PHILLIPS 66 (NYSE: PSX) October 30, 2020, at 12 P.M

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2019 Annual Report Are Commission-Free

Table of Contents 1 Letter to Our Shareholders 4 Financial Highlights 6 Our Businesses Midstream Chemicals Refining Marketing and Specialties 7 Our Value Chain 8 Our Strategy Operating Excellence Growth Returns Distributions High-Performing Organization 28 Board of Directors 30 Executive Leadership Team 31 Non-GAAP Reconciliations 32 Form 10-K | ON THE COVER AND TABLE OF CONTENTS Lake Charles Refinery WESTLAKE, LA In 2019, Lake Charles Manufacturing Complex achieved a sustained safety record of more than 55 months, equivalent to 7.5 million safe work hours. 2019 PHILLIPS 66 ANNUAL REPORT 1 To Our Shareholders We have the right strategy in place to create shareholder value, and our employees are executing it well. Phillips 66 achieved 34% total shareholder return during 2019, which exceeded our peer group average and the S&P 100. In 2019, we delivered earnings of $3.1 billion and earnings per share of $6.77. Adjusted earnings were $3.7 billion or $8.05 per share. During the year, we generated $4.8 billion of operating cash flow. We reinvested $3.9 billionback into the business and returned $3.2 billion of capital to shareholders through dividends and share repurchases. We increased our quarterly dividend 12.5% and announced a $3 billion increase to our share repurchase program. Since our formation, we have returned $26 billion to shareholders through dividends, share repurchases and exchanges, reducing our initial shares outstanding by 33%. Operating excellence is our No. 1 priority and core to everything we do. Our goal is zero incidents, zero accidents and zero injuries. We believe this is attainable, and we strive for it daily. -

Report Document

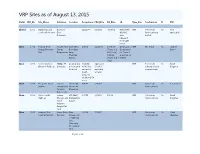

VRP Sites as of August 13, 2015 Status VRP_No. Site_Name Volunteer Location Acceptance DatePRA_Date RA_Date LA Type_Site Contaminant IC PM Closed 1001 Rail siding and Big Horn 12/11/00 3/26/02 3/26/02 NFA Letter VRP Petroleum No Not coal load out area Coal 4/26/02; hydrocarbons, applicable Company area metals released from LQD bond Open 1002 Powder River Powder River 1095 West 1/8/01 10/17/01 10/01/07 Certificate of VRP Oil, diesel No Jaymee Energy Sheridan Energy Brundage (Tracts 8, 9, Completion Binion Site Corporation Lane, & 10 only), for Tracts 8, Sheridan, 5/18/09 9, and 10 on 82801 (Tracts 6 & 7 5/8/09 only) Open 1003 Former Conoco Phillips 66 Located 1/2 3/19/01; Approved VRP Petroleum No Sarah Glenrock Refinery Company mile west of 6/28/2011 5/13/02; refinery related Bargsten Glenrock amended amended contaminants South 9/19/02 property additional 54 acres Open 1004 Cheyenne Crude Suncor 199 South 4/4/01 5/30/06 VRP Petroleum No Ben Luckey Station Energy USA, Morrie Av, hydrocarbons formerly Cheyenne Conoco Inc. Open 1005 Union Pacific Former 543 West 4/4/01 7/31/03 1/3/05 VRP Petroleum No Sarah Railroad Chicago and Midwest Av, Hydrocarbons Bargsten North Casper Western Casper Rail Yard Open 1006 Laramie Yard Union Pacific Near 4/4/01 7/09/04 VRP Petroleum No Cindi Fueling Platform Railroad intersection Hydrocarbons Martinez of Railroad and University St., Laramie Yard Page 1 of 29 Status VRP_No. Site_Name Volunteer Location Acceptance DatePRA_Date RA_Date LA Type_Site Contaminant IC PM Closed 1007 Gulley Enterprises Cheyenne 411 E. -

2020 Fact Book 2 Our Businesses Our Strategy Midstream Chemicals Refining Marketing and Specialties Energy Research & Innovation Global Asset Map General Information

