The Right Rocket for the Job: Small Launch Providers Target Small Satellites

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cape Canaveral Air Force Station Support to Commercial Space Launch

The Space Congress® Proceedings 2019 (46th) Light the Fire Jun 4th, 3:30 PM Cape Canaveral Air Force Station Support to Commercial Space Launch Thomas Ste. Marie Vice Commander, 45th Space Wing Follow this and additional works at: https://commons.erau.edu/space-congress-proceedings Scholarly Commons Citation Ste. Marie, Thomas, "Cape Canaveral Air Force Station Support to Commercial Space Launch" (2019). The Space Congress® Proceedings. 31. https://commons.erau.edu/space-congress-proceedings/proceedings-2019-46th/presentations/31 This Event is brought to you for free and open access by the Conferences at Scholarly Commons. It has been accepted for inclusion in The Space Congress® Proceedings by an authorized administrator of Scholarly Commons. For more information, please contact [email protected]. Cape Canaveral Air Force Station Support to Commercial Space Launch Colonel Thomas Ste. Marie Vice Commander, 45th Space Wing CCAFS Launch Customers: 2013 Complex 41: ULA Atlas V (CST-100) Complex 40: SpaceX Falcon 9 Complex 37: ULA Delta IV; Delta IV Heavy Complex 46: Space Florida, Navy* Skid Strip: NGIS Pegasus Atlantic Ocean: Navy Trident II* Black text – current programs; Blue text – in work; * – sub-orbital CCAFS Launch Customers: 2013 Complex 39B: NASA SLS Complex 41: ULA Atlas V (CST-100) Complex 40: SpaceX Falcon 9 Complex 37: ULA Delta IV; Delta IV Heavy NASA Space Launch System Launch Complex 39B February 4, 2013 Complex 46: Space Florida, Navy* Skid Strip: NGIS Pegasus Atlantic Ocean: Navy Trident II* Black text – current programs; -

2008 Estes-Cox Corp. All Rights Reserved

Estes-Cox Corp. 1295 H Street, P.O. BOX 227 Patent Pending Penrose, CO 81240-0227 ©2008 Estes-Cox Corp. All rights reserved. (9-08) PN 2927-8 TABLE OF CONTENTS HOW DO I START MY OWN ESTES ROCKET FLEET? The best way to begin model rocketry is with an Estes flying model rocket Starter Set or Launch Set. You can ® Index . .2 Skill Level 2 Rocket Kits . .30 either start with a Ready To Fly Starter Set or Launch Set that has a fully constructed model rocket or an E2X How To Start . .3 Skill Level 3 Rocket Kits . .34 Starter Set or Launch Set with a rocket that requires assembly prior to launching. Both types of sets come What to Know . .4 ‘E’ Engine Powered Kits . .36 complete with an electrical launch controller, adjustable launch pad and an information booklet to get you out Model Rocket Safety Code . .5 Blurzz™ Rocket Racers . .36 and flying in no time. Starter Sets include engines, Launch Sets let you choose your own engines (not includ- Ready To Fly Starter Sets . .6 How Model Rocket Engines Work . .38 ed). You’ll need four ‘AA’ alkaline batteries and perhaps glue, depending on which set you select. E2X® Starter Sets . .8 Model Rocket Engine Chart . .39 Ready to Fly Launch Sets . .10 Engine Time/Thrust Curves . .40 Launch Sets . .12 Model Rocket Accessories . .41 HOW EASY AND HOW MUCH TIME DOES IT TAKE TO BUILD MY ROCKETS? Ready To Fly Rockets . .14 Estes R/C Airplanes . .42 ® E2X Rocket Kits . .16 Estes Educator™ Products . -

Commercial Space Transportation Developments and Concepts: Vehicles, Technologies and Spaceports

