Sun TV Network Limited: Rating Reaffirmed Summary of Rating Action

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Genre Channel Name Channel No Hindi Entertainment Star Bharat 114 Hindi Entertainment Investigation Discovery HD 136 Hindi Enter

Genre Channel Name Channel No Hindi Entertainment Star Bharat 114 Hindi Entertainment Investigation Discovery HD 136 Hindi Entertainment Big Magic 124 Hindi Entertainment Colors Rishtey 129 Hindi Entertainment STAR UTSAV 131 Hindi Entertainment Sony Pal 132 Hindi Entertainment Epic 138 Hindi Entertainment Zee Anmol 140 Hindi Entertainment DD National 148 Hindi Entertainment DD INDIA 150 Hindi Entertainment DD BHARATI 151 Infotainment DD KISAN 152 Hindi Movies Star Gold HD 206 Hindi Movies Zee Action 216 Hindi Movies Colors Cineplex 219 Hindi Movies Sony Wah 224 Hindi Movies STAR UTSAV MOVIES 225 Hindi Zee Anmol Cinema 228 Sports Star Sports 1 Hindi HD 282 Sports DD SPORTS 298 Hindi News ZEE NEWS 311 Hindi News AAJ TAK HD 314 Hindi News AAJ TAK 313 Hindi News NDTV India 317 Hindi News News18 India 318 Hindi News Zee Hindustan 319 Hindi News Tez 326 Hindi News ZEE BUSINESS 331 Hindi News News18 Rajasthan 335 Hindi News Zee Rajasthan News 336 Hindi News News18 UP UK 337 Hindi News News18 MP Chhattisgarh 341 Hindi News Zee MPCG 343 Hindi News Zee UP UK 351 Hindi News DD UP 400 Hindi News DD NEWS 401 Hindi News DD LOK SABHA 402 Hindi News DD RAJYA SABHA 403 Hindi News DD RAJASTHAN 404 Hindi News DD MP 405 Infotainment Gyan Darshan 442 Kids CARTOON NETWORK 449 Kids Pogo 451 Music MTV Beats 482 Music ETC 487 Music SONY MIX 491 Music Zing 501 Marathi DD SAHYADRI 548 Punjabi ZEE PUNJABI 562 Hindi News News18 Punjab Haryana Himachal 566 Punjabi DD PUNJABI 572 Gujrati DD Girnar 589 Oriya DD ORIYA 617 Urdu Zee Salaam 622 Urdu News18 Urdu 625 Urdu -

