Doing Business and Investing in Estonia 2014 Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Here in 2017 Sillamäe Vabatsoon 46% of Manufacturing Companies with 20 Or More Employees Were Located

Baltic Loop People and freight moving – examples from Estonia Final Conference of Baltic Loop Project / ZOOM, Date [16th of June 2021] Kaarel Kose Union of Harju County Municipalities Baltic Loop connections Baltic Loop Final Conference / 16.06.2021 Baltic Loop connections Baltic Loop Final Conference / 16.06.2021 Strategic goals HARJU COUNTY DEVELOPMENT STRATEGY 2035+ • STRATEGIC GOAL No 3: Fast, convenient and environmentally friendly connections with the world and the rest of Estonia as well as within the county. • Tallinn Bypass Railway, to remove dangerous goods and cargo flows passing through the centre of Tallinn from the Kopli cargo station; • Reconstruction of Tallinn-Paldiski (main road no. 8) and Tallinn ring road (main highway no. 11) to increase traffic safety and capacity • Indicator: domestic and international passenger connections (travel time, number of connections) Tallinn–Narva ca 1 h NATIONAL TRANSPORT AND MOBILITY DEVELOPMENT PLAN 2021-2035 • The main focus of the development plan is to reduce the environmental footprint of transport means and systems, ie a policy for the development of sustainable transport to help achieve the climate goals for 2030 and 2050. • a special plan for the Tallinn ring railway must be initiated in order to find out the feasibility of the project. • smart and safe roads in three main directions (Tallinn-Tartu, Tallinn-Narva, Tallinn-Pärnu) in order to reduce the time-space distances of cities and increase traffic safety (5G readiness etc). • increase speed on the railways to reduce time-space distances and improve safety; shift both passenger and freight traffic from road to rail and to increase its positive impact on the environment through more frequent use of rail (Tallinn-Narva connection 2035 1h45min) GENERAL PRINCIPLES OF CLIMATE POLICY UNTIL 2050 / NEC DIRECTIVE / ETC. -

The Baltic Republics

FINNISH DEFENCE STUDIES THE BALTIC REPUBLICS A Strategic Survey Erkki Nordberg National Defence College Helsinki 1994 Finnish Defence Studies is published under the auspices of the National Defence College, and the contributions reflect the fields of research and teaching of the College. Finnish Defence Studies will occasionally feature documentation on Finnish Security Policy. Views expressed are those of the authors and do not necessarily imply endorsement by the National Defence College. Editor: Kalevi Ruhala Editorial Assistant: Matti Hongisto Editorial Board: Chairman Prof. Mikko Viitasalo, National Defence College Dr. Pauli Järvenpää, Ministry of Defence Col. Antti Numminen, General Headquarters Dr., Lt.Col. (ret.) Pekka Visuri, Finnish Institute of International Affairs Dr. Matti Vuorio, Scientific Committee for National Defence Published by NATIONAL DEFENCE COLLEGE P.O. Box 266 FIN - 00171 Helsinki FINLAND FINNISH DEFENCE STUDIES 6 THE BALTIC REPUBLICS A Strategic Survey Erkki Nordberg National Defence College Helsinki 1992 ISBN 951-25-0709-9 ISSN 0788-5571 © Copyright 1994: National Defence College All rights reserved Painatuskeskus Oy Pasilan pikapaino Helsinki 1994 Preface Until the end of the First World War, the Baltic region was understood as a geographical area comprising the coastal strip of the Baltic Sea from the Gulf of Danzig to the Gulf of Finland. In the years between the two World Wars the concept became more political in nature: after Estonia, Latvia and Lithuania obtained their independence in 1918 the region gradually became understood as the geographical entity made up of these three republics. Although the Baltic region is geographically fairly homogeneous, each of the newly restored republics possesses unique geographical and strategic features. -

