Deloitte Access Economics Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Pay TV in Australia Markets and Mergers

Pay TV in Australia Markets and Mergers Cento Veljanovski CASE ASSOCIATES Current Issues June 1999 Published by the Institute of Public Affairs ©1999 by Cento Veljanovski and Institute of Public Affairs Limited. All rights reserved. First published 1999 by Institute of Public Affairs Limited (Incorporated in the ACT)␣ A.C.N.␣ 008 627 727 Head Office: Level 2, 410 Collins Street, Melbourne, Victoria 3000, Australia Phone: (03) 9600 4744 Fax: (03) 9602 4989 Email: [email protected] Website: www.ipa.org.au Veljanovski, Cento G. Pay TV in Australia: markets and mergers Bibliography ISBN 0 909536␣ 64␣ 3 1.␣ Competition—Australia.␣ 2.␣ Subscription television— Government policy—Australia.␣ 3.␣ Consolidation and merger of corporations—Government policy—Australia.␣ 4.␣ Trade regulation—Australia.␣ I.␣ Title.␣ (Series: Current Issues (Institute of Public Affairs (Australia))). 384.5550994 Opinions expressed by the author are not necessarily endorsed by the Institute of Public Affairs. Printed by Impact Print, 69–79 Fallon Street, Brunswick, Victoria 3056 Contents Preface v The Author vi Glossary vii Chapter One: Introduction 1 Chapter Two: The Pay TV Picture 9 More Choice and Diversity 9 Packaging and Pricing 10 Delivery 12 The Operators 13 Chapter Three: A Brief History 15 The Beginning 15 Satellite TV 19 The Race to Cable 20 Programming 22 The Battle with FTA Television 23 Pay TV Finances 24 Chapter Four: A Model of Dynamic Competition 27 The Basics 27 Competition and Programme Costs 28 Programming Choice 30 Competitive Pay TV Systems 31 Facilities-based -

Channel Guide

Channel Guide To view your favourite channels, simply turn on your TV using the remote provided and select the channel number listed below. Entertainment 101 / 149 103 / 150 1105 / 105 / 151 1106 / 106 / 152 A fun, vibrant channel, that celebrates A cracking celebration of brilliant British Escape with larger than life reality, soap Your destination for original, exclusive TV Hits we love to love. See more on entertainment. dramas and daytime favourites – Arena and award winning local and TVH!TS+2 on channel 149. has it all. international lifestyle productions. 1108 / 108 111 / 154 113 / 156 1119 / 119 / 161 Hungry for non-stop entertainment? Provides a fun, entertaining place to FOX Classics is the only channel which Be entertained by edgy and FOX8’s got you covered with relax and watch your favourite gems. showcases classic movies and classic unconventional cinematic drama your favourite animations and DC television, 24 hours a day. series that redefine the genre. superheroes. 121 / 162 1122 / 122 / 614 1123 / 123 / 163 124 The home of comedy. Australia’s Discover genuine, passionate and Absorbing, accessible and adventurous. MTV showcases an array of international 24-hour channel dedicated to making authentic characters who risk life, limb There’s always something to feed your reality, drama & live music shows PLUS people laugh. and fortune to survive and win. imagination on Syfy. LIVE action from its annual award shows. 125 126 127 / 164 128 As Pop Culture evolves, E! will always be Expertise and inspiration for women who Australia’s dedicated food channel The ultimate destination for home at the heart of it, making sure you don’t aspire to look fabulous, live well, be daring delivering the best in delicious and property entertainment. -

