Media Buzz Large Regional TV Opportunity; Competitive Intensity on the Rise

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Liste Complète Des Chaînes Du Pack Raj IPTV

Liste complète des chaînes du Pack Raj IPTV Indien Pakistan Sud-indien Colors TV HD India ARY Digital Sun TV – Tamil 9X Jalwa (Best) ARY Digital (Feed 2) Jaya Movies – Tamil 9X Music ARY Music Raj TV – Tamil SAB TV Duniya News Raj Music – Malayalam B4U Music HD Express News KTV – Tamil Pogo Hindi Geo News – SD Raj Vissa – Telugu Zee Classic HD Geo News – HD Maa UTV Action HD Geo TV Surya TV – Malayalam B4U Movies HD Geo TV Pak – HD Kantipur TV Times News English Hum TV – HD Nepal Star Plus HD Hum TV – HD (Feed 2) Jeevan – Malayalam Star Gold HD CNBC Pak HD Asia Net News – Malayalam Star Cricket HD Noor TV Zee Marathi Ten Cricket HD Peace TV Star Pravah – Marthi Sony ARY QTV MI Marathi Setmax ARY News HD Uday ATV – Kannada Zee TV HD ARY ZAQU ATN Bangla News Zee Cinema Masala TV NTV HD Zoom TV Express ENT Zee Bangla Zee Jagran / Astha Indus Vision HD Star Viijay - Tamil NDTV Hind News PTV Global NDTV Profit Metero One HD Film Mazia HD Film World HD Dawn News HD Punjabi Anglais Sports & Arabe Sangat TV Animal Planet HD Geo Super HD DD Punjabi National Geo HD News One MH1 BBC World HD Sport 1 HD Chardikala Time TV Cartoon Network Sport 2 HD British Asia Disney Cinemajic Sport 3 HD PTC Punjabi Fox Premier Sport 4 HD PTC News HBO HD Zee Café Zee Punjabi Max Cinema HD Neo Prime Life OK National Geo ADV HD Ten Sport HD AAj TAK News HD Star World HD Dubai Sport HD Ajazeera News Men & Movies Aljazeera Doc HD ETC Punjabi Aljazeera Kids HD RTM 1 – Live Aljazeera Baraem HD RTM 2 – Live Sharjah TV HD MTV India Somali TV HD UTV Movies BBC Arabic HD UTV Star Saudi Arab Saudi Sport . -

11. Mumbai & Thane

11. MUMBAI & THANE Service Name City BST Silver Gold Sony Mumbai & Thane N Y Y Sony SAB Mumbai & Thane N Y Y Colors Mumbai & Thane N Y Y Rishtey Mumbai & Thane N Y Y Sony PAL Mumbai & Thane N Y Y Shop CJ Mumbai & Thane N Y Y Home Shop 18 Mumbai & Thane Y Y Y I D Mumbai & Thane N Y Y Zoom Mumbai & Thane N N Y Epic Mumbai & Thane N N N ETV Bihar JH Mumbai & Thane N Y Y ETV MP CG Mumbai & Thane N Y Y ETV Rajasthan Mumbai & Thane N Y Y ETV UP UK Mumbai & Thane N Y Y DEN snapdeal tv-shop Mumbai & Thane Y Y Y Sahara One Mumbai & Thane N Y Y DD National Mumbai & Thane Y Y Y DD Rajasthan Mumbai & Thane Y Y Y DD Uttar Pradesh Mumbai & Thane Y Y Y DD Madhya Pradesh Mumbai & Thane Y Y Y DD Bihar Mumbai & Thane Y Y Y Sony MAX Mumbai & Thane N Y Y SONY MAX 2 Mumbai & Thane N Y Y B4U Movies Mumbai & Thane N Y Y Cinema TV Mumbai & Thane N Y Y Multiplex Mumbai & Thane Y Y Y DEN Cinema Mumbai & Thane Y Y Y Filmy Mumbai & Thane N N Y DEN Movies Mumbai & Thane N Y Y AXN Mumbai & Thane N Y Y Comedy Central Mumbai & Thane N Y Y Colors Infinity Mumbai & Thane N Y Y DSN INFO Mumbai & Thane Y Y Y Sony PIX Mumbai & Thane N Y Y Movies Now Mumbai & Thane N N Y Romedy Now Mumbai & Thane N N Y Discovery Turbo Mumbai & Thane N Y Y TLC Mumbai & Thane N Y Y Fashion TV Mumbai & Thane N N Y Food Food Mumbai & Thane N N Y News 18 India Mumbai & Thane N Y Y India TV Mumbai & Thane Y Y Y News 24 Mumbai & Thane N N N Aajtak Tez Mumbai & Thane N Y Y ABP News Mumbai & Thane Y Y Y Aajtak Mumbai & Thane N Y Y News Nation Mumbai & Thane Y Y Y India News Mumbai & Thane Y Y Y DD -

