Toronto North and East Office Market Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

ELECTORAL DISTRICTS Proposal for the Province of Ontario Published

ELECTORAL DISTRICTS Proposal for the Province of Ontario Published pursuant to the Electoral Boundaries Readjustment Act Table of Contents Preamble ......................................................................................................................................... 3 Process for Electoral Readjustment ................................................................................................ 3 Notice of Sittings for the Hearing of Representations .................................................................... 4 Requirements for Making Submissions During Commission Hearings ......................................... 5 Rules for Making Representations .................................................................................................. 6 Reasons for the Proposed Electoral Boundaries ............................................................................. 8 Schedule A – Electoral District Population Tables....................................................................... 31 Schedule B – Maps, Proposed Boundaries and Names of Electoral Districts .............................. 37 2 FEDERAL ELECTORAL BOUNDARIES COMMISSION FOR THE PROVINCE OF ONTARIO PROPOSAL Preamble The number of electoral districts represented in the House of Commons is derived from the formula and rules set out in sections 51 and 51A of the Constitution Act, 1867. This formula takes into account changes to provincial population, as reflected in population estimates in the year of the most recent decennial census. The increase -

The Historical Development of Agricultural Policy and Urban Planning in Southern Ontario

Settlement, Food Lands, and Sustainable Habitation: The Historical Development of Agricultural Policy and Urban Planning in Southern Ontario By: Joel Fridman A thesis submitted in conformity with the requirements for the degree of Masters of Arts in Geography, Collaborative Program in Environmental Studies Department of Geography and Program in Planning University of Toronto © Copyright by Joel Fridman 2014 Settlement, Food Lands, and Sustainable Habitation: The Historical Development of Agricultural Policy and Urban Planning in Southern Ontario Joel Fridman Masters of Arts in Geography, Collaborative Program in Environmental Studies Department of Geography and Program in Planning University of Toronto 2014 Abstract In this thesis I recount the historical relationship between settlement and food lands in Southern Ontario. Informed by landscape and food regime theory, I use a landscape approach to interpret the history of this relationship to deepen our understanding of a pertinent, and historically specific problem of land access for sustainable farming. This thesis presents entrenched barriers to landscape renewal as institutional legacies of various layers of history. It argues that at the moment and for the last century Southern Ontario has had two different, parallel sets of determinants for land use operating on the same landscape in the form of agricultural policy and urban planning. To the extent that they are not purposefully coordinated, not just with each other but with the social and ecological foundations of our habitation, this is at the root of the problem of land access for sustainable farming. ii Acknowledgements This thesis is accomplished with the help and support of many. I would like to thank my supervisor, Professor Harriet Friedmann, for kindly encouraging me in the right direction. -

City of Toronto — Detached Homes Average Price by Percentage Increase: January to June 2016

City of Toronto — Detached Homes Average price by percentage increase: January to June 2016 C06 – $1,282,135 C14 – $2,018,060 1,624,017 C15 698,807 $1,649,510 972,204 869,656 754,043 630,542 672,659 1,968,769 1,821,777 781,811 816,344 3,412,579 763,874 $691,205 668,229 1,758,205 $1,698,897 812,608 *C02 $2,122,558 1,229,047 $890,879 1,149,451 1,408,198 *C01 1,085,243 1,262,133 1,116,339 $1,423,843 E06 788,941 803,251 Less than 10% 10% - 19.9% 20% & Above * 1,716,792 * 2,869,584 * 1,775,091 *W01 13.0% *C01 17.9% E01 12.9% W02 13.1% *C02 15.2% E02 20.0% W03 18.7% C03 13.6% E03 15.2% W04 19.9% C04 13.8% E04 13.5% W05 18.3% C06 26.9% E05 18.7% W06 11.1% C07 29.2% E06 8.9% W07 18.0% *C08 29.2% E07 10.4% W08 10.9% *C09 11.4% E08 7.7% W09 6.1% *C10 25.9% E09 16.2% W10 18.2% *C11 7.9% E10 20.1% C12 18.2% E11 12.4% C13 36.4% C14 26.4% C15 31.8% Compared to January to June 2015 Source: RE/MAX Hallmark, Toronto Real Estate Board Market Watch *Districts that recorded less than 100 sales were discounted to prevent the reporting of statistical anomalies R City of Toronto — Neighbourhoods by TREB District WEST W01 High Park, South Parkdale, Swansea, Roncesvalles Village W02 Bloor West Village, Baby Point, The Junction, High Park North W05 W03 Keelesdale, Eglinton West, Rockcliffe-Smythe, Weston-Pellam Park, Corso Italia W10 W04 York, Glen Park, Amesbury (Brookhaven), Pelmo Park – Humberlea, Weston, Fairbank (Briar Hill-Belgravia), Maple Leaf, Mount Dennis W05 Downsview, Humber Summit, Humbermede (Emery), Jane and Finch W09 W04 (Black Creek/Glenfield-Jane -

