SEPA Request-To-Pay

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Public Bank Unionpay Lifestyle Debit Card Product Disclosure Sheet

PRODUCT DISCLOSURE SHEET Public Bank Berhad (6463-H) Read this Product Disclosure Sheet before you PB Visa/MasterCard Lifestyle Debit – Generic decide to take up the PB Visa/MasterCard/Union Pay Lifestyle Debit. Be sure to also read the PB Visa/MasterCard Lifestyle Debit – Basic general terms and conditions. Savings Account/Basic Current Account PB UnionPay Lifestyle Debit – PB UnionPay Savings Account Date: 1. What is this product about? PB Visa/MasterCard/UnionPay Lifestyle Debit is a two-in-one card combining Visa/MasterCard/ UnionPay debit card and ATM functions. The card is linked to the Savings Account/Current Account/Basic Savings Account/Basic Current Account/PB UnionPay Savings Account (“Banking Account”) of the individual and any expenditure will be deducted directly from the Banking Account. This is a PB Visa/MasterCard/UnionPay Lifestyle Debit, a payment instrument which allows you to pay via a direct deduction of the cost for goods and services from your Banking Account at participating retail and service outlets. You are required to maintain a Banking Account with us, to be linked to your PB Visa/MasterCard/UnionPay Lifestyle Debit. If you close your Banking Account maintained with us, your PB Visa/MasterCard/UnionPay Lifestyle Debit will be automatically cancelled. 2. What are the fees and charges I have to pay? (i) Annual Fee x Generic/PB UnionPay Savings Account: RM8.00 x Basic Savings Account/Basic Current Account: Waived (subject to eight (8) ATM cash withdrawals and six (6) over-the-counter withdrawals per month*) *Note: Fee for exceeding the threshold will be RM1.00 per transaction. -

New Debit Card Solutions At

New Debit Card Solutions Debit Mastercard and Visa Debit are ready Swiss Banking Services Forum, 22 May 2019 Philippe Eschenmoser, Head Cards & A2A, Swisskey Ltd Maestro/V PAY Have Established Themselves As the “Key to the Account” – Schemes, However, Are Forcing Market Entry For Successor Products Response from the Maestro and V PAY are successful… …but are not future-capable products schemes # cards Maestro V PAY on Lower earnings potential millions8 for issuers as an alternative payment traffic products (e.g. 6 credit cards, TWINT) Issuer 4 V PAY will be 2 decommissioned by VISA Functional limitations: in 20211 – Visa Debit as 0 • No e-commerce the successor 2000 2018 • No preauthorizations Security and stability have End- • No virtualization proven themselves customer High acceptance in CH and Merchants with an online MasterCard is positioning abroad in Europe offer are demanding an DMC in the medium term online-capable debit as the successor to Standard product with an Merchan product Maestro integrated bank card t 2 1: As of 2021 no new V PAY may be issued TWINT (Still) No Substitute For Debit Cards – Credit Cards With Divergent Market Perception TWINT (still) not alternative for debit Credit cards a no alternative for debit Lacking a bank card Debit function Limited target group (age, ~1.1 M 1 ~10 M. creditworthiness...) Issuer ~48.5 k ~170 k1 No direct account debiting DMC/ Visa Debit Potentially high annual fee End-customer Lower customer penetration Banks and merchants DMC/ P2P demand an online- Higher costs Merchant Visa Debit -

