The Marin-Sonoma Artisan Cheese Cluster by Carol A. Pranka a Dissertation Submitted in Partial Satisfaction Of

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ims List Sanitation Compliance and Enforcement Ratings of Interstate Milk Shippers April 2017

IMS LIST SANITATION COMPLIANCE AND ENFORCEMENT RATINGS OF INTERSTATE MILK SHIPPERS APRIL 2017 U.S. Department of Health and Human Services Public Health Service Food and Drug Administration Rules For Inclusion In The IMS List Interstate milk shippers who have been certified by State Milk sanitation authorities as having attained the milk sanitation compliance ratings are indicated in the following list. These ratings are based on compliance with the requirements of the USPHS/FDA Grade A Pasteurized Milk Ordinance and Grade A Condensed and Dry Milk Products and Condensed and Dry Whey and were made in accordance with the procedures set forth in Methods of Making Sanitation Rating of Milk Supplies. *Proposal 301 that was passed at 2001 NCIMS conference held May 5-10, 2001, in Wichita, Kansas and concurred with by FDA states: "Transfer Stations, Receiving Stations and Dairy Plants must achieve a sanitation compliance rating of 90 or better in order to be eligible for a listing in the IMS List. Sanitation compliance rating scores for Transfer and Receiving Stations and Dairy Plants will not be printed in the IMS List". Therefore, the publication of a sanitation compliance rating score for Transfer and Receiving Stations and Dairy Plants will not be printed in this edition of the IMS List. THIS LIST SUPERSEDES ALL LISTS WHICH HAVE BEEN ISSUED HERETOFORE ALL PRECEDING LISTS AND SUPPLEMENTS THERETO ARE VOID. The rules for inclusion in the list were formulated by the official representatives of those State milk sanitation agencies who have participated in the meetings of the National Conference of Interstate Milk Shipments. -

James E. Tillison, the Alliance of Western Milk Producers (Pdf)

,- tU. rllllldtlll~l ~ ~.elt:~l ft rlU||l, dllll IllllauIt I../l:ltl~.. II I"IId.UU~ lillll~., t. I t .3"t" r"lVl Page 2 of 5 USDA The Ilia n c e OALJ/HCO of Western Milk Procluoers ZOO0 JUL 11..4 I::9 U,: 22 July 14, 2000 RECEIVED Office of the Hearing Clerk USDA Room 1081, South Building, 1400 Independence Ave., S. W. Washington, D.C., 20250 SUBJECT: Milk in the Northeast and other Marketing Areas Docket No. AO-14-A69, et al., DA-003 Alexandria, Virginia May 8-12, 2000 Dear Sir: The Alliance of Westem Milk Producers is a trade association that represents two major operating cooperatives in Califomia -- California Dairies Inc. and Humboldt Creamery. These organizations represent nearly 50 percent of the milk and milk producers in California. Comments on the above federal order milk marketing hearing are being submitted on their behalf. While California is not part of the federal milk marketing system, what the federal system does has both direct and indirect impacts on California milk producers and the cooperatives they own. That is why the Alliance both attended the hearing and is now submitting this post-hearing brief on the proposals submitted prior to the hearing and the testimony given at the hearing. Butterfat value Several proposals were submitted to modify the value of butterfat in the price formulas under consideration at this hearing. The National Milk Producers Federation (NMPF) and the International Dairy Foods Association (IDFA) both proposed lowering the value of butterfat. NMPF proposed reducing the Class IV blatterfat value by six cents a pound. -

Organic Agriculture in Humboldt County, from Social Movement to Economic Development: Interviews with Organic Dairy and Row Crop Farmers

