Full Report – BP Statistical Review of World Energy 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Coal and Oil: the Dark Monarchs of Global Energy – Understanding Supply and Extraction Patterns and Their Importance for Futur

nam et ipsa scientia potestas est List of Papers This thesis is based on the following papers, which are referred to in the text by their Roman numerals. I Höök, M., Aleklett, K. (2008) A decline rate study of Norwe- gian oil production. Energy Policy, 36(11):4262–4271 II Höök, M., Söderbergh, B., Jakobsson, K., Aleklett, K. (2009) The evolution of giant oil field production behaviour. Natural Resources Research, 18(1):39–56 III Höök, M., Hirsch, R., Aleklett, K. (2009) Giant oil field decline rates and their influence on world oil production. Energy Pol- icy, 37(6):2262–2272 IV Jakobsson, K., Söderbergh, B., Höök, M., Aleklett, K. (2009) How reasonable are oil production scenarios from public agen- cies? Energy Policy, 37(11):4809–4818 V Höök M, Söderbergh, B., Aleklett, K. (2009) Future Danish oil and gas export. Energy, 34(11):1826–1834 VI Aleklett K., Höök, M., Jakobsson, K., Lardelli, M., Snowden, S., Söderbergh, B. (2010) The Peak of the Oil Age - analyzing the world oil production Reference Scenario in World Energy Outlook 2008. Energy Policy, 38(3):1398–1414 VII Höök M, Tang, X., Pang, X., Aleklett K. (2010) Development journey and outlook for the Chinese giant oilfields. Petroleum Development and Exploration, 37(2):237–249 VIII Höök, M., Aleklett, K. (2009) Historical trends in American coal production and a possible future outlook. International Journal of Coal Geology, 78(3):201–216 IX Höök, M., Aleklett, K. (2010) Trends in U.S. recoverable coal supply estimates and future production outlooks. Natural Re- sources Research, 19(3):189–208 X Höök, M., Zittel, W., Schindler, J., Aleklett, K. -

Oil Shale and Tar Sands

Fundamentals of Materials for Energy and Environmental Sustainability Editors David S. Ginley and David Cahen Oil shale and tar sands James W. Bunger 11 JWBA, Inc., Energy Technology and Engineering, Salt Lake City, UT, USA 11.1 Focus 11.2 Synopsis Tar sands and oil shale are “uncon- Oil shale and tar sands occur in dozens of countries around the world. With in-place ventional” oil resources. Unconven- resources totaling at least 4 trillion barrels (bbl), they exceed the world's remaining tional oil resources are characterized petroleum reserves, which are probably less than 2 trillion bbl. As petroleum becomes by their solid, or near-solid, state harder to produce, oil shale and tar sands are finding economic and thermodynamic under reservoir conditions, which parity with petroleum. Thermodynamic parity, e.g., similarity in the energy cost requires new, and sometimes of producing energy, is a key indicator of economic competitiveness. unproven, technology for their Oil is being produced on a large commercial scale by Canada from tar sands, recovery. For tar sands the hydrocar- and to a lesser extent by Venezuela. The USA now imports well over 2 million barrels bon is a highly viscous bitumen; for of oil per day from Canada, the majority of which is produced from tar sands. oil shale, it is a solid hydrocarbon Production of oil from oil shale is occurring in Estonia, China, and Brazil albeit on called “kerogen.” Unconventional smaller scales. Importantly, the USA is the largest holder of oil-shale resources. oil resources are found in greater For that reason alone, and because of the growing need for imports in the USA, quantities than conventional petrol- oil shale will receive greater development attention as petroleum supplies dwindle. -