भारतीय Čबंध संùथान, लखनऊ Tender Document for Direct To

भारतीय बंध सं थान ,,, लखनऊ INDIAN INSTITUTE OF MANAGEMENT, LUCKNOW Prabandh Nagar, IIM Road, Lucknow – 226013 TENDER DOCUMENT FOR DIRECT TO HOME SD CONNECTIONS FOR IIM LUCKNOW NIT NO. DT.01/07/2019 Tender No. IIML/PUR/DTH /17/2019-20 Published Date 01/07/2019 Pre Bid Meeting 12/07/2019 at 11:00 AM Last Date of Bid 24/07/2019 upto 02:00 PM Submission Date of Technical 26/07/2019 at 03:00 PM Bid Opening Indian Institute of Management, Lucknow NIT No. IIML/PUR/DTH/17/2019-20 DT.01/07/2019 TENDER FOR DIRECT TO HOME SD CONNECTIONS FOR ONE YEAR Indian institute of Management, Lucknow invites tender from reputed and interested firm/Organization/vendor for Providing Direct to Home SD Connections for IIM Lucknow Campus. For this firm/Organization/vendor should install a centralized installation box for providing Wi-Fi Direct to Home connection all through the campus. User may select channel or choose a package depend upon their interest and capacity to pay. (Package charge must be as per New Guidance of TRAI). Eligibility Criteria The bidder must submit: • All the vendors have to submit a letter of Authorization from OEM indicating that the bidder is authorized to bid for this specific tender. Any OEM directly participate the tender need not submit such letters. • Backend support commitment letter from the OEM specific to this tender by the vendor. OEM should submit a commitment letter along with the tender for providing full onsite support at Lucknow campus. • Submit an undertaking of adequate facilities and manpower (technical staff) to ensure the necessary support to IIM during the warranty period. -

ABSTRACT: in India Till 1991 There Was Only One Television Channel

ABSTRACT: In India till 1991 there was only one television channel –Doordarshan, the public service broadcaster. With the opening up of the Indian economy in early 1990s enabled the entry of private broadcasters in India. The number of television channels has proliferated manifold. By 2005 India had more than 200 digital channels. The number of television channels has grown from around 600 in 2010 to 800 in 2012.This includes more than 400 news and current affairs channel. Technological changes have caused intense competition in news and general entertainment channels, as a result of which there is growth in regional and niche channels. The growth of cable and satellite television and direct to home television services has continued to drive television as the most preferred medium among advertisers. Broadcasters are also tapping into online and mobile media to increase their revenue. This paper seeks to study the impact of privatisation on media policy of the Government of India and how it has evolved various institutional mechanisms to deal with the growth of television as the medium to study the effect of privatisation and convergence on media regulations as television is the most powerful medium. The visual images transmitted by television reach large section of the Indian population irrespective of linguistic and cultural differences. GROWTH OF THE TELEVISION INDUSTRY IN INDIA: Television began in India in 1959 as an educational project supported by the United Nations Educational Scientific and Cultural Organisation (UNESCO) and the Ford Foundation. Television was based on the model of a public broadcasting system prevalent in many countries of Europe. -

Download Package Activation Form (PAF)