MSO Name:- STAR CLUB

MSO Name:- STAR CLUB Sl No Name Broadcaster Genre Language 1 TRAI INFO @STAR CLUB FTA OTHERS BENGALI 2 SAHARA MP FTA REGIONAL Hindi 3 SAHARA UP FTA REGIONAL Hindi 4 SAHARA MUMBAI FTA REGIONAL Hindi 5 SKYSTAR TELEGU FTA REGIONAL Telugu 6 DD RANCHI FTA REGIONAL Hindi 7 DD RAJASTHAN FTA REGIONAL Hindi 8 DD NORTH EAST FTA REGIONAL Hindi 9 DD RAIPUR FTA REGIONAL Hindi 10 DD MP FTA REGIONAL Hindi 11 DD UP FTA REGIONAL Hindi 12 DD DEHRADUN FTA REGIONAL Hindi 13 DD KOHIMA FTA REGIONAL Hindi 14 DD AIZWAL FTA REGIONAL Hindi 15 DD IMPHAL FTA REGIONAL Hindi 16 DD ARUNPRABHA FTA REGIONAL Hindi 17 DD KASHIR FTA REGIONAL Hindi 18 DD GIRNAR FTA REGIONAL Telugu 19 DD CHANDANA FTA REGIONAL Telugu 20 PRATIDIN TIME FTA REGIONAL BENGALI 21 TAZA TV FTA REGIONAL Hindi 22 HARIYANA NEWS FTA REGIONAL Hindi 23 AAHO MUSIC FTA REGIONAL PUNJABI 24 SANDAR CINEMA FTA REGIONAL BHOHPURI 25 ANJAN TV FTA REGIONAL BHOHPURI 26 BHAKTI SAGAR 2 FTA BHAKTI Hindi 27 SUBHA CINEMA FTA BHAKTI Hindi 28 SUBHA TV FTA BHAKTI Hindi 29 SURIYA BHAKTI FTA BHAKTI Hindi 30 SADHANA BHAKTI FTA BHAKTI Hindi 31 VAIDEK FTA BHAKTI Hindi 32 HARE KRISHNA FTA BHAKTI Hindi 33 FOOD FOOD FTA LIFE STYLE Hindi 34 SAHARA NCR FTA HINDI NEWS Hindi 35 SHOW BOX FTA HINDI MUSIC Hindi 36 M TUNE SD FTA HINDI MUSIC Hindi 37 ZINGAAT FTA HINDI MOVIES Hindi 38 MANORANJAN GRAND FTA HINDI MOVIES Hindi 39 MULTIPLEX FTA HINDI MOVIES Hindi 40 HOUSEFULL ACTION FTA HINDI MOVIES Hindi 41 MOVIE PLUS FTA HINDI MOVIES Hindi 42 BFLIX MOVIES FTA HINDI MOVIES Hindi 43 WOW CINEMA FTA HINDI MOVIES Hindi 44 DD INDIA FTA HINDI ENTERTAINMENT -

ABSTRACT: in India Till 1991 There Was Only One Television Channel

ABSTRACT: In India till 1991 there was only one television channel –Doordarshan, the public service broadcaster. With the opening up of the Indian economy in early 1990s enabled the entry of private broadcasters in India. The number of television channels has proliferated manifold. By 2005 India had more than 200 digital channels. The number of television channels has grown from around 600 in 2010 to 800 in 2012.This includes more than 400 news and current affairs channel. Technological changes have caused intense competition in news and general entertainment channels, as a result of which there is growth in regional and niche channels. The growth of cable and satellite television and direct to home television services has continued to drive television as the most preferred medium among advertisers. Broadcasters are also tapping into online and mobile media to increase their revenue. This paper seeks to study the impact of privatisation on media policy of the Government of India and how it has evolved various institutional mechanisms to deal with the growth of television as the medium to study the effect of privatisation and convergence on media regulations as television is the most powerful medium. The visual images transmitted by television reach large section of the Indian population irrespective of linguistic and cultural differences. GROWTH OF THE TELEVISION INDUSTRY IN INDIA: Television began in India in 1959 as an educational project supported by the United Nations Educational Scientific and Cultural Organisation (UNESCO) and the Ford Foundation. Television was based on the model of a public broadcasting system prevalent in many countries of Europe. -

Media Buzz Large Regional TV Opportunity; Competitive Intensity on the Rise

Asia Pacific | India Media - General (Citi) Industry Focus 5 December 2008 23 pages Media Buzz Large Regional TV Opportunity; Competitive Intensity on the Rise High growth regional entertainment market — The size of the six major regional markets is estimated to be ~Rs 21b, thus contributing about a fourth of the overall Surendra Goyal, CFA1 TV ad revenues in India. Sun TV Network and Zee News are the larger listed players that benefit from the regional entertainment market opportunity. 'Viewership - Revenue' mismatch — The share of advertising revenue for the Aditya Mathur1 regional language channels (~25%) is far less when compared to the viewership share (~37%). Regional advertising is growing at a pace faster than the national Jason Brueschke2 growth. Of the ad revenue pie, ~60% comes from regional ads. Large players enter the regional genre — The market is expanding as the number of corporates with deep pockets enter. Zee News has entered the Tamil, Telugu & Kannada markets while Star has entered the Marathi & Bengali segments and has aggressive plans for South India through its JV with Jupiter Entertainment. Increasing competition results in pressure on content/talent and other costs. Zee News management meeting takeaways — (a) ZEEN expects to grow at least 5% more than overall industry; (b) Zee Telugu broke even in 2QFY09 and mgmt expects Zee Kannada to breakeven by mid CY09; (c) Zee Bangla & Zee Marathi contribute to about half of ZEEN's revenues; (d) In Tamil Nadu, ZEEN targets the No 2 position, after Sun TV, within the next 12-18 months. Noteworthy this month: (1) GEC ratings decline as no fresh content aired...— For ~20 days, Hindi GECs were not airing fresh content, which led to a steep drop in ratings. -

