Viewpoint: Contrasting Payments Innovation in Europe and the U.S

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

PIN Debit Networks November 7, 2013

Meeting Between Federal Reserve Board Staff and Representatives of PIN Debit Networks November 7, 2013 Participants: Louise Roseman, Stephanie Martin, Jeffrey Marquardt, Susan Foley, David Mills, Samantha Pelosi, Mark Manuszak, Krzysztof Wozniak, Tyler Standage, Aaron Rosenbaum, and Linda Healey (Federal Reserve Board) Terry Maher (Baird Holm LLP); Leah Work (CO-OP Financial Services); Jonathan Genovese and Rob Rankin (Jeanie Network); Cathy Morrissey (NETS); Robert Woodbury (NYCE Payments Network); Judith McGuire (PULSE); Scott Dobesh and Terry Dooley (Shazam Network); Nancy Loomis (Star Network); Paul Tomasofsky (Two Sparrows Consulting) Summary: Representatives of several PIN debit networks met with Federal Reserve Board staff to discuss their observations of market developments related to deployment of EMV (i.e., chip-based) debit cards in the United States. Issues discussed included (i) technological aspects of EMV payment cards with a focus on methods for enabling multiple networks on an EMV card, and (ii) the network participants’ views of issuer, merchant, and payment card network concerns related to EMV deployment, particularly as those concerns pertain to Regulation II’s prohibition on network exclusivity and merchant routing restrictions. In particular, the network representatives stressed the importance of industry adoption of an EMV model that best facilitates merchant routing choice, and expressed concern that the current approach advocated by Visa and MasterCard does not meet this objective. A copy of the presentation the -

AUTOMATED TELLER MACHINE (Athl) NETWORK EVOLUTION in AMERICAN RETAIL BANKING: WHAT DRIVES IT?

AUTOMATED TELLER MACHINE (AThl) NETWORK EVOLUTION IN AMERICAN RETAIL BANKING: WHAT DRIVES IT? Robert J. Kauffiiian Leollard N.Stern School of Busivless New 'r'osk Universit,y Re\\. %sk, Net.\' York 10003 Mary Beth Tlieisen J,eorr;~rd n'. Stcr~iSchool of B~~sincss New \'orl; University New York, NY 10006 C'e~~terfor Rcseai.clt 011 Irlfor~i~ntion Systclns lnfoornlation Systen~sI)epar%ment 1,eojrarcl K.Stelm Sclrool of' Busir~ess New York ITuiversity Working Paper Series STERN IS-91-2 Center for Digital Economy Research Stem School of Business Working Paper IS-91-02 Center for Digital Economy Research Stem School of Business IVorking Paper IS-91-02 AUTOMATED TELLER MACHINE (ATM) NETWORK EVOLUTION IN AMERICAN RETAIL BANKING: WHAT DRIVES IT? ABSTRACT The organization of automated teller machine (ATM) and electronic banking services in the United States has undergone significant structural changes in the past two or three years that raise questions about the long term prospects for the retail banking industry, the nature of network competition, ATM service pricing, and what role ATMs will play in the development of an interstate banking system. In this paper we investigate ways that banks use ATM services and membership in ATM networks as strategic marketing tools. We also examine how the changes in the size, number, and ownership of ATM networks (from banks or groups of banks to independent operators) have impacted the structure of ATM deployment in the retail banking industry. Finally, we consider how movement toward market saturation is changing how the public values electronic banking services, and what this means for bankers. -

GLOBAL PAYMENTS INC. (Exact Name of Registrant As Specified in Charter) Georgia 58-2567903 (State Or Other Jurisdiction of (I.R.S

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K È ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended May 31, 2004 OR ‘ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to . Commission File No. 001-16111 GLOBAL PAYMENTS INC. (Exact name of registrant as specified in charter) Georgia 58-2567903 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 10 Glenlake Parkway, North Tower, Atlanta, Georgia 30328-3495 (Address of principal executive offices) (Zip Code) Registrant’s telephone number, including area code: 770-829-8234 Securities registered pursuant to Section 12(b) of the Act: Name of each exchange Title of each class on which registered Common Stock, No Par Value New York Stock Exchange Series A Junior Participating Preferred Share Purchase Rights New York Stock Exchange Securities registered pursuant to Section 12(g) of the Act: NONE (Title of Class) Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes È No ‘ Indicate by check mark if disclosure of delinquent filer pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. -

