. 2,500/- Rs. 2,500/- Rs. 2,500/- Rs. 2,500/- Rs. 1,000/- Rs. 100/- Zero Zero Rs. 2,500/- Rs. 2,500/- Minimum Balance for Account ( ) USD = 5,000 To keep Zero Rs. 100,000/- Zero Rs. 50,000/- Zero Zero Zero Zero Zero ( ) GBP = 3,000 ( ) EUR = 3,000 Account Maintenance Fee Zero Rs. 43/- Zero Rs. 43/- Zero Zero Zero Zero Zero 1 USD/GBP/EUR Is profit paid on account subject to the applicable tax rate No No No No No No No No No No Indicative Profit Rate (%) Profit Payment Frequency Provide example Premature / Early Encashment / Withdrawal Fee Service Charges IMPORTANT: This is a list of the main service charges for this account. -

Debit Cards Visa Silver Clearing SMS Alerts Monthly ADC/Digital For

Key Fact Statement (KFS) for Deposit Accounts BANK AL HABIB LTD Date __________ branch IMPORTANT: Read this document carefully if you are considering opening a new account. It is available in English and Urdu. You may also use this document to compare different accounts offered by other banks. You have the right to receive KFS from other banks for comparison. Account Types & Salient Features: Fixed Term Deposit This information is accurate as of the date above. Services, fees and mark up rates may change on Quarterly basis. For updated fees/charges, you may visit our website at www.bankalhabib.com or visit our branches. • No penalty on Premature Encashment. Indicative Rates of Profit on Fixed Deposit Schemes 1 Month Deposit 5.50% p.a 3 Months Deposit 5.50% p.a 6 Months Deposit 5.50% p.a 1 Year Deposit 6.10% p.a 2 Year Deposit 6.30% p.a 3 Year Deposit 6.55% p.a 4 Year Deposit 6.55% p.a 5 Year Deposit 6.55% p.a On premature encashment, profit will be calculated as per rate of last nearest completed tenure while profit on the remaining number of days deposit held, will be calculated and paid on the Savings Account Profit Rate, applicable at the time of Booking of deposit Note: Kindly refer Schedule of Charges (SOC) for exemptions of service charges. Conventional Particulars Fixed Term Deposit Currency PKR Minimum Balance for To open 0 Account To keep 0 Account Maintenance Fee 0 Is Profit Paid on account Yes Subject to the applicable tax rate Indicative Profit Rate. -

Government of Pakistan, Commercial Bank, Development Finance Institutions

Budget Special 2014-15 1. Budget Speech 2014-15 2. Finance Bill 2014-15 3. Notes on Clauses 4. Salient Features 5. Budget at a glance 2014-15 6. Budget Brief 2014-15 7. www.imranghazi.com/mtbaTax Expenditure 8. Fiscal Development 9. Highlights of Economic Survey 2013-14 10. Comments on Budget 2014-15 For more material, visit "www.imranghazi.com/mtba" Budget Special 2014-15 Speech BUDGET SPEECH 2014-15 Bismillahir-Rehmanir-Rahim PART-I Mr. Speaker, 1. As I rise to present the second budget of the democratic government, I want to thank Allah (SWT) for remarkable mercies He has bestowed on us by giving enormous success to the policies and initiatives we announced in our first budget. This success is the outcome of a democratic process that has allowed people to choose their representatives and they, in turn, are working to achieve their aspirations. 2. When we started our journey, we were facing the most daunting task of repairing a broken economy. We embarked on a very comprehensive agenda of economic reforms aimed to reinvigorate the economy, spur growth, maintain price stability, provide jobs to the youth and rebuild the key infrastructure of the country. Prime Minister Mohammed Nawaz Sharif set a rare example of foresight, courage and political sagacity when he did not shy away from taking painful decisions; decisions that were surely unpopular but imperative for restoringwww.imranghazi.com/mtba economic health of the country. Today, with the blessings of Allah, I say in all humility that we have not only restored the health of the economy but have put it firmly on the path of stability and growth. -

Annual REPORT 2011 SILKBANKT

ANNUAl REPORT 2011 SILKBANKT Notice of AGM & Auditors' Review 35 Auditors' Report 39 Financial Statements 43 Six Years' Rnancial Highlights 44 Statement of Financial Position 50 Profit & Loss Account 51 Statement of Comprehensive Income 52 Vision & Mission 02 Cash Row Statement 53 Message from Chairman 04 Statement of Changes in Equity 54 President & CEO's Review 06 Notes to the Financial Statements 55 Senior Management Committee 09 Statement of Written-off Loans 100 Profiles of Board of Directors 13 Achievements & CSR 103 Corporate Information 17 Additional Shareholders' Information 110 Directors' Report 21 Pattern of Share Holdings CDC & Physical 111 Statement of Compliance with 29 Branch Network 114 the Code of Corporate Governance Foreign Correspondents 116 & Statement of Internal Control Proxy Form 119 To be the leader in premier banking, trusted by customers for accessibility, service and innovation; be an employer of choice creating value for all stakeholders In the aftermath of the economic slowdown since 2008, Non-Performing Loans (NPLs) have dampened the profitability dynamics of commercial banks. I am pleased to advise you that contrary to the banking industry trend, your Bank managed to register a significant reduction in NPLs, in each consecutive year since the takeover by the new management. An NPL reduction by the Special Assets Management team of Rs. 3.398 billion and a Provision Reversal of Rs. 1.829 billion was recorded for the year 2011. The Real Estate Asset Management team (REAM) also supported the Special Assets Management team by successfully selling off various properties held as OREO (Other Real Estate Owned), during the year.