Papers for Accounts Commission Meeting

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Accounts Commission Papers for Meeting

The Accounts Commission for Scotland Agenda Meeting on Thursday 20 January 2011, in the offices of Audit Scotland, 18 George Street, Edinburgh The meeting will begin at 10:00 am 1. Apologies for absence 2. Declarations of interest 3. Decisions on taking business in private: The Commission will consider whether to take items 13, 14 and 15 in private. 4. Minutes of meeting of 9 December 2010 5. Minutes of meeting of the Performance Audit Committee of 9 December 2010 6. Chair’s introduction: The Chair will report on recent activity and issues of interest to the Commission. 7. Update report by the Controller of Audit: The Commission will consider a report from the Controller of Audit on significant recent activity in relation to the audit of local government. 8. Public Services Reform (Scotland) Act 2010: The Commission will consider a report on duties arising from the Act. 9. Scottish Government Spending Plans and Draft Budget 2011/12: The Commission will consider a briefing. 10. Grampian Police and Grampian Joint Police Board - Best Value Audit and Inspection: The Commission will consider a joint report by the Controller of Audit and Her Majesty’s Inspectorate of Constabulary for Scotland. 11. Shetland Islands Council: The Commission will consider a report by the Controller of Audit on the annual audit 2009/10. 12. 2010 Local Government Overview: The Commission will consider a report by the Controller of Audit. 13. Grampian Police and Grampian Joint Police Board - Best Value Audit and Inspection: The Commission will consider the action it wishes to take on the report. -

BBC Radio Post-1967

1967 1968 1969 1970 1971 1972 1973 1974 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 Operated by BBC Radio 1 BBC Radio 1 Dance BBC Radio 1 relax BBC 1Xtra BBC Radio 1Xtra BBC Radio 2 BBC Radio 3 National BBC Radio 4 BBC Radio BBC 7 BBC Radio 7 BBC Radio 4 Extra BBC Radio 5 BBC Radio 5 Live BBC Radio Five Live BBC Radio 5 Live BBC Radio Five Live Sports Extra BBC Radio 5 Live Sports Extra BBC 6 Music BBC Radio 6 Music BBC Asian Network BBC World Service International BBC Radio Cymru BBC Radio Cymru Mwy BBC Radio Cymru 2 Wales BBC Radio Wales BBC Cymru Wales BBC Radio Wales BBC Radio Wales BBC Radio Wales BBC Radio Gwent BBC Radio Wales Blaenau Gwent, Caerphilly, Monmouthshire, Newport & Torfaen BBC Radio Deeside BBC Radio Clwyd Denbighshire, Flintshire & Wrexham BBC Radio Ulster BBC Radio Foyle County Derry BBC Northern Ireland BBC Radio Ulster Northern Ireland BBC Radio na Gaidhealtachd BBC Radio nan Gàidheal BBC Radio nan Eilean Scotland BBC Radio Scotland BBC Scotland BBC Radio Orkney Orkney BBC Radio Shetland Shetland BBC Essex Essex BBC Radio Cambridgeshire Cambridgeshire BBC Radio Norfolk Norfolk BBC East BBC Radio Northampton BBC Northampton BBC Radio Northampton Northamptonshire BBC Radio Suffolk Suffolk BBC Radio Bedfordshire BBC Three Counties Radio Bedfordshire, Hertfordshire & North Buckinghamshire BBC Radio Derby Derbyshire (excl. -

Radio in 1984

UK and Ireland Radio Stations in 1984 During the 1980s, there were six main radio services in the UK: Radios 1 to 4, BBC 1984 is a good point at which to take a snapshot. A major expansion of BBC and local and regional radio and a single tier of independent local stations. Most Independent local radio had just completed, supported by the opening of new stations broadcast on both FM and AM, known as simulcasting. The main FM spectrum between 102 and 105 MHz. Most parts of the country could receive exception was Radio 1, which was only available on AM. However, the BBC either a BBC or independent local radio station, but not necessarily both. The national networks broadcast separate FM and AM programmes at certain times. reorganisation of the local radio FM sub-bands did not happen until 1986-7, so Radio 1 borrowed Radio 2’s FM network for a few hours a week. A few Radio 2 many stations (or their successors) now use different frequencies. Many music programmes were also carried on FM only with sport opting out on AM. transmitter powers were also increased after the frequency changes. Radio 3’s AM network sometimes broadcast cricket commentaries with regular By 1984, all of the minor upgrades to the BBC’s national AM networks, following programmes on FM only. Meanwhile Radio 4’s FM network opted out with the reorganisation in 1978 had been completed, leaving them (essentially in their education programmes. final form). The re-engineering of the FM network had begun with 30 new sites Simulcasting was needed because most car radios were AM-only during the added since the late 1970s and several transmitters upgraded to mixed 1980s and many AM-only portable radios purchased in the 1960s and early 1970s polarisation. -