Trailside Esterbrooke Kingslake Harringay

MILLIKEN COMMUNITY TRAIL CONTINUES TRAIL CONTINUES CENTRE INTO VAUGHAN INTO MARKHAM Roxanne Enchanted Hills Codlin Anthia Scoville P Codlin Minglehaze THACKERAY PARK Cabana English Song Meadoway Glencoyne Frank Rivers Captains Way Goldhawk Wilderness MILLIKEN PARK - CEDARBRAE Murray Ross Festival Tanjoe Ashcott Cascaden Cathy Jean Flax Gardenway Gossamer Grove Kelvin Covewood Flatwoods Holmbush Redlea Duxbury Nipigon Holmbush Provence Nipigon Forest New GOLF & COUNTRY Anthia Huntsmill New Forest Shockley Carnival Greenwin Village Ivyway Inniscross Raynes Enchanted Hills CONCESSION Goodmark Alabast Beulah Alness Inniscross Hullmar Townsend Goldenwood Saddletree Franca Rockland Janus Hollyberry Manilow Port Royal Green Bush Aspenwood Chapel Park Founders Magnetic Sandyhook Irondale Klondike Roxanne Harrington Edgar Woods Fisherville Abitibi Goldwood Mintwood Hollyberry Canongate CLUB Cabernet Turbine 400 Crispin MILLIKENMILLIKEN Breanna Eagleview Pennmarric BLACK CREEK Carpenter Grove River BLACK CREEK West North Albany Tarbert Select Lillian Signal Hill Hill Signal Highbridge Arran Markbrook Barmac Wheelwright Cherrystone Birchway Yellow Strawberry Hills Strawberry Select Steinway Rossdean Bestview Freshmeadow Belinda Eagledance BordeauxBrunello Primula Garyray G. ROSS Fontainbleau Cherrystone Ockwell Manor Chianti Cabernet Laureleaf Shenstone Torresdale Athabaska Limestone Regis Robinter Lambeth Wintermute WOODLANDS PIONEER Russfax Creekside Michigan . Husband EAST Reesor Plowshare Ian MacDonald Nevada Grenbeck ROWNTREE MILLS PARK Blacksmith -