Cover Photo: Taft Storage Facility at Gray Oak Pipeline TAFT, TX Contents 3 4 5 OUR BUSINESSES OUR STRATEGY MIDSTREAM Ferndale Ferndale Rail Terminal* Renton North Spokane Tacoma (MT) Yellowstone Cut Bank Moses Lake Thompson 17Falls Rail 24 14 Spokane Terminal Palermo* UROPE DLE EA Portland D Great Falls E I ST Portland (MT) Missoula Rail Terminal M Yello Glacier Sacagawea* Missoula wsto Helena Roundup Keene CDP* ne Billings Crude* Bozeman Billings Billings Humber SPCo & S-Chem ooth Sheridan* Semino Bakk Beart en Bayway MiRO CHEMICALS REFINING * MARKETING AND SPECIALTIES Bighorn e* Linden* Q-Chem I & II Casper* Tremley Pt. (MT)* * Po Rock Springs wd Bayway Rail eminoe er Ri Terminal* S Harbor Red Line Oil North Salt Lake Pioneer ve Des Moines s r Sacramento Rockies Expr Hartford Lincoln ess Line 20 ess Richmond (MT) Rockies Expr San Francisco Denver Borg Conway Kansas City* Po 0 Rockies Expres to Wichita wd Paola er-Den Gold Line* Wood River er Riv Wichita N.* Products* HeartlandPaola* Blue Line 0 Wichita S.* E. St. ver Jeerson City* Junction er Louis* Southern Hills* m Cherokee North* r*Hartford* Line 30 re Line 40 ol Standish* La Junta * h Ponca City* Explo his Ponca City ld Line C Crude* Go 0 Los Angeles Medford* eeMount Vernon* ok t Los Angeles Borger CherEas Torrance Cherokee Colton Borger to Amarillo* Blue LineSouth* Glenpool* Ponca Selmer Line O* * CushPo* Albuquerque* K PL Sk AC ATA Line* elly ST Cushing City SA Oklahoma City* Amarillo* -Belvieu Los Angeles AL Borger Oklahoma Crude* * Explor Wichita Falls* Lubbock* Savannah North -

Investor Update February 2018

Investor Update February 2018 NYSE: PSX www.phillips66.com Lake Charles Refinery Cautionary Statement This presentation contains certain forward-looking statements. Words and phrases such as “is anticipated,” “is estimated,” “is expected,” “is planned,” “is scheduled,” “is targeted,” “believes,” “intends,” “objectives,” “projects,” “strategies” and similar expressions are used to identify such forward-looking statements. However, the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements relating to the operations of Phillips 66 and Phillips 66 Partners LP (including their respective joint venture operations) are based on management’s expectations, estimates and projections about these entities, their interests and the energy industry in general on the date this presentation was prepared. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict. Therefore, actual outcomes and results may differ materially from what is expressed or forecast in such forward-looking statements. Factors that could cause actual results or events to differ materially from those described in the forward-looking statements can be found in filings that Phillips 66 and Phillips 66 Partners LP make with the Securities and Exchange Commission. Phillips 66 and Phillips 66 Partners LP are under no obligation (and expressly disclaim any such obligation) to update or alter these forward-looking statements, whether as a result of new information, future events or otherwise. This presentation includes non-GAAP financial measures. You can find the reconciliations to comparable GAAP financial measures at the end of the presentation materials or in the “Investors” section of the websites of Phillips 66 and Phillips 66 Partners LP. -

Billings Area Emergency Response Action Plan

BILLINGS AREA EMERGENCY RESPONSE ACTION PLAN PHMSA Sequence Number 2988 Owner/Operator: Phillips 66 3010 Briarpark Drive Houston, Texas 77024 24-Hour Number: (800) 231-2551 or (877) 267-2290 Page A7-1 Confidentiality Notice: This document is for the sole use of the intended recipient(s) and contains information that is considered to be proprietary to Phillips 66. Any unauthorized review, use, disclosure or distribution is strictly prohibited. Billings Area Appendix 7: Response Zone Appendix ERAP Appendix 7: ERAP Table of Contents 7.1 Area Information .......................................................................................................... 1 7.1.1 Tank Table ....................................................................................................... 2 7.2 Communication Equipment ......................................................................................... 2 7.3 Notification Sequence ................................................................................................. 2 7.4 Emergency Notification Contact List ........................................................................... 5 7.5 Emergency Response Equipment, Testing & Deployment ......................................... 9 7.6 Immediate Actions ..................................................................................................... 10 7.7 Maps and Diagrams .................................................................................................. 12 7.8 Response Forms ...................................................................................................... -

Presentation Title Slide

Investor Update Second Quarter 2015 Execution Investor Update Second Quarter 2015 NYSE: PSX www.phillips66.com Cautionary Statement This presentation contains certain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, which are intended to be covered by the safe harbors created thereby. Words and phrases such as “is anticipated,” “is estimated,” “is expected,” “is planned,” “is scheduled,” “is targeted,” “believes,” “intends,” “objectives,” “projects,” “strategies” and similar expressions are used to identify such forward-looking statements. However, the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements relating to Phillips 66’s operations (including joint venture operations) are based on management’s expectations, estimates and projections about the company, its interests and the energy industry in general on the date this presentation was prepared. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict. Therefore, actual outcomes and results may differ materially from what is expressed or forecast in such forward-looking statements. Factors that could cause actual results or events to differ materially from those described in the forward-looking statements include fluctuations in NGL, crude oil and natural gas prices, and petrochemical and refining margins; unexpected changes -