Commercial Space Transportation 2006 Commercial Space Transportation Developments and Concepts: Vehicles, Technologies and Spaceports January 2006 HQ003606.INDD 2006 U.S. Commercial Space Transportation Developments and Concepts About FAA/AST About the Office of Commercial Space Transportation The Federal Aviation Administration’s Office of Commercial Space Transportation (FAA/AST) licenses and regulates U.S. commercial space launch and reentry activity, as well as the operation of non-federal launch and reentry sites, as authorized by Executive Order 12465 and Title 49 United States Code, Subtitle IX, Chapter 701 (formerly the Commercial Space Launch Act). FAA/AST’s mission is to ensure public health and safety and the safety of property while protecting the national security and foreign policy interests of the United States during commercial launch and reentry operations. In addition, FAA/AST is directed to encour- age, facilitate, and promote commercial space launches and reentries. Additional information concerning commercial space transportation can be found on FAA/AST’s web site at http://ast.faa.gov. Federal Aviation Administration Office of Commercial Space Transportation i About FAA/AST 2006 U.S. Commercial Space Transportation Developments and Concepts NOTICE Use of trade names or names of manufacturers in this document does not constitute an official endorsement of such products or manufacturers, either expressed or implied, by the Federal Aviation Administration. ii Federal Aviation Administration Office of Commercial Space Transportation 2006 U.S. Commercial Space Transportation Developments and Concepts Contents Table of Contents Introduction . .1 Significant 2005 Events . .4 Space Competitions . .6 Expendable Launch Vehicles . .9 Current Expendable Launch Vehicle Systems . .9 Atlas 5 - Lockheed Martin Corporation . -

IT's a Little Chile up Here

IT’s A Little chile up here Press Kit | NET 29 July 2021 LAUNCH INFORMATION LAUNCH WINDOW ORBIT 12-day launch window opening from 29 July 2021 600km DAILY LAUNCH OPPORTUNITY The launch timing for this mission is the same for each day of the launch window. SATELLITES Time Zone Window Open Window Close NZT 18:00 20:00 UTC 06:00 08:00 1 EDT 02:00 04:00 PDT 23:00 01:00 The launch window extends for 12 days. INCLINATION 37 Degrees LAUNCH SITE Launch Complex 1, Mahia, New Zealand CUSTOMER LIVE STREAM Watch the live launch webcast: USSF rocketlabusa.com/live-stream Dedicated mission for U.S. Space Force 2 | Rocket Lab | Press Kit: It’s A Little Chile Up Here Mission OVERVIEW About ‘It’s a Little Chile Up Here’ Electron will launch a research and development satellite to low Earth orbit from Launch Complex 1 in New Zealand for the United States Space Force COMPLEX 1 LAUNCH MAHIA, NEW ZEALAND Electron will deploy an Air Force Research Laboratory- sponsored demonstration satellite called Monolith. ‘It’s a Little Chile Up Here’ The satellite will explore and demonstrate the use of a deployable sensor, where the sensor’s mass is a will be Rocket Lab’s: substantial fraction of the total mass of the spacecraft, changing the spacecraft’s dynamic properties and testing ability to maintain spacecraft attitude control. Analysis from the use of a deployable sensor aims to th st enable the use of smaller satellite buses when building 4 21 future deployable sensors such as weather satellites, launch for Electron launch thereby reducing the cost, complexity, and development timelines. -

Press Release

Rocket Lab, an End-to-End Space Company and Global Leader in Launch, to Become Publicly Traded Through Merger with Vector Acquisition Corporation End-to-end space company with an established track record, uniquely positioned to extend its lead across a launch, space systems and space applications market forecast to grow to $1.4 trillion by 2030 One of only two U.S. commercial companies delivering regular access to orbit: 97 satellites deployed for governments and private companies across 16 missions Second most frequently launched U.S. orbital rocket, with proven Photon spacecraft platform already operating on orbit and missions booked to the Moon, Mars and Venus Transaction will provide capital to fund development of reusable Neutron launch vehicle with an 8-ton payload lift capacity tailored for mega constellations, deep space missions and human spaceflight Proceeds also expected to fund organic and inorganic growth in the space systems market and support expansion into space applications enabling Rocket Lab to deliver data and services from space Business combination values Rocket Lab at an implied pro forma enterprise value of $4.1 billion. Pro forma cash balance of the combined company of approximately $750 million at close Rocket Lab forecasts that it will generate positive adjusted EBITDA in 2023, positive cash flows in 2024 and more than $1 billion in revenue in 2026 Group of top-tier institutional investors have committed to participate in the transaction through a significantly oversubscribed PIPE of approximately $470 million, with 39 total investors including Vector Capital, BlackRock and Neuberger Berman Transaction is expected to close in Q2 2021, upon which Rocket Lab will be publicly listed on the Nasdaq under the ticker RKLB Current Rocket Lab shareholders will own 82% of the pro forma equity of combined company Long Beach, California – 1 March 2021 – Rocket Lab USA, Inc. -

