To See 2014 Health Policy Survey Results

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sprouting Pinenut September 2018

1 Numa News Sprouting Pinenut September 2018 Fallon Paiute Shoshone Tribal Newsletter www.fpst.org Volume 12 Issue 9 September 2018 1 2 Laura Ijames Tribal Secretary Report [email protected] Our department participated in the Back to School Night which was held at the Fallon Convention Center. Jolene Thomas, Secretary’s Assistant, invested her time as a volunteer for the event where many backpacks and supplies given out for the new school year. It was good to see the whole community come out and support our youth. I would like to thank the FPST Co-Ed Softball team for donating their winning plaque to the tribe. Since the tribe donated to the team, they named the team after the tribe. I am glad to see that tribal donations are enriching our young adults in a positive way. If you would like to see the plaque and picture it will be in the lobby at the administration building. A successful antelope hunt The Labor Day weekend is coming soon and I hope everyone has a safe holiday weekend. Committee Openings: Land and Water Resources– 2 vacancies Senior Committee– 1 vacancies Election Committee Alternate-1vacancy Any interested Tribal Member may submit a Committee Appointment form to the FBC Secretary 3 1 4 5 1 6 7 1 8 FPST CO-ED SLOWPITCH CHAMPIONS Congratulations to the FPST Co-Ed Softball Team on their 1st place win in the Oasis Adult Softball Association League on Tuesday, August 8, 2018. The league winners received a 1st place plague as they showed why they are the top team in the league, with a big contin- gent of them tribal members. -

Vista Comparison to the Commercial Electronic Health Record Marketplace Final Report

VistA Comparison to the Commercial Electronic Health Record Marketplace Final Report February 4, 2011 Prepared for: U.S. Department of Veterans Affairs Martin Geffen Vice President Gartner Consulting [email protected] GARTNER CONSULTING This presentation, including any supporting materials, is owned by Gartner, Inc. and/or its affiliates and is for the sole use of the intended Gartner audience or other authorized recipients. This presentation may contain information that is confidential, proprietary or otherwise legally protected, and it may not be further copied, distributed or publicly displayed without the express written permission of Gartner, Inc. or its affiliates. © 2010 Gartner, Inc. and/or its affiliates. All rights reserved. Table of Contents ■ Executive Summary ■ Project Objectives and Approach ■ Electronic Health Record Systems Marketplace ■ VistA Overall Findings ■ VistA Capability Assessment ■ Appendices © 2011 Gartner, Inc. and/or its affiliates. All rights reserved. Gartner is a registered trademark of Gartner, Inc. or its affiliates. 1 Executive Summary © 2011 Gartner, Inc. and/or its affiliates. All rights reserved. Gartner is a registered trademark of Gartner, Inc. or its affiliates. 2 Objective and Approach ■ Project Objective – The Department of Veterans Affairs (VA) engaged Gartner to develop a fact-based assessment of how VistA capabilities compare to those that are found in leading commercial off-the-shelf (COTS) Electronic Health Record (EHR) products. ■ Approach – Gartner applied an evaluation framework which is based on Gartner research, Gartner‘s definition of an EHR and methodologies (e.g., Magic Quadrant, Generations Model, Hype Cycle) to compare VistA clinical functionality to that of the EHR COTS products. – The evaluation framework compared VistA capabilities to those of COTS products in three major categories: • Core Clinical Capabilities • Support for Key Care Venues • Support for select Stakeholders © 2011 Gartner, Inc. -

AC Group's 2007 Annual Report the Digital Medical Office of the Future

AC Group’s 2007 Annual Report The Digital Medical Office of the Future Computer Systems for the Physician’s Office May 2007 Comprehensive Report on: Overview of Physician adoption The Six Levels of Physician IT Maturity Practice Management Marketplace Secured Internet Document Image Management PDA and Mobile Healthcare Electronic Medical Record Functionality Electronic Medical Health Marketplace Regional Healthcare Information Organizations Mark R. Anderson, CPHIMS, FHIMSS Healthcare IT Futurist AC Group, Inc. (v) 281-413-5572 [email protected] www.acgroup.org AC Group’s 2007 Annual Report The Digital Medical Office of the Future Computer Systems for the Physician’s Office More about the Author Mr. Anderson is one of the nation's premier IT research futurists dedicated to health care. He is one of the leading national speakers on healthcare and physician practices and has spoken at more than 350 conferences and meetings since 2000. He has spent the last 30+ years focusing on Healthcare – not just technology questions, but strategic, policy, and organizational considerations. He tracks industry trends, conducts member surveys and case studies, assesses best practices, and performs benchmarking studies. Besides serving at the CEO of AC Group, Mr. Anderson served as the interim CIO for the Taconic IPA in 2004-05 (a 500 practice, 2,300+ physician IPA located in upper New York). Prior to joining AC Group, Inc. in February of 2000, Mr. Anderson was the worldwide head and VP of healthcare for META Group, Inc., the Chief Information Officer (CIO) with West Tennessee Healthcare, the Corporate CIO for the Sisters of Charity of Nazareth Health System, the Corporate Internal IT Consultant with the Sisters of Providence (SOP) Hospitals, and the Executive Director for Management Services for Denver Health and Hospitals and Harris County Hospital District. -