ORGANIC AGRICULTURE IN HUMBOLDT COUNTY, FROM SOCIAL MOVEMENT TO ECONOMIC DEVELOPMENT: INTERVIEWS WITH ORGANIC DAIRY AND ROW CROP FARMERS By Allyson L. Carroll A Thesis Presented to The Faculty of Humboldt State University In Partial Fulfillment of the Requirements for the Degree Master of Arts In Social Sciences August, 2006 ORGANIC AGRICULTURE IN HUMBOLDT COUNTY, FROM SOCIAL MOVEMENT TO ECONOMIC DEVELOPMENT: INTERVIEWS WITH ORGANIC DAIRY AND ROW CROP FARMERS By Allyson L. Carroll Approved by the Master's Thesis Committee: Judith Little, Major Professor Date Michael Smith, Committee Member Date Steven Hackett, Committee Member Date Selma Sonntag, Graduate Coordinator Date Christopher Hopper, Dean for Research and Graduate Studies Date ABSTRACT Organic agriculture is a concept that has evolved with its history, representing a farming method, social movement, and growing industry. Some analysts have critiqued organic agriculture as losing its grassroots soul and representing the conventional model of agriculture rather than an alternative to it. In order to ascertain current perceptions of organic agriculture from growers themselves, I interviewed 17 organic farmers in Humboldt County, California. These in-depth interviews focused on farmers’ rationale for certifying organic, values behind their farming style, associations with social movements, views of the federal regulations, and personal and regional economics. I interviewed both organic dairy and row crop farmers in order to compare groups and gain a spectrum of viewpoints. This study represents a place-based snapshot, particular to Humboldt County, California, a relatively rural and isolated area in need of viable economic development options. For the interviewed dairy farmers, organic agriculture represented a combination of an economic opportunity to maintain their multi-generational family farms combined with a farming method that reflected their existing techniques. -

BUY FRESH BUY LOCAL FOOD GUIDE Where to Find & Enjoy the Local Foods of Humboldt County

BUY FRESH BUY LOCAL FOOD GUIDE Where to find & enjoy the local foods of Humboldt County Known for its rural beauty, pristine beaches and magnificent redwoods, Humboldt County is also rich in local agriculture. Its broad and varied microclimates range from mild coastal regions to hot inland pockets, allowing for diverse, year-round agricultural production. Seasonal rains make for some of the best rangelands in the state, making cattle the foundation of niche markets in fine goat cheese, organic ice cream and sustainable grass-fed beef. Humboldt County retains a genuine farm culture due to the numerous small family-owned farms, many of them reaching back generations. Forward thinking residents and business owners proudly support local food and the many farmers’ markets. J J J This guide is designed to be your companion in discovering Humboldt County agriculture and to encourage you to buy fresh and buy local. The guide lists Humboldt County producers, farmers’ markets, CSAs, farm stands, U-picks, and food and farming organizations. Produced by the Community Alliance with Family Farmers, (CAFF) it is a brief introduction to food and farming on the North Coast; an overview of CAFF’s innovative programs; and an introduction to our Buy Fresh Buy Local campaign. All the information in this guide, and more, is available on CAFF’s Buy Fresh Buy Local website: wwwbuylocal.org or visit www.caff.org and click on the Buy Fresh Buy Local logo. Community Alliance with Family Farmers CAFF is building a movement of rural and urban people to foster family-scale agricul- ture that cares for the land, sustains local economies and promotes social justice. -

Humboldt County

HHUUMMBBOOLLDDTT CCOOUUNNTTYY AAGGRRIICCUULLTTUURREE SSUURRVVEEYY FFIINNAALL RREEPPOORRTT November 2003 Agricultural producers, landowners and the general public provide compelling insights and quantitative results on the importance of local agriculture to the economy, environment and quality of life in Humboldt County Sponsored by the Farm Bureau of Humboldt County and Humboldt State University Produced by Ben Morehead Department of Natural Resource Sciences Graduate Program, H.S.U. Humboldt County Agriculture Survey Final Report ACKNOWLEDGEMENTS Gratitude to the sponsors of this survey, the Farm Bureau of Humboldt County and Humboldt State University for financing this project. This research could not have been done without the support and endorsement of the following agricultural groups and support organizations in Humboldt County. They provided mailing lists and encouraged their members to participate. The Creamery donated ice cream gift certificates for survey participants. • Farm Bureau of Humboldt County • Humboldt – Del Norte Cattlemen’s Association • Buckeye Conservancy • North Coast Growers Association • Humboldt Creamery Association • University of California Cooperative Extension Many thanks to the dozens of community members who reviewed and edited drafts of the surveys and provided feedback for this report. Thank you to the producers and the public who took the time to participate in this survey research. Thank you to all the agricultural producers of Humboldt County. Your efforts to protect and best use the land are appreciated. Stay strong for future generations. Ben Morehead, project director. November 2003 For additional information: Katherine Ziemer, Director Farm Bureau of Humboldt County 5601 South Broadway Eureka, CA 95503 707-443-4844 Report on the internet at: www.buckeyeconservancy.org Recommended Citation: Morehead, B. -