2019 Nano/Microsatellite Market Forecast, 9Th Edition

2019 NANO/MICROSATELLITE MARKET FORECAST, 9TH EDITION Copyright 2018, SpaceWorks Enterprises, Inc. (SEI) APPROVED FOR PUBLIC RELEASE. SPACEWORKS ENTERPRISES, INC., COPYRIGHT 2018. 1 Since 2008, SpaceWorks has actively monitored companies and economic activity across both the satellite and launch sectors 0 - 50 kg 50 - 250kg 250 - 1000kg 1000 - 2000kg 2000kg+ Custom market assessments are available for all mass classes NANO/MICROSATELLITE DEFINITION Picosatellite Nanosatellite Microsatellite Small/Medium Satellite (0.1 – 0.99 kg) (1 – 10 kg) (10 – 100 kg) (100 – 1000 kg) 0 kg 1 kg 10 kg 100 kg 1000 kg This report bounds the upper range of interest in microsatellites at 50 kg given the relatively large amount of satellite development activity in the 1 – 50 kg range FORECASTING METHODOLOGY SpaceWorks’ proprietary Launch Demand Database (LDDB) Downstream serves as the data source for all satellite market Demand assessments ▪ Planned The LDDB is a catalogue of over 10,000+ historical and Constellations future satellites containing both public and non-public (LDDB) satellite programs Launch Supply SpaceWorks newly updated Probabilistic Forecast Model (PFM) is used to generate future market potential SpaceWorks PFM Model ▪ The PFM considers down-stream demand, announced/planed satellite constellations, and supply-side dynamics, among other relevant factors Expert Analysis The team of expert industry analysts at SpaceWorks SpaceWorks further interprets and refines the PFM results to create Forecast accurate market forecasts Methodology at a Glance 2018 SpaceWorks forecasted 2018 nano/microsatellite launches with unprecedented accuracy – actual satellites launched amounted to just 5% below our analysts’ predictions. In line with SpaceWorks’ expectations, the industry corrected after a record launch year in 2017, sending 20% less nano/microsatellites to orbit than in 2018. -

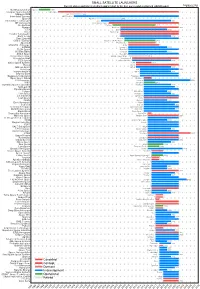

Small Satellite Launchers

SMALL SATELLITE LAUNCHERS NewSpace Index 2020/04/20 Current status and time from development start to the first successful or planned orbital launch NEWSPACE.IM Northrop Grumman Pegasus 1990 Scorpius Space Launch Demi-Sprite ? Makeyev OKB Shtil 1998 Interorbital Systems NEPTUNE N1 ? SpaceX Falcon 1e 2008 Interstellar Technologies Zero 2021 MT Aerospace MTA, WARR, Daneo ? Rocket Lab Electron 2017 Nammo North Star 2020 CTA VLM 2020 Acrux Montenegro ? Frontier Astronautics ? ? Earth to Sky ? 2021 Zero 2 Infinity Bloostar ? CASIC / ExPace Kuaizhou-1A (Fei Tian 1) 2017 SpaceLS Prometheus-1 ? MISHAAL Aerospace M-OV ? CONAE Tronador II 2020 TLON Space Aventura I ? Rocketcrafters Intrepid-1 2020 ARCA Space Haas 2CA ? Aerojet Rocketdyne SPARK / Super Strypi 2015 Generation Orbit GoLauncher 2 ? PLD Space Miura 5 (Arion 2) 2021 Swiss Space Systems SOAR 2018 Heliaq ALV-2 ? Gilmour Space Eris-S 2021 Roketsan UFS 2023 Independence-X DNLV 2021 Beyond Earth ? ? Bagaveev Corporation Bagaveev ? Open Space Orbital Neutrino I ? LIA Aerospace Procyon 2026 JAXA SS-520-4 2017 Swedish Space Corporation Rainbow 2021 SpinLaunch ? 2022 Pipeline2Space ? ? Perigee Blue Whale 2020 Link Space New Line 1 2021 Lin Industrial Taymyr-1A ? Leaf Space Primo ? Firefly 2020 Exos Aerospace Jaguar ? Cubecab Cab-3A 2022 Celestia Aerospace Space Arrow CM ? bluShift Aerospace Red Dwarf 2022 Black Arrow Black Arrow 2 ? Tranquility Aerospace Devon Two ? Masterra Space MINSAT-2000 2021 LEO Launcher & Logistics ? ? ISRO SSLV (PSLV Light) 2020 Wagner Industries Konshu ? VSAT ? ? VALT -

