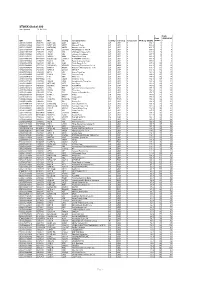

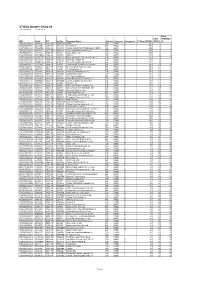

Taiwan's Top 50 Corporates

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

ASUSTEK COMPUTER INC. NON-CONSOLIDATED FINANCIAL STATEMENTS December 31, 2007 and 2006 with Report of Independent Auditors

ASUSTEK COMPUTER INC. NON-CONSOLIDATED FINANCIAL STATEMENTS December 31, 2007 and 2006 With Report of Independent Auditors The reader is advised that these financial statements have been prepared originally in Chinese. In the event of a conflict between these financial statements and the original Chinese version or difference in interpretation between the two versions, the Chinese language financial statements shall prevail. English Translations of Financial Statements Originally Issued in Chinese ASUSTEK COMPUTER INC. NON-CONSOLIDATED BALANCE SHEETS DECEMBER 31, 2007 AND 2006 (Expressed in New Taiwan Thousand Dollars) ASSETS Notes 2007 2006 LIABILITIES AND STOCKHOLDERS' EQUITY Notes 2007 2006 CURRENT ASSETS CURRENT LIABILITIES Cash and cash equivalents II, IV.1 $9,174,219 $10,791,836 Notes and accounts payable $80,372,075 $109,230,069 Financial assets at fair value through profit or loss-current II, IV.2 7 ,257,169 4,218,719 Notes and accounts payable -affiliated companies V 837,669 9,007,117 Notes and accounts receivable-Net II, IV.3 61 ,863,244 80,950,232 Income tax payable II, IV.19 5,795,472 3,558,780 Accounts receivable-affiliated companies-Net II, IV.3, V 45 ,747,118 21,152,900 Accrued expenses II, IV.12, V 31,771,898 21,553,421 Other receivables-Net II,V 5 ,069,634 1,627,107 Other payables V 771,563 469,653 Inventories-Net II, IV.4 53 ,643,865 72,627,961 Receipts in advance V 2,412,198 2,502,732 Prepayments V 121 ,788 162,382 Bonds payable-current portion IV.11 - 6,613,377 Other current assets 101 ,863 - Other current liabilities -

Global Capital, the State, and Chinese Workers: the Foxconn Experience

MCX38410.1177/0097700 447164412447164Pun and ChanModern China © 2012 SAGE Publications Reprints and permission: sagepub.com/journalsPermissions.nav Articles Modern China 38(4) 383 –410 Global Capital, the State, © 2012 SAGE Publications Reprints and permission: and Chinese Workers: sagepub.com/journalsPermissions.nav DOI: 10.1177/0097700412447164 The Foxconn Experience http://mcx.sagepub.com Pun Ngai1 and Jenny Chan2 Abstract In 2010, a startling 18 young migrant workers attempted suicide at Foxconn Technology Group production facilities in China. This article looks into the development of the Foxconn Corporation to understand the advent of capi- tal expansion and its impact on frontline workers’ lives in China. It also pro- vides an account of how the state facilitates Foxconn’s production expansion as a form of monopoly capital. Foxconn stands out as a new phenomenon of capital expansion because of the incomparable speed and scale of its capital accumulation in all regions of China. This article explores how the workers at Foxconn, the world’s largest electronics manufacturer, have been subjected to work pressure and desperation that might lead to suicides on the one hand but also open up daily and collective resistance on the other hand. Keywords global capital, Chinese state, student workers, rural migrant workers, Foxconn Technology Group When Time magazine nominated workers in China as the runners-up for the 2009 Person of the Year, the editor commented that Chinese workers have brightened the future of humanity by “leading the world to economic 1Hong Kong Polytechnic University, Kowloon, Hong Kong 2Royal Holloway, University of London, Surrey, UK Corresponding Author: Pun Ngai, Department of Applied Social Sciences, Hong Kong Polytechnic University, Kowloon, Hong Kong Email: [email protected] 384 Modern China 38(4) recovery” (Time, Dec. -