Class Action Summary | Butter and Cheese Class Action This Is Not an Official Court Notice

dynamicsettlement.com 888.374.2033 Class Action Summary | Butter and Cheese Class Action This is not an official Court Notice. Information contained in this summary is subject to change. Case Overview: A $220 million settlement has been reached in a class action lawsuit brought against National Milk Producers Federation, Agri-Mark, Inc., Dairy Farmers of America, Inc., and Land O’Lakes, Inc. (collectively “Defendants”). The lawsuit claimed that an effort known as Cooperatives Working Together (CWT) operated a Herd Retirement Program that was a conspiracy to reduce milk output that violated the law. WHO IS ELIGIBLE TO PARTICIPATE IN THIS SETTLEMENT? Businesses and individual consumers in the United States that purchased butter and/or cheese directly from one or more of the CWT members including the Defendants, during the period from December 6, 2008 to July 31, 2013. Members of the CWT: Agri-Mark, Inc. Arkansas Dairy Associated Milk Producers Bongards Creameries Burke Milk Producers Cooperative Association Inc. Cooperative, Inc. California Dairies Inc. Cass-Clay Creamery Inc. Champlain Milk Producers Conesus Milk Producers Continental Dairy Products, Cooperative Cooperative Association, Inc. Inc. Cooperative Milk Producers Cortland Bulk Milk Dairy Farmers of America Dairylea Cooperative Inc. Dairymen's Marketing Association, Inc. Producers Cooperative Cooperative Inc. Ellsworth Cooperative Empire Keystone Farmers Cooperative First District Cooperative Foremost Farms USA Creamery Cooperative Creamery Association Humboldt Creamery Jefferson Bulk Milk Just Jersey Cooperative, Land O'Lakes, Inc. Lone Star Milk Producers Association Cooperative, Inc. Inc. Lowville Producers Dairy Magic Valley Quality Milk Manitowoc Milk Producers Maryland & Virginia Milk Massachusetts Coop. Milk Cooperative Producers, Inc. Cooperative Producers Cooperative Producers Fed. -

