Investor Update February 2018

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2019 Annual Report Are Commission-Free

Table of Contents 1 Letter to Our Shareholders 4 Financial Highlights 6 Our Businesses Midstream Chemicals Refining Marketing and Specialties 7 Our Value Chain 8 Our Strategy Operating Excellence Growth Returns Distributions High-Performing Organization 28 Board of Directors 30 Executive Leadership Team 31 Non-GAAP Reconciliations 32 Form 10-K | ON THE COVER AND TABLE OF CONTENTS Lake Charles Refinery WESTLAKE, LA In 2019, Lake Charles Manufacturing Complex achieved a sustained safety record of more than 55 months, equivalent to 7.5 million safe work hours. 2019 PHILLIPS 66 ANNUAL REPORT 1 To Our Shareholders We have the right strategy in place to create shareholder value, and our employees are executing it well. Phillips 66 achieved 34% total shareholder return during 2019, which exceeded our peer group average and the S&P 100. In 2019, we delivered earnings of $3.1 billion and earnings per share of $6.77. Adjusted earnings were $3.7 billion or $8.05 per share. During the year, we generated $4.8 billion of operating cash flow. We reinvested $3.9 billionback into the business and returned $3.2 billion of capital to shareholders through dividends and share repurchases. We increased our quarterly dividend 12.5% and announced a $3 billion increase to our share repurchase program. Since our formation, we have returned $26 billion to shareholders through dividends, share repurchases and exchanges, reducing our initial shares outstanding by 33%. Operating excellence is our No. 1 priority and core to everything we do. Our goal is zero incidents, zero accidents and zero injuries. We believe this is attainable, and we strive for it daily. -

Report Document

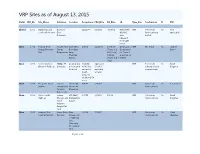

VRP Sites as of August 13, 2015 Status VRP_No. Site_Name Volunteer Location Acceptance DatePRA_Date RA_Date LA Type_Site Contaminant IC PM Closed 1001 Rail siding and Big Horn 12/11/00 3/26/02 3/26/02 NFA Letter VRP Petroleum No Not coal load out area Coal 4/26/02; hydrocarbons, applicable Company area metals released from LQD bond Open 1002 Powder River Powder River 1095 West 1/8/01 10/17/01 10/01/07 Certificate of VRP Oil, diesel No Jaymee Energy Sheridan Energy Brundage (Tracts 8, 9, Completion Binion Site Corporation Lane, & 10 only), for Tracts 8, Sheridan, 5/18/09 9, and 10 on 82801 (Tracts 6 & 7 5/8/09 only) Open 1003 Former Conoco Phillips 66 Located 1/2 3/19/01; Approved VRP Petroleum No Sarah Glenrock Refinery Company mile west of 6/28/2011 5/13/02; refinery related Bargsten Glenrock amended amended contaminants South 9/19/02 property additional 54 acres Open 1004 Cheyenne Crude Suncor 199 South 4/4/01 5/30/06 VRP Petroleum No Ben Luckey Station Energy USA, Morrie Av, hydrocarbons formerly Cheyenne Conoco Inc. Open 1005 Union Pacific Former 543 West 4/4/01 7/31/03 1/3/05 VRP Petroleum No Sarah Railroad Chicago and Midwest Av, Hydrocarbons Bargsten North Casper Western Casper Rail Yard Open 1006 Laramie Yard Union Pacific Near 4/4/01 7/09/04 VRP Petroleum No Cindi Fueling Platform Railroad intersection Hydrocarbons Martinez of Railroad and University St., Laramie Yard Page 1 of 29 Status VRP_No. Site_Name Volunteer Location Acceptance DatePRA_Date RA_Date LA Type_Site Contaminant IC PM Closed 1007 Gulley Enterprises Cheyenne 411 E. -