Multi-Lateral Mechanism of Cash Machines: Virtue Or Hassel

International Journal of Engineering Technology Science and Research IJETSR www.ijetsr.com ISSN 2394 – 3386 Volume 4, Issue 10 October 2017 Multi-Lateral Mechanism of Cash Machines: Virtue or Hassel Peeush Ranjan Agrawal1 and Sakshi Misra Shukla2 1 Professor, School of Management studies, MNNIT, Allahabad, Uttar Pradesh,India 2Assistant Professor, Department of MBA, S.P. Memorial Institute of Technology, Allahabad, India ABSTRACT Automated Teller Machines or Cash Machines became an organic constituent of the banking sector. The paper envisionsthe voyage that these cash machines have gone through since their initiation in the foreign banks operating in India. The study revolves around the indispensible factors in the foreign banking environment like availability, connectivity customer base, security, network gateways and clearing houses which were thoroughly reviewed and analyzed in the research paper. The methodology of the research paper includes literature review, derivation of variables, questionnaire formulation, pilot testing, data collectionand application of statistical tools with the help of SPSS software. The paper draws out findings related to the usage, congregation, multi-lateral functioning, security and growth of ATMs in the foreign banks operating in the country. The paper concludes by rendering recommendations to theforeign bankers to vanquish the stumbling blocks of the cash machines functioning. Keywords: ATMs, Cash Machines, Anywhere Banking, Foreign Banking, Online Banking 1. INTRODUCTION The Automated Teller Machine (ATM) has become an integral part of banking operations. Initially perceived as ‘cash machines’, which dispenses cash to depositors, ATMs can accept deposits, sell postage stamps, print statements and be used at institutions where the depositor does not have an account. -

Field Guide to Alternative Payments

9TH ANNUAL rewards in ways that would have been unimaginable a few years earlier. It's the new world of alternative payments, and it's pretty much a mobile FIELD GUIDE TOworl d now. That's thanks not only to smart phones but also to clever applica• tion programing interfaces and the relatively recent opening of tech shops to ALTERNATIVE outside developers with smart ideas for integrating payments functionality with new apps (for more on this, see page 2A). PAYMENTS So here we are with our 9th Annual Field Guide to Alternative Payments, The increasing commercialization of mobile and, as you might expect, it bears little resemblance to the first Guide we put payments is showing up in a proliferation together in 2009. Herein, you'll find fully 27 entries that either didn't exist back of so-called Pays from a bevy of banks, then, or that were too nascent to include. tech companies, and merchants. You'll also find more than half a dozen "Pays," more if you count services like BY JOHN STEWART, JIM DALY, AND KEVIN WOODWARD People Pay and Self Pay. The inventors of the smart phone may not have conceived of the device as a payments tool, but in due course that is what it has become. As in prior years, Digital Transactions generally defines an alternative-payment system as any network or consumer interface (a mobile app, for example) that displaces the Visa/MasterCard/ AmEx/Discover networks (seen as one traditional system for this purpose), enables payments in a way that stands apart from that network (even if it ulti• mately uses it), and/or stands between that network and the consumer in an important way. -

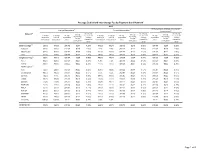

Average Debit Card Interchange Fee by Payment Card Network1

Average Debit Card Interchange Fee by Payment Card Network1 2015 All transactions (exempt and covered Exempt transactions 3 Covered transactions 4 transactions) 5 2 Interchange Interchange Interchange Network Average Average Average % of total % of total Average fee as % of % of total % of total Average fee as % of Average fee as % of interchange interchange interchange number of value of transaction average number of value of transaction average transaction average fee per fee per fee per transactions6 transactions6 value7 transaction transactions10 transactions10 value7 transaction value7 transaction transaction8 transaction8 transaction8 value9 value9 value9 11 Dual-message 38.2% 37.0% $36.49 $0.51 1.39% 61.8% 63.0% $38.38 $0.23 0.60% $37.66 $0.34 0.89% Discover 99.6% 99.5% $41.67 $0.65 1.56% 0.4% 0.5% $43.38 $0.24 0 55% $41.67 $0.65 1.55% MasterCard 50.8% 50.3% $37.98 $0.57 1.50% 49.2% 49.7% $38.77 $0.24 0.61% $38.37 $0.41 1.06% Visa 34.2% 32.7% $35.77 $0.48 1.34% 65.8% 67.3% $38.29 $0.23 0 59% $37.43 $0.31 0.84% Single-message12 35.2% 35.1% $39.04 $0.26 0.65% 64.8% 64.9% $39.36 $0.24 0.60% $39.25 $0.24 0.62% Accel 93.2% 92.8% $43.26 $0.21 0.48% 6.8% 7.2% $45.66 $0.24 0 53% $43.43 $0.21 0.49% AFFN 88.3% 86.9% $34.55 $0.25 0.72% 11.7% 13.1% $39.48 $0.21 0 54% $35.12 $0.25 0.70% Alaska Option13 ATH 14.2% 20.0% $50.58 $0.25 0.50% 85.8% 80.0% $33.44 $0.19 0 57% $35.87 $0.20 0.56% Credit Union 99.5% 99.5% $48.17 $0.23 0.47% 0.5% 0.5% $42.93 $0.20 0.47% $48.14 $0.23 0.47% Interlink 10.2% 9.4% $35.43 $0.35 0.99% 89.8% 90.6% $38.95 $0.24 -