National Qualifications Curriculum Support

NATIONAL QUALIFICATIONS CURRICULUM SUPPORT English and Communication Using Scottish Texts Support Notes and Bibliographies [MULTI-LEVEL] Edited by David Menzies INTRODUCTION First published 1999 Electronic version 2001 © Scottish Consultative Council on the Curriculum 1999 This publication may be reproduced in whole or in part for educational purposes by educational establishments in Scotland provided that no profit accrues at any stage. Acknowledgement Learning and Teaching Scotland gratefully acknowledge this contribution to the Higher Still support programme for English. The help of Gordon Liddell is acknowledged in the early stages of this project. Permission to quote the following texts is acknowledged with thanks: ‘Burns Supper’ by Jackie Kay, from Two’s Company (Blackie, 1992), is reproduced by permission of Penguin Books Ltd; ‘War Grave’ by Mary Stewart, from Frost on the Window (Hodder, 1990), is reproduced by permission of Hodder & Stoughton Ltd; ‘Stealing’, from Selling Manhattan by Carol Ann Duffy, published by Anvil Press Poetry in 1987; ‘Ophelia’, from Ophelia and Other Poems by Elizabeth Burns, published by Polygon in 1991. ISBN 1 85955 823 2 Learning and Teaching Scotland Gardyne Road Dundee DD5 1NY www.LTScotland.com HISTORY 3 CONTENTS Section 1: Introduction (David Menzies) 1 Section 2: General works and background reading (David Menzies) 4 Section 3: Dramatic works (David Menzies) 7 Section 4: Prose fiction (Beth Dickson) 30 Section 5: Non-fictional prose (Andrew Noble) 59 Section 6: Poetry (Anne Gifford) 64 Section 7: Media texts (Margaret Hubbard) 85 Section 8: Gaelic texts in translation (Donald John MacLeod) 94 Section 9: Scots language texts (Liz Niven) 102 Section 10: Support for teachers (David Menzies) 122 ENGLISH III INTRODUCTION HISTORY 5 INTRODUCTION SECTION 1 Introduction One of the significant features of the provision for English in the Higher Still Arrangements is the prominence given to the study of Scottish language and literature. -

Ripe 2019: Universalism in Public Service Media

UNIVERSALISM IN PUBLIC SERVICE MEDIA RIPE 2019 Edited by: Philip Savage, Mercedes Medina, & Gregory Ferrell Lowe Ferrell Lowe, G. & Savage, P. (2020). Universalism in public service media: Paradoxes, challenges, and development in Philip Savage, Mercedes Medina and Gregory Ferrell Lowe (eds.) Universalism in Public Service Media. Gteborg: Nordicom. NORDICOM 1 Logotyp Logotyp Nordicoms huvudlogotyp består av namnet Nordicoms huvudlogotyp består av namnet ”Nordicom”. Logotypen är det enskilt viktigaste ”Nordicom”. Logotypen är det enskilt viktigaste elementet i Nordicoms visuella identitet och den Centrum fr nordisk medieforskning Centrum fr nordisk medieforskning ska finnas med i allt material där Nordicom står som avsändare. Använd alltid godkända original, de kan laddas ner här. Logotypens tre versioner Nordicoms logotyp finns i tre godkända grundversioner. • Logotyp. • Logotyp med undertext. • Logotyp på platta. Centre for Nordic Media Research Centre for Nordic Media Research Logotyp med undertext ska användas i lite större Logotyp med undertext ska användas i lite större format för att presentera Nordicom. Logotyp format för att presenteraBased at the Nordicom. University of Gothenburg,Logotyp Nordicom is a Nordic non-proft knowledge Contacts på platta ska användas där det behövs något centre that collects and communicates facts and research in the feld of media and communication. The purpose of our work is to develop the knowledge of media’s role Editor Administration, sales Postal address grafiskt med mer tyngd. in society. We do this through: Johannes Bjerling, PhD Anne Claesson Nordicom phone: +46 766 18 12 39 phone: +46 31 786 12 16 University of Gothenburg Following and documenting media development in terms of media structure, • [email protected] [email protected] PO Box 713 media ownership, media economy, and media use. -