GENRE DEN BASIC (109 CH.) Rs.160/- P.M. DEN PLATINUM-1 (260 CH.) Rs. 380/- P.M. DEN JUMBO PACK (287 CH.) Rs. 425/- P.M. HINDI GENERAL STAR UTSAV, ZEE ANMOL, HOME SHOP 18, DEN SD TV SHOP, DD NATIONAL, DD BHARATI, STAR PLUS, LIF OK, CHANNEL [V], SONY TV, SAB TV, SONY PAL, DISCOVERY ID, SAHARA ONE, ZEE TV, ZEE SMILE, STAR PLUS, LIF OK, CHANNEL [V], SONY TV, SAB TV, SONY PAL, DISCOVERY ID, SAHARA ONE, ZEE TV, ENTERTAINMENT DD INDIA, DD RAJASTHAN, DD UP, DD MP, DD BIHAR, COLORS, ZOOM, BIG MAGIC, BINDASS, EPIC TV, RISHTEY, ETV BIHAR, ETV MP, ETV RAJASTHAN, ETV UP ZEE SMILE, COLORS, ZOOM, BIG MAGIC, BINDASS, EPIC TV, RISHTEY, ETV BIHAR, ETV MP, DD KISAN, BEST DEAL TV. BINDASS PLAY, STAR UTSAV, ZEE ANMOL, ZINDAGI, HOME SHOP 18, DEN SD TV SHOP, DD NATIONAL, & TV, ETV RAJASTHAN, ETV UP, BINDASS PLAY, STAR UTSAV, ZEE ANMOL, ZINDAGI, HOME SHOP 18, SHOP CJ ALIVE, DD BHARATI, DD INDIA, DD RAJASTHAN, DD UP, DD MP, DD BIHAR, DD KISAN, BEST DEAL TV. DEN SD TV SHOP, FOOD FOOD, DD NATIONAL, & TV, SHOP CJ ALIVE, DD BHARATI, DD INDIA, DD RAJASTHAN, DD UP, DD MP, DD BIHAR, DD KISAN, BEST DEAL TV. HINDI MOVIES DEN CINEMA, DEN MOVIES, DEN GOLD, DEN SOUTH, DEN MAGIC, WOW CINEMA, MOVIES OK, STAR GOLD, SONY MAX, B4U MOVIES, ZEE CINEMA, & PICTURES, UTV MOVIES, MOVIES OK, STAR GOLD, SONY MAX, B4U MOVIES, ZEE CINEMA, & PICTURES, UTV MOVIES, DEN COMEDY, DEN CLASSIC. UTV ACTION, ZEE ACTION, ZEE CLASSIC, ZEE PREMIER, SONY MAX-2, MAGIC OF CINEMA, DEN CINEMA, UTV ACTION, ZEE ACTION, ZEE CLASSIC, ZEE PREMIER, SONY MAX-2, MAGIC OF CINEMA, DEN CINEMA, FILMI, DEN MOVIES, DEN GOLD, MULTIPLEX, DEN SOUTH, DEN MAGIC, DEN COMEDY, DEN CLASSIC, FILMI, DEN MOVIES, DEN GOLD, MULTIPLEX, DEN SOUTH, DEN MAGIC, DEN COMEDY, DEN CLASSIC, CINEMA TV, WOW CINEMA, DEN ACTION. -