Sustainable Jet Fuel for Aviation

Sustainable jet fuel for aviation Nordic perpectives on the use of advanced sustainable jet fuel for aviation Sustainable jet fuel for aviation Nordic perpectives on the use of advanced sustainable jet fuel for aviation Erik C. Wormslev, Jakob Louis Pedersen, Christian Eriksen, Rasmus Bugge, Nicolaj Skou, Camilla Tang, Toke Liengaard, Ras- mus Schnoor Hansen, Johannes Momme Eberhardt, Marie Katrine Rasch, Jonas Höglund, Ronja Beijer Englund, Judit Sandquist, Berta Matas Güell, Jens Jacob Kielland Haug, Päivi Luoma, Tiina Pursula and Marika Bröckl TemaNord 2016:538 Sustainable jet fuel for aviation Nordic perpectives on the use of advanced sustainable jet fuel for aviation Erik C. Wormslev, Jakob Louis Pedersen, Christian Eriksen, Rasmus Bugge, Nicolaj Skou, Camilla Tang, Toke Liengaard, Rasmus Schnoor Hansen, Johannes Momme Eberhardt, Marie Katrine Rasch, Jonas Höglund, Ronja Beijer Englund, Judit Sandquist, Berta Matas Güell, Jens Jacob Kielland Haug, Päivi Luoma, Tiina Pursula and Marika Bröckl ISBN 978-92-893-4661-0 (PRINT) ISBN 978-92-893-4662-7 (PDF) ISBN 978-92-893-4663-4 (EPUB) http://dx.doi.org/10.6027/TN2016-538 TemaNord 2016:538 ISSN 0908-6692 © Nordic Council of Ministers 2016 Layout: Hanne Lebech Cover photo: Scanpix Print: Rosendahls-Schultz Grafisk Copies: 100 Printed in Denmark This publication has been published with financial support by the Nordic Council of Ministers. However, the contents of this publication do not necessarily reflect the views, policies or recom- mendations of the Nordic Council of Ministers. www.norden.org/nordpub Nordic co-operation Nordic co-operation is one of the world’s most extensive forms of regional collaboration, involv- ing Denmark, Finland, Iceland, Norway, Sweden, and the Faroe Islands, Greenland, and Åland. -

2020 Fact Book 2 Our Businesses Our Strategy Midstream Chemicals Refining Marketing and Specialties Energy Research & Innovation Global Asset Map General Information

Cover Photo: Taft Storage Facility at Gray Oak Pipeline TAFT, TX Contents 3 4 5 OUR BUSINESSES OUR STRATEGY MIDSTREAM Ferndale Ferndale Rail Terminal* Renton North Spokane Tacoma (MT) Yellowstone Cut Bank Moses Lake Thompson 17Falls Rail 24 14 Spokane Terminal Palermo* UROPE DLE EA Portland D Great Falls E I ST Portland (MT) Missoula Rail Terminal M Yello Glacier Sacagawea* Missoula wsto Helena Roundup Keene CDP* ne Billings Crude* Bozeman Billings Billings Humber SPCo & S-Chem ooth Sheridan* Semino Bakk Beart en Bayway MiRO CHEMICALS REFINING * MARKETING AND SPECIALTIES Bighorn e* Linden* Q-Chem I & II Casper* Tremley Pt. (MT)* * Po Rock Springs wd Bayway Rail eminoe er Ri Terminal* S Harbor Red Line Oil North Salt Lake Pioneer ve Des Moines s r Sacramento Rockies Expr Hartford Lincoln ess Line 20 ess Richmond (MT) Rockies Expr San Francisco Denver Borg Conway Kansas City* Po 0 Rockies Expres to Wichita wd Paola er-Den Gold Line* Wood River er Riv Wichita N.* Products* HeartlandPaola* Blue Line 0 Wichita S.* E. St. ver Jeerson City* Junction er Louis* Southern Hills* m Cherokee North* r*Hartford* Line 30 re Line 40 ol Standish* La Junta * h Ponca City* Explo his Ponca City ld Line C Crude* Go 0 Los Angeles Medford* eeMount Vernon* ok t Los Angeles Borger CherEas Torrance Cherokee Colton Borger to Amarillo* Blue LineSouth* Glenpool* Ponca Selmer Line O* * CushPo* Albuquerque* K PL Sk AC ATA Line* elly ST Cushing City SA Oklahoma City* Amarillo* -Belvieu Los Angeles AL Borger Oklahoma Crude* * Explor Wichita Falls* Lubbock* Savannah North -