Major Emergency Procedure

Shetland Major Emergency Procedure Version Version 06/2014 Completion date June 2014 Review date June 2017 Responsible officer Director of Public Health Approved by NHS Shetland Senior Management Team 2nd July 2014 Major Emergency Procedure Contents Amendment List Record ................................................................................... 4 Distribution List ..................................................................................................5 Part A Overview Introduction Preface Aim Legislation Definitions Background Associated Plans and Documentation Business / Service Continuity Risk Registers Audits Requests for Medical or Nursing Assistance at Incidents Voluntary Organisations‟ Aid Supplies Part B Message/Reporting System App B-1 Major Emergency - Information Flow App B-2 Event Log Part C Alerting and Activation App C-1 Receipt of Alert App C-2 Sample of Accident Information Form App C-3 Stages of Alert Part D Hospital Control Centre App D-1 Floor Plan of Hospital Control Centre Part E Hospital Evacuation Scheme Part F Casualty Treatment & Reception App F-1 Sample „Information on Emergency Patients for A&E Dept‟. App F-2 Ground Floor Plan - Accident & Emergency App F-3 Sample 'Major Incident Casualty Card' App F-4 Movement Plan - Major Incident Casualty Card Page 2 of 7 06/2014 Major Emergency Procedure Part G Finance Part H Media & Other Enquiries App H-1 Press Conferences Part I Exercises/Testing Part J Social Care Services to Casualties, Survivors and Next-of-Kin Part K Transport Part L NHS 24 Part -

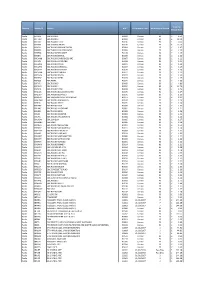

Domain Station ID Station UDC Performance Date No of Days in Period Total Per Minute Rate Radio BR ONE BBC RADIO 1 B0001 Census

Total Per Domain Station ID Station UDC Performance Date No of Days in Period Minute Rate Radio BR ONE BBC RADIO 1 B0001 Census 90 £ 4.51 Radio BR TWO BBC RADIO 2 B0002 Census 90 £ 18.00 Radio BR1EXT BBC RADIO 1XTRA B0106 Census 90 £ 0.60 Radio BR4DIG BBC SCHOOL RADIO B0109 Census 90 £ 13.70 Radio BRASIA BBC RADIO ASIAN NETWORK B0064 Census 90 £ 1.47 Radio BRBEDS BBC THREE COUNTIES RADIO B0065 Census 90 £ 1.25 Radio BRBERK BBC RADIO BERKSHIRE B0103 Census 90 £ 1.19 Radio BRBRIS BBC RADIO BRISTOL B0066 Census 90 £ 1.16 Radio BRCAMB BBC RADIO CAMBRIDGESHIRE B0067 Census 90 £ 1.22 Radio BRCLEV BBC RADIO CLEVELAND B0068 Census 90 £ 1.22 Radio BRCMRU BBC RADIO CYMRU B0011 Census 90 £ 1.24 Radio BRCORN BBC RADIO CORNWALL B0069 Census 90 £ 1.29 Radio BRCOVN BBC RADIO COVENTRY B0070 Census 90 £ 1.18 Radio BRCUMB BBC RADIO CUMBRIA B0071 Census 90 £ 1.23 Radio BRDEVN BBC RADIO DEVON B0072 Census 90 £ 1.30 Radio BRDRBY BBC RADIO DERBY B0073 Census 90 £ 1.25 Radio BRESSX BBC ESSEX B0074 Census 90 £ 1.36 Radio BRFIVE BBC RADIO 5 B0005 Census 90 £ 4.89 Radio BRFOUR BBC RADIO 4 B0004 Census 90 £ 13.70 Radio BRFOYL BBC RADIO FOYLE B0019 Census 90 £ 1.76 Radio BRGLOS BBC RADIO GLOUCESTERSHIRE B0075 Census 90 £ 1.17 Radio BRGUER BBC RADIO GUERNSEY B0076 Census 90 £ 1.13 Radio BRHRWC BBC HEREFORD AND WORCESTER B0077 Census 90 £ 1.21 Radio BRHUMB BBC RADIO HUMBERSIDE B0078 Census 90 £ 1.29 Radio BRJERS BBC RADIO JERSEY B0079 Census 90 £ 1.14 Radio BRKENT BBC RADIO KENT B0080 Census 90 £ 1.32 Radio BRLANC BBC RADIO LANCASHIRE B0081 Census 90 £ 1.21 Radio -