ZONE COUNTRIES OPERATOR TADIG CODE Calls

Calls made abroad SMS sent abroad Calls To Belgium SMS TADIG To zones SMS to SMS to SMS to ZONE COUNTRIES OPERATOR received Local and Europe received CODE 2,3 and 4 Belgium EUR ROW abroad (= zone1) abroad 3 AFGHANISTAN AFGHAN WIRELESS COMMUNICATION COMPANY 'AWCC' AFGAW 0,91 0,99 2,27 2,89 0,00 0,41 0,62 0,62 3 AFGHANISTAN AREEBA MTN AFGAR 0,91 0,99 2,27 2,89 0,00 0,41 0,62 0,62 3 AFGHANISTAN TDCA AFGTD 0,91 0,99 2,27 2,89 0,00 0,41 0,62 0,62 3 AFGHANISTAN ETISALAT AFGHANISTAN AFGEA 0,91 0,99 2,27 2,89 0,00 0,41 0,62 0,62 1 ALANDS ISLANDS (FINLAND) ALANDS MOBILTELEFON AB FINAM 0,08 0,29 0,29 2,07 0,00 0,09 0,09 0,54 2 ALBANIA AMC (ALBANIAN MOBILE COMMUNICATIONS) ALBAM 0,74 0,91 1,65 2,27 0,00 0,41 0,62 0,62 2 ALBANIA VODAFONE ALBVF 0,74 0,91 1,65 2,27 0,00 0,41 0,62 0,62 2 ALBANIA EAGLE MOBILE SH.A ALBEM 0,74 0,91 1,65 2,27 0,00 0,41 0,62 0,62 2 ALGERIA DJEZZY (ORASCOM) DZAOT 0,74 0,91 1,65 2,27 0,00 0,41 0,62 0,62 2 ALGERIA ATM (MOBILIS) (EX-PTT Algeria) DZAA1 0,74 0,91 1,65 2,27 0,00 0,41 0,62 0,62 2 ALGERIA WATANIYA TELECOM ALGERIE S.P.A. -

The Mineral Industry of Taiwan in 2004

THE MINERAL INDUSTRY OF TAIWAN By Pui-Kwan Tse Taiwan is an island that is located south of Japan and east encourage Taiwanese businesses to stay in Taiwan and would of mainland China in the Pacific Ocean. In 2004, Taiwan’s attract foreign businesses to set up global logistics centers in economy grew by 5.7%, which was the largest increase since Taiwan. Developing service industries such as entertainment, 2000. After reaching a peak of 7.9% in the second quarter, environmental protection, medicine and healthcare, and tourism the economy slowed to 3.3% in the fourth quarter because of and sports recreation would enhance the quality of life in higher global oil prices and the deceleration of export growth Taiwan. The CEPD projected that the service sector would during the second half of the year. The economic growth was grow 6.1% per year through 2008 and that the percentage of the generated by private consumption and investment. Private GDP generated by the service sector would increase to 67% in consumption increased by 3.1% and private investment rose by 2008 from 63.5% in 2003 (Taiwan Headlines, 2004b§; 2005d§). 28.2% compared with that of the previous year. The recovery The Taiwan authorities carried out the second phase of of the information and communication technologies industry Taiwan’s financial reform program in 2004. The number of was the main reason for the increased business investment. In state-owned banks (banks in which the government held 30% 2004, Government fixed investment decreased by 4.2% because or more interest) would be reduced to 6 from 12 at yearend of higher prices on construction materials and because some 2005. -