Semi-Annual Market Review

Semi-Annual Market Review HEALTH IT & HEALTH INFORMATION SERVICES JULY 2019 www.hgp.com TABLE OF CONTENTS 1 Health IT Executive Summary 3 2 Health IT Market Trends 6 3 HIT M&A (Including Buyout) 9 4 Health IT Capital Raises (Non-Buyout) 14 5 Healthcare Capital Markets 15 6 Macroeconomics 19 7 Health IT Headlines 21 8 About Healthcare Growth Partners 24 9 HGP Transaction Experience 25 10 Appendix A – M&A Highlights 28 11 Appendix B – Buyout Highlights 31 12 Appendix C – Investment Highlights 34 Copyright© 2019 Healthcare Growth Partners 2 HEALTH IT EXECUTIVE SUMMARY 1 An Accumulating Backlog of Disciplined Sellers Let’s chat about fireside chats. The term first used to describe a series of evening radio addresses given by U.S. President Franklin D. Roosevelt during the Great Depression and World War II is now investment banker speak for “soft launches” of sell-side and capital raise transactions. Every company has a price, and given a market of healthy valuations, more companies are testing the waters to find out whether they can achieve that price. That process now looks a little more informal, or how you might envision a fireside chat. Price (or valuation) discovery for a company can range from a single conversation with an individual buyer to a full-blown auction with hundreds of buyers and everything in between, including a fireside chat. Given the increasing share of informal conversations, the reality is that more companies are for sale than meets the eye. While the healthy valuations publicized and press-released are encouraging more and more companies to price shop, there is a simultaneous statistical phenomenon in perceived valuations that often goes unmentioned: survivorship bias. -

Private Equity Buyouts in Healthcare: Who Wins, Who Loses? Eileen Appelbaum and Rosemary Batt Working Paper No

Private Equity Buyouts in Healthcare: Who Wins, Who Loses? Eileen Appelbaum* and Rosemary Batt† Working Paper No. 118 March 15, 2020 ABSTRACT Private equity firms have become major players in the healthcare industry. How has this happened and what are the results? What is private equity’s ‘value proposition’ to the industry and to the American people -- at a time when healthcare is under constant pressure to cut costs and prices? How can PE firms use their classic leveraged buyout model to ‘save healthcare’ while delivering ‘outsized returns’ to investors? In this paper, we bring together a wide range of sources and empirical evidence to answer these questions. Given the complexity of the sector, we focus on four segments where private equity firms have been particularly active: hospitals, outpatient care (urgent care and ambulatory surgery centers), physician staffing and emergency * Co-Director and Senior Economist, Center for Economic and Policy Research. [email protected] † Alice H. Cook Professor of Women and Work, HR Studies and Intl. & Comparative Labor ILR School, Cornell University. [email protected]. We thank Andrea Beaty, Aimee La France, and Kellie Franzblau for able research assistance. room services (surprise medical billing), and revenue cycle management (medical debt collecting). In each of these segments, private equity has taken the lead in consolidating small providers, loading them with debt, and rolling them up into large powerhouses with substantial market power before exiting with handsome returns. https://doi.org/10.36687/inetwp118 JEL Codes: I11 G23 G34 Keywords: Private Equity, Leveraged Buyouts, health care industry, financial engineering, surprise medical billing revenue cycle management, urgent care, ambulatory care. -

