Balaji Telefilms 4QFY2008 Result Update

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Outcome-AGM-2016.Pdf

Spine to be adjusted by printer C-13, Balaji House, Dalia Industrial Estate, Opposite Laxmi Industrial Estate, New Link Road, Andheri (West) Mumbai - 400 053. www.balajitelefilms.com world.com dickenson www. dickenson Spine to be adjusted by printer Spine to be adjusted by printer Spine to be adjusted by printer We are content innovators, creators and producers of unmatched credentials and long-standing success. We operate as a vertically integrated studio model, which allows us to create, distribute and monetise content, not only in ways that are best aligned with viewer preferences, but in ways in which we can capture the maximum value stream. With a focus on chasing quality growth, we continue to create gripping content – content that is relevant to As global viewership diverse sets of audiences and accessible across multiple platforms. continues to evolve, we have With geographical boundaries disappearing in the seamless world of the anticipated future trends and internet, we aim to make our content seamlessly available. Improvement in created new entertainment mobile broadband infrastructure, gradual reduction in cost of internet and paradigms. Today, we increase in smartphone screen sizes is driving consumer preferences. straddle across all the three The Subscription Video on Demand (SVOD) market in India is on the cusp distinct platforms through of a meteoric take-off. As Over The Top (OTT) video consumption continues which people consume to grow tremendously, we are leveraging our capabilities to create content entertainment – across platforms. Our motive is vertical integration across the value chain by Television, offering our own OTT services. We are making our delivery channels more closely aligned to the emerging needs and creating entertainment-on-the-go Movies and for our dynamic audiences. -

Balaji Telefilms Limited 10 20 11 Company Review

annual report Balaji Telefilms Limited 10 20 11 Company Review 02 A Snapshot of Our World 04 Shifting Paradigms 06 Performance Highlights 07 Financial Highlights 08 Letter to the Shareholders 09 Managing Director’s Review Statutory Report 10 Joint Managing 14 Management Financial Statements Director’s Message Discussion & Analysis 34 Standalone Financial 11 Balaji Shows on 20 Directors’ Report Statements Television 24 Corporate Goverance 61 Consolidated 12 Board of Directors Report Financial Statements Balaji Motion Pictures Limited 86 Directors’ Report 89 Financial Statements 107 AGM Notice Forward looking statement In this Annual Report, we have disclosed forward looking information to enable investors to comprehend our prospects and take investment decisions. This report and other statements, written and verbatim, that we periodically make contain forward looking statements that set out anticipated results based on the management’s plans and assumptions. We have tried wherever possible to identify such statements by using words such as ‘anticipate’, ‘estimate’, ‘expects’, ‘projects’, ‘intends’, ‘plans’, ‘believes’, and words of similar substance in connection with any discussion of future performance. We cannot guarantee that these forward looking statements will be realised, although we believe we have been prudent in assumptions. The achievements of results are subject to risks, uncertainties, and even inaccurate assumptions. Should known or unknown risks or uncertainties materialise, or should underlying assumptions prove inaccurate, actual results could vary materially from those anticipated, estimated, or projected. Readers should keep this in mind. We undertake no obligation to publicly update any forward looking statements, whether as a result of new information, future events or otherwise. Vision is all about looking ahead It is seldom static but often consistent. -