Credit Cards American Express Company 24-Hour Number: (800) 528-2121 (U.S

Credit Cards American Express Company 24-Hour Number: (800) 528-2121 (U.S. and Canada) American Express Cards include: Personal Green (pictured), Gold, Platinum, Corporate Green (pic - tured), Corporate Gold, Corporate Platinum, Corpo - rate Optima, Optima, Optima Gold, Purchasing Card, American Express Blue (pictured), Green and Gold Rewards, and more. American Express also issues co-branded cards, including Hilton, Delta SkyMiles (pictured), ITT Sheraton Club Miles, and more. American Express issues multiple styles of prepaid cards. Gift Cards (4 are pictured) can be variable load or pre-denominated ranging from $25 to $3,000. Gift Cards are not reloadable and can be personalized or issued anonymously. Reloadable prepaid cards are also available in various styles and offer different functionality. Serve and Bluebird prepaid cards are multifunction cards with many new features such as bill pay, check writing, and funds transfer. All prepaid cards have the word “PREPAID” printed on either the front or back of the card. Account numbers are 15 digits, begin with 37 or 34, and are sequenced 4-6-5. UV light reveals large “AMEX” and phosphorescence on the face of each card, excluding the Gift Card. The Centurion or the American Express Blue Box appears on most Amer - ican Express cards. To establish the validity of a card, or determine its status, please call (866) 375-3684. 98 Credit Cards Diners Club International ® 2500 Lake Cook Rd. Riverwoods, IL 60015 Security Contacts: Law Enforcement Phone Line: 1-800-347-3083 for law enforcement officers Merchant Code 10 Authorization: 1-800-347-1111 for suspicious transactions Diners Club ® account numbers start with 36 or 55. -

Ssb3: Debit Card Updates / / / / /

SSB3: DEBIT CARD UPDATES If only Part A or B is completed, please send to: DBS Bank Ltd – Credit Ops, 2 Changi Business Park Crescent, #07-03, DBS Asia Hub, S486029. If only Part C is completed, please send to: DBS Bank Ltd – Account Services, Simpang Bedok Post Office, PO Box 215, Singapore 914808, unless otherwise stated. If Part A, B and C are completed, please send to: DBS Bank Ltd – Credit Ops, 2 Changi Business Park Crescent, #07-03, DBS Asia Hub. Name: IC/ Passport No.*: Existing Debit Card (“Card”) No.: PART A: Instruction for POSB Multitude, Takashimaya Debit, Capita Debit, DBS SUTD, DBS NUSSU, HomeTeamNS-PAssion-POSB or SAFRA DBS Debit Card ☐ Lost (Please call Lost Card No. at 18001111111 immediately to report loss of your Card.) ☐ Non-receipt ☐ Damaged / Faulty Card* (Existing PIN to be used with the new Card issued.) Replace Card due to: ☐ Change of name embossed on the Card to: (Max 19 characters. Existing PIN to be used with the new Card issued.) ☐ Retained at ATM. Location: Change of Language Choice: ☐ English ☐ Selection at ATM PART B: Instruction for POSB GO! Debit MasterCard, PAssion POSB Debit Card, DBS Visa Debit, DBS UnionPay Debit, DBS Treasures Visa Debit, DBS Treasures Private Client Visa Debit or DBS Private Banking Visa Debit Card ☐ Lost (Please call Lost Card No. at 18001111111 immediately to report loss of your Card.) ☐ Non-receipt Replace Card due to: ☐ Damaged / Faulty Card (New Card and PIN will be sent in two separate mailers) Note: A $5 Debit Card replacement fee ☐ Change of name embossed on the Card to: is applicable for Lost Card (Max 19 characters) ☐ Retained at ATM. -

BAHRAIN Cial Services in South Asia

March 2015 Issue 517 www.cardsinternational.com REWARD AND REAP Levaraging Big Data while pulling in the punters ● COMMENT: ACQUIRING ● ANALYSIS: LOYALTY ● INTERVIEW: FINTECH ‘NON-BANKS’ ● OPINION: BIOMETRICS CI 517.indd 1 26/03/2015 09:18:10 Delivering innovative mobile & online financial services solutions to organisations that need to provide secure access To find out more about us please visit: www.intelligentenvironments.com We are an international provider of innovative mobile and online solutions for financial service organisations. Our mission is to enable our clients always to stay close to their customers. We do this through Interact®, our single software platform, which enables secure financial applications, engagement, transaction and servicing across all digital channels. Today these are predominantly focused on mobile, PCs & tablets. However Interact® can and will support other form factors, as and when they proliferate (as seen by our work to develop digital banking for the Smartwatch). We provide a ready alternative to internally developed solutions, enabling our clients with a faster route to market, expertise in managing the complexity of multiple devices and operating systems, and a constantly evolving solution. IE-Advert-Dec-2014.indd 1 16/12/2014 12:25:21 Cards International EDITOR’S LETTER CONTENTS EDITOR’S LETTER 2 COMMENT: BETHAN COWPER Bethan Cowper examines the differences between age groups and Prepaid Middle East: their attitudes towards new and established payment services 6 INTERVIEW: FINTECH ‘NON-BANKS’ huge growth but still APS has become the first fintech non-bank to offer banking services through the Post Office’s branch scratching the surface network. -

