Journal of Applied Science and Agriculture a Study on The

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

IRAN UNDER SANCTIONS Iran’S Economy Has Been Under Sanctions in One Form Or Another Since the 1979 Revolution

IRAN UNDER IRANSANCTIONS UNDER SANCTIONS U.S. SanctionsU.S. Sanctions and Iran’s Energy Strategy and Iran’s EnergySARA VAKHSHOURI Strategy SARA VAKHSHOURI ABOUT IRAN UNDER SANCTIONS Iran’s economy has been under sanctions in one form or another since the 1979 revolution. Yet little systematic knowledge exists on the short- and medium-term impacts of sanctions on the growth patterns of the Iranian economy, the general welfare of its people in the cities and rural areas, societal dynamics, civic space, and the country’s environment. The focus has often been on a few metrics that flare up with tightening of sanctions: currency depreciation, inflation, and recession, which are then followed by increases in unemployment and poverty. But the more comprehensive picture is lost in political cacophony around the policy’s merits. This is the gap that SAIS is filling with its Iran Under Sanctions project, which is a 360-degree in-depth view on the implications of sanctions on Iran. This first-of-its-kind research provides for an instructive case study on the use of sanctions as a tool of statecraft. For any questions or feedback on the project, please reach out to Ali Vaez at [email protected]. ABOUT THE AUTHOR Sara Vakhshouri is the founder and president of SVB Energy International, a strategic energy consulting firm with offices in Washington, DC, and Dubai. She has more than two decades of experience working in the energy industry and has extensive experience in global energy market studies, energy strategy, energy security, and geopolitical risk. She has consulted with numerous public and private entities, as well as policy leaders and international organizations, including the International Monetary Fund, the World Bank, the International Energy Agency (IEA), and the US Energy Information Administration (EIA). -

Federal Register/Vol. 85, No. 63/Wednesday, April 1, 2020/Notices

18334 Federal Register / Vol. 85, No. 63 / Wednesday, April 1, 2020 / Notices DEPARTMENT OF THE TREASURY a.k.a. CHAGHAZARDY, MohammadKazem); Subject to Secondary Sanctions; Gender DOB 21 Jan 1962; nationality Iran; Additional Male; Passport D9016371 (Iran) (individual) Office of Foreign Assets Control Sanctions Information—Subject to Secondary [IRAN]. Sanctions; Gender Male (individual) Identified as meeting the definition of the Notice of OFAC Sanctions Actions [NPWMD] [IFSR] (Linked To: BANK SEPAH). term Government of Iran as set forth in Designated pursuant to section 1(a)(iv) of section 7(d) of E.O. 13599 and section AGENCY: Office of Foreign Assets E.O. 13382 for acting or purporting to act for 560.304 of the ITSR, 31 CFR part 560. Control, Treasury. or on behalf of, directly or indirectly, BANK 11. SAEEDI, Mohammed; DOB 22 Nov ACTION: Notice. SEPAH, a person whose property and 1962; Additional Sanctions Information— interests in property are blocked pursuant to Subject to Secondary Sanctions; Gender SUMMARY: The U.S. Department of the E.O. 13382. Male; Passport W40899252 (Iran) (individual) Treasury’s Office of Foreign Assets 3. KHALILI, Jamshid; DOB 23 Sep 1957; [IRAN]. Control (OFAC) is publishing the names Additional Sanctions Information—Subject Identified as meeting the definition of the of one or more persons that have been to Secondary Sanctions; Gender Male; term Government of Iran as set forth in Passport Y28308325 (Iran) (individual) section 7(d) of E.O. 13599 and section placed on OFAC’s Specially Designated [IRAN]. 560.304 of the ITSR, 31 CFR part 560. Nationals and Blocked Persons List Identified as meeting the definition of the 12. -