Liberty Global's Australian Subsidiary AUSTAR Receives a Non-Binding

Liberty Global’s Australian Subsidiary AUSTAR Receives a Non-Binding and Conditional Acquisition Proposal from FOXTEL Englewood, Colorado – May 25, 2011: Liberty Global, Inc. (“Liberty Global”) (NASDAQ: LBTYA, LBTYB and LBTYK) announced today that its 54.2%-owned subsidiary, AUSTAR United Communications Limited (“AUSTAR”), has received an indicative, non-binding and conditional proposal (“Proposal”) from FOXTEL to acquire 100% of AUSTAR for a price of 1.52 Australian dollars (AUD) in cash per share. A copy of AUSTAR’s release to the Australian Securities Exchange is set forth below. The Proposal values AUSTAR at AUD 2.5 billion (including net debt of AUD 525 million at March 31, 2011), representing an enterprise value multiple of approximately 10 times AUSTAR’s consolidated operating cash flow (as customarily defined by Liberty Global) for the 12 months ended March 31, 2011. Assuming definitive agreements are reached on the indicative terms and the conditions to closing are satisfied, Liberty Global would realize gross proceeds of AUD 1.0 billion ($1.1 billion based on the exchange rate at May 24, 2011) for its 688.5 million AUSTAR shares. In light of the non-binding and conditional nature of the Proposal, no assurance can be given that the Proposal will lead to a definitive transaction. Further, to the extent a definitive transaction is entered into, no assurance can be given that the conditions to closing that definitive transaction will ultimately be satisfied. Liberty Global is being advised by Allen & Overy in connection with this Proposal. About Liberty Global, Inc. Liberty Global is the leading international cable operator offering advanced video, voice and broadband internet services to connect its customers to the world of entertainment, communications and information. -

This Article Is Downloaded From

This article is downloaded from http://researchoutput.csu.edu.au It is the paper published as Author: D. Cameron Title: Sky News Active: Notes from a digital TV newsroom Conference Name: Media Literacy in the Pacific & Asia Conference Location: Fiji Publisher: JEA Year: 2004 Date: 5-9 December, 2004 Abstract: This paper describes the desktop technology employed in the Sky newsroom to provide eight mini-channels of digital TV news content to subscribers. It outlines the developing workflow that has emerged as Sky News pioneers this form of television news content production in Australia. Many of the staff employed specifically to work on the digital service are recent graduates from journalism courses, and this paper notes some of the entry-level skills required by such employees to produce the digital content. Author Address: [email protected] URL: http://www.usp.ac.fj/journ/jea/docs/JEA04Abstracts.htm http://www.usp.ac.fj/journ/jea/ http://researchoutput.csu.edu.au/R/-?func=dbin-jump- full&object_id=11274&local_base=GEN01-CSU01 CRO identification number: 11274 Sky News Active: Notes from a digital TV newsroom David Cameron Charles Sturt University [email protected] Introduction “Sky News Active – This is News – How you want it, when you want it, 24/7” (Foxtel Digital promotion 2004) Sky News Australia launched its digital interactive service on 5 January 2004, as one of the more than 120 channels and interactive services being offered as part of Foxtel’s $550 million rollout of digital subscriber services in Australia (Kruger 2004). This major initiative is a joint venture of the Seven Network Australia, Publishing and Broadcasting Limited (owner of the Nine television network), and the British Sky Broadcasting (BSkyB) network. -

Media Concentration: Australia

3/17/2010 Media Concentration: Australia Australia: Overview • Traditional media: highly concentrated - 1-3 dominant players • Newspapers (total daily & Sunday circulation) – News Ltd = 58% approx; Fairfax = 29% approx . • Magazines (circulation: PBL = 44%; Pacific = 27%) • Commercial TV (3 Networks – 77% ads) • Commercial Radio (4 groups - 55% ads) • Telecoms (Telstra 64% total/41% wireless) • Pay TV [Foxtel 63.1% (96): Austar, Optus resell ] – Owners: Telstra 50%, News Ltd 25%, PBL 25% • ISP: Bigpond/Telstra (44%) 1 3/17/2010 AUSTRALIA: Newspapers (1984-2008) 100% 5000 90% 4500 80% 4000 70% 3500 60% 3000 50% 2500 40% 2000 30% 1500 20% 1000 10% 500 0% 0 1984 1988 1992 1996 2000 2004 2008 C4 HHI 2 3/17/2010 AUSTRALIA: Magazines (2000-2008) 100% 3000 90% 2500 80% 70% 2000 60% 50% 1500 40% 1000 30% 20% 500 10% 0% 0 1984 1988 1992 1996 2000 2004 2008 C4 HHI 3 3/17/2010 AUSTRALIA: BROADCAST TELEVISION (1988-2007) (All data relates to fiscal year ending 30 June) 1988 1992 1996 2000 2004 2007 Share of Total Revenue (%) COMMERCIAL TV Seven Network 17.0 21.2 22.8 26.2 22.1 24.9 Nine Network 23.6 24.4 25.7 27.9 25.8 21.5 Ten Network 17.6 11.5 15.4 13.6 17.9 18.2 Other Commercial TV 24.7 24.4 20.4 17.8 20.5 20.0 PUBLIC TV ABC 14.6 16.1 12.5 11.6 10.2 12.4 SBS 2.5 2.5 3.1 3.0 3.5 3.0 Total Revenue ($A million) 1,592.9 2,282.0 2,913.8 3,828.7 4316.7 4,689.9 C4 72.9 73.2 76.5 79.2 76.0 77.0 HHI 1372 1435 1579 1780 1578 1566 Noam Index 380 398 422 514 476 472 AUSTRALIA: BROADCAST TELEVISION (1988-2007) 100% 3000 90% 2500 80% 70% 2000 60% 50% 1500 40% -