DSN Vikhrolipaf November 2015.Cdr

GENRE DEN BASIC (109 CH.) Rs.160/- P.M. DEN PLATINUM-1 (260 CH.) Rs. 380/- P.M. DEN JUMBO PACK (287 CH.) Rs. 425/- P.M. HINDI GENERAL STAR UTSAV, ZEE ANMOL, HOME SHOP 18, DEN SD TV SHOP, DD NATIONAL, DD BHARATI, STAR PLUS, LIF OK, CHANNEL [V], SONY TV, SAB TV, SONY PAL, DISCOVERY ID, SAHARA ONE, ZEE TV, ZEE SMILE, STAR PLUS, LIF OK, CHANNEL [V], SONY TV, SAB TV, SONY PAL, DISCOVERY ID, SAHARA ONE, ZEE TV, ENTERTAINMENT DD INDIA, DD RAJASTHAN, DD UP, DD MP, DD BIHAR, COLORS, ZOOM, BIG MAGIC, BINDASS, EPIC TV, RISHTEY, ETV BIHAR, ETV MP, ETV RAJASTHAN, ETV UP ZEE SMILE, COLORS, ZOOM, BIG MAGIC, BINDASS, EPIC TV, RISHTEY, ETV BIHAR, ETV MP, DD KISAN, BEST DEAL TV. BINDASS PLAY, STAR UTSAV, ZEE ANMOL, ZINDAGI, HOME SHOP 18, DEN SD TV SHOP, DD NATIONAL, & TV, ETV RAJASTHAN, ETV UP, BINDASS PLAY, STAR UTSAV, ZEE ANMOL, ZINDAGI, HOME SHOP 18, SHOP CJ ALIVE, DD BHARATI, DD INDIA, DD RAJASTHAN, DD UP, DD MP, DD BIHAR, DD KISAN, BEST DEAL TV. DEN SD TV SHOP, FOOD FOOD, DD NATIONAL, & TV, SHOP CJ ALIVE, DD BHARATI, DD INDIA, DD RAJASTHAN, DD UP, DD MP, DD BIHAR, DD KISAN, BEST DEAL TV. HINDI MOVIES DEN CINEMA, DEN MOVIES, DEN GOLD, DEN SOUTH, DEN MAGIC, WOW CINEMA, MOVIES OK, STAR GOLD, SONY MAX, B4U MOVIES, ZEE CINEMA, & PICTURES, UTV MOVIES, MOVIES OK, STAR GOLD, SONY MAX, B4U MOVIES, ZEE CINEMA, & PICTURES, UTV MOVIES, DEN COMEDY, DEN CLASSIC. UTV ACTION, ZEE ACTION, ZEE CLASSIC, ZEE PREMIER, SONY MAX-2, MAGIC OF CINEMA, DEN CINEMA, UTV ACTION, ZEE ACTION, ZEE CLASSIC, ZEE PREMIER, SONY MAX-2, MAGIC OF CINEMA, DEN CINEMA, FILMI, DEN MOVIES, DEN GOLD, MULTIPLEX, DEN SOUTH, DEN MAGIC, DEN COMEDY, DEN CLASSIC, FILMI, DEN MOVIES, DEN GOLD, MULTIPLEX, DEN SOUTH, DEN MAGIC, DEN COMEDY, DEN CLASSIC, CINEMA TV, WOW CINEMA, DEN ACTION. -

Sun TV Network Limited: Rating Reaffirmed Summary of Rating Action

July 01, 2019 Sun TV Network Limited: Rating Reaffirmed Summary of rating action Previous Rated Amount Current Rated Amount Instrument* Rating Action (Rs. crore) (Rs. crore) Short term - Non-fund based 12.50 12.50 [ICRA]A1+; reaffirmed Total 12.50 12.50 *Instrument details are provided in Annexure-1 Rationale The rating reaffirmation draws comfort from STNL’s established presence; strong brand equity of ‘Sun TV’; and the company’s strong financial profile. The company witnessed strong revenue growth of 27.7% in FY2019 supported by healthy growth in subscription and advertisement revenues, and its margins remained strong at an OPM of 68.9% and NPM of 37.5%, aided by its scale, high bargaining power and nil debt position. The company has had zero debt every year, with sizeable cash and liquid investments of Rs. 2,686.5 crore as on March 31, 2019 (PY: Rs,1,896.9), facilitated by its strong accruals. By virtue of ‘Sun TV’ being one of the top viewership channels and having consistently high television rating points (TRP’s), the company has significant bargaining power over its content providers. This, in turn, has aided in control over telecasted content and facilitated advertisement revenue growth. As per the new TRAI order, every customer is entitled to a set free to air channels which may or may not include popular channels offered by major broadcasters. In addition, customers can choose channels/packs offered by the broadcasters based on their interest. However, Sun TV is part of the base pack in its viewership locations by virtue of user preference. -