Estonian Ministry of Education and Research

Estonian Ministry of Education and Research LANGUAGE EDUCATION POLICY PROFILE COUNTRY REPORT ESTONIA Tartu 2008 Estonian Ministry of Education and Research LANGUAGE EDUCATION POLICY PROFILE COUNTRY REPORT ESTONIA Estonian Ministry of Education and Research LANGUAGE EDUCATION POLICY PROFILE COUNTRY REPORT ESTONIA Tartu 2008 Authors: Language Education Policy Profile for Estonia (Country Report) has been prepared by the Committee established by directive no. 1010 of the Minister of Education and Research of 23 October 2007 with the following members: Made Kirtsi – Head of the School Education Unit of the Centre for Educational Programmes, Archimedes Foundation, Co-ordinator of the Committee and the Council of Europe Birute Klaas – Professor and Vice Rector, University of Tartu Irene Käosaar – Head of the Minorities Education Department, Ministry of Education and Research Kristi Mere – Co-ordinator of the Department of Language, National Examinations and Qualifications Centre Järvi Lipasti – Secretary for Cultural Affairs, Finnish Institute in Estonia Hele Pärn – Adviser to the Language Inspectorate Maie Soll – Adviser to the Language Policy Department, Ministry of Education and Research Anastassia Zabrodskaja – Research Fellow of the Department of Estonian Philology at Tallinn University Tõnu Tender – Adviser to the Language Policy Department of the Ministry of Education and Research, Chairman of the Committee Ülle Türk – Lecturer, University of Tartu, Member of the Testing Team of the Estonian Defence Forces Jüri Valge – Adviser, Language Policy Department of the Ministry of Education and Research Silvi Vare – Senior Research Fellow, Institute of the Estonian Language Reviewers: Martin Ehala – Professor, Tallinn University Urmas Sutrop – Director, Institute of the Estonian Language, Professor, University of Tartu Translated into English by Kristel Weidebaum, Luisa Translating Bureau Table of contents PART I. -

Revitalisering Av Historiske Bykjerner Ni Utvalgte Estiske Byer

Revitalisering av historiske bykjerner Ni utvalgte estiske byer Estland har 12 beskyttede kulturmiljøer – Heritage Conservation Areas – hvorav 11 er i historiske bykjerner. Utlysningen «Historic old town centres with cultural heritage protection areas» retter seg mot de 9 beskyttede kulturmiljøene som ligger i henholdsvis byene Pärnu, Haapsalu, Kuressaare, Rakvere, Paide, Viljandi, Võru, Valga og Lihula. Mange av disse byene lider av synkende befolkningstall, som skyldes både lav fødselsrate og høy grad av fraflytting. Dette er en del av en ond sirkel av begrensede arbeidsmuligheter, lite investeringer i byene, og, i verste tilfelle, tap av byens identitet. På tross av disse utfordringene har de ni ovennevnte byene hver sine unike kulturmiljøer med bevarte historiske områder. PÄRNU Fylke: Pärnu fylke Grunnlagt: 1251 Areal: 32,22 km² Befolkning: 39 605 (2020) Befolkningstetthet: 1200 innb./km² Pärnu gamleby. Foto: ERR Pärnu er, med sine 39 605 (2020) innbyggere, Estlands fjerde største by. Den ligger sørvest i landet og har fått kallenavnet «Estlands sommerhovedstad» på grunn av sin rolle som feriedestinasjon. Økonomien er også sterkt knyttet til sesongaktiviteter og turisme. Dersom man ikke tar hensyn til sesong-baserte endringer, ligger befolkningstallet i Pärnu relativt stabilt, om enn med en svak nedgang. Den markante økningen i folketall sammenlignet med folketellingen i 2011 skyldes endringer i kommunegrensene. Villa Ammende. Foto: Visit Estonia. https://www.visitestonia.com/en/villa-ammende Det røde tårnet. Foto: PuhkaEestis.ee 2 https://www.puhkaeestis.ee/et/punane-torn Pärnu kulturmiljø De eldste områdene i kulturmiljøet i Pärnu er knyttet til byens middelalderslott og til den Hanseatiske byen. Spor etter Pärnu middelalderby er bevart, inkludert «det røde tårnet» og det historiske gatenettet, men det er det senere, barokke Pärnu som er mest tydelig. -

Lessons and Challenges Kuressaare, Saaremaa

LOCAL RESPONSE TO HARMFUL USE OF ALCOHOL: LESSONS AND CHALLENGES KURESSAARE, SAAREMAA Anu Vares Development Adviser Saaremaa Municipality Government, Estonia WHAT DID WE LEARN? • Local evidence and data help to address the community • Support of local government council and municipality mayor is crucial to implementation of activities • Finding the right spokespersons for alcohol-related topics is very important • It is necessary to talk to youngsters to find out their opinion on alcohol WHAT DID WE LEARN? • Schools can be difficult partners due to many different ongoing activities – thus it is very important to engage a “project manager” within the school • It is complicated to explain the school headmasters that the drug prevention action plan is necessary for the school, not for the local government and the police • Public debate following the project has encouraged other municipalities to plan systematic activities in alcohol prevention WHAT DID WE LEARN? • It is possible to create change at the local level • Cooperation is the crucial power • Will and dedicated people are more important than money • Desired results are not achieved quickly, it takes time and patience • To prevent and to reduce the consumption of alcohol by minors, it is necessary to address activities to adults as well as to change the environment around youngsters • Besides hobby education attention must be paid to children’s and youngsters’ relations with family and friends MAIN CHALLENGES • Where and how to address parents? • What is the role of schools and headmasters? • How to assure motivation of local actors and the continuity of activities? WHAT WILL HAPPEN IN SAAREMAA IN 2018+? • A new and very big municipality (2705 km2, 31 819 residents, 1 city, 9 small towns, 426 villages) • How to use experience gained in 2015–2017 in Kuressaare in other areas of the municipality? LAST, BUT NOT LEAST • Minors drink, but alcohol is made available by adults around them • Our common goal in Kuressaare / Saaremaa: adults do not sell, buy and offer alcohol to minors . -