PDF (Accepted Manuscript)

Swinburne Research Bank http://researchbank.swinburne.edu.au Author: Morsillio, R. & Barr, T. Title: Innovation or disruption? The National Broadband Network comes to Australian TV Year: 2013 Journal: International Journal of Digital Television Volume: 4 Issue: 3 Pages: 239-260 URL: http://doi.org/10.1386/jdtv.4.3.239_1 Copyright: Copyright © 2013 Intellect. This is the author’s version of the work, posted here with the permission of the publisher for your personal use. No further distribution is permitted. You may also be able to access the published version from your library. The definitive version is available at: http://ingentaconnect.com Swinburne University of Technology | CRICOS Provider 00111D | swinburne.edu.au Powered by TCPDF (www.tcpdf.org) Innovation or disruption? The National Broadband Network comes to Australian TV Robert Morsillo and Trevor Barr, Swinburne University Abstract There are many forces for change confronting the well-established institutional arrangements underpinning Australian media industries, with commercial television, in particular, likely to be most challenged during the next five years. New distribution and delivery models connected to the proposed high capacity National Broadband Network (NBN), along with new content providers and changing viewer preferences are likely to drive major changes to existing television arrangements. In a rapidly changing environment, this article seeks to relate established concepts of innovation and creative destruction, disintermediation and disruption to the impact these new NBN mediated opportunities may have on existing TV arrangements, both free-to-air (FTA) and subscription (STV). It seeks to explore the extent to which TV-like services over the NBN might disrupt incumbent TV broadcasters; the extent to which changing consumer preferences and practices might disrupt current business models; and how incumbent TV broadcasters might be responding to these threats with their own innovations. -

Download the Fetch Mobi App User Guide

Fetch Mobi App User Guide What’s inside Welcome to the Fetch Mobi App 3 Before you start 4 Sign into the Fetch Mobi App 8 Connect to your Fetch Box 10 Home 11 Watch Live TV and Catch-Up 14 Using the TV Guide 15 Managing your Recordings 17 Watch movies 20 Watch shows from the TV Store 24 Find your movies and shows in My Stuff 27 Manage your Account 29 Playing content on your mobile or tablet 32 2 Welcome to the Fetch Mobi App With the Fetch Mobi App, you can use your phone or tablet to enjoy Fetch at home or on the go: • Buy and rent Movies from the Movie Store. • Buy TV Shows from the TV Store. • Watch content from the Movie and TV Stores in SD. • Download movies and TV shows onto your phone or tablet to watch on the go. • Watch Movie Box movies if included with your subscription. • Watch selected entertainment channels if included in your subscription. • Browse available content and watch trailers. • Set recordings from anywhere so you never miss your shows. • Manage your recordings and Series Tags on the go • Doubles as a handy remote for controlling your Fetch box. 3 1 Before you start Before installing the Fetch Mobi App, check that your mobile Note: device is supported and you are aware of the network and The Fetch Mobi app screens used in this guide connection requirements. may look slightly different depending on which mobile device you are using. Supported phones and tablets iOS Devices * iOS users will need to rent or buy through your Fetch box, or Fetch Account at www.fetchtv.com.au/account. -