Taiwan Semiconductor Manufacturing Company Limited and Subsidiaries

Taiwan Semiconductor Manufacturing Company Limited and Subsidiaries Consolidated Financial Statements for the Nine Months Ended September 30, 2020 and 2019 and Independent Auditors’ Review Report Taiwan Semiconductor Manufacturing Company Limited and Subsidiaries NOTES TO CONSOLIDATED FINANCIAL STATEMENTS FOR THE NINE MONTHS ENDED SEPTEMBER 30, 2020 AND 2019 (Amounts in Thousands of New Taiwan Dollars, Unless Specified Otherwise) (Reviewed, Not Audited) 1. GENERAL Taiwan Semiconductor Manufacturing Company Limited (TSMC), a Republic of China (R.O.C.) corporation, was incorporated on February 21, 1987. TSMC is a dedicated foundry in the semiconductor industry which engages mainly in the manufacturing, selling, packaging, testing and computer-aided design of integrated circuits and other semiconductor devices and the manufacturing of masks. On September 5, 1994, TSMC’s shares were listed on the Taiwan Stock Exchange (TWSE). On October 8, 1997, TSMC listed some of its shares of stock on the New York Stock Exchange (NYSE) in the form of American Depositary Shares (ADSs). The address of its registered office and principal place of business is No. 8, Li-Hsin Rd. 6, Hsinchu Science Park, Taiwan. The principal operating activities of TSMC’s subsidiaries are described in Note 4. 2. THE AUTHORIZATION OF FINANCIAL STATEMENTS The accompanying consolidated financial statements were reported to the Board of Directors and issued on November 10, 2020. 3. APPLICATION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS a. Initial application of the amendments to the International Financial Reporting Standards (IFRS), International Accounting Standards (IAS), IFRIC Interpretations (IFRIC), and SIC Interpretations (SIC) (collectively, “IFRSs”) endorsed and issued into effect by the Financial Supervisory Commission (FSC) The initial application of the amendments to the IFRSs endorsed and issued into effect by the FSC did not have a significant effect on TSMC and its subsidiaries’ (collectively as the “Company”) accounting policies. -

USD XINT M EM HL Taiwan NTR USD Index

Created on 30 th April 2020 XINT M EM HL Taiwan NTR USD Index USD The XINT M EM HL Taiwan NTR USD Index covers the highly liquid and liquid segment of the Taiwanese equity market. The index membership comprises the 89 largest companies by freefloat adjusted market value and represents approximately 85% of the Taiwanese market. INDEX PERFORMANCE - PRICE RETURN USD 130 120 110 100 90 80 70 Dec 2017 Mar 2018 Jun 2018 Sep 2018 Dec 2018 Mar 2019 Jun 2019 Sep 2019 Dec 2019 Mar 2020 Index Return % annualised Standard Deviation % annualised Maximum Drawdown 3M -7.33 3M 36.87 From 14 Jan 2020 6M 1.07 6M 27.83 To 19 Mar 2020 1Y 11.14 1Y 22.27 Return -29.23% Index Intelligence GmbH - Grosser Hirschgraben 15 - 60311 Frankfurt am Main Tel.: +49 69 247 5583 50 - [email protected] www.index-int.com TOP 10 Largest Constituents FFMV million Weight Industry Sector Taiwan Semiconductor Man Co Ltd 37.57% 252,160 37.57% Technology Hon Hai Precision Industry Co Ltd 4.81% 32,296 4.81% Industrial Goods & Services MediaTek Inc 3.14% 21,069 3.14% Technology Chunghwa Telecom Co Ltd 2.08% 13,992 2.08% Telecommunications Largan Precision Co Ltd 2.07% 13,900 2.07% Personal & Household Goods Formosa Plastics Corp 1.96% 13,167 1.96% Chemicals CTBC Financial Holding Co Ltd 1.86% 12,453 1.86% Banks Nan Ya Plastics Corp 1.71% 11,472 1.71% Chemicals Uni-President Enterprises Corp 1.68% 11,284 1.68% Food & Beverage Mega Financial Holding Co Ltd 1.64% 11,009 1.64% Banks Total 392,803 58.52% This information has been prepared by Index Intelligence GmbH (“IIG”). -