STOXX BRIC 100 Last Updated: 01.08.2017

STOXX BRIC 100 Last Updated: 01.08.2017 Rank Rank (PREVIOU ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) S) CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 60.5 1 1 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 50.8 2 2 INE040A01026 B5Q3JZ5 HDBK.BO IN00CH HDFC Bank Ltd IN INR Y 47.7 3 3 INE002A01018 6099626 RELI.BO IN0027 Reliance Industries Ltd IN INR Y 44.4 4 6 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 41.3 5 4 INE001A01036 6171900 HDFC.BO IN00EJ Housing Development Finance Co IN INR Y 37.5 6 7 INE154A01025 B0JGGP5 ITC.BO IN007C ITC Ltd IN INR Y 34.6 7 5 BRITUBACNPR1 B037HR3 ITUB4.SA BR0035 ITAU UNIBANCO HOLDING SA -PREF BR BRL Y 32.7 8 9 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 32.0 9 10 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 31.8 10 8 INE009A01021 6205122 INFY.BO IN006B Infosys Ltd IN INR Y 30.6 11 11 INE090A01021 BSZ2BY7 ICBK.BO IN00BG ICICI Bank Ltd IN INR Y 25.6 12 12 BRBBDCACNPR8 B00FM53 BBDC4.SA BR0079 BANCO BRADESCO SA - PREF BR BRL Y 25.0 13 13 RU0009029540 4767981 SBER.MM EV023 SBERBANK RU RUB Y 23.9 14 14 BRABEVACNOR1 BG7ZWY7 ABEV3.SA BR01UX AMBEV BR BRL Y 23.0 15 15 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 20.0 16 16 INE018A01030 B0166K8 LART.BO IN00AF Larsen & Toubro Ltd IN INR Y 19.3 17 17 INE467B01029 B01NPJ1 TCS.BO IN005A Tata Consultancy Services Ltd IN INR Y 17.3 18 20 INE237A01028 6135661 KTKM.BO IN06Q1 Kotak Mah Bk IN INR Y 16.9 19 22 INE238A01034 BPFJHC7 AXBK.BO IN00MR AXIS BANK IN INR Y 16.4 20 21 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 16.4 21 18 RU0007661625 B59L4L7 GAZP.MM EV019 GAZPROM RU RUB Y 16.2 22 19 BRVALEACNPA3 2257127 VALE5.SA BR10JM VALE S.A. -