TSB-A-97(86)S:12/97:NYCE Corporation,Petition No. S971015D

New York State Department of Taxation and Finance Taxpayer Services Division TSB-A-97(86)S Technical Services Bureau Sales Tax STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO.S971015D On October 15, 1997, the Department of Taxation and Finance received a Petition for Advisory Opinion from NYCE Corporation, 300 Tice Boulevard, Woodcliff Lake, New Jersey 07675. The issue raised by Petitioner, NYCE Corporation, is whether the fee it charges members of its banking network per transaction for electronic banking services performed through Automated Teller Machines (ATMs) and other similar machines is subject to New York State and local sales taxes under Section 1105(b) of the Tax Law. Petitioner submitted the following facts as the basis for this Advisory Opinion. Petitioner operates and administers a network through which it handles electronic banking transactions for members of the network. Members include both "banks" and "non-banks." All members pay a one-time initiation fee to join the network, but no annual fee thereafter. Each member participates in the network through a contract with Petitioner that is called a "Participation Agreement." The Participation Agreement incorporates by reference certain "Operating Rules." Petitioner included with its Petition, a copy of the Participation Agreement and the Operating Rules. There are thousands of possible combinations of activities and functions that Petitioner might perform with respect to an individual banking transaction. Petitioner must react to each transaction depending on the circumstances surrounding it. However, a "simple" transaction through the network from start to finish would generally take the following steps. Transaction Acquisition. -

CIDI Resolution Plan Public Section July 1, 2018 Submission

CIDI Resolution Plan Public Section July 1, 2018 Submission FRC 2018 Resolution Plan: Public Section Table of Contents 1 Introduction...................................................................................................................... 4 1.1 Overview of First Republic ................................................................................... 6 1.2 First Republic Organizational Structure .............................................................. 8 2 Material Entities .............................................................................................................. 11 3 Core Business Lines......................................................................................................... 12 4 Summary of Financial Information.................................................................................. 13 4.1 Financial Statements............................................................................................. 14 4.2 Capital .................................................................................................................. 16 4.3 Funding................................................................................................................. 16 4.4 Liquidity ................................................................................................................ 18 5 Description of Derivative and Hedging Activities ........................................................... 19 6 Membership in Material Payment, Clearing and Settlement Systems............................ -

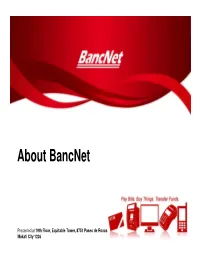

About Bancnet

About BancNet Presented at 19th Floor, Equitable Tower, 8751 Paseo de Roxas Makati City 1226 Who is BancNet • Electronic Switch Network that has financial institutions as its shareholders / members • 113 Member Banks • The largest inter bank network in the Philippines • First and Largest ATM Consortium in the Philippines • More than 23 years experience in ATM Networks • 113 Member Banks and Subscribers … and growing • Over 33.2 Million Active Cardholders, 11,383 ATMs • Strategy of Going Beyond ATM Banking • Multi-Bank, Multi-Channel Electronic Payment Network National and International Interconnection • ATM Networks Expressnet, Megalink • ATM Networks Mastercard, VISA • ATM & POS Network China Union Pay (CUP) • International partnership with NYCE BancNet Network I.CAN Government Agencies EPS POS POS Network ATM Network Network WeePay Member Banks ECS Bankard POS Network GHL BDO POS Network ATM Network Channels, Products & Services Point-of-Sale Internet Mobile Phone Mobile Phone Cash Withdrawal Intrabank Fund Transfer Cash Advance Inter Bank Fund Transfer Intrabank Fund Transfer Debit Card Purchase/Cash (CUP/VISA/JBC/Discover/D Checkbook Reorder Inter Bank Fund Transfer Withdrawal or Cash-out iners/MasterCard/Local) e-Shopping Checkbook Reorder Intrabank Fund Transfer Tax Payment e-Load Inter Bank Fund Transfer SSS-EDI Corporate G-Cash Reload Checkbook Reorder Philhealth (softlaunch) Statement Request Pagibig (Soon) G-Cash Reload/Auto Reload Balance Inquiry and Bills Payment Going Beyond ATM Banking BANCNET TAX PAYMENT ENROLLMENT PROCESS via BIR WEBSITE BANCNET BIR RDO EMPLOYER HSBC-AAB INFRASTRUCTURE Enroll via BIR Website Validate required documents submitted by Employer Bank to enroll the ff: via BancNet TPG Receive email 1. -