Preparing for Emergencies in the Highlands and Islands

Preparing for Emergencies in the Highlands and Islands A Guide to Civil Contingencies and Resilience Contents O Civil Contingencies 1 O Integrated Emergency Management 2 O Planning your own Emergency Arrangements 5 O How to put together an “Emergency Supply Kit” 6 O Evacuation 10 O Shelter 12 O Local Television and Radio Stations 13 O Floods 14 O Winter storms and extreme cold 17 O Heatwave 20 O Information on Flu 21 O Incidents with hazardous materials 23 O Fire 24 O Pets 27 O The recovery from a disaster 28 O The Procurator Fiscal Service 30 O Useful contact numbers and web pages 31 Introduction In today’s world there is an ongoing need to plan for the unpredictable and unexpected. Emergencies are triggered by a variety of causes - like the weather, transport accidents and terrorism, to name just three. This Guide, produced by the Highlands and Islands Strategic Co-ordinating Group (SCG), provides basic information about what Government does and is doing to protect its population and what you can do to protect yourself and your family in the event of a major emergency. The Guide provides general information and the basic dos and don’ts in simple steps to prepare for such an emergency without unnecessary interruption to day to day activities. The SCG welcomes this opportunity to inform the public and hopes that the information in this guide provides useful help to improve your ability to respond to any emergency. Civil Contingencies Central Government’s approach to civil Resilience is built around several contingency planning is built around the key activities. -

List of Radio Stations in the United Kingdom - Wikipedia, the Free Encyclopedia List of Radio Stations in the United Kingdom from Wikipedia, the Free Encyclopedia

2014년 5월 8일 List of radio stations in the United Kingdom - Wikipedia, the free encyclopedia List of radio stations in the United Kingdom From Wikipedia, the free encyclopedia This is a list of radio stations in the United Kingdom: Contents 1 National analogue and digital stations 2 Semi-National analogue, digital & online stations 3 Local and regional stations 3.1 BBC Local Radio 3.2 BBC Regional Radio 3.3 Local Commercial Radio 3.3.1 England 3.3.2 Former English stations 3.3.3 Northern Ireland 3.3.4 Former Northern Irish stations 3.3.5 Scotland 3.3.6 Former Scottish stations 3.3.7 Wales 3.3.8 Former Welsh stations 3.3.9 The Channel Islands & the Isle of Man 4 Community radio stations 5 Former community radio stations 6 RSL stations 7 Student and schools radio 8 Hospital radio stations 9 Satellite radio stations 10 Other 11 Frequencies 12 See also 13 References 14 External links National analogue and digital stations This list does not include stations which broadcast on numerous local digital multiplexes or MW licences to achieve near-national coverage DAB Name Format FM Frequencies AM Frequencies Freeview Freesat Sky Virgin Channels 11D (England, adult- Wales and Absolute 1197, 1215, 1233, 1242, 1260 orientated 105.8 FM (London) Northern 727 724 0107 915 Radio MW pop/rock music Ireland) 12A (Scotland) 11D (England, Wales and Absolute Music from the Northern 726 0200 951 80s 1980s Ireland) 12A (Scotland) 11D (England, Absolute Wales and Music from the Radio Northern 0203 1990s 90s Ireland) 12A (Scotland) youth- BBC orientated pop 97.6 -