Hathway Fta Pack

HATHWAY FTA PACK DELHI DELHI FTA Total Channels 142 SD + 0 HD LANG - GENRE CHANNEL_NAME SD/HD Assamese - Gec DD ArunPrabha SD Assamese - Gec DD ASSAM SD Assamese - News PRAG NEWS SD Bengali - Gec AAKASH AATH SD Bengali - Gec DD BANGLA SD Bengali - Gec RUPASI BANGLA SD Bengali - Movie ENTERR10 MOVIES SD Bengali - Music SANGEET BANGLA SD Bengali - News ABP ANANDA SD Bhojpuri - Gec DANGAL SD Bhojpuri - Movie BHOJPURI CINEMA SD Bhojpuri - Movie PITAARA SD Bhojpuri - Movie SURYA BHOJPURI SD Bhojpuri - Music SANGEET BHOJPURI SD English - Devotional PEACE OF MIND SD English - Lifestyle FASHION TV SD English - News REPUBLIC TV SD Gujarati - Gec DD GIRNAR SD Haryanvi - Gec RAGNI SPECIAL SD Haryanvi - Music APNA HARYANA SD Hindi - Devotional AASTHA SD Hindi - Devotional AASTHA BHAJAN SD Hindi - Devotional ARIHANT SD Hindi - Devotional DIVINE SD Hindi - Devotional HARE KRSNA TV SD Hindi - Devotional HINDU DHARMAM SD Hindi - Devotional LORD BUDDHA TV SD Hindi - Devotional PARAS SD Hindi - Devotional SANSKAR SD Hindi - Devotional SATSANG SD Hindi - Devotional SHRADDHA MH ONE SD Hindi - Devotional SHUBHSANDESH SD Hindi - GEC A1TV SD Page 1 of 47 Hindi - Gec ABZY COOL SD Hindi - Gec CCC SD Hindi - Gec DD BIHAR SD Hindi - Gec DD MADHYA PRADESH SD Hindi - Gec DD NATIONAL SD Hindi - Gec DD RAJASTHAN SD Hindi - Gec DD UTTAR PRADESH SD Hindi - GEC DISHUM SD Hindi - Gec ENTERR10 SD Hindi - Gec HATHWAY HARYANVI SD Hindi - GEC KISHORE MANCH SD Hindi - GEC PANINI SD Hindi - GEC SHARDA SD Hindi - GEC SHEMAROO TV SD Hindi - Infotainment DD BHARATI SD Hindi - Infotainment -

Declaration Under Section 4 (4) of the Telecommunication (Broadcasting and Cable) Services Interconnection (Addressable System) Regulation, 2017 (No

Version 3/202104 Declaration Under Section 4 (4) of The Telecommunication (Broadcasting and Cable) Services Interconnection (Addressable System) Regulation, 2017 (No. 1 of 2017) 4(4)a: Target Market States/Parts of State covered as "Coverage Area" 1. Andhra Pradesh 2. Assam 3. Delhi 4. Haryana 5. Karnataka 6. Madhya Pradesh 7. Maharashtra 8. Odisha 9. Rajasthan 10. Sikkim 11. Telangana 12. Tripura 13. Uttar Pradesh 14. Uttarakhand 15. West Bengal 4(4)b: Total Channel carrying capacity Distribution Network Location Capacity in SD Terms Bangalore 506 Bhopal 358 Delhi 384 Hyderabad 456 Kolkata 472 Mumbai 447 Kindly Note: 1. Local Channels considered as 1 SD; 2. Consideration in SD Terms is clarified as 1 SD = 1 SD; 1 HD = 2 SD; 3. Number of channels will vary within the area serviced by a distribution network location depending upon available Bandwidth capacity. Page 1 of 39 Version 3/202104 4(4)c: List of channels available on network List attached below in Annexure I 4(4)d: Number of channels which signals of television channels have been requested by the distributor from broadcasters and the interconnection agreements signed Nil 4(4)e: Spare channels capacity available on the network for the purpose of carrying signals of television channels Distribution Network Location Spare Channel Capacity in SD Terms Bangalore Nil Bhopal Nil Delhi Nil Hyderabad Nil Kolkata Nil Mumbai Nil 4(4)f: List of channels, in chronological order, for which requests have been received from broadcasters for distribution of their channels, the interconnection -

LCN Home Channel 1 SD 100 Star Plus SD 101 ZEE TV SD 103 &Tv SD 104 Colors SD 105 DANGAL SD 106 Star Bharat SD 107 SET SD 109 Dr