Handler List 2004 FINAL

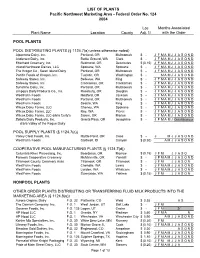

LIST OF PLANTS Pacific Northwest Marketing Area - Federal Order No. 124 2004 Loc Months Associated Plant Name Location County Adj. 1/ with the Order POOL PLANTS POOL DISTRIBUTING PLANTS (§ 1124.7(a) unless otherwise noted) Alpenrose Dairy, Inc. Portland, OR Multnomah $ - JFMAMJJASOND Andersen Dairy, Inc. Battle Ground, WA Clark $ - JFMAMJJASOND Eberhard Creamery, Inc. Redmond, OR Deschutes $ (0.15) JFMAMJJASOND Inland Northwest Dairies, LLC Spokane, WA Spokane $ - JFMAMJJASOND The Kroger Co., Swan Island Dairy Portland, OR Multnomah $ - JFMAMJJASOND Pacific Foods of Oregon, Inc. Tualatin, OR Washington$ - M A M J J A S O N D Safeway Stores, Inc. Bellevue, WA King $ - JFMAMJJASOND Safeway Stores, Inc. Clackamas, OR Clackamas $ - JFMAMJJASOND Sunshine Dairy, Inc. Portland, OR Multnomah $ - JFMAMJJASOND Umpqua Dairy Products Co., Inc. Roseburg, OR Douglas $ - JFMAMJJASOND WestFarm Foods Medford, OR Jackson $ - JFMAMJJASOND WestFarm Foods Portland, OR Multnomah $ - JFMAMJJASOND WestFarm Foods Seattle, WA King $ - JFMAMJJASOND Wilcox Dairy Farms, LLC Cheney, WA Spokane $ - JFMAMJJASOND Wilcox Dairy Farms, LLC Roy, WA Pierce $ - JFMAMJJASOND Wilcox Dairy Farms, LLC d/b/a Curly's Salem, OR Marion $ - JFMAMJJASOND Zottola Dairy Products, Inc. Grants Pass, OR Josephine $ - J F MA MJ Out of Business d/b/a Valley of the Rogue Dairy POOL SUPPLY PLANTS (§ 1124.7(c)) Valley Crest Foods, Inc. Myrtle Point, OR Coos $ - JMJJASOND WestFarm Foods Caldwell, ID Canyon $ (0.30) AMJ J ASOND COOPERATIVE POOL MANUFACTURING PLANTS (§ 1124.7(d)) Columbia River Processing, Inc. Boardman, OR Morrow $ (0.15) JFM JJASO Farmers Cooperative Creamery McMinnville, OR Yamhill $ - JFMAMJJASOND Tillamook County Creamery Assn. Tillamook, OR Tillamook $ - JFM JJASON WestFarm Foods Chehalis, WA Lewis $ - JFMAMJJASOND WestFarm Foods Lynden, WA Whatcom $ - JFMAMJJASOND WestFarm Foods Sunnyside, WA Yakima $ (0.15) JFM JJASON NONPOOL PLANTS OTHER ORDER PLANTS DISTRIBUTING OR TRANSFERRING FLUID MILK PRODUCTS INTO THE MARKETING AREA (§ 1124.8(a)) Aurora Organic Dairy F.O. -

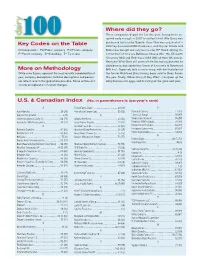

Key Codes on the Table More on Methodology Where Did They

Where did they go? Three companies depart the list this year, having been ac- quired early enough in 2007 to not be listed. Alto Dairy was Key Codes on the Table purchased last year by Saputo, Cass Clay was acquired at in 2007 by Associated Milk Producers, and Crystal Cream and C=Cooperative Pu=Public company Pr=Private company Butter was bought out early last year by HP Hood. Joining the P=Parent company S=Subsidiary T= Tie in rank list for the first time are BelGioso Cheese (No. 75), Ellsworth Creamery (84) and Roth Kase USA (96) all from Wisconsin. Next year Winn-Dixie will come off the list, having divested its dairy processing capabilities (some of it recently to Southeast More on Methodology Milk Inc.). Supervalu tells a similar story, with the final plant of While sales figures represent the most recently completed fiscal the former Richfood Dairy having been sold to Dean Foods year, company descriptions, facilities descriptions and person- this year. Finally, Wilcox Dairy of Roy, Wash., has given up the nel reflect recent changed where possible. Some entries will dairy business for eggs, and its listing will be gone next year. include an explanation of recent changes. U.S. & Canadian Index (No. in parentheses is last year’s rank) A Foster Farms Dairy ....................................... 50 (48) P Agri-Mark Inc. .............................................. 29 (29) Friendly Ice Cream Corp. ...............................55 (56) Parmalat Canada .........................................12 (13) Agropur Cooperative .........................................6 (9) G Perry’s Ice Cream ........................................ 97 (97) Anderson Erickson Dairy Co. ......................... 66 (71) Glanbia Foods Inc. ........................................ 23 (32) Plains Dairy Products ....................................95 (99) Associated Milk Producers Inc. -