Tallinn & Saaremaa Opera Days

Tallinn & Saaremaa Opera Days July 21 - 25, 2014 Mon, July 21 / Tallinn Individual arrival to the capital of Estonia. Transfer to a 4*hotel. Check-in for one night. Tue, July 22 / Tallinn – Muhu island – Kuressaare Breakfast and check-out 11:20 Departure to Saaremaa island 14:00 - 14:20 Ferry trip from the mainland of Estonia to Muhu – a tiny island where time rests 15:00 – 16:30 Lunch in a local farmstead Tõnise Majatalo on Muhu island 18:00 Check-in for two nights at Georg Ots SPA Hotel**** in Kuressaare It is the 5th best hotel in Estonia in 2013 according to clients feedback in TripAdvisor 19:20 Departure to a concert in Laurentius church 20:00 Mozart „Requiem“ performed by Estonian Philharmonic Chamber Choir and the Tallinn Chamber Orchestra Wed, July 23/ Eastern part of Saaremaa island fr. 07:00 Breakfast 09:30 Guided walking tour in Kuressaare and in the Bishop Castle of Kuressaare 11:00 Half day tour to an Eastern part of Saaremaa island to explore its unique nature. We visit the organic soaps cottage industry Goodkaarma and take part of a popular soap making workshop there. Next stop is at Kaali field of meteorite craters where we will have lunch The approximate time of Kaali meteorite fall is 7500-7600 years ago. Meteorite fall caused big damages on already inhabited Saaremaa, it could be compared to explosion of atomic bomb. At the height of 5-10 km meteorite fell apart and came down to the ground in pieces the biggest of which created a big crater with diameter of 110 m and depth of 22 m and 8 smaller craters. -

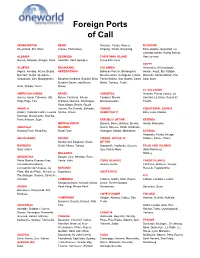

PORTS of CALL WORLDWIDE.Xlsx

Foreign Ports of Call AFGHANISTAN BENIN Shantou, Tianjin, Xiamen, ECUADOR Kheyrabad, Shir Khan Cotnou, Porto-Novo Xingang, Yantai, Zhanjiang Esmeraoldas, Guayaquil, La Libertad, Manta, Puerto Bolivar, ALBANIA BERMUDA CHRISTMAS ISLAND San Lorenzo Durres, Sarande, Shegjin, Vlore Hamilton, Saint George’s Flying Fish Cove EGYPT ALGERIA BOSNIAAND COLOMBIA Alexandria, Al Ghardaqah, Algiers, Annaba, Arzew, Bejaia, HERZEGOVINA Bahia de Portete, Barranquilla, Aswan, Asyut, Bur Safajah, Beni Saf, Dellys, Djendjene, Buenaventura, Cartagena, Leticia, Damietta, Marsa Matruh, Port Ghazaouet, Jijel, Mostaganem, Bosanka Gradiska, Bosakni Brod, Puerto Bolivar, San Andres, Santa Said, Suez Bosanki Samac, and Brcko, Marta, Tumaco, Turbo Oran, Skikda, Tenes Orasje EL SALVADOR AMERICAN SAMOA BRAZIL COMOROS Acajutla, Puerto Cutuco, La Aunu’u, Auasi, Faleosao, Ofu, Belem, Fortaleza, Ikheus, Fomboni, Moroni, Libertad, La Union, Puerto El Pago Pago, Ta’u Imbituba, Manaus, Paranagua, Moutsamoudou Triunfo Porto Alegre, Recife, Rio de ANGOLA Janeiro, Rio Grande, Salvador, CONGO, EQUATORIAL GUINEA Ambriz, Cabinda, Lobito, Luanda Santos, Vitoria DEMOCRATIC Bata, Luba, Malabo Malongo, Mocamedes, Namibe, Porto Amboim, Soyo REPUBLIC OF THE ERITREA BRITISH VIRGIN Banana, Boma, Bukavu, Bumba, Assab, Massawa ANGUILLA ISLANDS Goma, Kalemie, Kindu, Kinshasa, Blowing Point, Road Bay Road Town Kisangani, Matadi, Mbandaka ESTONIA Haapsalu, Kunda, Muuga, ANTIGUAAND BRUNEI CONGO, REPUBLIC Paldiski, Parnu, Tallinn Bandar Seri Begawan, Kuala OF THE BARBUDA Belait, Muara, Tutong -