Channel Name SD/HD LCN Home Channel 1 SD 100 Star Plus SD 101 ZEE TV SD 103 &tv SD 104 colors SD 105 DANGAL SD 106 Star Bharat SD 107 SET SD 109 Dr. Shuddhi SD 110 ID SD 111 Big Magic SD 112 SONY SAB SD 113 ABZY Cool SD 114 ZEE ANMOL SD 116 d2h Positive SD 117 EZ MALL SD 118 bindass SD 120 colors rishtey SD 121 Shemaroo TV SD 123 Anjan SD 128 Ayushman Active SD 130 Comedy Active SD 131 Fitness Active SD 132 Thriller Active SD 134 Shorts TV Active SD 135 Korean Drama Active SD 136 Watcho SD 144 Cooking Active SD 146 Zee Zest SD 147 DD NATIONAL SD 149 DD Retro SD 151 STAR UTSAV SD 156 SONY PAL SD 159 TOPPER SD 160 STAR WORLD SD 179 ZEE cafe SD 181 Colors Infinity SD 183 COMEDY CENTRAL SD 185 ZEEPLEX Screen 1 SD 200 SONY MAX SD 201 &pictures SD 202 ZEE CINEMA SD 203 Jyotish Duniya SD 204 Star GOLD SD 205 ABZY MOVIES SD 206 UTV MOVIES SD 207 B4U Kadak SD 210 UTV ACTION SD 211 Box Cinema SD 212 Cine Active SD 213 Rangmanch Active SD 214 Evergreen Classics Active SD 215 Hits Active SD 217 ZEE Bollywood SD 218 EZ MALL SD 219 colors cineplex SD 221 Movies Active SD 222 Housefull Movies SD 223 enterr 10 Movies SD 225 ABZY Dhadkan SD 226 Star Gold 2 SD 227 ZEE Action SD 228 B4U MOVIES SD 229 Star Gold Select SD 231 Star Utsav Movies SD 234 EZ MALL SD 235 Zee Anmol Cinema SD 237 Dr. -

List of Channel Available in 'D2h' Platform

List of Channel available in 'd2h' platform &flix RENGONI Disha TV 9X JALWA SAAM GOODNESS TV AAJ TAK DD Retro hm tv ABP ASMITA SAFARI TV ISAI ARUVI ABP NEWS SAI TV Janam TV BBC WORLD NEWS SAKSHI TV KAPPA TV CNBC AWAAZ Sandesh News Kasthuri TV CNBC TV 18 Sathiyam tv Kaumudy CNN International SUBHAVAARTHA TV LOK SABHA CNN NEWS 18 SUDARSHAN NEWS madha colors SUPER SVBC 2 MAKKAL TV COMEDY CENTRAL T NEWS Malai Murasu Seithikal DD NEWS PTC Punjabi Gold manorama NEWS ET NOW India News Haryana MATHRUBHUMI NEWS HBO THANTHI TV MAZHAVIL MANORAMA INDIA TODAY TV 5 NEWS MURASU INDIA TV TV5 Kannada Nambikkkai Mirror Now Twenty Four News18 Kerala MNX V6 NEWS NEWS NATION MOVIES NOW Velicham TV NEWS18 TAMIL NADU NDTV 24x7 WE Paras Gold NDTV INDIA 24 GHANTA Peace of Mind NEWS18 India ADITHYA TV Polimer REPUBLIC TV Asianet Polimer NEWS Romedy NOW ASIANET MOVIES PUTHIYA THALAIMURAI SONY PIX ASIANET PLUS raj MUSIX MALAYALAM STAR MOVIES CHUTTI TV RAJ MUSIX TELUGU STAR WORLD colors Kannada RAJ NEWS KANNADA TIMES NOW colors Oriya Raj NEWS MALAYALAM WB DD KASHIR Raj News Telugu WION DHOOM Music RUPASI BANGLA ZEE BIHAR JHARKHAND ETV PLUS Russia Today ZEE BUSINESS ETV Telugu SANSKAR ZEE cafe ez mall DD Gyandarshan Zee Hindustan GEMINI COMEDY Satsang ZEE MP CHATTISGARH GEMINI MOVIES SEITHIGAL ZEE NEWS GEMINI Music SHALOM TV ZEE Rajasthan NEWS Gemini TV Suvarna News 24x7 ZEE SARTHAK JAYA TV TV9 GUJARATI 7S Music KALAIGNAR TV9 KANNADA DY 365 Kochu TV TV9 MARATHI NEWS 18 Gujarati KTV VASANTH TV Harvest TV MEGA TV Vendhar Tv News 18 Uttar Pradesh Uttranchal NEWS 18 Kannada -