010 30060Nys090216 5

New York Science Journal 2016;9(2) http://www.sciencepub.net/newyork Rating of firms involved in Tehran Stock Exchange based on the accounting and non-accounting criteria using Fuzzy Topsis method Abdollah Kaabi Department of Accounting, Persian Gulf International Branch, Islamic Azad University, Khorramshahr, Iran [email protected] Abstract: In this study, companies operating in the Tehran Stock Exchange based on accounting standards (which are directly derived from the Company's financial statement data) include: Cash conversion cycle, liquidity, capital structure, return on assets and the size of the company and also non-accounting criteria for performance evaluation include: Economic value added, Jensen's alpha, Sharpe Ratio and proportion Trainor, using Fuzzy Topsis method ranked and with ranking based on the Tehran Stock Exchange indices were compared and their correlation were obtained. The main objective of this study is to determine whether the company according to reports from Tehran Stock Exchange is ranked top among other companies, in ranking based on accounting and non-accounting criteria for evaluating the performance of other companies is higher or not. The research method used for this study was survey. To do the calculations and analyze the spreadsheet data software (Excel) and to test hypotheses 16 Spss and Spearman correlation coefficient was used. The results of hypothesis testing and correlation analysis shows that between ranking companies of Stock Exchange based on stock indexes and ranking based on accounting and non- accounting variables, there is a weak correlation and the ranking of the exchange only in terms of liquidity and return on assets, of accounting standards, and of non accounting standards with Jensen's alpha coefficient and Economic value added, there is a significant relationship. -

Credit Rating Companies with Multi-Criteria Decision Making Models and Artificial Neural Network Model

J. Basic. Appl. Sci. Res., 3(5)536-546, 2013 ISSN 2090-4304 Journal of Basic and Applied © 2013, TextRoad Publication Scientific Research www.textroad.com Credit Rating Companies with Multi-Criteria Decision Making Models and Artificial Neural Network Model Maghsoud Amiri1, Mehdi Biglari Kami*2 1Allameh Tabatabaei University, Tehran, Iran 2Institute of Higher Education Raja, Qazvin, Iran ABSTRACT This research seeks to develop a procedure for credit rating of manufacturing corporations accepted in Tehran stock exchange. So, financial ratios of 181 manufacturing corporations in Iran stock exchange were extracted, These ratios reflect the financial ability to pay principal and interest of loan. Initially, fifty selected corporations ranked by using TOPSIS method based on financial ratios by using of Shannon entropy will be obtained the weight of each criterion. In addition, classification credit with neural network has compared by logistic regression; and finally, each had more credibility, used to rank all corporations. Then all corporations have classified by neural network. Finally, the neural network classification results compared with the expert classification. About 95% of the neural network data has placed in its respective class, and the data results indicated a robust neural network classification based on training. The neural network offered far more accurate answer than the logistic regression in this classification. At the end, the neural network ranked all corporations, and neural network classification results compared with expert opinion, showing that the neural network classification was very close to an expert opinion. KEYWORDS: Financial ratios; TOPSIS; Artificial neural network; Logistic regression. INTRODUCTION Today, the credit industry plays an important role in the economy of corporations. -

Members of Iranian Oil, Gas & Petrochemical Products Exporters

Members of Iranian Oil, Gas & Petrochemical Products Exporters’ Union No. Name of Company Web Products 1. Abadan Petrochemical Co. www.abadan.petro.com PVC Paraffin, Solid / Liquid, Vaselin, 2. Afra Shimi Yazd Co. www.afrashimi.com Foots Oil Import & Export Lubricant 3. Afzoon Ravan Co. www.afzoonravan.com Additives, Import & Export Lubricant Oil’s Furfural Extract, Paraffin, Oil 4. Alborz Chelic Iran Co. www.alborzchelic.com Products 5. Alborz Palayesh Eshtehard Co www.apec-ref.com Thinner 6. Alborz Rouzbehan Invesment Invesment Paraffin Wax, Residue Wax, 7. Ali Mohammad Jabarouti Trading www.jabarouti.com Foots Oil 8. Ali Pardazan Atiye Co. www.apainterco.com Bitumen Paraffin Wax, Foots Oil, RPO, 9. Ali Reza Zarenejad Trading www.zarenejadtrdg.com Base Oil 10. Alvan Sadegh Toos Co. Petrochemicals 11. Apadana Petro Bazargan Co. www.apadana-petro.com Hydrocarbons, Oil products 12. Aram Oil Co. www.aramoilco.com Extract, Bitumen 13. Arash Mahya Paraffin Manufacturing Co. www.arashmahya.com Paraffin Wax, Residue Wax Gas, Oil, Petroleum, Gas Oil L20- 14. Araz Shimi Jolfa Co. www.arazshimi.com L62, Light Oil, Mazout, Cyclic and non-CYCLIC hydrocarbons Base Oil , Motor Oil & Industrial 15. Aria Jam Oil Industries CO Oil 16. Aria Sanat Behineh Co. www.arialubricant.ir Oil, Grease, Anti Freeze 17. Arian Atlas Motor Oil Co. Motor Oil, Gear Oil 18. Arkan Gas Co. www.arkangas.com Gas & Petrochemical Products Bitumen,base Slack Wax Oil & و Armities Persia Co. www.armities.com .19 Petrochemical Products 20. Arvand Shimi Sorour Co. Oil, Grease Paraffin, Foots Oil, Furfural 21. Aryaparaffin Co. www.aryaparaffinco.com Extract, White Oil 22. -