Jersey Energy Trends 2018 Report

Energy Trends 2018 Statistics Jersey: www.gov.je/statistics Overview This report examines supply and use of energy in Jersey through the importation, distribution and consumption of fuels such as petroleum products and electricity. The focus of the report is on energy supply and use in 2018. Figures are also presented for calendar years 2014 to 2017. Longer term trends, going back to 1991, are shown for road fuel consumption and for electricity importation and generation. The energy data presented in this report provides the basis for calculating carbon emissions for Jersey. Through the UK, Jersey is a signatory to the Kyoto Protocol; the document “Pathway 2050: An Energy Plan for Jersey”11outlines how the Island intends to reduce its carbon emissions in line with the commitments of the UK and other European nations. Jersey’s energy data is submitted annually to the compilers of the UK’s national greenhouse gas inventory, Aether, who independently verify and validate the data using internationally agreed methodologies. The resultant emissions calculated for Jersey are published by Aether2 and submitted to the international inventories as part of the UK’s national inventory. Summary for 2018 Supply • almost all of Jersey’s energy supply was imported; about 2% was produced on-Island as electricity generated by the Energy from Waste Facility • petroleum products accounted for almost two-thirds (63%) of Jersey’s energy supply; electricity (imported and on-Island generated) accounted for the remainder (37%) • Jersey’s total primary energy -

Peak Oil, Peak Energy Mother Nature Bats Last

Peak Oil, Peak Energy Mother Nature Bats Last Martin Sereno 1 Feb 2011 (orig. talk: Nov 2004) Oil is the Lifeblood of Industrial Civilization • 80 million barrels/day, 1000 barrels/sec, 1 cubic mile/year • highly energy-dense • easy to transport, store • moves goods and people • allows us to fly (there will never be a battery-operated jet plane) • digs huge holes and puts up huge buildings • ballooned our food supply (fertilize, cultivate, irrigate, transport) • our 'stuff' is made from it (iPods to the roads themselves) • we're not "addicted to oil" -- that's like saying a person has an "addiction to blood" Where Oil Comes From • raw organic material for oil (e.g., from plankton) is present in low concentrations in ‘all’ sedimentary rocks, but esp. from two warm periods 90 million and 140 million years ago • temperature rises with depth (radioactivity, Kelvin’s mistake) • oil is generated in rocks heated to 60-120 deg Celsius • rocks at this temp. occur at different depths in different places (N.B.: water depth doesn't count) • oil is ‘cracked’ to natural gas at higher temps (deeper) • abiotic oil from “crystalline basement” is negligible, if it exists • exhausted oil fields do not refill Recoverable Oil • oil must collect in a “trap” to be practically recoverable • a trap is a permeable layer capped by an impermeable one • obvious traps: anticlines, domes (“oil in those hills”) • less obvious traps found by seismic imaging: turned up edges of salt domes, near buried meteorite crater (Mexico) • harder-to-get-at traps: shallow continental shelf (GOM) • even-harder-to-get-at traps: edge continental slope (Macondo, resevoir pressure: 12,000 pounds [6 tons] per sq inch) • essentially no oil in basaltic ocean floor or granitic basement (Used to be!) Second Largest Oilfield Cantarell used to supply 2% of world oil (water) Guzman, A.E. -

Statoil ASA Statoil Petroleum AS

Offering Circular A9.4.1.1 Statoil ASA (incorporated with limited liability in the Kingdom of Norway) Notes issued under the programme may be unconditionally and irrevocably guaranteed by Statoil Petroleum AS (incorporated with limited liability in the Kingdom of Norway) €20,000,000,000 Euro Medium Term Note Programme On 21 March 1997, Statoil ASA (the Issuer) entered into a Euro Medium Term Note Programme (the Programme) and issued an Offering Circular on that date describing the Programme. The Programme has been subsequently amended and updated. This Offering Circular supersedes any previous dated offering circulars. Any Notes (as defined below) issued under the Programme on or after the date of this Offering Circular are issued subject to the provisions described herein. This does not affect any Notes issued prior to the date hereof. Under this Programme, Statoil ASA may from time to time issue notes (the Notes) denominated in any currency agreed between the Issuer and the relevant Dealer (as defined below). The Notes may be issued in bearer form or in uncertificated book entry form (VPS Notes) settled through the Norwegian Central Securities Depositary, Verdipapirsentralen ASA (the VPS). The maximum aggregate nominal amount of all Notes from time to time outstanding will not exceed €20,000,000,000 (or its equivalent in other currencies calculated as described herein). The payments of all amounts due in respect of the Notes issued by the Issuer may be unconditionally and irrevocably guaranteed by Statoil A6.1 Petroleum AS (the Guarantor). The Notes may be issued on a continuing basis to one or more of the Dealers specified on page 6 and any additional Dealer appointed under the Programme from time to time, which appointment may be for a specific issue or on an ongoing basis (each a Dealer and together the Dealers). -