In India Till 1991 There Was Only One Television Channel –Doordarshan, the Public Service Broadcaster

The Asian Conference on Media and Mass Communication 2013 Official Conference Proceedings Osaka, Japan Privatisation,convergence and Broadcasting regulations:A case study of the Indian Television Industry, Padma Rani School of communication;Manipal University, India 0139 The Asian Conference on Media and Mass Communication 2013 Official Conference Proceedings 2013 Abstract In India till 1991 there was only one television channel –Doordarshan, the public service broadcaster. With the opening up of the Indian economy in early 1990s enabled the entry of private broadcasters in India. The number of television channels has proliferated manifold. By 2005 India had more than 200 digital channels. The number of television channels has grown from around 600 in 2010 to 800 in 2012.This includes more than 400 news and current affairs channel. Technological changes have caused intense competition in news and general entertainment channels, as a result of which there is growth in regional and niche channels. The growth of cable and satellite television and direct to home television services has continued to drive television as the most preferred medium among advertisers. Broadcasters are also tapping into online and mobile media to increase their revenue. This paper seeks to study the impact of privatisation on media policy of the Government of India and how it has evolved various institutional mechanisms to deal with the growth of television as the medium to study the effect of privatisation and convergence on media regulations as television is the most powerful medium. The visual images transmitted by television reach large section of the Indian population irrespective of linguistic and cultural differences. -

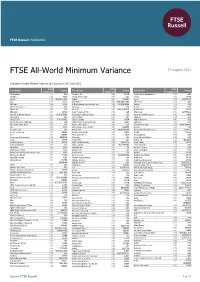

FTSE All-World Minimum Variance

2 FTSE Russell Publications 19 August 2021 FTSE All-World Minimum Variance Indicative Index Weight Data as at Closing on 30 June 2021 Index Index Index Constituent Country Constituent Country Constituent Country weight (%) weight (%) weight (%) 3M Company 0.1 USA Ajinomoto Co 0.05 JAPAN Annaly Capital Management 0.07 USA 3M India 0.02 INDIA Akamai Technologies 0.14 USA Anritsu 0.03 JAPAN a2 Milk 0.03 NEW ZEALAND Akbank 0.01 TURKEY Ansell 0.02 AUSTRALIA A2A 0.01 ITALY Akzo Nobel 0.02 NETHERLANDS ANSYS Inc 0.08 USA ABB India 0.04 INDIA Al Rajhi Banking & Investment Corp 0.04 SAUDI ARABIA Anthem 0.08 USA Abbott Laboratories 0.09 USA Albemarle 0.06 USA Aon plc 0.09 USA AbbVie Inc 0.11 USA Alcon AG 0.02 SWITZERLAND Aozora Bank 0.03 JAPAN ABC-Mart 0.03 JAPAN Aldar Properties PJSC 0.02 UAE APA Group 0.02 AUSTRALIA Abdullah Al Othaim Markets 0.04 SAUDI ARABIA Alexandria Real Estate Equity 0.09 USA Apollo Hospitals Enterprise 0.04 INDIA Abiomed Inc 0.11 USA Alexion Pharm 0.12 USA Apple Inc. 0.09 USA Aboitiz Power 0.02 PHILIPPINES Alfresa Holdings 0.02 JAPAN Applied Materials 0.06 USA Abu Dhabi Commercial Bank 0.02 UAE Alibaba Pictures Group (P Chip) 0.02 CHINA Aptiv PLC 0.04 USA Abu Dhabi Islamic Bank 0.03 UAE Align Technology Inc 0.05 USA Arab National Bank 0.03 SAUDI ARABIA ACC 0.04 INDIA Alimentation Couche-Tard B 0.02 CANADA Aramark 0.04 USA Accenture Cl A 0.09 USA Alinma Bank 0.04 SAUDI ARABIA Arca Continental SAB de CV 0.03 MEXICO Accton Technology 0.03 TAIWAN A-Living Services (H) 0.02 CHINA Arcelik 0.01 TURKEY Acer 0.04 TAIWAN Alkem Laboratories -