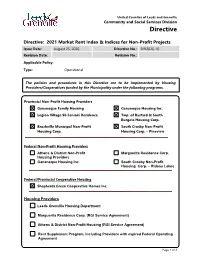

2021 Market Rent Index & Indices for Non-Profit Projects

United Counties of Leeds and Grenville Community and Social Services Division Directive Directive: 2021 Market Rent Index & Indices for Non-Profit Projects Issue Date: August 25, 2020 Directive No.: DIR2020-10 Revision Date: Revision No.: Applicable Policy: Type: Operational The policies and procedures in this Directive are to be implemented by Housing Providers/Cooperatives funded by the Municipality under the following programs. Provincial Non-Profit Housing Providers Gananoque Family Housing Gananoque Housing Inc. Legion Village 96 Seniors Residence Twp. of Bastard & South Burgess Housing Corp. Brockville Municipal Non-Profit South Crosby Non-Profit Housing Corp. Housing Corp. – Pineview Federal Non-Profit Housing Providers Athens & District Non-Profit Marguerita Residence Corp. Housing Providers Gananoque Housing Inc. South Crosby Non-Profit Housing Corp. – Rideau Lakes Federal/Provincial Cooperative Housing Shepherds Green Cooperative Homes Inc. Housing Providers Leeds Grenville Housing Department Marguerita Residence Corp. (RGI Service Agreement) Athens & District Non-Profit Housing (RGI Service Agreement) Rent Supplement Program, including Providers with expired Federal Operating Agreement Page 1 of 3 United Counties of Leeds and Grenville Community and Social Services Division Directive Directive: 2021 Market Rent Index & Indices for Non-Profit Projects Issue Date: August 25, 2020 Directive No.: DIR2020-10 Revision Date: Revision No.: BACKGROUND Each year, the Ministry provides indices for costs and revenues to calculate subsidies under the Housing Services Act (HSA). The indices to be used for 2021 are contained in this directive. PURPOSE The purpose of this directive is to advise housing providers of the index factors to be used in the calculation of subsidy for 2021. ACTION TO BE TAKEN Housing providers shall use the index factors in the table below to calculate subsidies under the Housing Services Act, 2011 (HSA) on an annual basis. -

The North York East LIP Strategic Plan and Report

The North York East LIP Strategic Plan and Report The North York East Strategic Plan has been developed around six areas of focus: Information & Outreach; Civic Engagement; Collaboration & Capacity Building; Language Training & Supports; Labour Market; and Health Services.Six working groups will be established to address these areas of focus. In- depth directions for each working group are outlined in the main body of this report Executive Summary In 2009, Citizenship and Immigration Canada (CIC), in partnership with the Ontario Ministry of Citizenship and Immigration, launched Local Immigration Partnership (LIP) projects throughout Ontario. LIPs were developed as research initiatives to identify ways to coordinate and enhance local service delivery to newcomers across the province, while promoting efficient use of resources. In October 2009, Working Women Community Centre entered an agreement with CIC to lead a LIP project in the North York East area of Toronto. The North York East LIP is located in the far north of the city, contained by Steeles Avenue to the north, Highway 401 to the south, Victoria Avenue East to the east and the Don Valley River to the west. The area population is almost 80,000, 70% of which are immigrants to Canada. A major priority for the North York East LIP project was to root its research in the real-life experiences of local newcomers and local community organizations. In total, over 400 newcomers & immigrants, and over 100 service providers were consulted and engaged with to identify challenges, solutions and new directions for the settlement sector in the area. Methods of engagement for both newcomers and service providers included focus group research, key-informant interviews, community consultations and advisory panel workshops. -

City Planning Phone Directory

City Planning 1 City Planning City Planning provides advice to City Council on building issues. The division undertakes complex research projects, which lead to policy development in land use, environmental sustainability, community development, urban design and transportation. City Planning reviews development applications and recommends actions on these matters to Community Councils and the Planning and Transportation Committee. The division administers the Committee of Adjustment and provides expert planning advice to four Committee panels. Toronto City Hall Director 12th fl. E., 100 Queen St. W. Neil Cresswell ....................................... 394-8211 Toronto ON M5H 2N2 Administrative Assistant Annette Sukhai ...................................... 394-8212 Facsimile - General ..................................... 392-8805 Central Section (Wards 1, 2, 4, 6 – East of Royal York) - Chief Planner’s Office .............. 392-8115 Manager Bill Kiru ................................................. 394-8216 Administrative Assistant Chief Planner & Executive Director Kelly Allen ............................................ 394-8234 Jennifer Keesmaat ................................. 392-8772 Senior Planner Administrative Assistant Carly Bowman ....................................... 394-8228 Helen Skouras ........................................ 392-8110 Kathryn Thom ....................................... 394-8214 Adriana Suyck ....................................... 392-5217 Planner Program Manager Ellen Standret ....................................... -