Annexure I -Channel List of Odisha

Annexure I -Channel list of Odisha NO OF HD NO Of SD CHANNELS 226 CHANNELS 15 ENGLISH ENT HINDI MOVIES LIFE STYLE BENGALI HD CHANNELS STAR WORLD SET MAX FOX LIFE ABP ANANDA MAX HD AXN STAR GOLD NDTV GOODTIMES ATN BANGLA MN+HD FX UTV MOVIES FTV DD BANGLA SONY PIX HD ENGLISH MOVIES MAX2 FOOD FOOD TV SONY AATH HBO HD MOVIES NOW 2 STAR MOVIES UTV ACTION TLC KOLKATA TV HD SONY PIX MOVIES OK CARE WORLD SANGEET BANGLA SONY LEPLEX HD MOVIES NOW WOW CINEMA KIDS STAR JHALSA SONY ESPN HD CARTOON MOVIES NOW2 VAA MOVIES NETWORK AKASH AATH SONY SIX HD ROMEDY NOW CINEMA TV DISNEY JHALSA MOVIES BBC EARTH STAR UTSAV STAR MOVIES ACTION MOVIES HUNGAMA ZEE 24 GHANTA ROX HD HINDI ENT B4U MOVIES POGO MUSIC F SONY HD STAR PLUS GREEN NAAPTOL DISNEY JUNIOR RUPASI BANGLA SAB TV HD SONY BFLIX MOVIES DISNEY XD DHOOM MUSIC TRAVEL XP HD STAR SPORTS HD SAB TV MOVIE HOUSE SONY YAY R PLUS GOLD 1 STAR SPORTS HD LIFE OK SONY WAH DISCOVERY KIDS NEWS TIME 3 ZEE ANMOL BINDASS CINEMA MU BU TV ZEE BANGLA SONY PAL SAHARA FILMY NICK TELUGU SHOP CJ MUSIC BABY TV ABN HOME SHOP 18 SONY MIX KNOWLEDGE GEMINI BLUE NAAPTOL CHANEL V NAT GEO GEMINI MOVIES ZOOM B4U MUSIC DISCOVERY ZEE TELUGU STAR UTSAV BINDAS PLAY SONY BBC EARTH MAA ZEE ANMOL 9X M ANIMAL PLANET MAA GOLD DISCOVERY ID MUSIC INDIA NGC WILD MAA MOVIES EPIC 9X JALWA DISCOVERY TURBO NTV DD NATIONAL NGC MUSIC DISCOVERU SCIENCE GEMINI COMEDY ZEE TV 9XO NGC PEOPLE GEMINI MUSIC DD INDIA 9X TASHAN GYAN DARSHAN GEMINI LIFE COLORS SPORTS DD KISHAN KHUSI TV DD BHARATI STAR SPORS1 HINDI NEWS GEMINI NEWS & TV STAR SPORS2 AAJ TAK TV9 SAHARA -