Billings Area Emergency Response Action Plan

BILLINGS AREA EMERGENCY RESPONSE ACTION PLAN PHMSA Sequence Number 2988 Owner/Operator: Phillips 66 3010 Briarpark Drive Houston, Texas 77024 24-Hour Number: (800) 231-2551 or (877) 267-2290 Page A7-1 Confidentiality Notice: This document is for the sole use of the intended recipient(s) and contains information that is considered to be proprietary to Phillips 66. Any unauthorized review, use, disclosure or distribution is strictly prohibited. Billings Area Appendix 7: Response Zone Appendix ERAP Appendix 7: ERAP Table of Contents 7.1 Area Information .......................................................................................................... 1 7.1.1 Tank Table ....................................................................................................... 2 7.2 Communication Equipment ......................................................................................... 2 7.3 Notification Sequence ................................................................................................. 2 7.4 Emergency Notification Contact List ........................................................................... 5 7.5 Emergency Response Equipment, Testing & Deployment ......................................... 9 7.6 Immediate Actions ..................................................................................................... 10 7.7 Maps and Diagrams .................................................................................................. 12 7.8 Response Forms ...................................................................................................... -

Toxicological Profile for Jp-5, Jp-8, and Jet a Fuels

TOXICOLOGICAL PROFILE FOR JP-5, JP-8, AND JET A FUELS U.S. DEPARTMENT OF HEALTH AND HUMAN SERVICES Public Health Service Agency for Toxic Substances and Disease Registry March 2017 JP-5, JP-8, AND JET A FUELS ii DISCLAIMER Use of trade names is for identification only and does not imply endorsement by the Agency for Toxic Substances and Disease Registry, the Public Health Service, or the U.S. Department of Health and Human Services. JP-5, JP-8, AND JET A FUELS iii UPDATE STATEMENT A Toxicological Profile for JP-5, JP-8, and Jet A Fuels, Draft for Public Comment was released in February 2016. This edition supersedes any previously released draft or final profile. Toxicological profiles are revised and republished as necessary. For information regarding the update status of previously released profiles, contact ATSDR at: Agency for Toxic Substances and Disease Registry Division of Toxicology and Human Health Sciences Environmental Toxicology Branch 1600 Clifton Road NE Mailstop F-57 Atlanta, Georgia 30329-4027 JP-5, JP-8, AND JET A FUELS iv This page is intentionally blank. JP-5, JP-8, AND JET A FUELS v FOREWORD This toxicological profile is prepared in accordance with guidelines* developed by the Agency for Toxic Substances and Disease Registry (ATSDR) and the Environmental Protection Agency (EPA). The original guidelines were published in the Federal Register on April 17, 1987. Each profile will be revised and republished as necessary. The ATSDR toxicological profile succinctly characterizes the toxicologic and adverse health effects information for these toxic substances described therein. Each peer-reviewed profile identifies and reviews the key literature that describes a substance's toxicologic properties. -

Sustainable Aviation Fuels Road-Map

SUSTAINABLE AVIATION FUELS ROAD-MAP Fueling the future of UK aviation sustainableaviation.co.uk Sustainable Aviation wishes to thank the following organisations for leading the work in producing this Road-Map: Sustainable Aviation (SA) believes the data forecasts and analysis of this report to be correct as at the date of publication. The opinions contained in this report, except where specifically attributed to, are those of SA, and based upon the information that was available to us at the time of publication. We are always pleased to receive updated information and opinions about any of the contents. All statements in this report (other than statements of historical facts) that address future market developments, government actions and events, may be deemed ‘forward-looking statements’. Although SA believes that the outcomes expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance: actual results or developments may differ materially, e.g. due to the emergence of new technologies and applications, changes to regulations, and unforeseen general economic, market or business conditions. CONTENTS EXECUTIVE SUMMARY INTRODUCTION 1.1 Addressing the sustainability challenge in aviation 1.2 The role of sustainable aviation fuels 1.3 The Sustainable Aviation Fuels Road-Map SUSTAINABLE AVIATION FUELS 2.1 Sustainability of sustainable aviation fuels 2.2 Sustainable aviation fuels types 2.3 Production and usage of sustainable aviation fuels to date THE FUTURE FOR SUSTAINABLE -