Koel Chatterjee Phd Thesis

Bollywood Shakespeares from Gulzar to Bhardwaj: Adapting, Assimilating and Culturalizing the Bard Koel Chatterjee PhD Thesis 10 October, 2017 I, Koel Chatterjee, hereby declare that this thesis and the work presented in it is entirely my own. Where I have consulted the work of others, this is always clearly stated. Signed: Date: 10th October, 2017 Acknowledgements This thesis would not have been possible without the patience and guidance of my supervisor Dr Deana Rankin. Without her ability to keep me focused despite my never-ending projects and her continuous support during my many illnesses throughout these last five years, this thesis would still be a work in progress. I would also like to thank Dr. Ewan Fernie who inspired me to work on Shakespeare and Bollywood during my MA at Royal Holloway and Dr. Christie Carson who encouraged me to pursue a PhD after six years of being away from academia, as well as Poonam Trivedi, whose work on Filmi Shakespeares inspired my research. I thank Dr. Varsha Panjwani for mentoring me through the last three years, for the words of encouragement and support every time I doubted myself, and for the stimulating discussions that helped shape this thesis. Last but not the least, I thank my family: my grandfather Dr Somesh Chandra Bhattacharya, who made it possible for me to follow my dreams; my mother Manasi Chatterjee, who taught me to work harder when the going got tough; my sister, Payel Chatterjee, for forcing me to watch countless terrible Bollywood films; and my father, Bidyut Behari Chatterjee, whose impromptu recitations of Shakespeare to underline a thought or an emotion have led me inevitably to becoming a Shakespeare scholar. -

~Alaii C(;;Etetitms E£Tb. C-13

~alaii C(;;etetitms e£tB. C-13. Balaji House, Dalia Industrial Estate.Opp. Laxmi Industries New link Road. Andheri (West). Mumbai - 400 053. Te1.:40698000 • Fax: 40698181 182183 Website: www.balajitelefilms.com CIN No .. L99999MH1994PLC082802 August 08, 2018 To, BSE Ltd. National Stock Exchange of India Ltd. Phiroze Jeejeebhoy Towers, "Exchange Plaza", Dalal Street, Bandra-Kurla Complex, Bandra(East), Mumbai400001 Mumbai400051 Stock Code: 532382 Stock Code: BALAJITELE Sub: Intimation of 24th Annual General Meeting and Book Closure Date Dear Sir/Madam, Pursuant to Regulation 30 of Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015 ("Listing Regulations") this is to inform you that 24th Annual General Meeting of the Members of the Company is scheduled to be held on Friday, August 31, 2018 at 12.00 noon at "The Oub", 197, Juhu Versova Link Road, Opp. D. N. Nagar Police Station, Andheri (W), Mumbai - 400 053, Maharashtra (AGM notice attachecf). As per section 108 of the Companies Act, 2013, read with the Rule 20 of the Companies (Management and Administration) Rules, 2014 and Regulation 44 of the Listing Regulations, the Company is pleased to provide its members the facility to cast their vote(s) on all resolutions set forth in the Notice by electronic means ("remote e-voting"). The instructions for remote e-voting are mentioned in the Notice. Further pursuant to Regulation 42 of Listing Regulations, Register of Members and Share Transfer Books will remain closed from Saturday, August 25, 2018 to Friday, August 31, 2018 (both days inclusive) for the purpose of AGM and determining the Members eligible to receive Final Dividend recommended by the Board of Directors for the financial year 2017-18. -

Representation of Sikh Character in Bollywood Movies:A Study on Selective Bollywood Movies

PJAEE, 17(6) (2020) REPRESENTATION OF SIKH CHARACTER IN BOLLYWOOD MOVIES:A STUDY ON SELECTIVE BOLLYWOOD MOVIES Navpreet Kaur Assistant Professor University Institute of Media Studies, Chandigarh University, Punjab, India [email protected] Navpreet Kaur, Representation Of Sikh Character In Bollywood Movies: A Study On Selective Bollywood Movies– Palarch’s Journal of Archaeology of Egypt/Egyptology 17(6) (2020), ISSN 1567-214X. Keywords: Bollywood, Sikh, Sikh Character, War, Drama, Crime, Biopic, Action, Diljit Dosanhj, Punjab Abstract Sikhs have been ordinarily spoken to in mainstream Hindi film either as courageous warriors or as classless rustics. In the patriot message in which the envisioned was an urban North Indian, Hindu male, Sikh characters were uprooted and made to give entertainment. Bollywood stars have donned the turban to turn Sikh cool, Sikhs view the representation of the community in Bollywood as demeaning and have attempted to revive the Punjabi film industry as an attempt at authentic self-representation. But with the passage of time the Bollywood makers experimented with the role and images of Sikh character. Sunny Deol's starrer movie Border and Gadar led a foundation of Sikh identity and real image of Sikh community and open the doors for others. This paper examines representation of Sikhs in new Bollywood films to inquire if the romanticization of Sikhs as representing rustic authenticity is a clever marketing tactic used by the Bollywood. Introduction Bollywood is the sobriquet for India's Hindi language film industry, situated in the city of Mumbai, Maharashtra. It is all the more officially alluded to as Hindi film. The expression "Bollywood" is frequently utilized by non-Indians as a synecdoche to allude to the entire of Indian film; be that as it may, Bollywood legitimate is just a piece of the bigger Indian film industry, which incorporates other creation communities delivering films in numerous other Indian dialects. -