History of Scots

History of Scots From the Middle Ages to the present day What is the Scots language? The Scots Language is one of the three indigenous languages of Scotland. Scotland’s other languages are English and Gaelic. English is used throughout Scotland, while Gaelic is used mostly in the Highlands and the Western Isles. Scots is spoken throughout the Lowlands, in the Scottish cities, and in the Northern Isles. Scots has often been misunderstood as slang, or as corrupt or inferior English. It isn’t wid ely known that Scots is a Germanic language in its own right, or that it is a sister language to English, with which it shares a common ancestor in Anglo-Saxon. It isn’t always appreciated that Scots has some 60,000 unique words and expressions, that it is the language of a magnificent, centuries-old literature, or that it was once a language of state used by kings, politicians and ordinary people alike. Scots is spoken on a continuum: this means that some people use more, and some people use less. Some of us use the occasional word or expression, such as wee, scunner, bonny, wean, peedie or peely-wally. Others speak in rich, braid Scots - replete with its own unique pronouns, prepositions, grammar and word-order. There are many different varieties of Scots. Some of these have names of their own, and they are sometimes known as ‘dialects’. It is important not to confuse dialects of Scots with dialects of English, or to imagine that Scots is a dialect of English. The dialects of Caithness, Orkney or Shetland are varieties of Scots. -

Challenges for Public Service Radio in Small Nations Lessons from Scotland

Chapter 8 Challenges for public service radio in small nations Lessons from Scotland Aleksandar Kocic & Jelena Milicev Abstract Scotland does not have any public service radio on a local level, except for a few bulletins or programmes offered by the British Broadcasting Corporation (BBC) Radio Scotland on an opt-out basis. Scottish commercial radio stations do cover local issues, but only in the form of brief hourly news bulletins without any in- depth coverage. By neglecting local news, BBC Scotland fails to meet one of its key obligations as a public service broadcaster – universality of content. Through a review of the existing literature on the role of media in democracy – and in particular the role of local radio – interviews with academics whose expertise lies in the fields of media policy and regulation, and focus groups with members of the public, this study formulates proposals on how to achieve universality in this key area of news provision in Scotland. Keywords: local, radio, public, service, news, regulation Introduction Scotland is a stateless nation, or as the British Broadcasting Corporation (BBC) refers to it in the context of its own structure – a national region. In the radio arena, Scotland has a very strong national player in the form of BBC Radio Scotland, which is both a national radio for Scotland and, as part of the bigger BBC family, a regional one. What Scotland lacks, though, is lo- cal public service radio along the lines of similar services in many countries, including south of the border in England. In terms of local news provision, radio audiences in Scotland are served by a network of commercial radio sta- tions, while the BBC in Scotland offers local news only on its website. -

SADA 18-19 Q4 Report

2018 - 2019: Quarter 4 Report of activity relating to Priority Areas of Activity Statements Case Studies: UHI Live Event Production module, Arts in Care Notable variances between target and actual Key Performance Indicators Interim Key Performance Indicator Statistics (appendix) Priority Area: Youth Arts Shetland has a vibrant Youth Arts scene provided by Q4 in numbers a range of individuals and groups. We will support and contribute to this provision, create and sustain engagement, and nurture creativity and talent through 2 Concerts / Screenings / Exhibition days an annual programme of access-level cross-artform 90 Audience attendances workshops, artform specific “intensives”, high-quality 25 Development Sessions music and drama productions and subsidised access to events and activities. 205 Participations John Haswell delivered a series of skills development workshops for Shetland Youth Theatre in preparation for their celebratory 25th Anniversary event later in the year. This is an event we’re very much looking forward to! The Shetland Young Promoters Group (SYPG) celebrated the 10th anniversary of the Battle of the Bands. Shetland Arts partnered with Shetland Youth Services to support and mentor the group whilst they organised the venue, technical specifications, marketing and promotion of the event. The night’s entertainment featured guest slots from established local acts as well as nine acts entering the competitive element of the competition. As in previous years, the winning band was gifted a free day of recording in the Mareel Recording Studio. Our Creativity Club program continued with blocks of Craft with Jane Cockayne and Photography with Steven Johnson. Priority Area: Education & Learning Our Education & Learning programme is diverse Q4 in numbers and offers provision at all levels.