Taiwan: Policy Drive for Innovation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

AU OPTRONICS CORP Form SD Filed 2018-05-31

SECURITIES AND EXCHANGE COMMISSION FORM SD Specialized Disclosure Report Filing Date: 2018-05-31 SEC Accession No. 0000950103-18-006801 (HTML Version on secdatabase.com) FILER AU OPTRONICS CORP Business Address 1 LI HSIN RD 2 CIK:1172494| IRS No.: 000000000 SCIENC BASED INUSTRIAL Type: SD | Act: 34 | File No.: 001-31335 | Film No.: 18869971 PARK SIC: 3674 Semiconductors & related devices HSIN CHU 300 TAIWAN F5 00000 852-2514-7600 Copyright © 2018 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM SD Specialized Disclosure Report (Exact Name of Registrant as Specified in Its Charter) TAIWAN, REPUBLIC OF CHINA 001-31335 Not Applicable (State or other jurisdiction of incorporation or organization) (Commission File Number) (IRS Employer Identification No.) 1 LI-HSIN ROAD 2 HSINCHU SCIENCE PARK HSINCHU, TAIWAN REPUBLIC OF CHINA (Address of principal executive offices) Benjamin Tseng Chief Financial Officer 1 Li-Hsin Road 2 Hsinchu Science Park Hsinchu, Taiwan Republic of China Telephone No.: +886-3-500-8800 Facsimile No.: +886-3-564-3370 Email: [email protected] (Name and telephone, including area code, of the person to contact in connection with this report) Check the appropriate box to indicate the rule pursuant to which this form is being filed, and provide the period to which the information in this form applies: Rule 13p-1 under the Securities Exchange Act (17 CFR 240.13p-1) under the Exchange Act for the reporting period from ☒ January 1 to December 31, 2017. Copyright © 2018 www.secdatabase.com. -

The Mineral Industry of Taiwan in 2004

THE MINERAL INDUSTRY OF TAIWAN By Pui-Kwan Tse Taiwan is an island that is located south of Japan and east encourage Taiwanese businesses to stay in Taiwan and would of mainland China in the Pacific Ocean. In 2004, Taiwan’s attract foreign businesses to set up global logistics centers in economy grew by 5.7%, which was the largest increase since Taiwan. Developing service industries such as entertainment, 2000. After reaching a peak of 7.9% in the second quarter, environmental protection, medicine and healthcare, and tourism the economy slowed to 3.3% in the fourth quarter because of and sports recreation would enhance the quality of life in higher global oil prices and the deceleration of export growth Taiwan. The CEPD projected that the service sector would during the second half of the year. The economic growth was grow 6.1% per year through 2008 and that the percentage of the generated by private consumption and investment. Private GDP generated by the service sector would increase to 67% in consumption increased by 3.1% and private investment rose by 2008 from 63.5% in 2003 (Taiwan Headlines, 2004b§; 2005d§). 28.2% compared with that of the previous year. The recovery The Taiwan authorities carried out the second phase of of the information and communication technologies industry Taiwan’s financial reform program in 2004. The number of was the main reason for the increased business investment. In state-owned banks (banks in which the government held 30% 2004, Government fixed investment decreased by 4.2% because or more interest) would be reduced to 6 from 12 at yearend of higher prices on construction materials and because some 2005. -