2017 Investment Community Meeting September 7, 2017 Agenda 10:10 A.M

2017 Investment Community Meeting September 7, 2017 Agenda 7:30 a.m. Registration 10:30 a.m. International Markets Ann Cairns 8:30 a.m. Welcome 10:40 a.m. Europe Panel Discussion Warren Kneeshaw Ann Cairns, Javier Perez, Mark Barnett, Carlo Enrico 8:35 a.m. Our Strategy Advances 11:05 a.m. Emerging Markets Ajay Banga Ling Hai, Ari Sarker, Gilberto Caldart 8:50 a.m. Global Products: 11:20 a.m. Financial Perspective Powering Choice and Convenience Martina Hund-Mejean Michael Miebach 9:15 a.m. Addressing Digital Opportunities 11:35 a.m. Q&A Session Garry Lyons 9:35 a.m. Securing and Advancing Commerce Ajay Bhalla 9:45 a.m. North American Markets Craig Vosburg 10:10 a.m. Break ©2017 Mastercard. Forward looking statements Today’s presentation may contain, in addition to historical information, forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are based on our current assumptions, expectations and projections about future events which reflect the best judgment of management and involve a number of risks and uncertainties that could cause actual results to differ materially from those suggested by our comments today. You should review and consider the information contained in our filings with the SEC regarding these risks and uncertainties. Mastercard disclaims any obligation to publicly update or revise any forward-looking statements or information provided during today’s presentations. Any non-GAAP information contained in today’s presentations is reconciled to its GAAP equivalent in the appendices at the end of this presentation. -

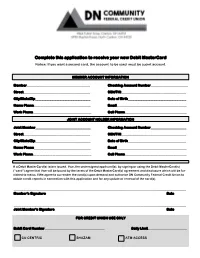

Complete This Application to Receive Your New Debit Mastercard Notice: If You Want a Second Card, the Account to Be Used Must Be a Joint Account

Complete this application to receive your new Debit MasterCard Notice: If you want a second card, the account to be used must be a joint account. MEMBER ACCOUNT INFORMATION Member_______________________________________ Checking Account Number_______________________ Street_________________________________________ SSN/TIN________________________________________ City/State/Zip__________________________________ Date of Birth____________________________________ Home Phone___________________________________ Email___________________________________________ Work Phone____________________________________ Cell Phone______________________________________ JOINT ACCOUNT HOLDER INFORMATION Joint Member__________________________________ Checking Account Number______________________ Street_________________________________________ SSN/TIN________________________________________ City/State/Zip__________________________________ Date of Birth____________________________________ Home Phone___________________________________ Email___________________________________________ Work Phone____________________________________ Cell Phone______________________________________ If a Debit MasterCard(s) is/are issued. I/we, the undersigned applicant(s), by signing or using the Debit MasterCard(s) (“card”) agree that I/we will be bound by the terms of the Debit MasterCard(s) agreement and disclosure which will be fur- nished to me/us. I/We agree to surrender the card(s) upon demand and authorize DN Community Federal Credit Union to obtain credit reports in connection with -