STOXX BRIC 100 Last Updated: 01.08.2017

STOXX BRIC 100 Last Updated: 01.08.2017 Rank Rank (PREVIOU ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) S) CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 60.5 1 1 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 50.8 2 2 INE040A01026 B5Q3JZ5 HDBK.BO IN00CH HDFC Bank Ltd IN INR Y 47.7 3 3 INE002A01018 6099626 RELI.BO IN0027 Reliance Industries Ltd IN INR Y 44.4 4 6 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 41.3 5 4 INE001A01036 6171900 HDFC.BO IN00EJ Housing Development Finance Co IN INR Y 37.5 6 7 INE154A01025 B0JGGP5 ITC.BO IN007C ITC Ltd IN INR Y 34.6 7 5 BRITUBACNPR1 B037HR3 ITUB4.SA BR0035 ITAU UNIBANCO HOLDING SA -PREF BR BRL Y 32.7 8 9 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 32.0 9 10 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 31.8 10 8 INE009A01021 6205122 INFY.BO IN006B Infosys Ltd IN INR Y 30.6 11 11 INE090A01021 BSZ2BY7 ICBK.BO IN00BG ICICI Bank Ltd IN INR Y 25.6 12 12 BRBBDCACNPR8 B00FM53 BBDC4.SA BR0079 BANCO BRADESCO SA - PREF BR BRL Y 25.0 13 13 RU0009029540 4767981 SBER.MM EV023 SBERBANK RU RUB Y 23.9 14 14 BRABEVACNOR1 BG7ZWY7 ABEV3.SA BR01UX AMBEV BR BRL Y 23.0 15 15 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 20.0 16 16 INE018A01030 B0166K8 LART.BO IN00AF Larsen & Toubro Ltd IN INR Y 19.3 17 17 INE467B01029 B01NPJ1 TCS.BO IN005A Tata Consultancy Services Ltd IN INR Y 17.3 18 20 INE237A01028 6135661 KTKM.BO IN06Q1 Kotak Mah Bk IN INR Y 16.9 19 22 INE238A01034 BPFJHC7 AXBK.BO IN00MR AXIS BANK IN INR Y 16.4 20 21 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 16.4 21 18 RU0007661625 B59L4L7 GAZP.MM EV019 GAZPROM RU RUB Y 16.2 22 19 BRVALEACNPA3 2257127 VALE5.SA BR10JM VALE S.A. -

Den Family Sr. No. Channel Name EPG No. 1 STAR PLUS 101 2 LIFE OK 102 3 Colors 103 4 Zee TV 104 5 SONY 105 6 &Tv 106 7 Risht

Den Family Sr. No. Channel Name EPG No. 1 STAR PLUS 101 2 LIFE OK 102 3 Colors 103 4 Zee TV 104 5 SONY 105 6 &tv 106 7 Rishtey 107 8 Sony SAB 108 9 ZINDGI 109 10 ZEE ANMOL 110 11 SONY PAL 111 12 BIG MAGIC 112 13 BINDASS 113 14 Bindass Play 114 15 STAR UTSAV 115 16 ID 119 17 CHANNEL V 121 18 Dangal 123 19 Living Foodz 124 20 Etv bihar 126 21 Den snapdeal tv-shop 132 22 Shop CJ 133 23 HOME SHOP 18 134 24 Naaptol 135 25 DD UP 137 26 DD NATIONAL 138 27 DD rajasthan 139 28 DD MP 140 29 DD BIHAR 142 30 Sri Anandpur Sahib 143 31 Sri Dukhnivaran Sahi 144 32 Sri Shaheedan Sahib 145 33 Sri Singh Sabha Sahi 146 34 Sri Durgiana Mata Ma 147 35 Sri Kali Mata Mandir 148 36 Amrit Gurbani 149 37 Ek Onkar 150 38 Den cinema 152 39 Star Gold 161 40 Movies ok 162 41 SONY MAX 163 42 ZEE CINEMA 164 43 UTV MOVIES 165 44 B4U MOVIES 166 45 Sont MAX 2 167 46 ZEE CALSSIC 168 47 & PICTURE 169 48 ZEE ACTION 170 49 Naaptol Green 171 50 UTV ACTION 172 51 Rishtey Cineplex 173 52 Housefull movies 174 53 CINEMA TV 175 54 Housefull Action 179 55 Movie House 180 56 Star Utsav movie 181 57 Sony Wah 182 58 Enter 10 Movies 183 59 Den Movies 191 60 STAR WORLD 201 61 FX 202 62 COMEDY CENTRAL 204 63 ZEE CAFÉ 205 64 AXN 207 65 Colors Infinity 210 66 STAR MOVIES 231 67 HBO 232 68 STAR MOVIES ACTION 233 69 SONY PIX 234 70 ZEE STUDIO 235 71 FOX Life 256 72 TLC 257 73 DISCOVERY TURBO 258 74 NDTV Good times 259 75 Living Zen 265 76 FTV 269 77 CARE WORLD 277 78 Den snapdeal tv-shop 2 299 79 INDIA TV 301 80 ABP NEWS 302 81 ZEE NEWS 303 82 NEWS 24 304 83 AAJTAK 305 84 NEWS NATION 306 85 -