Press Release

Press Release First quarter 2021 results With results of more than $3 billion, Total fully benefits from rebound in hydrocarbon prices LNG and renewables represent one-third of results Change Change 1Q21 1Q20 1Q19 vs 1Q20 vs 1Q19 Oil price - Brent ($/b) 61.1 50.1 +22% 63.1 -3% Average price of LNG ($/Mbtu) 6.1 6.3 -4% 7.2 -16% Variable cost margin - Refining Europe, VCM ($/t) 5.3 26.3 -80% 33.0 -84% Adjusted net income (Group share)1 - in billions of dollars (B$) 3.0 1.8 69% 2.8 +9% - in dollars per share 1.10 0.66 +68% 1.02 +8% DACF1 (B$) 5.8 4.3 +34% 6.3 -8% Cash Flow from operations (B$) 5.6 1.3 x4.3 3.6 +54% Net income (Group share) of 3.3 B$ in 1Q21 Net-debt-to-capital ratio of 19.5% at March 31, 2021 vs. 21.7% at December 31, 20202 Hydrocarbon production of 2,863 kboe/d in 1Q21, a decrease of 7% compared to 1Q20 First 2021 interim dividend set at 0.66 €/share 2 Paris, April 29, 2021 - The Board of Directors of Total SE, meeting on April 28, 2021, under the chairmanship of Chairman and Chief Executive Officer Patrick Pouyanné, approved the Group's first quarter 2021 accounts. On this occasion, Patrick Pouyanné said: « In the first quarter, the Group fully benefited from rising oil and gas prices, up 38% and 24%, respectively quarter-to- quarter, and its strategy to grow LNG and Renewables and Electricity. -

Crude Oil Reserves 1986

o un E I Introduction FACTS AND FIGURES is produced annually at the OPEC Secretariat in Vienna, to assist people requiring a means of rapidly assimilating important facts about the energy industry, without themselves having to delve into time- consuming research from an array of sources. Since it is the belief of OPEC Member Countries that energy cannot be viewed in isolation from other global economic considerations, parts of this booklet broach such related issues as comparisons between the economic fortunes of industrialized and developing nations. A wide range of authoritative sources have been con- sulted in producing this booklet. Where disparities have occurred among sources, great pains have been taken at the Secretariat to distill those figures which most faithfully reflect observed market trends. The graphs are presented in six sections. The first three examine energy issues on a global scale, the next two con- centrate on OPEC, while the final one makes broad econ- omic comparisons between different world groupings. It is hoped that this latest issue of FACTS AND FIGURES, which covers the period up to the end of 1986, will prove of interest and value to its readers. November 1987 Published by: The Secretariat, Organization of the Petroleum Exporting Countries, Obere Donaustrasse 93, A-1020 Vienna, Austria 1987 Printed in Austria by H Carl UeberreuterGes. m. b. H-, Vienna OPEC flows of crude and refined oil — 1986 I I OPEC Far East 4 Indonesia ^| OPEC Latin America - 2 Ecuador; 13 Venezuela • OPEC Africa 1 Algeria; 3 Gabon; 9 -

Secure Fuels from Domestic Resources ______Profiles of Companies Engaged in Domestic Oil Shale and Tar Sands Resource and Technology Development