Growing Value $245 Billion of Revenues As of Dec

www.conocophillips.com ConocoPhillips is an international, integrated energy company with interests around the world. Headquartered in Houston, the company had operations in more than 35 countries, approximately 29,800 employees, $153 billion of assets and Growing Value $245 billion of revenues as of Dec. 31, 2011. 2011 SUMMARY ANNUAL REPORT 90414conD1R1.indd 1 2/28/12 11:05 PM Shareholder Information 1 Letter to Shareholders Certain disclosures in this Summary Annual Annual Meeting Information Requests Copies of Form 10-K, Proxy Statement 49 Report may be considered “forward-looking” and Summary Annual Report 5 Financial and Operating Highlights ConocoPhillips’ annual meeting of For information about dividends and statements. These are made pursuant to “safe stockholders will be held: certificates, or to request a change of Copies of the Annual Report on Form 10-K 6 Repositioning harbor” provisions of the Private Securities address form, shareholders may contact: and the Proxy Statement, as filed with the Litigation Reform Act of 1995. The “Cautionary Wednesday, May 9, 2012 U.S. Securities and Exchange Commission, Statement” in Management’s Discussion and Omni Houston Hotel Westside Computershare are available free by making a request on Our Commitments Analysis in Appendix A of ConocoPhillips’ 2012 13210 Katy Freeway, Houston, Texas P.O. Box 358015 the company’s website, calling 918-661- Proxy Statement should be read in conjunction Pittsburgh, PA 15252-8015 8 Enhancing Financial Performance Notice of the meeting and proxy materials 3700 or writing: with such statements. Toll-free number: 800-356-0066 are being sent to all shareholders. 10 Empowering Our People Outside the U.S.: 201-680-6578 ConocoPhillips – 2011 Form 10-K TDD for hearing impaired: 800-231-5469 B-41 Adams Building 12 Operating Responsibly “ConocoPhillips,” “the company,” “we,” “us” Direct Stock Purchase and Dividend and “our” are used interchangeably in this report TDD outside the U.S.: 201-680-6610 411 South Keeler Ave. -

3Qtr17 Spirit-Magazine.Pdf

CONOCOPHILLIPS Third Quarter 2017 Providing energy for the world while staying committed to our values. ConocoPhillips is proud to be an industry leader in fi nding and producing the oil and gas the world needs. At the foundation of our work is the commitment we have to our SPIRIT Values—Safety, People, Integrity, Responsibility, Innovation and Teamwork. To learn more, visit www.conocophillips.com © ConocoPhillips Company. 2017. All rights reserved. SHARING INSIGHTS From the desk of Ryan Lance Chairman & CEO AS THE HOUSTON AREA RECOVERS from the devastating aftermath of Hurricane Harvey, I continue to be impressed by the incredible compassion and resilience of our ConocoPhillips workforce. We are forging ahead on many fronts, including the completion of this special issue of spirit Magazine featuring the annual SPIRIT of Performance Awards. One of the most important responsibilities of my job is meeting with ConocoPhillips employees and listening to their ideas and concerns. During the past quarter, I visited China, Malaysia and Indonesia and saw the amazing work our people are doing on projects such as additional development phases at the Peng Lai field in Bohai Bay; production rampup and an active exploration program in Malaysia; and an initiative to sell more gas in Indonesia. During a visit to Alaska, I heard excitement around our Willow discovery in the National Petroleum Reserve and the active upcoming winter drilling campaign. In July, the company’s board of directors joined me on a visit to our Bakken operations in North Dakota, where the team patiently answered all our questions and showed why ConocoPhillips is recognized as an operator of choice in that important region. -

Phillips Petroleum Company 2001 Annual Report

Phillips Petroleum Company 2001 Annual Report NEW EXPECTATIONS PHILLIPS’ MISSION IS TO PROVIDE SUPERIOR RETURNS FOR SHAREHOLDERS THROUGH TOP PERFORMANCE IN ALL OUR BUSINESSES. PHILLIPS PETROLEUM CONTENTS COMPANY IN BRIEF 2 PHILLIPS’WORLDWIDE OPERATIONS Phillips Petroleum Company is a 4 LETTER TO SHAREHOLDERS major integrated U.S. oil and gas CEO Jim Mulva describes Phillips’ journey and explains why the company has company. It is headquartered in new expectations for increased shareholder returns. Bartlesville, Oklahoma. The company 7 THE CHAIRMAN’S PERSPECTIVE was founded in 1917. Phillips’ core Jim Mulva responds to questions about the company as it prepares to enter a new era. activities are: 9 FINANCIAL SUMMARY ■ Petroleum exploration and produc- Phillips remains financially strong despite a challenging economic climate. tion on a worldwide scale. 10 EXPLORATION AND PRODUCTION (E&P) ■ Petroleum refining, marketing and Phillips anticipates increased oil and gas output from existing projects, and is transportation, primarily in the carrying out a balanced and focused exploration program. United States. 18 REFINING, MARKETING AND TRANSPORTATION (RM&T) ■ Chemicals and plastics production Following its acquisition of Tosco, Phillips is capturing synergies and taking advantage and distribution worldwide through of its expanded capabilities as one of the largest U.S. refiners and marketers. a 50 percent interest in Chevron 24 CHEMICALS Phillips Chemical Company Chevron Phillips Chemical Company is weathering a difficult market, holding down (CPChem). costs and carrying out growth projects. ■ Natural gas gathering, processing 26 GAS GATHERING, PROCESSING AND MARKETING and marketing in North America Phillips’ midstream joint venture is making the most of its strengths while through a 30.3 percent interest in pursuing growth opportunities. -