Taiwan Semiconductor Manufacturing Company Limited and Subsidiaries

Taiwan Semiconductor Manufacturing Company Limited and Subsidiaries Consolidated Financial Statements for the Nine Months Ended September 30, 2020 and 2019 and Independent Auditors’ Review Report Taiwan Semiconductor Manufacturing Company Limited and Subsidiaries NOTES TO CONSOLIDATED FINANCIAL STATEMENTS FOR THE NINE MONTHS ENDED SEPTEMBER 30, 2020 AND 2019 (Amounts in Thousands of New Taiwan Dollars, Unless Specified Otherwise) (Reviewed, Not Audited) 1. GENERAL Taiwan Semiconductor Manufacturing Company Limited (TSMC), a Republic of China (R.O.C.) corporation, was incorporated on February 21, 1987. TSMC is a dedicated foundry in the semiconductor industry which engages mainly in the manufacturing, selling, packaging, testing and computer-aided design of integrated circuits and other semiconductor devices and the manufacturing of masks. On September 5, 1994, TSMC’s shares were listed on the Taiwan Stock Exchange (TWSE). On October 8, 1997, TSMC listed some of its shares of stock on the New York Stock Exchange (NYSE) in the form of American Depositary Shares (ADSs). The address of its registered office and principal place of business is No. 8, Li-Hsin Rd. 6, Hsinchu Science Park, Taiwan. The principal operating activities of TSMC’s subsidiaries are described in Note 4. 2. THE AUTHORIZATION OF FINANCIAL STATEMENTS The accompanying consolidated financial statements were reported to the Board of Directors and issued on November 10, 2020. 3. APPLICATION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS a. Initial application of the amendments to the International Financial Reporting Standards (IFRS), International Accounting Standards (IAS), IFRIC Interpretations (IFRIC), and SIC Interpretations (SIC) (collectively, “IFRSs”) endorsed and issued into effect by the Financial Supervisory Commission (FSC) The initial application of the amendments to the IFRSs endorsed and issued into effect by the FSC did not have a significant effect on TSMC and its subsidiaries’ (collectively as the “Company”) accounting policies. -

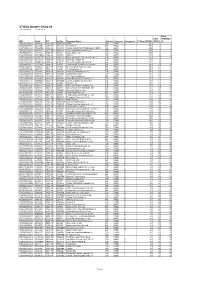

STOXX Greater China 80 Last Updated: 01.08.2017

STOXX Greater China 80 Last Updated: 01.08.2017 Rank Rank (PREVIOU ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) S) TW0002330008 6889106 2330.TW TW001Q TSMC TW TWD Y 113.9 1 1 HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 80.6 2 2 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 60.5 3 3 TW0002317005 6438564 2317.TW TW002R Hon Hai Precision Industry Co TW TWD Y 51.5 4 4 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 50.8 5 5 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 41.3 6 6 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 32.0 7 9 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 31.8 8 7 KYG217651051 BW9P816 0001.HK 619027 CK HUTCHISON HOLDINGS HK HKD Y 31.1 9 8 HK0388045442 6267359 0388.HK 626735 Hong Kong Exchanges & Clearing HK HKD Y 28.0 10 10 HK0016000132 6859927 0016.HK 685992 Sun Hung Kai Properties Ltd. HK HKD Y 20.6 11 12 HK0002007356 6097017 0002.HK 619091 CLP Holdings Ltd. HK HKD Y 20.0 12 11 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 20.0 13 13 TW0003008009 6451668 3008.TW TW05PJ LARGAN Precision TW TWD Y 19.7 14 15 KYG2103F1019 BWX52N2 1113.HK HK50CI CK Property Holdings HK HKD Y 18.3 15 14 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 16.4 16 16 HK0823032773 B0PB4M7 0823.HK B0PB4M Link Real Estate Investment Tr HK HKD Y 15.4 17 19 HK0883013259 B00G0S5 0883.HK 617994 CNOOC Ltd. -