April & May 2010 No.43-44, Volume 4

ran nvestment TURQUOISE Monthly April & May 2010 Volume 4, No 43-44 PARTNERS THIS MONTH Market Overview 2 Over the course of March and April, the Tehran Stock Exchange (TSE) performed strongly and hit a 3-year record high in trade volumes, due to further gains in global prices of commodities and crude oil in March. However, towards the end of April, and in line with a downturn in global commodities market, the TSE showed signals of a trend reversal. Turquoise Iran Equity Investments 5 This section provides data and charts on the performance of all portfolios of Turquoise Iran Equity Investments for the month of April. Country Overview 7 Iran’s state budget for the new Iranian Calendar year and the government’s plans to reduce Tehran’s population will be discussed in this section. Economy 9 Iran’s Economy in 1388, the new foreign investment law, Tejarat Bank’s credit rating and the South Pars field Euro bonds will be covered in this section. Iran Investment Monthly is produced by Turquoise Partners, No. 17 East Gord Alley, Turquoise Partners. Distributed electroni- Bidar St., Fayyazi (Fereshteh) Ave. cally by exclusive subscription. Tel :+98 21 220 35 830 Fax :+98 21 220 49 260 Chief Editor: Ramin Rabii Email : [email protected] Consulting Editor: Eddie Kerman To find out more about Turquoise Partners, Authors: Shervin Shahriari visit our website at: Ali Mashayekhi www.turquoisepartners.com. Iran Khodro’s Production Line in Tehran , Iran ‘s Largest Car Manufacturer , Iran ‘s Largest Tehran Production Line in Iran Khodro’s © 2010 All rights reserved Market Overview 2 March 2010 In March, the Tehran Stock Exchange bucked its historical trend. -

The Political Economy of the IRGC's Involvement in the Iranian Oil and Gas Industry

The Political Economy of the IRGC’s involvement in the Iranian Oil and Gas Industry: A Critical Analysis MSc Political Science (Political Economy) Thesis Research Project: The Political Economy of Energy University of Amsterdam, Graduate School of Social Sciences 5th June 2020 Author: Hamed Saidi Supervisor: Dr. M. P. (Mehdi) Amineh (1806679) Second reader: Dr. S. (Said) Rezaeiejan [This page is intentionally left blank] 2 Table of Contents Table of Contents ................................................................................................................................ 3 Abstract ............................................................................................................................................... 6 Acknowledgments ............................................................................................................................... 7 Maps ................................................................................................................................................ 8 List of Figures and Tables ................................................................................................................. 10 List of Abbreviations ........................................................................................................................ 11 I: RESEARCH DESIGN .................................................................................................................................... 13 1.1. Introduction ........................................................................................................................ -