18 Wynford Drive Professional Office/Medical Building

18 Wynford Drive Professional Office/Medical Building Ariel Stern, Broker 416.649.5925 [email protected] For Lease: Office/Medical Here is where your business will grow. 200-55 University Avenue, Toronto 416.649.5920 • lennard.com 18 Wynford Drive Welcoming and radiant professional office/medical building availabe for lease on the corner of Wynford and Gervais Drive off Don Mills Road Suites Leasing Agent Unit 705/706 Ariel Stern Broker Available Space 416.649.5925 2,024 SF [email protected] Net Rent $15.00 PSF Suites Availability Unit 703/704 May 1, 2020 Available Space 2,189 SF Term Net Rent 3 to 5 years $20.00 PSF Additional Rent $12.00 PSF Commission $1.25 PSF/annum Property Highlights • Professional office/medical building • Onsite cafe and pharmacy • Paid surface parking, or Two (2) underground parking spots at $60/month each • Quick access to DVP and Public Transit lennard.com 18 Wynford Drive What’s Near By • Aga Khan Museum • CF Shops at Don Mills • Ontario Science Centre • Easy access to transit & DVP Statements and information contained are based on the information furnished by principals and sources which we deem reliable but for which we can assume no responsibility. Lennard Commercial Realty, Brokerage 2019. Ariel Stern, Broker 416.649.5925 • [email protected] lennard.com 18 Wynford Drive Floor Plan: 705-706 Ariel Stern, Broker 416.649.5925 • [email protected] lennard.com 18 Wynford Drive Floor Plan: 703 - 704 Ariel Stern, Broker 416.649.5925 • [email protected] lennard.com 18 Wynford Drive Units 705 - 706 Ariel Stern, Broker 416.649.5925 • [email protected] lennard.com 18 Wynford Drive Units 703 - 704 Ariel Stern, Broker 416.649.5925 • [email protected] lennard.com. -

Area 83 Eastern Ontario International Area Committee Minutes June 2

ALCOHOLICS ANONYMOUS AREA 83 EASTERN ONTARIO INTERNATIONAL Area 83 Eastern Ontario International Area Committee Minutes June 2, 2018 ACM – June 2, 2018 1 ALCOHOLICS ANONYMOUS AREA 83 EASTERN ONTARIO INTERNATIONAL 1. OPENING…………………………………………………………………………….…………….…4 2. REVIEW AND ACCEPTANCE OF AGENDA………………………………….…………….…...7 3. ROLL CALL………………………………………………………………………….……………….7 4. REVIEW AND ACCEPTANCE OF MINUTES OF September 9, 2017 ACM…………………7 5. DISTRICT COMMITTEE MEMBERS’ REPORTS ……………………………………………....8 District 02 Malton……………………………………………………………………………….…….. 8 District 06 Mississauga……………………………………………………………………….…….. 8 District 10 Toronto South Central…………………………………………………………….….…. 8 District 12 Toronto South West………………………………………………………………….…. 9 District 14 Toronto North Central………………………………………………………………..….. 9 District 16 Distrito Hispano de Toronto…………………………………………………….………..9 District 18 Toronto City East……………………………………………………………………........9 District 22 Scarborough……………………………………………………………………………… 9 District 26 Lakeshore West………………………………………………………………….……….10 District 28 Lakeshore East……………………………………………………………………………11 District 30 Quinte West…………………………………………………………………………….. 11 District 34 Quinte East……………………………………………………………………………… 12 District 36 Kingston & the Islands……………………………………………………………….… 12 District 42 St. Lawrence International………………………………………………………………. 12 District 48 Seaway Valley North……………………………………………………………….……. 13 District 50 Cornwall…………………………………………………………………………………… 13 District 54 Ottawa Rideau……………………………………………………………………………. 13 District 58 Ottawa Bytown…………………………………………………………………………… -