Presentation Title Slide

Investor Update Second Quarter 2015 Execution Investor Update Second Quarter 2015 NYSE: PSX www.phillips66.com Cautionary Statement This presentation contains certain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, which are intended to be covered by the safe harbors created thereby. Words and phrases such as “is anticipated,” “is estimated,” “is expected,” “is planned,” “is scheduled,” “is targeted,” “believes,” “intends,” “objectives,” “projects,” “strategies” and similar expressions are used to identify such forward-looking statements. However, the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements relating to Phillips 66’s operations (including joint venture operations) are based on management’s expectations, estimates and projections about the company, its interests and the energy industry in general on the date this presentation was prepared. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict. Therefore, actual outcomes and results may differ materially from what is expressed or forecast in such forward-looking statements. Factors that could cause actual results or events to differ materially from those described in the forward-looking statements include fluctuations in NGL, crude oil and natural gas prices, and petrochemical and refining margins; unexpected changes -

Foreign ICAO 3LD Additions, Deletions, and Modifications (Excluding U.S.)

U.S. DEPARTMENT OF TRANSPORTATION N JO 7340.589 NOTICE FEDERAL AVIATION ADMINISTRATION Air Traffic Organization Policy Effective Date: July 14, 2020 Cancellation Date: July 14, 2021 SUBJ: Foreign ICAO 3LD Additions, Deletions, and Modifications (excluding U.S.) 1. Purpose of This Notice. This notice modifies FAA Order J 7340.2, Contractions, Chapter 3, Sections 1, 2, and 3, ICAO Aircraft Company Three-Letter Identifier and/or Telephony Designator. This notice reflects recent changes initiated by countries other than the United States (U.S.) including new ICAO three letter designators (3LDs), deletions of defunct ICAO 3LDs, and modifications to ICAO 3LDs, associated telephonies, and companies/agencies. This Notice supplements FAA Order JO 7340.2 until the additions and modifications are incorporated into the Order. This Notice does not replace or substitute for GENOTs issued by the Federal Aviation Administration (FAA) Air Traffic Organization (ATO) for ICAO 3LDs assigned and authorized for U.S. aircraft operators. 2. Audience. This notice applies to the following Air Traffic Organization (ATO) service units: Air Traffic Services, and System Operations Services; ATO Safety and Technical Training; and all associated air traffic control facilities. This notice is informational in nature and does not require documentation as supplemental training in FAA Form 3120-1, Training and Proficiency Record. 3. Where Can I Find This Notice? This notice is available on the MyFAA employee website at https://employees.faa.gov/tools_resources/orders_notices/ and on the air traffic publications website at http://www.faa.gov/air_traffic/publications/. 4. Source Document. The source document for the ICAO 3LD additions and modifications contained in this notice is ICAO Document 8585, Designators for Aircraft Operating Agencies, Aeronautical Authorities, and Services. -