Draft Version of the Undertaking

ACCC NOT TO OPPOSE AUSTAR ACQUISITION AFTER UNDERTAKING RESOLVES CONCERNS The Australian Competition and Consumer Commission will not oppose the proposed acquisition of AUSTAR United Communications Limited by FOXTEL Management Pty Limited after accepting court-enforceable undertakings from FOXTEL. The undertakings will prevent FOXTEL from acquiring exclusive internet protocol television (IPTV) rights for a range of attractive television program and movie content, including: • Linear channels supplied by independent content suppliers, including more than 60 linear channels that are currently broadcast by FOXTEL and many more that are broadcast internationally • Subscription Video on Demand (SVOD) rights to current or past seasons of television programs that form part of a linear channel supplied by an independent content supplier • Movie linear channels (or movies for inclusion in a linear channel) from more than 50% of the eight major movie studios or more than 50% of the eight specified independent movie studios • SVOD rights to movies, except for an 18 month window in relation to the movie studios from which FOXTEL is not prohibited from acquiring exclusive linear rights. The undertaking further prohibits FOXTEL from exclusively acquiring any movie delivered on a Transactional Video on Demand (TVOD) basis. Importantly, the undertaking also prevents FOXTEL from acquiring exclusive mobile rights to the content referred to above where those rights are sought by competitors to combine with IPTV rights. This means that those competitors will have the opportunity to deliver a seamless and integrated package of programming across a number of devices. A full list of channels that are currently broadcast on the FOXTEL satellite or cable subscription television platform that are covered by the undertaking is at Attachment A. -

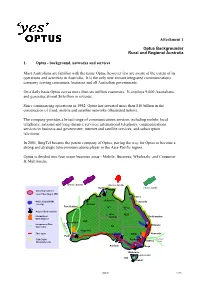

1. Optus - Background, Networks and Services

Attachment 1 Optus Backgrounder Rural and Regional Australia 1. Optus - background, networks and services Most Australians are familiar with the name Optus, however few are aware of the extent of its operations and activities in Australia. It is the only new entrant integrated communications company serving consumers, business and all Australian governments. On a daily basis Optus serves more than six million customers. It employs 9,000 Australians, and generates almost $6 billion in revenue. Since commencing operations in 1992, Optus has invested more than $10 billion in the construction of fixed, mobile and satellite networks (illustrated below). The company provides a broad range of communications services including mobile; local telephony; national and long distance services; international telephony; communications services to business and government; internet and satellite services; and subscription television. In 2001, SingTel became the parent company of Optus, paving the way for Optus to become a strong and strategic telecommunications player in the Asia-Pacific region. Optus is divided into four major business areas - Mobile; Business; Wholesale; and Consumer & Multimedia. B-Series Satellite A-Series Satellite Darwin C-Series Satellite Switching Systems/ Local Fibre Ring in CBD Cairns Mobile Digital(GSM) Katherine Townsville coverage Broome Port Hedland NT Mt Isa National Earth Stations Alice QLD International Springs Rockhampton Earth Station s WA S Geraldton International Fibre e M Brisbane e SA Optic Cable W e 3 Kalgoorlie Fibre Optic Port Augusta NSW Newcastle Perth SDH Digital Canberra Southern Sydney Microwave Link Cross VIC Adelaide Bega Melbourne Launceston TAS Hobart Optus 1 of 5 The company’s Mobile business unit has captured around one-third of the total Australian GSM mobile market and leads the market in mobile data take up. -