Inventec Corporation

(English Translation of Pro Forma Financial Report Originally Issued in Chinese) PEGATRON CORPORATION AND ITS SUBSIDIARIES PRO FORMA CONSOLIDATED FINANCIAL STATEMENTS DECEMBER 31, 2008 AND 2007 (With Independent Auditors’ Report Thereon) Address: 5F., No.76, Ligong St., Beitou District, Taipei City 112, Taiwan Telephone: 886-2-8143-9001 - 1 - TABLE OF CONTENTS Contents Page Cover Page 1 Table of Contents 2 Independent Auditors’ Report 3 Pro Forma Consolidated Balance Sheets 4 Pro Forma Consolidated Statements of Income 5 Pro Forma Consolidated Statements of Changes in Stockholders’ Equity 6 Pro Forma Consolidated Statements of Cash Flows 7 Notes to Pro Forma Consolidated Financial Statements (1) Organization and Business 8 (2) Summary of Significant Accounting Policies 8-28 (3) Reasons for and Effects of Accounting Changes 28 (4) Summary of Major Accounts 28-49 (5) Related-Party Transactions 50-56 (6) Pledged Assets 56 (7) Significant Commitments and Contingencies 57-58 (8) Significant Catastrophic Losses 59 (9) Significant Subsequent Events 59 (10) Others 59 (11)Additional Disclosures 60-61 (12)Segment Information 61-62 - 2 - (English Translation of Financial Report Originally Issued in Chinese) PEGATRON CORPORATION AND ITS SUBSIDIARIES PRO FORMA CONSOLIDATED BALANCE SHEETS DECEMBER 31, 2008 AND 2007 (All Amounts Expressed in Thousands of New Taiwan Dollars, Except for Share Data) December 31, 2008 December 31, 2007 Amount % Amount % ASSETS Current Asset: Cash (Notes 2 and 4(1)) $ 27,065,987 12 26,294,882 9 Financial assets reported -

Taiwan's Top 50 Corporates

Title Page 1 TAIWAN RATINGS CORP. | TAIWAN'S TOP 50 CORPORATES We provide: A variety of Chinese and English rating credit Our address: https://rrs.taiwanratings.com.tw rating information. Real-time credit rating news. Credit rating results and credit reports on rated corporations and financial institutions. Commentaries and house views on various industrial sectors. Rating definitions and criteria. Rating performance and default information. S&P commentaries on the Greater China region. Multi-media broadcast services. Topics and content from Investor outreach meetings. RRS contains comprehensive research and analysis on both local and international corporations as well as the markets in which they operate. The site has significant reference value for market practitioners and academic institutions who wish to have an insight on the default probability of Taiwanese corporations. (as of June 30, 2015) Chinese English Rating News 3,440 3,406 Rating Reports 2,006 2,145 TRC Local Analysis 462 458 S&P Greater China Region Analysis 76 77 Contact Us Iris Chu; (886) 2 8722-5870; [email protected] TAIWAN RATINGS CORP. | TAIWAN'S TOP 50 CORPORATESJenny Wu (886) 2 872-5873; [email protected] We warmly welcome you to our latest study of Taiwan's top 50 corporates, covering the island's largest corporations by revenue in 2014. Our survey of Taiwan's top corporates includes an assessment of the 14 industry sectors in which these companies operate, to inform our views on which sectors are most vulnerable to the current global (especially for China) economic environment, as well as the rising strength of China's domestic supply chain. -

Taiwan: Semiconductor Cluster

Taiwan: Semiconductor Cluster Yao Chew Ruijian Li Eric Otoo David Tiomkin Tina Tran Harvard Business School Microeconomics of Competitiveness Course Paper May 2, 2007 Table of Contents 1. Introduction............................................................................................................................. 2 2. Country Analysis ..................................................................................................................... 2 2.1. Position, Brief History and Political Tension with Mainland China..................................... 2 2.2. Taiwan’s Country Balance Sheet in 1950............................................................................ 3 2.3. Economy from 1950 to present ........................................................................................... 4 2.4. Current Economic Position ................................................................................................. 5 2.5. Productivity and Competitiveness ....................................................................................... 7 2.6. Business and Political Environment .................................................................................... 8 2.7. National Diamond............................................................................................................. 10 3. Cluster Analysis..................................................................................................................... 12 3.1 The ITRI and Institutes for Collaboration (IFCs) .............................................................. -

Abstract: the Preparatory Briefing on Taiwan Is the Result of the Collection of Relevant Cluster Information in the Country