5th Edition Secure Fuels from Domestic Resources ______________________________________________________________________________ Profiles of Companies Engaged in Domestic Oil Shale and Tar Sands Resource and Technology Development Prepared by INTEK, Inc. For the U.S. Department of Energy • Office of Petroleum Reserves Naval Petroleum and Oil Shale Reserves Fifth Edition: September 2011 Note to Readers Regarding the Revised Edition (September 2011) This report was originally prepared for the U.S. Department of Energy in June 2007. The report and its contents have since been revised and updated to reflect changes and progress that have occurred in the domestic oil shale and tar sands industries since the first release and to include profiles of additional companies engaged in oil shale and tar sands resource and technology development. Each of the companies profiled in the original report has been extended the opportunity to update its profile to reflect progress, current activities and future plans. Acknowledgements This report was prepared by INTEK, Inc. for the U.S. Department of Energy, Office of Petroleum Reserves, Naval Petroleum and Oil Shale Reserves (DOE/NPOSR) as a part of the AOC Petroleum Support Services, LLC (AOC- PSS) Contract Number DE-FE0000175 (Task 30). Mr. Khosrow Biglarbigi of INTEK, Inc. served as the Project Manager. AOC-PSS and INTEK, Inc. wish to acknowledge the efforts of representatives of the companies that provided information, drafted revised or reviewed company profiles, or addressed technical issues associated with their companies, technologies, and project efforts. Special recognition is also due to those who directly performed the work on this report. Mr. Peter M. Crawford, Director at INTEK, Inc., served as the principal author of the report. -

OPEC in a Shale Oil World

OPEC in a Shale Oil World Mohamed Ramady • Wael Mahdi OPEC in a Shale Oil World Where to Next? Mohamed Ramady Wael Mahdi Department of Finance and Economics Regus, Building 12, Level 4 Trust Tower Visiting Associate Professor OPEC & Middle East Energy King Fahd University of Petroleum Correspondent Bloomberg News and Minerals Manama , Bahrain Dhahran , Saudi Arabia ISBN 978-3-319-22370-4 ISBN 978-3-319-22371-1 (eBook) DOI 10.1007/978-3-319-22371-1 Library of Congress Control Number: 2015946616 Springer Cham Heidelberg New York Dordrecht London © Springer International Publishing Switzerland 2015 This work is subject to copyright. All rights are reserved by the Publisher, whether the whole or part of the material is concerned, specifi cally the rights of translation, reprinting, reuse of illustrations, recitation, broadcasting, reproduction on microfi lms or in any other physical way, and transmission or information storage and retrieval, electronic adaptation, computer software, or by similar or dissimilar methodology now known or hereafter developed. The use of general descriptive names, registered names, trademarks, service marks, etc. in this publication does not imply, even in the absence of a specifi c statement, that such names are exempt from the relevant protective laws and regulations and therefore free for general use. The publisher, the authors and the editors are safe to assume that the advice and information in this book are believed to be true and accurate at the date of publication. Neither the publisher nor the authors or the editors give a warranty, express or implied, with respect to the material contained herein or for any errors or omissions that may have been made. -

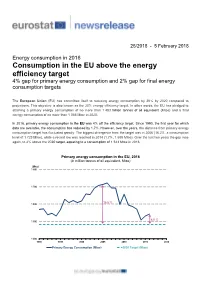

Consumption in the EU Above the Energy Efficiency Target 4% Gap for Primary Energy Consumption and 2% Gap for Final Energy Consumption Targets

25/2018 - 5 February 2018 Energy consumption in 2016 Consumption in the EU above the energy efficiency target 4% gap for primary energy consumption and 2% gap for final energy consumption targets The European Union (EU) has committed itself to reducing energy consumption by 20% by 2020 compared to projections. This objective is also known as the 20% energy efficiency target. In other words, the EU has pledged to attaining a primary energy consumption of no more than 1 483 million tonnes of oil equivalent (Mtoe) and a final energy consumption of no more than 1 086 Mtoe in 2020. In 2016, primary energy consumption in the EU was 4% off the efficiency target. Since 1990, the first year for which data are available, the consumption has reduced by 1.7%. However, over the years, the distance from primary energy consumption target has fluctuated greatly. The biggest divergence from the target was in 2006 (16.2%, a consumption level of 1 723 Mtoe), while a record low was reached in 2014 (1.7%, 1 509 Mtoe). Over the last two years the gap rose again, to 4% above the 2020 target, equating to a consumption of 1 543 Mtoe in 2016. Primary energy consumption in the EU, 2016 (in million tonnes of oil equivalent, Mtoe) (Mtoe) 1 800 1 700 15.5 % 1 600 4.0 % 1 500 1 400 1990 1995 2000 2005 2010 2015 2020 Primary Energy Consumption (Mtoe) 2020 Target (Mtoe) In 2016, final energy consumption in the EU was 1 108 Mtoe, 2.0% above the efficiency target. -