Case Studies of Vista Implementation— United States and International

39251_CH09_223_284 11/27/06 5:26 PM Page 223 CHAPTER 9 Case Studies of VistA Implementation— United States and International “VHA’s integrated health information system, including its framework for using performance measures to improve quality, is considered one of the best in the nation.” Institute of Medicine (IOM) Report, “Leadership by Example: Coordinating Government Roles in Improving Health Care Quality, 2002” Introduction The U.S. Department of Veterans Affairs (VA) has developed and imple- mented a comprehensive health information system and EHR system known as VistA, which was built from the ground up with a clinical focus. Many of the commercial off-the-shelf (COTS) health information systems in the private sector today were designed from a financial perspective and now are being reengineered to address medical and clinical informatics requirements. The VistA system is a proven product and can be readily adapted for use in acute care, ambulatory, and long-term care settings. It has been used in public and private healthcare provider organizations across the United States and in a number of international settings. 223 39251_CH09_223_284 11/27/06 5:26 PM Page 224 224 CASE STUDIES OF VISTA IMPLEMENTATION—UNITED STATES AND INTERNATIONAL Table 9-1 VistA Software Modules VistA Software Packages Pharmacy: Inpatient Medications Health Data Systems Pharmacy: Inpatient Medications— Automated Medical Information Exchange Intravenous (IV) (AMIE) Pharmacy: Inpatient Medications— Incident Reporting Unit Dose (UD) Lexicon Utility Pharmacy: -

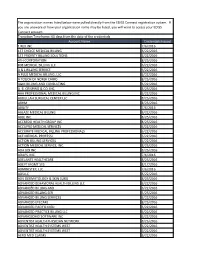

Organization Name Credentials Sent Date 1 REX INC 7/6/2016 1ST CHOICE MEDICAL BILLING 6/22/2016 1ST PRIORITY BILLING SOLUTIONS 6

The organization names listed below were pulled directly from the EDISS Connect registration system. If you are unaware of how your organization name may be listed, you will want to access your EDISS Connect account. Organization Name Credentials Sent Date 1 REX INC 7/6/2016 1ST CHOICE MEDICAL BILLING 6/22/2016 1ST PRIORITY BILLING SOLUTIONS 6/22/2016 808 MEDICAL BILLING LLC 6/22/2016 A & L BILLING SERVICE 6/22/2016 A PLUS MEDICAL BILLING, LLC 6/22/2016 A TOUCH OF NORSK CHIRO 8/3/2016 A&M BILLING AND CONSULTING 6/22/2016 A. B. CRISPINO & CO. INC. 8/3/2016 AAA PROFESSIONAL MEDICAL BILLING INC 6/22/2016 ABDULLAH SURGICAL CENTER LLC 8/3/2016 ABHM 8/3/2016 ABILITY 7/6/2016 ABLAZE MEDICAL BILLING 6/22/2016 ACCUPRO MEDICAL SERVICES 6/22/2016 ACCURATE MEDICAL BILLING PROFESSIONALS 6/22/2016 ACE MEDICAL PROFESSI 6/22/2016 ACTION BILLING SERVICES 6/22/2016 ACTION MEDICAL SERVICE, INC. 8/3/2016 ADA BOI INC 8/3/2016 ADAPS, INC. 7/6/2016 ADELANTE HEALTHCARE 8/3/2016 ADMINISTEP, LLC 7/6/2016 ADSLLC 6/22/2016 ADV DERMATOLOGY & SKIN SURG 8/3/2016 ADVANCED BEHAVIORAL HEALTH BILLING LLC 6/22/2016 ADVANCED BILLING AND 6/22/2016 ADVANCED BILLING SER 5/25/2016 ADVANCED BILLING SERVICES 6/22/2016 ADVANCED EYECARE 8/3/2016 ADVANCED PACIFIC MED 6/22/2016 ADVANCED PRACTICE BILLING LLC 6/22/2016 ADVANCEDMD SOFTWARE INC 6/22/2016 ADVENTIST HEALTH SYSTEMS WEST 6/22/2016 ADVENTIST HEALTH SYSTEMS WEST 6/22/2016 AERO MED CLAIMS 6/22/2016 AFFILIATED PROFESSIONAL SERVICES, INC. -