Aspirational Movie List

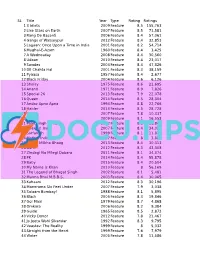

SL Title Year Type Rating Ratings 1 3 Idiots 2009 Feature 8.5 155,763 2 Like Stars on Earth 2007 Feature 8.5 71,581 3 Rang De Basanti 2006 Feature 8.4 57,061 4 Gangs of Wasseypur 2012 Feature 8.4 32,853 5 Lagaan: Once Upon a Time in India 2001 Feature 8.2 54,714 6 Mughal-E-Azam 1960 Feature 8.4 3,425 7 A Wednesday 2008 Feature 8.4 30,560 8 Udaan 2010 Feature 8.4 23,017 9 Swades 2004 Feature 8.4 47,326 10 Dil Chahta Hai 2001 Feature 8.3 38,159 11 Pyaasa 1957 Feature 8.4 2,677 12 Black Friday 2004 Feature 8.6 6,126 13 Sholay 1975 Feature 8.6 21,695 14 Anand 1971 Feature 8.9 7,826 15 Special 26 2013 Feature 7.9 22,078 16 Queen 2014 Feature 8.5 28,304 17 Andaz Apna Apna 1994 Feature 8.8 22,766 18 Haider 2014 Feature 8.5 28,728 19 Guru 2007 Feature 7.8 10,337 20 Dev D 2009 Feature 8.1 16,553 21 Paan Singh Tomar 2012 Feature 8.3 16,849 22 Chakde! India 2007 Feature 8.4 34,024 23 Sarfarosh 1999 Feature 8.1 11,870 24 Mother India 1957 Feature 8 3,882 25 Bhaag Milkha Bhaag 2013 Feature 8.4 30,313 26 Barfi! 2012 Feature 8.3 43,308 27 Zindagi Na Milegi Dobara 2011 Feature 8.1 34,374 28 PK 2014 Feature 8.4 55,878 29 Baby 2015 Feature 8.4 20,504 30 My Name Is Khan 2010 Feature 8 56,169 31 The Legend of Bhagat Singh 2002 Feature 8.1 5,481 32 Munna Bhai M.B.B.S. -

About Balaji Telefilms

Private and Confidential Unique, Distinctive, Disruptive Investor Presentation Unique, Distinctive, Disruptive Disclaimer Certain words and statements in this communication concerning Balaji Telefilms Limited (“the Company”) and its prospects, and other statements relating to the Company‟s expected financial position, business strategy, the future development of the Company‟s operations and the general economy in India & global markets, are forward looking statements. Such statements involve known and unknown risks, uncertainties and other factors, which may cause actual results, performance or achievements of the Company, or industry results, to differ materially from those expressed or implied by such forward-looking statements. Such forward-looking statements are based on numerous assumptions regarding the Company‟s present and future business strategies and the environment in which the Company will operate in the future. The important factors that could cause actual results, performance or achievements to differ materially from such forward-looking statements include, among others, changes in government policies or regulations of India and, in particular, changes relating to the administration of the Company‟s industry, and changes in general economic, business and credit conditions in India. The information contained in this presentation is only current as of its date and has not been independently verified. No express or implied representation or warranty is made as to, and no reliance should be placed on, the accuracy, fairness or completeness of the information presented or contained in this presentation. None of the Company or any of its affiliates, advisers or representatives accepts any liability whatsoever for any loss howsoever arising from any information presented or contained in this presentation. -