Annual Report Annual Report

Tehran Stock Exchange Annual Report Exchange 2011 Stock Tehran Tehran Stock Exchange Address: No.228,Hafez Ave. Tehran - Iran Tel: (+98 021) 66704130 - 66700309 - 66700219 Fax: (+98 021) 66702524 Zip Code: 1138964161 Gun-metal relief discovered in Lorestan prov- ince, among the Achaemedian dynasty’s (550-330 BC)Antiquities. Featuring four men, hand in hands, indicating unity and cooperation; standing inside circles of 2011 globe,which is it, according to Iranian ancient myths, put on the back of two cows, ANNUAL symbols of intelligence and prosperity. Tehran Stock Exchange Implementation: CAPITAL&MARKET REPORT ANNUAL REPORT Tehran Stock Exchange 2011 Tehran Stock Exchange Tehran www.tse.ir Annual Report 2011 2 Tehran Stock Exchange Tehran www.tse.ir Mission Statement To develop a fair, efficient and transparent market equipped with diversified instruments and easy access in order to create added value for the stakeholders. Vision To be the region’s leading Exchange and country’s economic growth driver. Goals To increase the capital market’s share in financing the economic productive activities. To apply the effective rules and procedures to protect the market’s integrity and shareholders’ equity. To expand the market through using updated and efficient technology and processes. To promote financial literacy and develop investing and shareholding culture in Iran. To extend and facilitate the market access through information technology. To create value for shareholders and comply with transparency and accountability principles, with cooperation -

Abstract FC Approach in Portfolio Selection of Tehran's Stock Market

Elham Shadkam / Journal of Asian Finance, Economics and Business Vol. 1 No.2 (2014) 31-37 31 Print ISSN: 2288-4637 / Online ISSN 2288-4645 doi: 10.13106/jafeb.2014.vol1.no2.31. FC Approach in Portfolio Selection of Tehran’s Stock Market 6) Elham Shadkam* [Received: February 20, 2014 Revised: April 20, 2014 Accepted: April 28, 2014] One of the theories that in recent decades, had has a high Abstract position in determining the optimum portfolio, is the modern portfolio theory which belong to Harry Markowitz and William Sharpe. The modern portfolio theory has a holistic approach to The portfolio selection is one of the most important and vital the stock market. Contrary to technical or conservative ap- decisions that a real or legal person, who invests in stock mar- proach, this theory focuses all stock in market. In other words, ket, should make. The main purpose of this article is the deter- the perspective view of this theory is macro perspectives versus mination of the optimal portfolio with regard to relations among micro perspectives. One of the basic criteria for decision making stock returns of companies which are active in Tehran’s stock in stock is stock returns. Stock returns had has informative market. For achieving this goal, weekly statistics of company’s document by itself which most investors use it to predict and stocks since Farvardin 1389 until Esfand 1390, has been used. analysis financial Items (Ghodrati & Zahiri, 2014). In numerous For analyzing statistics and information and examination of studies have been done on determining the optimal portfolio, stocks of companies which has change in returns, factors analy- "the risk" has been mentioned as the main criteria for determin- sis approach and clustering analysis has been used (FC ap- ing the optimal stock portfolio. -

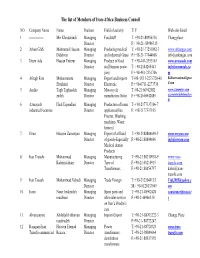

The List of Members of Iran-Africa Business Council

The list of Members of Iran-Africa Business Council NO Company Name Name Position Field of activity T/ F Web-site-Email 1 -------------- Mir Khodavandi Managing Foodstuff T: +98-21-88986316 Chang place Director F:+ 98-21- 88986315 2 Arkan GAS Mohmmad Hassan Managing Producing medical T: +98-21-77251862-3 www.arkangas.com Didehvar Director and industrial Grass F:+ 98-21-77844068 [email protected] 3 Urum Ada Hassan Entezar Managing Produce of food T:+ 98-441-2353163 www.urumada.com Director stuff(tomato paste- T:+ 98-2144205443 [email protected] jam) F:+ 98-441-2351706 m 4 Afrugh Fars Mohammreza Managing Export and Import- T+98-:0711-2273720-40 Kidinternational@gma Ebrahimi Director Electronic F:+ 98-0711-2273730 il.com 5 Amiko Tagh Taghzadeh Managing Motorcycle T+98-21:66942882 www.azarmotor.com zadeh Director manufacture-Solar F:+ 98-2166942885 [email protected] m 6 Azmayesh Hadi Espandiari Managing Production of home T:+ 98-2177337106-7 industrial Factories Director appliances(like F: +98-2177337105 Freezer, Washing machines, Water heaters) 7 Ozan Hossein Zamanyan Managing Export of all kind T:+ 98-2188804690-5 www.owzan.com Director of goods-Especially F:+98-21:88804696 [email protected] Medical dentist Products 8 Iran Transfo Mohammad Managing Manufacturing T:+98-21:88210918-9 www.iran- Kabiriisfahani Director Type of F:+98-21:88210915 transfo.com Transformers F:+98-21:88056797 kabiri@iran- transfo.com 9 Iran Toseeh Mohammad Vahedi Managing Trade Foreign T:+ 98-2122049125 [email protected] Director M:+ 98-9121033949 om 10 Isaco Naser -