SL Number LCN Number Channels Name 1 3 SUN BANGLA (FREE) 2

SL LCN Channels Name Number Number 1 3 SUN BANGLA (FREE) 2 6 SAPTAK DIGITAL(FREE) 3 7 CN NEWS (FREE) 4 8 CTVN (FREE) 5 9 SAPTAK PLUS(FREE) 6 10 SAPTAK LIFE (FREE) 7 11 ABP ANANDA (FREE) 8 12 SAPTAK NEWS (FREE) 9 13 SAPTAK CLASSIC (FREE) 10 15 SADHNA NEWS (FREE) 11 16 DD BANGLA (FREE) 12 17 EN TV BANGLA (FREE) 13 18 BHOOMI (FREE) 14 20 BANGLA BHARAT (FREE) 15 26 SRISTI PLUS(FREE) 16 28 UTTAR BANGLA(FREE) 17 29 KOLKATA TV (FREE) 18 30 AB BARTA(FREE) 19 33 ONKAR ONLY TRUTH (FREE) 20 34 AAKASH AATH (FREE) 21 38 SRISTI TV (FREE) 22 39 RONGEEN TV (FREE) 23 41 ENTER 10 BANGLA (FREE) 24 42 SS BANGLA (FREE) 25 43 RUPOSHI BANGLA (FREE) 26 44 SONAR BANGLA(FREE) 27 45 R PLUS (FREE) 28 48 CHANNEL VISION(FREE) 29 49 BANGLA TIME (FREE) 30 50 BHAKTI TV(FREE) 31 55 SAPTAK BANGLA MUSIC (FREE) 32 56 AMAR BANGLA (FREE) 33 59 KHUSBOO BANGLA (FREE) 34 63 TUNES 6 (FREE) 35 64 TOLLYWOOD (FREE) 36 65 MUSIC ZONE (FREE) 37 66 PTC MUSIC (FREE) 38 68 FRESH TUNES (FREE) 39 69 MUSIC F (FREE) 40 70 MUSIC BANGLA(FREE) 41 71 ORANGE TV (FREE) 42 72 SANGEET BANGLA (FREE) 43 73 MAHUAA+ (FREE) 44 74 SHOW BOX (FREE) 45 75 KOLKATA LIVE (FREE) 46 76 MUSIC INDIA (FREE) 47 77 9X JHAKAAS (FREE) 48 78 WOW MUSIC (FREE) 49 79 P PLUS (FREE) 50 80 BALLE BALLE (FREE) 51 81 P TUNES (FREE) 52 82 KALAIGNAR ISAI ARUVI (FREE) 53 85 PITAARA (FREE) 54 87 MTUNES+ (FREE) 55 88 MASTII (FREE) 56 89 MH1 MUSIC (FREE) 57 90 9X JALWA (FREE) 58 91 B4U MUSIC (FREE) 59 92 PTC PUNJABI (FREE) 60 93 SANGEET BHOJPURI (FREE) 61 94 9XM (FREE) 62 95 PTC CHAKDE (FREE) 63 96 SAHANA (FREE) 64 97 9XO (FREE) 65 98