STOXX Global 200 Last Updated: 01.02.2018

STOXX Global 200 Last Updated: 01.02.2018 Rank Rank (PREVIOUS ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) ) US0378331005 2046251 AAPL.OQ AAPL Apple Inc. US USD Y 694.2 1 1 US5949181045 2588173 MSFT.OQ MSFT Microsoft Corp. US USD Y 588.4 2 2 US0231351067 2000019 AMZN.OQ AMZN Amazon.com Inc. US USD Y 466.7 3 3 US30303M1027 B7TL820 FB.OQ US20PD FACEBOOK CLASS A US USD Y 355.6 4 4 US46625H1005 2190385 JPM.N CHL JPMorgan Chase & Co. US USD Y 329.9 5 5 US4781601046 2475833 JNJ.N JNJ Johnson & Johnson US USD Y 297.7 6 6 US30231G1022 2326618 XOM.N XON Exxon Mobil Corp. US USD Y 296.9 7 7 US02079K1079 BYY88Y7 GOOG.OQ US40C2 ALPHABET CLASS C US USD Y 289.1 8 8 US0605051046 2295677 BAC.N NB Bank of America Corp. US USD Y 250.0 9 9 US9497461015 2649100 WFC.N NOB Wells Fargo & Co. US USD Y 237.5 10 11 KR7005930003 6771720 005930.KS KR002D Samsung Electronics Co Ltd KR KRW Y 223.3 11 10 US0846707026 2073390 BRKb.N BRKB Berkshire Hathaway Inc. Cl B US USD Y 218.2 12 13 CH0038863350 7123870 NESN.S 461669 NESTLE CH CHF Y 216.1 13 12 US4370761029 2434209 HD.N HD Home Depot Inc. US USD Y 192.8 14 17 US1667641005 2838555 CVX.N CHV Chevron Corp. US USD Y 190.6 15 15 US00206R1023 2831811 T.N SBC AT&T Inc. US USD Y 184.6 16 14 US92826C8394 B2PZN04 V.N U0401 VISA Inc. -

Representative Legal Matters Mark W.C

Representative Legal Matters Mark W.C. Tu Represented KKR in relation to its proposed buyout of Yageo Corporation. Represented Advanced Semiconductor Engineering Inc. in its acquisition of 100 percent shares of PowerASE Technology by way of tender offer and merger. Represented Morgan Stanley, the financial advisor to Polaris Securities Corporation, in relation to its share swap with Yuanta Financial Holding Company. Represented MediaTek Inc. for acquisition of 100 percent of outstanding shares of Ralink Technology Corporation by way of a share swap. Represented Chimei Optoelectronics Corporation in relation to its merger with Innolux Corporation. Represented Morgan Stanley, the financial advisor to Taiwan International Securities Corporation (TISC), in relation to the sale of all issued and outstanding shares of TISC to Capital Securities Corporation by way of a tender offer followed by a merger. Represented E.Sun Commercial Bank in its general business and asset assumption from Chu Nan Co-operative Credit Association. Represented Prime View International Co., Ltd. in relation to its acquisition of E. Ink Corporation by way of a share exchange. Represented Morgan Stanley Private Equity in its acquisition of a stake in CTCI Corporation. Representing WIN Semiconductors Corporation in relation to its issuance of global depositary receipts. Represented E.Sun Financial Holding Company. in relation to its issuance of global depositary receipts. Represented Cathay Financial Holding Company in relation to its issuance of European convertible bonds. Represented Chunghwa Telecom Co., Ltd. in relation to its Form 20-F filing submitted to the U.S. Securities and Exchange Commission. Represented Pegatron Corporation in relation to its issuance of European convertible bonds. -

STOXX Greater China 80 Last Updated: 01.08.2017

STOXX Greater China 80 Last Updated: 01.08.2017 Rank Rank (PREVIOU ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) S) TW0002330008 6889106 2330.TW TW001Q TSMC TW TWD Y 113.9 1 1 HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 80.6 2 2 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 60.5 3 3 TW0002317005 6438564 2317.TW TW002R Hon Hai Precision Industry Co TW TWD Y 51.5 4 4 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 50.8 5 5 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 41.3 6 6 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 32.0 7 9 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 31.8 8 7 KYG217651051 BW9P816 0001.HK 619027 CK HUTCHISON HOLDINGS HK HKD Y 31.1 9 8 HK0388045442 6267359 0388.HK 626735 Hong Kong Exchanges & Clearing HK HKD Y 28.0 10 10 HK0016000132 6859927 0016.HK 685992 Sun Hung Kai Properties Ltd. HK HKD Y 20.6 11 12 HK0002007356 6097017 0002.HK 619091 CLP Holdings Ltd. HK HKD Y 20.0 12 11 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 20.0 13 13 TW0003008009 6451668 3008.TW TW05PJ LARGAN Precision TW TWD Y 19.7 14 15 KYG2103F1019 BWX52N2 1113.HK HK50CI CK Property Holdings HK HKD Y 18.3 15 14 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 16.4 16 16 HK0823032773 B0PB4M7 0823.HK B0PB4M Link Real Estate Investment Tr HK HKD Y 15.4 17 19 HK0883013259 B00G0S5 0883.HK 617994 CNOOC Ltd. -