County Profile

FY 2019-20 ADOPTED BUDGET SECTION B:PROFILE GOVERNANCE Assessor County Counsel Auditor-Controller Human Resources Board of Supervisors Measure Z Clerk-Recorder Other Funds County Admin. Office Treasurer-Tax Collector Demographics County Comparison Population Infrastructure Education Agriculture Employment DEMOGRAPHICS Geography Located on the far North Coast of California, 200 miles north of San Francisco and about 50 miles south of the southern Oregon border, Humboldt County is situated along the Pacific coast in Northern California’s rugged Coastal (Mountain) Ranges, bordered on the north by Del Norte County, on the east by Siskiyou and Trinity SCENERY counties, on the south by Mendocino County and on the west by the Pacific Ocean. The county encompasses 2.3 million acres, 80 percent The climate is ideal for growth of which is forestlands, protected redwoods and recreational areas. of the world’s tallest tree - the A densely forested, mountainous, rural county with about 110 miles coastal redwood. Though these of coastline, more than any other county in the state, Humboldt trees are found from southern contains over forty percent of all remaining old growth Coast Redwood Oregon to the Big Sur area of forests, the vast majority of which is protected or strictly conserved California, Humboldt County within dozens of national, state, and local forests and parks, totaling contains the most impressive approximately 680,000 acres (over 1,000 square miles). Humboldt’s collection of Sequoia highest point is Salmon Mountain at 6,962 feet. Its lowest point is sempervirens. The county is located in Samoa at 20 feet. Humboldt Bay, California’s second largest home to Redwood National natural bay, is the only deep water port between San Francisco and and State Parks, Humboldt Coos Bay, Oregon, and is located on the coast at the midpoint of the Redwoods State Park (The county. -

Loleta Creamery Research Notes Susie Van Kirk

Humboldt State University Digital Commons @ Humboldt State University Susie Van Kirk Papers Special Collections 2-2013 Loleta Creamery Research Notes Susie Van Kirk Follow this and additional works at: https://digitalcommons.humboldt.edu/svk Part of the Agriculture Commons, Architecture Commons, and the United States History Commons Recommended Citation Van Kirk, Susie, "Loleta Creamery Research Notes" (2013). Susie Van Kirk Papers. 18. https://digitalcommons.humboldt.edu/svk/18 This Article is brought to you for free and open access by the Special Collections at Digital Commons @ Humboldt State University. It has been accepted for inclusion in Susie Van Kirk Papers by an authorized administrator of Digital Commons @ Humboldt State University. For more information, please contact [email protected]. SUSIE VAN KIRK HISTORIC RESOURCES CONSULTANT P.O. BOX 568 BAYSIDE, CA 95524 707-822-6066 [email protected] LOLETA CREAMERY RESEARCH NOTES November 2011-February 2013 APN 309-123-002 281 Loleta Drive Loleta, CA 95551 Owner: Peter van der Zee P.O. Box 334 Loleta, CA 95551 Site visit with Peter and Kathleen Stanton, 11/16/11 Peter wants to remove overhang in front in order to remove tanks. His engineers have told him the door and area where glass bricks are can be "popped out" to get tanks out. Cypress Grove goat cheese plant wants the tanks. There are nine tanks, each 7000 gallons. He wants to do this soon. Next year he wants to demolish the brick storage building in back of the main building. No way to save. He needs to take it down in order to remove the PG&E transformers. -