In India Till 1991 There Was Only One Television Channel –Doordarshan, the Public Service Broadcaster

The Asian Conference on Media and Mass Communication 2013 Official Conference Proceedings Osaka, Japan Privatisation,convergence and Broadcasting regulations:A case study of the Indian Television Industry, Padma Rani School of communication;Manipal University, India 0139 The Asian Conference on Media and Mass Communication 2013 Official Conference Proceedings 2013 Abstract In India till 1991 there was only one television channel –Doordarshan, the public service broadcaster. With the opening up of the Indian economy in early 1990s enabled the entry of private broadcasters in India. The number of television channels has proliferated manifold. By 2005 India had more than 200 digital channels. The number of television channels has grown from around 600 in 2010 to 800 in 2012.This includes more than 400 news and current affairs channel. Technological changes have caused intense competition in news and general entertainment channels, as a result of which there is growth in regional and niche channels. The growth of cable and satellite television and direct to home television services has continued to drive television as the most preferred medium among advertisers. Broadcasters are also tapping into online and mobile media to increase their revenue. This paper seeks to study the impact of privatisation on media policy of the Government of India and how it has evolved various institutional mechanisms to deal with the growth of television as the medium to study the effect of privatisation and convergence on media regulations as television is the most powerful medium. The visual images transmitted by television reach large section of the Indian population irrespective of linguistic and cultural differences. -

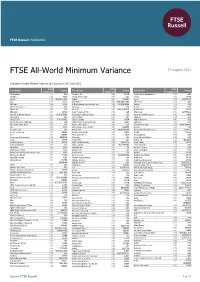

FTSE All-World Minimum Variance

2 FTSE Russell Publications 19 August 2021 FTSE All-World Minimum Variance Indicative Index Weight Data as at Closing on 30 June 2021 Index Index Index Constituent Country Constituent Country Constituent Country weight (%) weight (%) weight (%) 3M Company 0.1 USA Ajinomoto Co 0.05 JAPAN Annaly Capital Management 0.07 USA 3M India 0.02 INDIA Akamai Technologies 0.14 USA Anritsu 0.03 JAPAN a2 Milk 0.03 NEW ZEALAND Akbank 0.01 TURKEY Ansell 0.02 AUSTRALIA A2A 0.01 ITALY Akzo Nobel 0.02 NETHERLANDS ANSYS Inc 0.08 USA ABB India 0.04 INDIA Al Rajhi Banking & Investment Corp 0.04 SAUDI ARABIA Anthem 0.08 USA Abbott Laboratories 0.09 USA Albemarle 0.06 USA Aon plc 0.09 USA AbbVie Inc 0.11 USA Alcon AG 0.02 SWITZERLAND Aozora Bank 0.03 JAPAN ABC-Mart 0.03 JAPAN Aldar Properties PJSC 0.02 UAE APA Group 0.02 AUSTRALIA Abdullah Al Othaim Markets 0.04 SAUDI ARABIA Alexandria Real Estate Equity 0.09 USA Apollo Hospitals Enterprise 0.04 INDIA Abiomed Inc 0.11 USA Alexion Pharm 0.12 USA Apple Inc. 0.09 USA Aboitiz Power 0.02 PHILIPPINES Alfresa Holdings 0.02 JAPAN Applied Materials 0.06 USA Abu Dhabi Commercial Bank 0.02 UAE Alibaba Pictures Group (P Chip) 0.02 CHINA Aptiv PLC 0.04 USA Abu Dhabi Islamic Bank 0.03 UAE Align Technology Inc 0.05 USA Arab National Bank 0.03 SAUDI ARABIA ACC 0.04 INDIA Alimentation Couche-Tard B 0.02 CANADA Aramark 0.04 USA Accenture Cl A 0.09 USA Alinma Bank 0.04 SAUDI ARABIA Arca Continental SAB de CV 0.03 MEXICO Accton Technology 0.03 TAIWAN A-Living Services (H) 0.02 CHINA Arcelik 0.01 TURKEY Acer 0.04 TAIWAN Alkem Laboratories