Growing Value $245 Billion of Revenues As of Dec

www.conocophillips.com ConocoPhillips is an international, integrated energy company with interests around the world. Headquartered in Houston, the company had operations in more than 35 countries, approximately 29,800 employees, $153 billion of assets and Growing Value $245 billion of revenues as of Dec. 31, 2011. 2011 SUMMARY ANNUAL REPORT 90414conD1R1.indd 1 2/28/12 11:05 PM Shareholder Information 1 Letter to Shareholders Certain disclosures in this Summary Annual Annual Meeting Information Requests Copies of Form 10-K, Proxy Statement 49 Report may be considered “forward-looking” and Summary Annual Report 5 Financial and Operating Highlights ConocoPhillips’ annual meeting of For information about dividends and statements. These are made pursuant to “safe stockholders will be held: certificates, or to request a change of Copies of the Annual Report on Form 10-K 6 Repositioning harbor” provisions of the Private Securities address form, shareholders may contact: and the Proxy Statement, as filed with the Litigation Reform Act of 1995. The “Cautionary Wednesday, May 9, 2012 U.S. Securities and Exchange Commission, Statement” in Management’s Discussion and Omni Houston Hotel Westside Computershare are available free by making a request on Our Commitments Analysis in Appendix A of ConocoPhillips’ 2012 13210 Katy Freeway, Houston, Texas P.O. Box 358015 the company’s website, calling 918-661- Proxy Statement should be read in conjunction Pittsburgh, PA 15252-8015 8 Enhancing Financial Performance Notice of the meeting and proxy materials 3700 or writing: with such statements. Toll-free number: 800-356-0066 are being sent to all shareholders. 10 Empowering Our People Outside the U.S.: 201-680-6578 ConocoPhillips – 2011 Form 10-K TDD for hearing impaired: 800-231-5469 B-41 Adams Building 12 Operating Responsibly “ConocoPhillips,” “the company,” “we,” “us” Direct Stock Purchase and Dividend and “our” are used interchangeably in this report TDD outside the U.S.: 201-680-6610 411 South Keeler Ave. -

Explosion at the Conoco Humber Refinery – 16Th April 2001

SYMPOSIUM SERIES NO. 151 # 2006 Crown Copyright EXPLOSION AT THE CONOCO HUMBER REFINERY – 16TH APRIL 2001 Jonathan Carter, Peter Dawson and Robert Nixon Health and Safety Executive, Hazardous Installations Directorate # Crown Copyright 2006. This article is published with the permission of the Controller of HMSO and the Queen’s Printer for Scotland An explosion and fire occurred at the Conoco Humber Refinery on 16th April 2001, following the catastrophic failure of a 600 overhead pipe from a de-ethaniser column on the Saturate Gas Plant. Investigation revealed that the failure of the pipe was due to internal corrosion that had not been identified by the refinery pipework inspection regime. The paper describes the event and the emergency response. It also examines the immediate cause of the event, and how failures of the management of pipework inspection and management of change failed to prevent the accident occurring. The paper concludes with the lessons that can be learned from this event. THE REFINERY The Humber Refinery is located on the south bank of the estuary of the River Humber on the east coast of England, approximately 1.5 km north-west of the town of Immingham and 0.5 km east of the village of Killingholme. In 2001 Conoco Ltd owned the refinery. In August 2002 Conoco merged to form ConocoPhillips Ltd., the current owners of the refinery. The refinery was constructed between 1966 and 1969 and commissioned in 1970. The current capacity of the refinery is about 225,00 US barrels per day of crude oil, or about 11.4 million tonne per year. -

3Qtr17 Spirit-Magazine.Pdf

CONOCOPHILLIPS Third Quarter 2017 Providing energy for the world while staying committed to our values. ConocoPhillips is proud to be an industry leader in fi nding and producing the oil and gas the world needs. At the foundation of our work is the commitment we have to our SPIRIT Values—Safety, People, Integrity, Responsibility, Innovation and Teamwork. To learn more, visit www.conocophillips.com © ConocoPhillips Company. 2017. All rights reserved. SHARING INSIGHTS From the desk of Ryan Lance Chairman & CEO AS THE HOUSTON AREA RECOVERS from the devastating aftermath of Hurricane Harvey, I continue to be impressed by the incredible compassion and resilience of our ConocoPhillips workforce. We are forging ahead on many fronts, including the completion of this special issue of spirit Magazine featuring the annual SPIRIT of Performance Awards. One of the most important responsibilities of my job is meeting with ConocoPhillips employees and listening to their ideas and concerns. During the past quarter, I visited China, Malaysia and Indonesia and saw the amazing work our people are doing on projects such as additional development phases at the Peng Lai field in Bohai Bay; production rampup and an active exploration program in Malaysia; and an initiative to sell more gas in Indonesia. During a visit to Alaska, I heard excitement around our Willow discovery in the National Petroleum Reserve and the active upcoming winter drilling campaign. In July, the company’s board of directors joined me on a visit to our Bakken operations in North Dakota, where the team patiently answered all our questions and showed why ConocoPhillips is recognized as an operator of choice in that important region.