Balaji Telefilms Limited C-13, Balaji House, Dalia Industrial Estate, Opp

Balaji Telefilms Limited C-13, Balaji House, Dalia Industrial Estate, Opp. Laxmi Industries, New Link Road, Andheri (West), Mumbai 400 053 Tel: 40698000 Fax: 40698181/82/83 Website: www.balajitelefilms.com CIN: L99999MH1994PLC082802 Balaji Telefilms continues to entertain audiences with ALTBalaji subscriptions growing 60% th 20 April,2020: Balaji Telefilms Limited, India’s leading media and content powerhouse continues to closely monitor the COVID-19 situation and has taken necessary steps to protect the health and safety of all its stakeholders. The company has initiated work from home policy in line with regulatory directives. Key business updates ALTBalaji: Our Digital SVOD business ALTBalaji has seen a significant increase in engagement levels as consumers are switching their content consumption online. ALTBalaji continues to be a leader in the original Hindi SVOD space and one of the few homegrown success stories in the OTT space. Watch times and subscriptions have been seeing strong growth during this period and we are witnessing high level of growth in all our key markets and demographics. ALTBalaji is witnessing strong uptake of digital subscriptions with an average of 17,000subscriptions added per daypost lockdown vs an average of 10,600 in March 2020 pre lockdown a growth of 60% .As of date the platform has over 1.7m active direct subscribers. ALTBalaji has also successfully completed the first ever syndication of a web series to a broadcaster with 3 hit digital shows now airing on Prime Time television. Karrle Tu Bhi Mohabbat, Baarish and Kehne Ko Humsafar Hain are now available between 9pm and 11pm on Zee TV. -

DEFINATION the Capacity and Willingness to Develop, Organize

DEFINATION The capacity and willingness to develop, organize and manage a business venture along with any of its risks in order to make a profit. The most obvious example of entrepreneurship is the starting of new businesses. In economics, entrepreneurship combined with land, labor, natural resources and capital can produce profit. Entrepreneurial spirit is characterized by innovation and risk-taking, and is an essential part of a nation's ability to succeed in an ever changing and increasingly competitive global marketplace. Differences Between Women and Men Entrepreneurs When men and women start companies, do they approach the process the same way? Are there key differences? And how do those differences affect the success of the business venture? As a woman in the start-up community, I am frequently asked about women entrepreneurs. A popular question is: How are they different from men? There have been many studies of entrepreneurs and start-ups, and I’ve read a number of them. Many of them seem to me to fall short, because the researchers, not being entrepreneurs themselves, lack an in-depth understanding of the entrepreneurial mind. The result is often a lot of statistics that fail to enlighten readers about entrepreneurial behavior and motivation. So what follows are my personal opinions. They are not based on formal research, but on my own observations and interactions with other women entrepreneurs. 1. Women tend to be natural multitaskers, which can be a great advantage in start-ups. While founders typically have one core skill, they also need to be involved in many different aspects of their business. -