Project name Supporting international cluster and business network cooperation through the further development of the European Cluster Collaboration Platform Project acronym ECCP Deliverable title and number D 3.2. – Preparatory Briefing on Taiwan Related work package WP3 Deliverable lead, and partners SPI involved Reviewed by Inno, Commission Contractual delivery date M12 Actual delivery date M15 Start date of project September, 23rd 2015 Duration 4 years Document version V2 Abstract: The preparatory briefing on Taiwan is the result of the collection of relevant cluster information in the country, including business and sector trends, cluster policies and programmes, as well as a cluster mapping. This document is intended to provide an overview of the country’s opportunities for European cluster organisations and SMEs © — 2018 – European Union. All rights reserved The information and views set out in this report are those of the author(s) and do not necessarily reflect the official opinion of the Executive Agency for Small and Medium-sized Enterprises (EASME) or of the Commission. Neither EASME, nor the Commission can guarantee the accuracy of the data included in this study. Neither EASME, nor the Commission or any person acting on their behalf may be held responsible for the use which may be made of the information contained therein. D.3.2 - Preparatory Briefing on Taiwan Content 1 Objective of the report .................................................................................................................... 3 2 Taiwan -

Hsinchu Science Park 2006 04 May Hsia

The Development and Outlook of Taiwan’s Science Parks October 2, 2006 Definition of “Science Park” .Near Universities and research centers .Encouraging knowledge-based industries .Helping start-ups 1 Linear Model of Innovation 1. Basic Science Universities 2. Applied Science Research Institutes 3. Technological Development Companies 4. Product Markets Development of Science Parks .1950: Stanford University Science Park .1959: Research Triangle Science Park .1965: Herriot-Watt Univ. Science Park .1970: 22 Science Parks .1970-1980: 39-> Hsinchu Science Park .1980-1990: 270 .1990-2000: 473 2 Taiwan’s Economic Development .1950s –Consumer Goods Industry (Export Zones) .1960s - Rapid Growth of Light Industry (Industrial Parks) .1970s - Capital & Technology Intensive Industries (Research Institutes) .1980s - High-Tech Industries (Sciences Parks) Hsinchu Science Park TaipeiTaipei CKSCKS Internation1 Internation1 Airport Airport HSINCHU SCIENCE PARK TaichungTaichung KaoshiungKaoshiung 3 Hsinchu Science Park HISTORY: Started in 1980 OPERATION: Managed by Park Administration, National Science Council Objectives .Attract Domestic and International High-tech Investors .Facilitate High-tech Development .Recruit High-tech Talents To Enhance HSP Economic Development STSP CTSP 4 Development Model of Hsinchu Science Park 1. Basic Science Universities 2. Applied Science Research Institutes 3. Technological Development Companies 4. Product Markets Incentives and Supports 5 What Science Parks Offer .Easy Access .Academic Environment .Sound Infrastructure -

Chipmos to Present at Investor Conference Hosted by the Taipei Exchange and ICA

Contacts: In Taiwan In the U.S. Jesse Huang David Pasquale ChipMOS TECHNOLOGIES INC. Global IR Partners +886-6-5052388 ext. 7715 +1-914-337-8801 [email protected] [email protected] ChipMOS to Present at Investor Conference Hosted by the Taipei Exchange and ICA Hsinchu, Taiwan - March 31, 2021 - ChipMOS TECHNOLOGIES INC. (“ChipMOS” or the “Company”) (Taiwan Stock Exchange: 8150 and NASDAQ: IMOS), an industry leading provider of outsourced semiconductor assembly and test services (“OSAT”), today announced that it will present virtually at the Taiwan Stock Market Discovery Forum 2021, an investor conference hosted by the Taipei Exchange and ICA on April 8, 2021. Management from the Company, including Jesse Huang, Senior Vice President of Strategy and Investor Relations, will discuss the Company’s recent financial results, business trends and growth opportunities. The Company’s latest investor update is available on the investor relations’ section of its website at www.chipmos.com. About ChipMOS TECHNOLOGIES INC.: ChipMOS TECHNOLOGIES INC. (“ChipMOS” or the “Company”) (Taiwan Stock Exchange: 8150 and NASDAQ: IMOS) (https://www.chipmos.com) is an industry leading provider of outsourced semiconductor assembly and test services. With advanced facilities in Hsinchu Science Park, Hsinchu Industrial Park and Southern Taiwan Science Park in Taiwan, ChipMOS provide assembly and test services to a broad range of customers, including leading fabless semiconductor companies, integrated device manufacturers and independent semiconductor foundries. Forward-Looking Statements This press release may contain certain forward-looking statements. These forward-looking statements may be identified by words such as ‘believes,’ ‘expects,’ ‘anticipates,’ ‘projects,’ ‘intends,’ ‘should,’ ‘seeks,’ ‘estimates,’ ‘future’ or similar expressions or by discussion of, among other things, strategy, goals, plans or intentions. -