Account Name Credentials Issued 1 REX INC 7/6/2016 1ST CHOICE

The organization names listed below were pulled directly from the EDISS Connect registration system. If you are unaware of how your organization name may be listed, you will want to access your EDISS Connect account. Transition Timeframe: 60 days from the date of the credentials Account Name Credentials Issued 1 REX INC 7/6/2016 1ST CHOICE MEDICAL BILLING 6/22/2016 1ST PRIORITY BILLING SOLUTIONS 6/22/2016 4TH CORPORATION 8/25/2016 808 MEDICAL BILLING LLC 6/22/2016 A & L BILLING SERVICE 6/22/2016 A PLUS MEDICAL BILLING, LLC 6/22/2016 A TOUCH OF NORSK CHIRO 8/25/2016 A&M BILLING AND CONSULTING 6/22/2016 A. B. CRISPINO & CO. INC. 8/25/2016 AAA PROFESSIONAL MEDICAL BILLING INC 6/22/2016 ABDULLAH SURGICAL CENTER LLC 8/25/2016 ABHM 8/25/2016 ABILITY 7/6/2016 ABLAZE MEDICAL BILLING 6/22/2016 ABLE INC. 8/25/2016 ACCREDO HEALTH GROUP INC 8/25/2016 ACCUPRO MEDICAL SERVICES 6/22/2016 ACCURATE MEDICAL BILLING PROFESSIONALS 6/22/2016 ACE MEDICAL PROFESSI 6/22/2016 ACTION BILLING SERVICES 6/22/2016 ACTION MEDICAL SERVICE, INC. 8/25/2016 ADA BOI INC 8/25/2016 ADAPS, INC. 7/6/2016 ADELANTE HEALTHCARE 8/25/2016 ADEPT MGMT SYS 8/17/2016 ADMINISTEP, LLC 7/6/2016 ADSLLC 6/22/2016 ADV DERMATOLOGY & SKIN SURG 8/25/2016 ADVANCED BEHAVIORAL HEALTH BILLING LLC 6/22/2016 ADVANCED BILLING AND 6/22/2016 ADVANCED BILLING SER 5/25/2016 ADVANCED BILLING SERVICES 6/22/2016 ADVANCED EYECARE 8/25/2016 ADVANCED PACIFIC MED 6/22/2016 ADVANCED PRACTICE BILLING LLC 6/22/2016 ADVANCEDMD SOFTWARE INC 6/22/2016 ADVENTIST HEALTH PHYSICIAN NETWORK 8/25/2016 ADVENTIST HEALTH SYSTEMS WEST 6/22/2016 ADVENTIST HEALTH SYSTEMS WEST 6/22/2016 AERO MED CLAIMS 6/22/2016 AFFILIATED PROFESSIONAL SERVICES, INC. -

Open Platform Architecture Based Upon SMART Apps Platform and the HL7 FHIR® (DSTU) Demonstrated at HIMSS14

MAY 2014 Open Platform Architecture Based Upon SMART Apps Platform and the HL7 FHIR® (DSTU) Demonstrated at HIMSS14 By David Kreda, Translation Advisor, and Joshua Mandel MD, Lead Architect, SMART Platforms Project Harvard Medical School/Children’s Hospital Boston www.smartplatforms.org During the HIMSS14 Annual Conference (Feb- ferent internal architectures ruary 23-27, 2014 in Orlando, Florida), several and technologies, they healthcare IT exhibitors presented an eye-open- were nonetheless able to ing example of the potential of HL7’s newest supply the data via FHIR standard, FHIR® (Fast Healthcare Interoperabil- API calls made by the suite David Kreda ity Resources). The list of exhibitors included of SMART Apps that were Cerner, Intermountain Healthcare, Hewlett Pack- installed on their systems. ard, and Harris Corporation. They presented the Harris Corporation then SMART on FHIR Open Platform Architecture, demonstrated its services which combines FHIR and the open source, web- oriented architecture (SOA) standards based technology stack created by the service, which accepted SMART Platforms Project, a research effort based same FHIR API queries at Harvard Medical School and Children’s Hos- from the SMART apps, fed- pital Boston that enables real-time integration of erated queries to the same substitutable medical apps, or SMART apps, on EHR systems holding the EHR systems. patient data, and synthe- Josh Mandel, MD sized a cross system, longi- Three sophisticated EHR systems, including tudinal patient record, which was returned to the Cerner Millennium, HELP2 from Intermountain requesting SMART app. Healthcare, and VistA from the Veterans Health Administration, were each independently FHIR- Hewlett Packard, which engineered the SMART enabled in less than six weeks. -