NEWS RELEASE Phillips 66 Plans to Transform San Francisco Refinery

NEWS RELEASE Phillips 66 Plans to Transform San Francisco Refinery into World’s Largest Renewable Fuels Plant Conversion is expected to reduce the plant’s greenhouse gas emissions by 50% HOUSTON, Aug. 12, 2020 – Phillips 66 (NYSE: PSX), a diversified energy manufacturing and logistics company, announced today that it plans to reconfigure its San Francisco Refinery in Rodeo, California, to produce renewable fuels. The plant would no longer produce fuels from crude oil, but instead would make fuels from used cooking oil, fats, greases and soybean oils. The Phillips 66 Rodeo Renewed project would produce 680 million gallons annually of renewable diesel, renewable gasoline, and sustainable jet fuel. Combined with the production of renewable fuels from an existing project in development, the plant would produce greater than 800 million gallons a year of renewable fuels, making it the world’s largest facility of its kind. The project scope includes the construction of pre-treatment units and the repurposing of existing hydrocracking units to enable production of renewable fuels. The plant will utilize its flexible logistics infrastructure to bring in cooking oil, fats, greases and soybean oils from global sources and supply renewable fuels to the California market. This capital efficient investment is expected to deliver strong returns through the sale of high value products while lowering the plant’s operating costs. “Phillips 66 is taking a significant step with Rodeo Renewed to support demand for renewable fuels and help California meet its low carbon objectives,” said Greg Garland, chairman and CEO of Phillips 66. “We believe the world will require a mix of fuels to meet the growing need for affordable energy, and the renewable fuels from Rodeo Renewed will be an important part of that mix. -

Table 3. Capacity of Operable Petroleum Refineries by State As of January 1, 2021 (Barrels Per Stream Day, Except Where Noted)

Table 3. Capacity of Operable Petroleum Refineries by State as of January 1, 2021 (Barrels per Stream Day, Except Where Noted) Atmospheric Crude Oil Distillation Capacity Downstream Charge Capacity Barrels per Barrels per Thermal Cracking Calendar Day Stream Day Vacuum Delayed Other/Gas State/Refiner/Location Operating Idle Operating Idle Distillation Coking Fluid Coking Visbreaking Oil Alabama......................................................... 139,600 0 145,600 0 54,000 34,000 0 0 0 Goodway Refining LLC ....................................................................................................................................................................................................Atmore 4,100 0 5,000 0 0 0 0 0 0 Hunt Refining Co ....................................................................................................................................................................................................Tuscaloosa 48,000 0 50,000 0 25,000 34,000 0 0 0 Shell Chemical LP ....................................................................................................................................................................................................Saraland 87,500 0 90,600 0 29,000 0 0 0 0 Alaska......................................................... 164,200 0 178,500 0 26,000 0 0 0 0 ConocoPhillips Alaska Inc ....................................................................................................................................................................................................Prudhoe -

Phillips 66 (Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 SCHEDULE 14A Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934 (Amendment No. ) Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐ Check the appropriate box: ☐ Preliminary Proxy Statement ☐ Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) ☒ Definitive Proxy Statement ☐ Definitive Additional Materials ☐ Soliciting Material under §240.14a-12 Phillips 66 (Name of Registrant as Specified in its Charter) (Name of Person(s) Filing Proxy Statement, if other than the Registrant) Payment of Filing Fee (Check the appropriate box): ☒ No fee required. ☐ Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. (1) Title of each class of securities to which transaction applies: (2) Aggregate number of securities to which transaction applies: (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): (4) Proposed maximum aggregate value of transaction: (5) Total fee paid: ☐ Fee paid previously with preliminary materials. Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid ☐ previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. (1) Amount Previously Paid: (2) Form, Schedule or Registration Statement No.: (3) Filing Party: (4) Date Filed: From Our Chairman of the Board Dear Fellow Shareholders, Over the past year, we were faced with a number of unprecedented challenges.