Space Coast Is Getting Busy: 6 New Rockets Coming to Cape Canaveral, KSC

4/16/2019 Space Coast is getting busy: 6 new rockets coming to Cape Canaveral, KSC Space Coast is getting busy: 6 new rockets coming to Cape Canaveral, Kennedy Space Center Emre Kelly, Florida Today Published 4:04 p.m. ET April 11, 2019 | Updated 7:53 a.m. ET April 12, 2019 COLORADO SPRINGS, Colo. – If schedules hold, the Space Coast will live up to its name over the next two years as a half-dozen new rockets target launches from sites peppered across the Eastern Range. Company, government and military officials here at the 35th Space Symposium, an annual space conference, have reaffirmed their plans to launch rockets ranging from more traditional heavy-lift behemoths to smaller vehicles that take advantage of new manufacturing technologies. Even if some of these schedules slip, at least one thing is apparent to several spaceflight experts here: The Eastern Range is seeing an unprecedented growth in commercial space companies and efforts. Space Launch System: 2020 NASA's Space Launch System rocket launches from Kennedy Space Center's pad 39B in this rendering by the agency. (Photo: NASA) NASA's long-awaited SLS, a multibillion-dollar rocket announced in 2011, is slated to become the most powerful launch vehicle in history if it can meet a stringent late 2020 deadline. The 322-foot-tall rocket is expected to launch on its first flight – Exploration Mission 1 – from Kennedy Space Center with an uncrewed Orion capsule for a mission around the moon, which fits in with the agency's wider goal of putting humans on the surface by 2024. -

Launcherone Success Opens New Space Access Gateway Guy Norris January 22, 2021

1/22/21 7:05 1/6 LauncherOne Success Opens New Space Access Gateway Guy Norris January 22, 2021 With San Nicolas Island far below, LauncherOne headed for polar orbit. Credit: Virgin Orbit Virgin Orbit had barely tweeted news of the successful Jan. 17 space debut of its LauncherOne vehicle on social media when new launch contracts began arriving in the company’s email inbox. A testament to the pent-up market demand for small-satellite launch capability, the speedy reaction to the long-awaited demonstration of the new space-access vehicle paves the way for multiple follow-on Virgin Orbit missions by year-end and a potential doubling of the rate in 2022. First successful privately developed air-launched, liquid-fueled rocket Payloads deployed for NASA’s Venture Class Launch Services program The glitch-free !ight of LauncherOne on its second demonstration test was a critical and much-welcomed milestone for the Long Beach, California-based company. Coming almost nine years a"er the air-launch concept was #rst unveiled by Virgin founder Richard Branson, and six years a"er the start of full-scale development, the !ight followed last May’s #rst demonstration mission, which ended abruptly when the rocket motor shut o$ a"er just 4 sec. 1/22/21 7:05 2/6 A"er an exhaustive analysis and modi#cations to beef up the oxidizer feed line at the heart of the #rst !ight failure, the path to the Launch Demo 2 test was then delayed until January 2021 by the COVID-19 pandemic. With the LauncherOne system now proven, design changes veri#ed and the #rst 10 small satellites placed in orbit, Virgin Orbit is already focusing on the next steps to ramp up its production and launch-cadence capabilities. -

A Low-Cost Launch Assistance System for Orbital Launch Vehicles

Hindawi Publishing Corporation International Journal of Aerospace Engineering Volume 2012, Article ID 830536, 10 pages doi:10.1155/2012/830536 Review Article A Low-Cost Launch Assistance System for Orbital Launch Vehicles Oleg Nizhnik ERATO Maenaka Human-Sensing Fusion Project, 8111, Shosha 2167, Hyogo-ken, Himeji-shi, Japan Correspondence should be addressed to Oleg Nizhnik, [email protected] Received 17 February 2012; Revised 6 April 2012; Accepted 16 April 2012 Academic Editor: Kenneth M. Sobel Copyright © 2012 Oleg Nizhnik. This is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited. The author reviews the state of art of nonrocket launch assistance systems (LASs) for spaceflight focusing on air launch options. The author proposes an alternative technologically feasible LAS based on a combination of approaches: air launch, high-altitude balloon, and tethered LAS. Proposed LAS can be implemented with the existing off-the-shelf hardware delivering 7 kg to low-earth orbit for the 5200 USD per kg. Proposed design can deliver larger reduction in price and larger orbital payloads with the future advances in the aerostats, ropes, electrical motors, and terrestrial power networks. 1. Introduction point to the progress in the orbital delivery systems for these additional payload classes. Spaceflight is the mature engineering discipline—54 years old as of 2012. But seemingly paradoxically, it still relies solely 2. Overview of Previously Proposed LAS on the hardware and methodology developed in the very beginning of the spaceflight era. Modernly, still heavily-used A lot of proposals have been made to implement nonrocket Soyuz launch vehicle systems (LVSs) are the evolutionary LASandarelistedinTable 1. -