2901121 Safer Hospitals, Safer Wards

The NHS England Putting business plan for Patients First 2013/14 – 2015/16 SUPPORTING, DEVELOPING AND ASSURING THE DIRECT COMMISSIONING COMMISSIONING SYSTEM PARTNERSHIP STRATEGY, FOR RESEARCH Achieving an AND SAFER HOSPITALS INNOVATION integrated digital FOR OUTCOMES SAFER WARDS careEMERGENCY record AND PREPAREDNESS QUALITY GROWTH WORLD WORLD CLASS CLASS CUSTOMER CLINICAL SERVICE: DEVELOPING AND INFORMATION, CUSTOMER PROFESSIONAL TRANSPARENCY COMMISSIONING AND SUPPORT SERVICE: LEADERSHIP PARTICIPATION UNITS INFORMATION, PEOPLE ACCESSING TRANSPARENCY THEIR AND DATA PARTICIPATION RIGHT DATA, NHS NUMBER: RIGHT PLACE, RIGHT TIME INTEGRATING CARE COMMUNITY OF PRACTICE High quality care for all, now and for future generations NHS England INFORMATION READER BOX Directorate Medical Operations Patients and Information Nursing Policy Commissioning Development Finance Human Resources Publications Gateway Reference: 00201 Document Purpose Guidance and launch of the Safer Hospitals, Safer Wards Technology Fund Document Name Safer Hospitals, Safer Wards: Achieving an Integrated Digital Care Record Author NHS England Publication Date 01 July 2013 Target Audience Foundation Trust CEs, Foundation Trust Board Chairs, NHS Trust CEs, NHS Trust Board Chairs, Medical Directors, Directors of Nursing, Directors of Finance, NHS England Regional Directors, NHS England Area Directors Additional Circulation List CCG Clinical Leaders, CCG Accountable Officers, CSU Managing Directors, Local Authority CEs, Directors of Adult SSs, Academic Health Science Networks Description This document sets out the benefits case for adopting safe digital record keeping as a precursor to achieving integrated digital care records across the health and care system. It provides further details and support for NHS Trusts, including Foundation Trusts, relating to their progress from paper to paper-light and ultimately paperless record keeping. -

FINAL REPORT APPENDICES -- Assessing the SHARP Experience

FINAL REPORT APPENDICES Assessing the SHARP Experience JULY 2014 PRESENTED TO: PRESENTED BY: Dustin Charles NORC at the Office of the National Coordinator University of Chicago for Health Information Technology Adil Moiduddin U.S. Department of Health and Human Vice President, Health Care Research Services 55 East Monroe Street 200 Independence Avenue S.W. 30th Floor Suite 729-D Chicago, IL 60603 Washington, D.C. 20201 (312) 759-4000 (202) 690-7151 NORC | Assessing the SHARP Experience Table of Contents Appendix A. SHARP Vision Paper (March 2012) ..................................................................... 1 Appendix B. Awardee Overview............................................................................................. 15 Appendix C. SHARP Output Inventory .................................................................................. 17 Appendix D. Count by Output Type ....................................................................................... 63 Appendix E. Site Visit Summary for SHARPS ....................................................................... 64 Appendix F. Site Visit Summary for SHARPc ....................................................................... 85 Appendix G. Site Visit Summary for SMART ....................................................................... 104 Appendix H. Site Visit Summary for SHARPn ..................................................................... 123 Appendix I. Closing Discussion Participants ..................................................................... -

Images, Electronic Health Records, and Meaningful Use: a Vision For

Images, Electronic Health Records, and Meaningful Use: A Vision for the Future January 10–11, 2011 Bethesda, Maryland Executive Summary, Discussions, and Recommendations EXECUTIVE SUMMARY: MOVING TOWARD MULTIMEDIA ELECTRONIC HEALTH RECORDS: HOW DO WE GET THERE? The National Institute of Biomedical Imaging and Bioengineering (NIBIB) and the Office of the National Coordinator for Health Information Technology (ONC) co-sponsored a workshop in January 2011 to consider the opportunities and implications for health care when electronic health records (EHRs) contain multimedia data. The workshop provided a venue for a diverse group of stakeholders to share their vision and perspectives on both technical and practical implementation issues and how these issues may inform the future development of the definition of Meaningful Use of Electronic Health Records under the Health Information Technology for Economic and Clinical Health Act, 2009. The meeting was specifically not for policy development regarding Meaningful Use. Drawing from this diverse group of health care providers, patient advocates, health system leaders, payers, and commercial vendors, this workshop report presents a summary of their viewpoints and concludes with possible pathways toward multimedia electronic health records. When considering meaningful use of images, participants considered it important to focus on the goal of creating value and efficiency in health care and that health outcome should be the driving force toward that goal. Participants also recognized that electronic health records should be patient-centered and controlled. While safeguarding patient privacy, they also note that it is crucial to be able to access health information regardless of location to enable care providers to make decisions based on comprehensive, relevant data on the patient, including image data, at the point of care.