Formosa Plastics Corporation Financial Statements December 31, 2017 and 2016

1 Stock Code:1301 (English Translation of Financial Statements and Report Originally Issued in Chinese) FORMOSA PLASTICS CORPORATION FINANCIAL STATEMENTS DECEMBER 31, 2017 AND 2016 (With Independent Auditors’ Report Thereon) Address:No.100, Shuiguan Rd., Renwu Dist., Kaohsiung City 814, Taiwan (R.O.C.) Telephone:(07)371-1411;(02)2712-2211 The independent auditors’ report and the accompanying financial statements are the English translation of the Chinese version prepared and used in the Republic of China. If there is any conflict between, or any difference in the interpretation of, the English and Chinese language independent auditors’ report and financial statements, the Chinese version shall prevail. 2 Table of Contents Contents Page 1. Cover Page 1 2. Table of Contents 2 3. Independent Auditors’ Report 3 4. Balance Sheets 4 5. Statements of Comprehensive Income 5 6. Statements of Changes in Equity 6 7. Statements of Cash Flows 7 8. Notes to Financial Statements (1) Company history 8 (2) Approval date and procedures of the financial statements 8 (3) Application of new standards, amendments and interpretations 8~13 (4) Summary of significant accounting policies 13~25 (5) Critical accounting judgments and key sources of estimation uncertainly 26 (6) Significant account disclosures 26~55 (7) Related-party transactions 55~61 (8) Pledged properties 61 (9) Significant commitments and contingencies 61~62 (10) Losses due to major disasters 62 (11) Subsequent events 62 (12) Other 62 (13) Other disclosures (a) Information on significant transactions 63~68 (b) Information on investees 69 (c) Information on investment in mainland China 69 (14) Segment information 69 3 KPMG 〵⻍䋑11049⥌纏騟5媯7贫68垜(〵⻍101㣐垜) Telephone ꨶ鑨 + 886 (2) 8101 6666 68F., TAIPEI 101 TOWER, No. -

Inventec Corporation

(English Translation of Pro Forma Financial Report Originally Issued in Chinese) PEGATRON CORPORATION AND ITS SUBSIDIARIES PRO FORMA CONSOLIDATED FINANCIAL STATEMENTS DECEMBER 31, 2008 AND 2007 (With Independent Auditors’ Report Thereon) Address: 5F., No.76, Ligong St., Beitou District, Taipei City 112, Taiwan Telephone: 886-2-8143-9001 - 1 - TABLE OF CONTENTS Contents Page Cover Page 1 Table of Contents 2 Independent Auditors’ Report 3 Pro Forma Consolidated Balance Sheets 4 Pro Forma Consolidated Statements of Income 5 Pro Forma Consolidated Statements of Changes in Stockholders’ Equity 6 Pro Forma Consolidated Statements of Cash Flows 7 Notes to Pro Forma Consolidated Financial Statements (1) Organization and Business 8 (2) Summary of Significant Accounting Policies 8-28 (3) Reasons for and Effects of Accounting Changes 28 (4) Summary of Major Accounts 28-49 (5) Related-Party Transactions 50-56 (6) Pledged Assets 56 (7) Significant Commitments and Contingencies 57-58 (8) Significant Catastrophic Losses 59 (9) Significant Subsequent Events 59 (10) Others 59 (11)Additional Disclosures 60-61 (12)Segment Information 61-62 - 2 - (English Translation of Financial Report Originally Issued in Chinese) PEGATRON CORPORATION AND ITS SUBSIDIARIES PRO FORMA CONSOLIDATED BALANCE SHEETS DECEMBER 31, 2008 AND 2007 (All Amounts Expressed in Thousands of New Taiwan Dollars, Except for Share Data) December 31, 2008 December 31, 2007 Amount % Amount % ASSETS Current Asset: Cash (Notes 2 and 4(1)) $ 27,065,987 12 26,294,882 9 Financial assets reported