Asia Expat TV Complete Channel List

Asia Expat TV Complete Channel List Australia FOX Sport 502 FOX LEAGUE HD Australia FOX Sport 504 FOX FOOTY HD Australia 10 Bold Australia SBS HD Australia SBS Viceland Australia 7 HD Australia 7 TV Australia 7 TWO Australia 7 Flix Australia 7 MATE Australia NITV HD Australia 9 HD Australia TEN HD Australia 9Gem HD Australia 9Go HD Australia 9Life HD Australia Racing TV Australia Sky Racing 1 Australia Sky Racing 2 Australia Fetch TV Australia Live 1 HD (Live During Events Only) Australia AFL Live 2 HD (Live During Events Only) Australia AFL Live 3 HD (Live During Events Only) Australia AFL Live 4 HD (Live During Events Only) Australia AFL Live 5 HD (Live During Events Only) Australia AFL Live 6 HD (Live During Events Only) Australia AFL Live 7 HD (Live During Events Only) Australia AFL Live 8 HD (Live During Events Only) Australia AFL Live 9 HD (Live During Events Only) Australia NRL Live 1 HD (Live During Events Only) Australia NRL Live 2 HD (Live During Events Only) Australia NRL Live 3 HD (Live During Events Only) Australia NRL Live 4 HD (Live During Events Only) Australia Live 5 HD (Live During Events Only) Australia NRL Live 6 HD (Live During Events Only) Australia NRL Live 7 HD (Live During Events Only) Australia NRL Live 8 HD (Live During Events Only) Australia NRL Live 9 HD (Live During Events Only) Australia NRL Rugby League 1 HD (Only During Live Games) Australia NRL Rugby League 2 HD (Only During Live Games) Australia NRL Rugby League 3 HD (Only During Live Games) Australia VIP NZ: TVNZ 1HD Australia VIP NZ: TVNZ 2HD Australia -

ASIA PACIFIC PAY-TV DISTRIBUTION the Future of Pay-TV in Asia

ASIA PACIFIC PAY-TV DISTRIBUTION The Future of Pay-TV in Asia September 2017 About the Publisher As a leading independent consulting and research provider, MPA Advisory & Consulting Media Partners Asia (MPA) offers a range of customized MPA customizes our consulting services for a wide range of services and market research to help companies drive business players across the media & telecoms industry. Our expertise development, strategy & planning, M&A, and roll out new helps drive business across the ecosystem. MPA gives companies products & services. Based in Hong Kong, Singapore and India, the data, diligence, insights and strategies to achieve their our teams have local depth and expertise across 18 key markets objectives, including: in Asia Pacific and key international territories. » Benchmarking competition » Entering new markets with local partnerships MPA offers: in-depth research reports across key industry » Initial public offerings (IPOs) sectors; customized consulting services; industry events to » Launching new products and services spread knowledge and unlock partnerships; and publications » M&A transactions that provide insights into driving business. » Restructuring » Recruiting new talent MPA clients include all industry stakeholders, including media & telecoms owners, distributors, policymakers, trade bodies, MPA services include: technology companies and financial institutions. » Benchmarking studies » Due diligence services for M&A MPA Research Reports » Customized market research Our analysts produce 10 reports a year across a variety of sectors » Corporate strategy within the media & telecoms industry, providing data, research » IMC (Independent Market Consultant) research for IPOs and actionable insights that help businesses expand their reach into new markets and benchmark their current performance and MPA Events future growth trajectory. -

Herbert Geer Letter

20 March 2012 PUBLIC VERSION Mr Bruce Mikkelsen Australian Competition and Consumer Commission GPO Box 3131 Canberra ACT 2601 By email: [email protected] Dear Mr Mikkelsen Proposed acquisition of Austar by Foxtel – response to proposed undertakings This submission is provided by iiNet Limited and its wholly owned subsidiary TransACT Communications Pty Ltd (referred to collectively in this letter as iiNet) in response to the Commission‟s letter of 7 March 2012 inviting comments about the effectiveness of the section 87B undertaking offered by Foxtel in relation to its proposed acquisition of Austar. 1. INTRODUCTION The proposed undertaking will have little (if any) meaningful effect on the market for the acquisition of compelling content in the event that the merger is allowed to go ahead. The undertaking also does nothing to address the market dominance issue in the Australian subscription TV market, or related telecommunications markets, and actually exacerbates the issue which will result in a substantial lessening of competition. It is apparent from the preamble to the proposed undertaking that the main source of competition that is being relied on to provide competitive restraint is IPTV. The only way that this can realistically be achieved is if the undertaking improves the access to compelling content for new and emerging IPTV providers to a level where those IPTV providers will actually be in a position to compete with the merged entity for the acquisition of content. It is impossible for this objective to be achieved unless IPTV providers have access to premium content that is capable of attracting large numbers of subscribers.