Reporting Request for Information from U S Processors That Export To

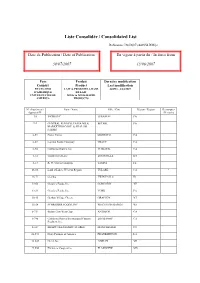

Liste Consolidée / Consolidated List Reference: D4 D(07) 440954 RM/js Date de Publication / Date of Publication: En vigeur à partir du / In force from 30/07/2007 13/08/2007 Pays Produit Dernière modification Country Product Last modification ETATS-UNIS LAIT & PRODUITS A BASE 440523 - 3/04/2007 D'AMERIQUE DE LAIT UNITED STATES OF MILK & MILK-BASED AMERICA PRODUCTS N° d’agrément / Nom / Name Ville / City Région / Region Remarques Approval N° / Remarks T4 INGRETEC LEBANON PA T-9 CENTRAL PENNSYLVANIA MILK BETHEL PA MARKETING COOP. & SHALOM FARMS 6-53 Foster Farms MODESTO CA 6-69 Leprino Foods Company TRACY CA 6-94 California Diaries, Inc. TURLOCK CA T-12 Tumbleweed LLC LOUISVILLE KY T-13 R. W. Garcia Company TAMPA FL 06-06 Land O'Lakes, Western Region TULARE CA * 16-71 Glanbia TWIN FALLS ID 33-08 Crowley Foods, Inc. CONCORD NH 42-82 Crowley Foods, Inc. YORK PA 50-15 Grafton Village Cheese GRAFTON VT 55-54 SCHREIBER FOODS, INC WISCONSIN RAPIDS WI 6-731 Brown Cow West Corp. ANTIOCH CA 6-748 California Dairies/International Custom LOS BANOS CA Products, Inc. S-367 SHADY GLEN DAIRY STORES MANCHESTER CT 22-592 Dairy Farmers of America FRANKLINTON LA 26-947 Diehl, Inc. ADRIAN MI 27-556 Plainview Cooperative PLAINVIEW MN 42-060 Crowley Foods, Inc. PHILADELPHIA PA 42-097 Crowley Foods, Inc. LANCASTER PA 46-206 ASSOCIATED MILK PRODUCERS, FREEMAN SD INC. 48-943 Burt Lewis, Inc./Associated Milk WINNSBORO TX Producers, Inc. 55-360 Foremost Farmers REEDSBURG WI 55-425 JOHN MORRELL & CO./YORKSHIRE PORTAGE WI FARM 55-648 JOHN MORRELL & CO./YORKSHIRE COMSTOCK WI FARM S-7356 MICHAEL ANGELO'S GOURMET AUSTIN TX FOODS 1011274 Schwan Food Company ATLANTA GA 1012872 McCormick ATLANTA GA 1014980 Salem Baking Company WINSTON-SALEM NC 1020084 Conagra Grocery Products Co. -

2009 Adpi/Abi Annual Conference Attendee List

2009 ADPI/ABI ANNUAL CONFERENCE ATTENDEE LIST COMPANY FIRST LAST CITY ST COUNTRY 3A Business Consulting Tage Affertsholt Aarhus C DENMARK ACSON Corporation Richard Freeland Scottsdale AZ Agri-Dairy Products, Inc. Steve Bronfield Purchase NY Agri-Dairy Products, Inc. Frank Reeves Purchase NY Agri-Dairy Products, Inc. Gabriel Sevilla Purchase NY Agri-Mark, Inc. John Costa Lawrence MA Agri-Mark, Inc. Raymond Dyke Montpelier VT Agri-Mark, Inc. Amantha Fields Lawrence MA Agri-Mark, Inc. Gale Goodwin Lawrence MA Agri-Mark, Inc. George Goodwin Lawrence MA Agri-Mark, Inc. Peter Gutierrez Lawrence MA Agri-Mark, Inc. Richard Langworthy Lawrence MA Agri-Mark, Inc. Daniel Serna Lawrence MA Agri-Mark, Inc. Richard Stammer Lawrence MA Agri-Mark, Inc. Scott Werme Lawrence MA Agropur Cooperative Reneck Cayen Longueuil QU CANADA Agropur Cooperative Sylvain Melancon Longueuil QU CANADA Alain Royer Consultant Inc. Gilles Paradis Boucherville QU CANADA Alamfoods Inc. Julia Zu Surrey BC CANADA Albus Dairy, Inc. Enrique Pedroza El Paso TX All American Dairy Products, Inc. Julie Knox Malvern PA All American Dairy Products, Inc. Paul Knox Malvern PA All American Dairy Products, Inc. Christophe Le Lan Malvern PA All American Dairy Products, Inc. Jon Olivier Malvern PA All American Dairy Products, Inc. Ed Tulskie Malvern PA All American Foods, Inc. Chad Anderson Mankato MN All American Foods, Inc. Karen Goltz Mankato MN All American Foods, Inc. Rod Mitchell Mankato MN All-Freight, LLC Gary Davis Glasgow KY American Agco Trading DJ Johnson Cottage Grove MN American Casein Company Michael Geiger Burlington NJ American Casein Company Clifford Lang Burlington NJ AMFP Inc.