Operating Guide

Operating Guide June 2021 Operating Guide OG2021/06 Table of Contents CHAPTER 1. ABOUT YOUR CARD PROGRAM ........................................................................................1 About Transaction Processing ...................................................................................................................................... 1 General Operating Guidelines ...................................................................................................................................... 2 CHAPTER 2. PROCESSING TRANSACTIONS...........................................................................................4 Company Compliance ................................................................................................................................................... 4 Transaction Processing Procedures ............................................................................................................................. 6 Authorization................................................................................................................................................................. 7 Settling Daily Transactions ........................................................................................................................................... 9 Settlement (Paying Company for Transactions) ....................................................................................................... 10 Transaction Processing Restrictions ......................................................................................................................... -

Dispute Best Practices Guide Overview 3

Dispute Best Practices A merchant’s user guide to help manage disputes June 2019 For Global Disputes excluding PaySecure Front End Merchants Table of Contents Dispute Best Practices Dispute Best Practices Guide overview 3 Authorization overview 4 Transaction overview 5 Retrieval overview 6 Chargeback overview 9 Fraud – Card-not-present (CNP) 12 Compelling evidence overview 13 Fraud – Card-present (CP) 15 No valid authorization 17 Credit not processed 19 Services/Merchandise defective or not as described 21 Services not provided; merchandise not received 23 No-shows 25 Canceled recurring transaction 26 Duplicate processing 28 Data entry error 30 Late presentment 32 Paid by other means 33 2 Dispute Best Practices Dispute Best Practices Guide overview The Dispute Best Practices Guide explains the numerous aspects of transaction and dispute processing. This guide will provide you and your staff with educational guidance as it relates to dispute processing and suggest ways for you to help prevent financial chargebacks and liability. This guide includes: > An overview of authorization and transaction processing > An overview of retrievals and chargebacks > Reason code guidelines for all credit and debit networks The following card networks are covered in the reason code guidelines: Credit Networks Debit Networks American Express Accel Interlink Discover ACS/eFunds* Maestro Mastercard AFFN* NYCE Visa ATH * PULSE CU24* SHAZAM EBT* STAR Jeanie* STAR Access *These networks do not have specific reason codes assigned to dispute; however, any retrieval that is received without a reason code will be assigned a default code of 1. Any chargeback that is received without a reason code will be assigned a default code of 53. -

Navigating EFT Network Routing Rules

NYCE: Optimizing Your Debit Network Relationship Franchesca Gayadan Product S ales C ons ultant – NYCE Payments Network Discussion Items •Durbin Amendment •Indus try Update •NYCE Network Overview •NYC E S trategic Imperative Durbin Amendment R E GULATION – K ey P oints . FIs must maintain at least two debit network relationships – Defined as having POS access to DDAs – No distinction between signature and PIN authentication – The two networks must not be affiliated . Merchants control routing – Issuers no longer can designate routing between networks – Multiple PIN network relationships will be economically devastating - “How low can you go?” . FIs with assets of $10B and above – Regulated interchange - $.12 initial thought – Cannot have net POS transaction income - circumvention . Final guidelines – The Fed is expected to release final guidelines ????? FINANCIAL INS TITUTION IMPACTS Provision Result FIs must have at least two FIs will need to join another unaffiliated debit networks network Exclusive MC/Maestro or Visa/Interlink will Replace existing PIN based relationship to no longer be permitted avoid impacts of merchant routing discretion Merchants will have full discretion FIs should maintain only one PIN in transaction routing based network relationship FIs in multiple PIN based debit networks will Maintain higher interchange by preventing likely see interchange virtually eliminated merchants from “least cost” PIN based thru competitive downward spiral routing FIs with $10B and above in assets Again, maintain only one PIN based will have interchange capped network relationship Proposed at $.12 Even though capped, removal of merchant routing discretion will likely preserve highest allowable interchange S TR ATE GIC IMPE R ATIVE . Single focus on issuer value proposition – Favorable interchange structure for issuers – ATM – POS – R each and maintain net income parity with signature debit .