Role of Media and Usage of Films and Documentaries As Political Tool

© 2018 JETIR June 2018, Volume 5, Issue 06 www.jetir.org (ISSN-2349-5162) Role of Media and Usage of Films and Documentaries as Political Tool DR. VIKRAMJIT SINGH, ASSOCIATE PROFESSOR DEPARTMENT OF POLITICAL SCIENCE, DAYANAND COLLGE, HISAR, HARYANA, INDIA Abstract Now days the usage of print as well as digital media is widely used for the propaganda to have the political advantage by the political parties. A number of movies and documentaries are intentionally released so that the political benefits can be taken. In this manuscript, the case scenarios of such movies and the film based propaganda are addressed so that the overall motive and the goals of the political parties can be identified. In this research paper, the case studies and the scenarios of assorted films and documentaries are cited so that the clear theme can be addressed with the higher degree of references and the proof of the mentioned work. In current scenarios, the political parties whether these are opposition or the ruling they are getting the huge benefits with the exploitations of emotions of the general public with the integration of films to defame or fame the particular person or parties. By this way, the overall scenario and integrity of movies and bollywood is getting affected with the favor of particular political benefits. Keywords: Propaganda Movie, Role of Media in Politics, Cinema as Political Tool Introduction The filmmakers are now days more focused on polishing the image of particular person or defaming the image of particular parties and these are visible from the assorted movies specifically in the time of elections but it is not the good practices to exploit the image of particular parties. -

The Midas Touch of SRK Married

‘It was an experiment. Looking back, I’m glad we did it but I’m glad we jumped ‘About the ending of the book and whether or not Rhett came back to his wife holly off when we did after three years of feeling like a laboratory rat’ – the singer Ozzy books – well, you have me out on a limb’ – a letter written by the late Margaret Mitchell Osbourne, who starred with his family in The Osbournes, says he didn’t enjoy having (pictured), revealing she didn’t know whether Scarlett O’Hara and Rhett Butler would to bolly his life chronicled in the show & views ever get back together in her novel Gone with the Wind ú 1. Rick Ross arrested ú 2. Ek Villain has ‘awesome’ opening day married life The rapper Rick Ross has been released after his arrest Mohit Suri’s romantic thriller Ek Villain hit more than 2,500 by Hala For parents, following a concert in the United States. Police said Ross screens in India on Friday, raking in 16.72 crore rupees (Dh10.23 The Midas touch of SRK Khalaf was taken into custody on Friday after the SuperJam million). “#EkVillain Fri (Rs.) 16.72 cr nett [2539 screens]. India concert in North Carolina. A court had issued an order for biz. Second highest opener of 2014. In terms of screen average, Ramadan is a his arrest because he failed to appear in court on a previous it’s HIGHEST. AWESOME!” tweeted the Indian trade analyst Taran Priti Salian speaks to Koral misdemeanour drugs charge. -

Declaration by the Candidate

DECLARATION BY THE CANDIDATE I hereby declare that the dissertation entitled “Objectification and commodification of women in the visual media: A critical study” submitted at National Law University, Delhi is the outcome of my own work carried out under the supervision of Dr. Sushila, Assistant Professor (Law), National Law University, Delhi. I further declare that to the best of my knowledge, the dissertation does not contain any part of my work, which has been submitted for the award of any degree either in this University or in any other institution without proper citation. Vighnesh Balaji 27/ LLM /18 Place: New Delhi National Law University, Delhi Date: 23.05.19 I CERTIFICATE OF SUPERVISOR This is to certify that the work reported in the LL.M. dissertation titled “Objectification and Commodification of Women in the Visual Media: A Critical Study” submitted by Vighnesh Balaji at National Law University, Delhi is a bona fide record of his original work carried out under my supervision. Dr. Sushila Assistant Professor (Law) Place: New Delhi National Law University, Delhi Date: 23.05.19 II ACKNOWLEDGMENT First, and foremost I would like to thank my wonderful supervisor Dr. Sushila who has always believed in me and has provided me insightful suggestions and has been a constant pillar of support throughout the dissertation period. My father, for always trying to balance me, My sisters, for holding my back, my friends, to whom I owe the world, NLU-Delhi for teaching me much more than the prescribed syllabus. Last but never the least; I thank Lord Shiva with all my heart for my unconditional mother, Suseela Ravichandran who has always firmly believed that the odds have to favour me.