Certificate of Approval

Certificate of Approval This is to certify that the Management System of: Powerchip Semiconductor Manufacturing Corp. No.18 Li-Hsin 1st Rd., Hsinchu Science Park, Hsinchu City 30078, Taiwan has been approved by LRQA to the following standards: ISO 14001:2015 Rhett Wang - Area Operations Manager, Greater China Issued by: Lloyd's Register Inspection Limited Taiwan Branch for and on behalf of: Lloyd's Register Quality Assurance Limited This certificate is valid only in association with the certificate schedule bearing the same number on which the locations applicable to this approval are listed. Current issue date: 29 April 2019 Original approval(s): Expiry date: 13 November 2020 ISO 14001 – 22 October 1998 Certificate identity number: 10187917 Approval number(s): ISO 14001 – 0068436 The scope of this approval is applicable to: Design and manufacturing of semiconductor devices and integrated circuits pack. Lloyd's Register Group Limited, its affiliates and subsidiaries, including Lloyd's Register Quality Assurance Limited (LRQA), and their respective officers, employees or agents are, individually and collectively, referred to in this clause as 'Lloyd's Register'. Lloyd's Register assumes no responsibility and shall not be liable to any person for any loss, damage or expense caused by reliance on the information or advice in this document or howsoever provided, unless that person has signed a contract with the relevant Lloyd's Register entity for the provision of this information or advice and in that case any responsibility or liability is exclusively on the terms and conditions set out in that contract. Issued by: Lloyd's Register Inspection Limited Taiwan Branch, Room 1008, 10th Floor, No. -

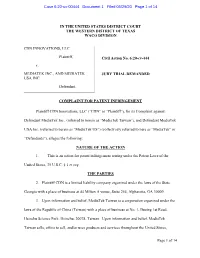

View Complaint

Case 6:20-cv-00444 Document 1 Filed 05/29/20 Page 1 of 14 IN THE UNITED STATES DISTRICT COURT THE WESTERN DISTRICT OF TEXAS WACO DIVISION CDN INNOVATIONS, LLC Plaintiff, Civil Action No. 6:20-cv-444 v. MEDIATEK INC., AND MEDIATEK JURY TRIAL DEMANDED USA INC. Defendant. COMPLAINT FOR PATENT INFRINGEMENT Plaintiff CDN Innovations, LLC (“CDN” or “Plaintiff”), for its Complaint against Defendant MediaTek Inc., (referred to herein as “MediaTek Taiwan”), and Defendant MediaTek USA Inc. (referred to herein as “MediaTek US”) (collectively referred to here as “MediaTek” or “Defendants”), alleges the following: NATURE OF THE ACTION 1. This is an action for patent infringement arising under the Patent Laws of the United States, 35 U.S.C. § 1 et seq. THE PARTIES 2. Plaintiff CDN is a limited liability company organized under the laws of the State Georgia with a place of business at 44 Milton A venue, Suite 254, Alpharetta, GA 30009. 3. Upon information and belief, MediaTek Taiwan is a corporation organized under the laws of the Republic of China (Taiwan) with a place of business at No. 1, Dusing 1st Road, Hsinchu Science Park, Hsinchu, 20078, Taiwan. Upon information and belief, MediaTek Taiwan sells, offers to sell, and/or uses products and services throughout the United States, Page 1 of 14 Case 6:20-cv-00444 Document 1 Filed 05/29/20 Page 2 of 14 including in this judicial district, and introduces infringing products and services into the stream of commerce knowing that they would be sold and/or used in this judicial district and elsewhere in the United States.