Unconventional Oil Resources Exploitation: a Review

Acta Montanistica Slovaca Volume 21 (2016), number 3, 247-257 Unconventional oil resources exploitation: A review Šárka Vilamová 1, Marian Piecha 2 and Zden ěk Pavelek 3 Unconventional crude oil sources are geographically extensive and include the tar sands of the Province of Alberta in Canada, the heavy oil belt of the Orinoco region of Venezuela and the oil shales of the United States, Brazil, India and Malagasy. High production costs and low oil prices have hitherto inhibited the inclusion of unconventional oil resources in the world oil resource figures. In the last decade, developing production technologies, coupled with the higher market value of oil, convert large quantities of unconventional oil into an effective resource. From the aspect of quantity and technological and economic recoverability are actually the most important tar sands. Tar sands can be recovered via surface mining or in-situ collection techniques. This is an up-stream part of exploitation process. Again, this is more expensive than lifting conventional petroleum, but for example, Canada's Athabasca (Alberta) Tar Sands is one example of unconventional reserve that can be economically recoverable with the largest surface mining machinery on the waste landscape with important local but also global environmental impacts. The similar technology of up-stream process concerns oil shales. The downstream part process of solid unconventional oil is an energetically difficult process of separation and refining with important increasing of additive carbon production and increasing of final product costs. In the region of Central Europe is estimated the mean volume of 168 million barrels of technically recoverable oil and natural gas liquids situated in Ordovician and Silurian age shales in the Polish- Ukrainian Foredeep basin of Poland. -

The Impact of the Decline in Oil Prices on the Economics, Politics and Oil Industry of Venezuela

THE IMPACT OF THE DECLINE IN OIL PRICES ON THE ECONOMICS, POLITICS AND OIL INDUSTRY OF VENEZUELA By Francisco Monaldi SEPTEMBER 2015 B | CHAPTER NAME ABOUT THE CENTER ON GLOBAL ENERGY POLICY The Center on Global Energy Policy provides independent, balanced, data-driven analysis to help policymakers navigate the complex world of energy. We approach energy as an economic, security, and environmental concern. And we draw on the resources of a world-class institution, faculty with real-world experience, and a location in the world’s finance and media capital. Visit us atenergypolicy. columbia.edu facebook.com/ColumbiaUEnergy twitter.com/ColumbiaUEnergy ABOUT THE SCHOOL OF INTERNATIONAL AND PUBLIC AFFAIRS SIPA’s mission is to empower people to serve the global public interest. Our goal is to foster economic growth, sustainable development, social progress, and democratic governance by educating public policy professionals, producing policy-related research, and conveying the results to the world. Based in New York City, with a student body that is 50 percent international and educational partners in cities around the world, SIPA is the most global of public policy schools. For more information, please visit www.sipa.columbia.edu THE IMPACT OF THE DECLINE IN OIL PRICES ON THE ECONOMICS, POLITICS AND OIL INDUSTRY OF VENEZUELA By Francisco Monaldi* SEPTEMBER 2015 *Francisco Monaldi is Baker Institute Fellow in Latin American Energy Policy and Adjunct Professor of Energy Economics at Rice University, Belfer Center Associate in Geopolitics of Energy at the Harvard Kennedy School, Professor at the Instituto de Estudios Superiores de Administracion (IESA) in Caracas, Venezuela, and Founding Director of IESA’s Center on Energy and the Environment.