Card Processing Guide - MOI 2015.Qxp GP 07/09/2015 17:45 Page 1

JM3150_Card Processing Guide - MOI 2015.qxp_GP 07/09/2015 17:45 Page 1 CARD PROCESSING GUIDE MERCHANT OPERATING INSTRUCTIONS SERVICE. DRIVEN. COMMERCE JM3150_Card Processing Guide - MOI 2015.qxp_GP 07/09/2015 17:45 Page 2 CONTENTS SECTION PAGE Welcome 1 Global Payments 1 About This Document 1 An Introduction To Card Processing 3 The Anatomy Of A Card Payment 3 Transaction Types 4 Risk Awareness 4 Card Present (CP) Transactions 9 Cardholder Verified By PIN 9 Cardholder Verified By Signature 9 Cardholder Verified By PIN And Signature 9 Contactless Card Payments 10 Checking Cards 10 Examples Of Card Logos 13 Examples Of Cards And Card Features 14 Accepting Cards Using An Electronic Terminal 18 Authorisation 19 ‘Code 10’ Calls 24 Account Verification/Status Checks 25 Recovered Cards 26 Refunds 27 How To Submit Your Electronic Terminal Transactions 29 Using Fallback Paper Vouchers 30 Card Not Present (CNP) Transactions 33 Accepting Mail And Telephone Orders 33 Accepting Internet Orders 34 Authorisation Of CNP Transactions 36 Confirming CNP Orders 38 Delivering Goods 39 Collection Of Goods 39 Special Transaction Types 40 Bureau de Change 40 Dynamic Currency Conversion (DCC) 41 Foreign Currency Transactions 41 Gratuities 42 Hotel And Car Rental Transactions 42 Prepayments/Deposits/Instalments 44 Purchase With Cashback 44 Recurring Transactions 45 Global Iris 48 HomeCurrencyPay 50 An Introduction To HomeCurrencyPay 50 JM3150_Card Processing Guide - MOI 2015.qxp_GP 07/09/2015 17:45 Page 3 SECTION PAGE Card Present (CP) HomeCurrencyPay Transactions -

Westpac Debit Mastercard®

Westpac Debit Mastercard Terms & Conditions for personal customers. Effective date: 13 September 2021 Your Bank. The advisory services and the banking products you’ll find in this booklet are provided to you by: Westpac Banking Corporation ABN 33 007 457 141 275 Kent Street, Sydney NSW 2000 AFSL and Australian credit licence number 233714. Postal Address. GPO Box 3433 Sydney NSW 2001 Cardholder enquiries. Cards Customer Service Call Centre Australia 1300 651 089 Overseas +61 2 9155 7700 Lost or stolen cards, suspected unauthorised transactions or divulged PINs. Cards lost in Australia or overseas can be promptly reported via the following numbers: Australia 1300 651 089 Overseas +61 2 9155 7700 Your PIN can be easily changed via Online Banking, at Westpac branded ATMs (provided you know your existing PIN) or by visiting any one of our branches in Australia (subject to verification of your identity). Emergency telephone numbers are displayed on, or within the immediate vicinity of all Westpac ATMs in Australia. Contents Introduction ................................................................................5 Changes to terms and conditions. ...................................................5 Definitions. ....................................................................................................8 Fees and charges ...................................................................... 11 Bank fees and charges. ..........................................................................11 Westpac Debit Mastercard fees and charges. -

Debit Mastercard® Guide to Benefits BELONG Important Information

Missoula Federal Credit Union Debit Mastercard® Guide to Benefits BELONG Important information. Please read and save. This Guide to Benefits contains detailed information about insurance, retail protection and travel services you can access as a preferred cardholder. This Guide supersedes any guide or program description you may have received earlier. To file a claim or for more information on any of these services, call the Mastercard Assistance Center at 1-800-Mastercard: 1-800-627-8372, or en Español: 1-800-633-4466. “Card” refers to Mastercard® card and “Cardholder” refers to a Mastercard® cardholder. Key Terms interface for cardholders. It serves as a repository of all the personally identifiable information (PII) data the cardholder Throughout this document, You and Your refer to the wants to monitor, tracks and displays cardholders’ risk cardholder. score, and provides access to identity protection tips. It Cardholder means the person who has been issued an is also the platform for cardholders to respond to identity account by the Participating Organization for the covered monitoring alerts. card. Monthly Risk Alert / Newsletter: Cardholders will receive Covered card means the Mastercard card. a monthly newsletter with information on the cardholder’s Mastercard ID Theft Protection™ risk score, and articles pertaining to good identity Program Description: protection practices. Mastercard ID Theft Protection (IDT) provides you with Identity Monitoring: IDT searches the internet to detect access to a number of Identity Theft resolution services, compromised credentials and potentially damaging use should you believe you are a victim of Identity Theft. This of your personal information, and alerts you via email so product offering will alert you about possible identity theft that you can take immediate action. -