Spacewatchafrica October 2020 Edition

Satellite communications in disaster management VVVolVolVolVol o6 o6 66l l. .No. NoNo. No78 N N 55 oo5.. 10 October 2018 2020 AFRICA Nigeria AFRICA REPORT MIDDLE EAST SPACE RACE How GPS is driving SPECIALautomation REPORT in transport industry C O N T E N T S Vol. 8 No. 10 UAE participates in WSIS Forum 2020 DLR institute of space systems Editor in-chief Aliyu Bello UAE deploys another home-grown satellite Executive Manager Tonia Gerrald Jubilations as Nigeria ignites Africa's first satellite-based SA to the editor in-Chief Ngozi Okey augmentation service Head, Application Services M. Yakubu Gilat reports Q2 2020 results Editorial/ICT Services John Daniel Connectivity demand soars as leisure vessels become Usman Bello safer places to work and rest, reports IEC Telecom Alozie Nwankwo Arabsat partners Airbus as Saudi Arabia Juliet Nnamdi expands fleet of satellites Client Relations Sunday Tache Russia to launch Angosat-2 telecoms satellite Lookman Bello for Angola in March 2022 Safiya Thani When staying connected matters most, supportingPublic Marketing Offy Pat Health needs around the world Tunde Nathaniel How 21st century GIS technologies are supporting Wasiu Olatunde the global fight against outbreaks and epidemics Media Relations Favour Madu Khadijat Yakubu Irdeto offers enhanced security services Zacheous Felicia to Forthnet Finance Folarin Tunde Rack Centre plans $100m expansion to create West Africa's largest data centre PayTV operator challenges exclusive agreements in pay-tv industry Space Watch Magazine is a publication of Satellite communications in disaster management Communication Science, Inc. All correspondence should be addressed to editor, space Watch Magazine. How GPS is driving automation in transport industry Abuja office: Plot 2009, Awka Street, UTC Building, GF 11, Area 10, Garki, Abuja, Nigeria Tel: 234 80336471114, 07084706167, email: [email protected] LEGAL CONSULTANTS Idowu Oriola & Co. -

China's Strategic Modernization: Implications for the United States

CHINA’S STRATEGIC MODERNIZATION: IMPLICATIONS FOR THE UNITED STATES Mark A. Stokes September 1999 ***** The views expressed in this report are those of the author and do not necessarily reflect the official policy or position of the Department of the Army, the Department of the Air Force, the Department of Defense, or the U.S. Government. This report is cleared for public release; distribution is unlimited. ***** Comments pertaining to this report are invited and should be forwarded to: Director, Strategic Studies Institute, U.S. Army War College, 122 Forbes Ave., Carlisle, PA 17013-5244. Copies of this report may be obtained from the Publications and Production Office by calling commercial (717) 245-4133, FAX (717) 245-3820, or via the Internet at [email protected] ***** Selected 1993, 1994, and all later Strategic Studies Institute (SSI) monographs are available on the SSI Homepage for electronic dissemination. SSI’s Homepage address is: http://carlisle-www.army. mil/usassi/welcome.htm ***** The Strategic Studies Institute publishes a monthly e-mail newsletter to update the national security community on the research of our analysts, recent and forthcoming publications, and upcoming conferences sponsored by the Institute. Each newsletter also provides a strategic commentary by one of our research analysts. If you are interested in receiving this newsletter, please let us know by e-mail at [email protected] or by calling (717) 245-3133. ISBN 1-58487-004-4 ii CONTENTS Foreword .......................................v 1. Introduction ...................................1 2. Foundations of Strategic Modernization ............5 3. China’s Quest for Information Dominance ......... 25 4.