Orking Rough, Living Poor

Working Rough, Living Poor Employment and Income Insecurities faced by Racialized Groups and their Impacts on Health Published by Access Alliance Multicultural Health and Community Services, 2011 Study funded by: To be cited as: Wilson, R.M., P. Landolt, Y.B. Shakya, G. Galabuzi, Z. Zahoorunissa, D. Pham, F. Cabrera, S. Dahy, and M-P. Joly. (2011). Working Rough, Living Poor: Employment and Income Insecurities Faced by Racialized Groups in the Black Creek Area and their Impacts on Health. Toronto: Access Alliance Multicultural Health and Community Services. The content for this report was collaboratively analyzed and written by the core team of the Income Security, Race and Health research working group. The research was designed and implemented with valuable feedback from all our Advisory Committee members and other community partners (see list in Acknowledgement section) The views expressed in this report do not necessarily represent the views of The Wellesley Institute or the Metcalf Foundation. Requests for permission and copies of this report should be addressed to: Access Alliance Multicultural Health and Community Services 500-340 College Street Toronto, ON M5S 3G3 Telephone: (416) 324-8677 Fax: (416) 324-9074 www.accessalliance.ca © 2011 Access Alliance Multicultural Health and Community Services About the Income Security, Race and Health Research Working Group The Income Security, Race and Health (ISRH) Research Working Group is a interdisciplinary research group comprising of academics, service providers, and peer researchers interested in examining racialized economic and health inequalities. The group was established in Toronto in 2006 under the leadership of Access Alliance. The key goals of the ISRH team are to investigate the systemic causes of growing racialized inequalities in employment and income, and to document the health impacts of these inequalities. -

Toronto North & East Office Market Report

Fourth Quarter 2019 / Office Market Report Toronto North & East Photo credit: York Region Quick Stats Collectively, the Toronto North and East office with 66,500 sf – lifting the overall market and 11.6% markets finished the fourth quarter and 2019 offsetting losses in the Yorkdale and Dufferin Overall availability rate in Toronto in positive territory. Combined occupancy and Finch nodes. SmartCentres’ mixed-use North, vs. 10.2% one year ago levels increased 358,000 square feet (sf) PWC-YMCA tower on Apple Mill Rd. in the with class B buildings in the East and class A Vaughan Metropolitan Centre (103,000 sf 10% buildings in the North making up the bulk of office space) opened for occupancy in Vaughan sublet available space of the gain. Quarter-over-quarter, overall November with PWC taking possession of four as a percentage of total available availability rose 30 basis points (bps) to 11.9%, floors (77,000 sf) for 230-plus employees. space while vacancy held steady at 7.2%. Available sublet space also remained flat, at 903,000 sf, The North market’s overall availability 190,800 sf as gains in the East market balanced losses jumped 130 bps quarter-over-quarter to Total new office area built in the 11.6% and sits 140 bps higher than one year Toronto North and East markets in the North. The East had an exceptionally during 2019 – all in Vaughan strong showing in 2019, as occupancy ago. This was largely attributed to RioCan increased 455,000 sf year-over-year. It was also REIT marketing a 99,000-sf contiguous block 5 a year of big lease transactions including: Bell over six floors (currently occupied by BMO Buildings with largest contiguous Canada (445,000 sf), Scotiabank (406,000 sf), Financial) at 4881 Yonge St. -

Community Conversations: North York West Sub-Region

Central LHIN System Transformation Sub-region Planning Community Conversations: North York West Sub-region April 5, 2017 Setting the Stage for Today’s Discussions Kick off sub-region planning & share the Central LHIN strategy; Bring sub-region communities together to strengthen relationships through collaborative networking; Listen and reflect upon experiences of patients and providers as they move through the system; Create a common understanding of sub-regional attributes related to their communities and populations; Generate greater context of sub-region needs and attributes through collaborative discussion; Set the stage to co-create the system collectively to identify gaps in care continuity during transitions 2 Central LHIN Community Conversation North York West Sub-region Agenda Time Item Presenters 7:45 to 8:30 am Registration & Light Refreshments Sub Region Community Wall 8:30 am Overview of the Day Welcome & Kick Off Kim Baker Central LHIN Sub-region Strategy: Transitions Chantell Tunney 9:50 am Sharing Experiences in Care Guest Speaker: Central LHIN Resident Cottean Lyttle Guest Speaker: Care Provider Dr. Jerome Liu 9:50 pm BREAK 10:00 am Building a Foundation: Information Eugene Wong 11:00 am Filling in the Gaps Group Work 11:25 am Wrap Up & Next Steps Chantell Tunney 3 Integrated Health Service Plan 2016 - 2019 4 Sub-region Strategy Building momentum, leveraging local strengths and co-designing innovative approaches to care continuity 5 Population Health – What does it mean to take a Population Health approach? Population health allows us to address the needs of the entire population, while reminding us that special attention needs to be paid to existing disparities in health.