Dual-Network Cards and Mobile Wallet Technology

Dual-Network Cards and Mobile Wallet Technology Consultation Paper December 2016 Contents 1. Introduction 1 Box A: The entities in mobile payments 2 2. Dual-Network Debit Cards 3 Box B: Dual-network cards and mobile wallets: experience in other jurisdictions 4 3. Mobile Wallet Technology 6 4. Some Emerging Issues 8 5. Consultation and Next Steps 10 © Reserve Bank of Australia 2016. All rights reserved. The contents of this publication shall not be reproduced, sold or distributed without the prior consent of the Reserve Bank of Australia. ISBN 978-0-9805857-8-0 (Online) 1. Introduction Mobile card payments are payments that are made using an electronic representation of a payment card in a mobile phone or other device, as opposed to using the traditional ‘plastic’ form factor. The electronic representation of the card is contained in a ‘mobile wallet’ – an ‘app’ provided either by the cardholder’s financial institution or by a third-party mobile wallet provider. Mobile wallets may also contain electronic representations of other cards and credentials that are typically found in traditional physical wallets. There is currently significant commercial activity in the mobile payments sphere in Australia involving financial institutions, card schemes and third-party mobile wallet providers. Almost all Australian card-issuing financial institutions have mobile banking apps and in many cases these issuer apps or wallets allow cardholders to make mobile payments using the near-field communication (NFC) or quick response (QR) code functionality of mobile devices to communicate with payment terminals.1 There are also currently three large third-party mobile wallet providers – Apple Pay, Android Pay and Samsung Pay – which allow mobile payments for customers of particular banks and via particular networks. -

Justice Department Sues to Block Visa's Proposed Acquisition of Plaid

1 JOHN R. READ (DC Bar #419373) MEAGAN K. BELLSHAW (CA Bar #257875) 2 CORY BRADER LEUCHTEN (NY Bar # 5118732) 3 SARAH H. LICHT (DC Bar #1021541) United States Department of Justice, Antitrust Division 4 450 Fifth Street, NW, Suite 4000 Washington, DC 20530 5 Telephone: (202) 307-0468 6 Facsimile: (202) 514-7308 E-mail: [email protected] 7 [Additional counsel listed on signature page] 8 9 Attorneys for Plaintiff United States of America 10 11 UNITED STATES DISTRICT COURT 12 NORTHERN DISTRICT OF CALIFORNIA 13 SAN FRANCISCO DIVISION 14 15 UNITED STATES OF AMERICA, Case No.: 16 Plaintiff COMPLAINT v. 17 18 VISA INC. and PLAID INC., 19 20 Defendants. 21 22 Visa seeks to buy Plaid – as its CEO said – as an “insurance policy” to neutralize a 23 “threat to our important US debit business.” Visa is a monopolist in online debit transactions, 24 extracting billions of dollars in fees annually from merchants and consumers. Plaid, a financial 25 technology firm with access to important financial data from over 11,000 U.S. banks, is a threat 26 to this monopoly: it has been developing an innovative new solution that would be a substitute 27 for Visa’s online debit services. By acquiring Plaid, Visa would eliminate a nascent competitive 28 threat that would likely result in substantial savings and more innovative online debit services for -1- COMPLAINT 1 merchants and consumers. For the reasons discussed below, the proposed acquisition violates 2 Section 2 of the Sherman Act, 15 U.S.C. § 2, and Section 7 of the Clayton Act, 15 U.S.C.