Special Edition of Nationwide Strike by the Workers of Petrochemical, Oil, Gas and Refineries,Terminals and Power Plants!

No. 140 - 141 [email protected] 15the July, 2021 Special edition of nationwide strike by the workers of Petrochemical, Oil, Gas and Refineries,Terminals and Power plants! - We strongly support the oil industries… P. 1 -Statement of contract oil workers... p. 5 . - A message of solidarity from... P. 6 - The solidarity of the workers of oil co.... P. 7 - We go home ... P. 8 - The committee for the defense ... P. 8 . -The latest update on the number of centers ... P. 9 - In the fourth week of the strike,… P. 10 . - Nationwide strike of 1,400 project ... p. 11 - We strike, because we've heard too ... P. 12 . - Brief News... P. 12 - The Remedy for the Workers Is Unity ... P. 15 . - We'll go home, you can work instead ... P. 19 - Iranian petrochemical workers take ... P. 20 We strongly support the oil industries workers’ strikes of ‘’Campaign 1400’’ Our oil workers are our enduring, tenacious, unshakable leaders On Tuesday, 22nd June, 2021, the workers of the Tehran Oil Refinery, along with the Gachsaran Petrochemical project workers and other Petrochemicals project workers went on a nationwide strike. On Wednesday, 23rd June, 2021, other oil and petrochemical industries in cities joined Tehran Oil Industries. The scope of the strikes and protests, are expanding rapidly. Following a call by the Council for Organizing the Protest, the Contracted Oil Workers, have started their strike for one week. The Council for Organizing the Protest has announced, that contract and project workers will join the official oil workers’ strike on Wednesday, 30th June, 2021. About us: “The Committees in Solidarity with the Iranian workers Movement -Abroad" consist of solidarity groups and individuals outside of Iran that support Iranian Workers’. -

National Subway Train Developed Despite Sanctions

WWW.TEHRANTIMES.COM I N T E R N A T I O N A L D A I L Y 8 Pages Price 50,000 Rials 1.00 EURO 4.00 AED 42nd year No.13904 Sunday MARCH 14, 2021 Esfand 24, 1399 Rajab 30, 1442 Persons with military Skocic protests AFC over Free medical services “The Sand Wolf” background can stand choosing Bahrain as for people aged hunts Iran’s Flying as candidates Page 2 Group C host Page 3 over 65 Page 7 Turtle Page 8 Iranian heavy crude oil price rises 11.5% in February: OPEC TEHRAN- Iranian heavy oil price increased in the previous year’s same period. $6.28 in February to register an 11.5-per- The report put Iranian crude output for Illogical presence cent rise compared to the previous month, February at 2.12 million barrels per day according to OPEC’s latest monthly report. indicating a 35,000-bpd increase compared See page 3 Iran sold its heavy crude oil at $60.66 to the figure for the previous month. U.S. faces trouble justifying presence in Iraq per barrel in the mentioned month, com- Based on OPEC data, the country’s av- pared to January’s $54.38 per barrel, IRIB erage crude output in the fourth quarter reported. of 2020 stood at 1.993 million barrels According to the report, the country’s per day indicating a near 45,000-bpd average heavy crude price was $57.52 from rise compared to the figure for the third the beginning of 2021 up to the report’s quarter of the year.