Leisure in Kuressaare in Leisure

14 Meri Spa Hotel*** (Pargi 16) – Saaremaa’s Meri Spa BILLIARDS ADVENTURE & TEAM GAMES ENG All roads lead to Kuressaare Hotel offers refreshing therapeutic procedures. The ho- 22 Kodulinna Lokaal (Tallinna 11) – Billiards isn’t just 36 360 Kraadi adventure company – Adventure Kuressaare is almost a ritual in itself. If you come to tel has its own gym, sauna and pool with underwater a sport, but an enjoyable game to play while talking to games for those seeking just fun or an extreme expe- Saaremaa, you won’t leave without having visited its massage features. C2 friends or relaxing of an evening. C3 rience. Team games for company events and games seaside capital. You can always be sure of a friendly, Ph +372 452 2100 www.saaremaaspahotels.eu Ph +372 453 1178 www.saaremaa.ee/kodulinn in the nature. laid back reception in the town. Having been here Ph +372 5663 2979 www.360.ee once, you’re sure to make a return visit. Your soul 15 Rüütli Spa Hotel water park (Pargi 12) – This hotel instinctively knows what’s good for it! 23 has a rehabilitative therapy centre, a sauna complex and Vaekoda pub (Tallinna 3) – You can play billiards on 37 Island holidays – Team and orienteering games A pleasantly sleepy town, Kuressaare breathes to a water park with a full-sized swimming pool, children’s the first floor of the pub. C2 using GPS, photo hunts and paintball. its own rhythm, with a faint tang of sea salt in the pool and water attractions. C2 Ph +372 453 3020 www.vaekoda.ee Ph +372 5621 3743 www.saarepuhkus.ee air. -

Integrated Review Service for Radioactive Waste and Spent Fuel Management, Decommissioning and Remediation (Artemis) Mission

INTEGRATED REVIEW SERVICE FOR RADIOACTIVE WASTE AND SPENT FUEL MANAGEMENT, DECOMMISSIONING AND REMEDIATION (ARTEMIS) MISSION TO ESTONIA TALLINN, ESTONIA 24 March to 1 April 2019 DEPARTMENT OF NUCLEAR SAFETY AND SECURITY DEPARTMENT OF NUCLEAR ENERGY REPORT OF THE INTEGRATED REVIEW SERVICE FOR RADIOACTIVE WASTE AND SPENT FUEL MANAGEMENT, DECOMMISSIONING AND REMEDIATION (ARTEMIS) MISSION TO ESTONIA ii REPORT OF THE INTEGRATED REVIEW SERVICE FOR RADIOACTIVE WASTE AND SPENT FUEL MANAGEMENT, DECOMMISSIONING AND REMEDIATION (ARTEMIS) MISSION TO ESTONIA Mission dates: 24 March to 1 April 2019 Location: Tallinn, Estonia Organized by: IAEA ARTEMIS REVIEW TEAM Ms Cherry TWEED ARTEMIS Team Leader (UK) Ms Maria Isabel F. PAIVA Reviewer (Portugal) Mr István LÁZÁR Reviewer (Hungary) Mr Stefan THEIS Reviewer (Switzerland) Mr Andrey GUSKOV IAEA Team Coordinator Mr Jiri FALTEJSEK IAEA Deputy Team Coordinator Ms Kristina NUSSBAUM IAEA Admin. Assistant IAEA-2019 iii The number of recommendations, suggestions and good practices is in no way a measure of the status of the national infrastructure for nuclear and radiation safety. Comparisons of such numbers between ARTEMIS reports from different countries should not be attempted. iv CONTENTS EXECUTIVE SUMMARY ....................................................................................................................... 1 I. INTRODUCTION ............................................................................................................................ 3 II. OBJECTIVE AND SCOPE ............................................................................................................ -

Higher Education Institution Kuressaare College, Tallinn

ASSESSMENT REPORT Higher Education Kuressaare College, Tallinn University of Technology Institution Study programme group Personal Services Study Programme (s) Tourism and Catering Management Prof HE INTRODUCTION The aim of the assessment panel was the evaluation of the following professional higher education study programmes of the Personal Services study programme group: Estonian School of Hotel and Tourism Management Hotel Management Estonian School of Hotel and Tourism Management Tour Operation Estonian School of Hotel and Tourism Management Catering Management Tallinn University of Technology, Kuressaare College Tourism and Catering Management University of Tartu, Pärnu College Tourism and Hotel Management The evaluation looked at each of the study programmes separately, but also at their similarities and differences. The following persons formed the assessment panel: Prof Peter Mason, Department of Marketing, Tourism and Hospitality, Faculty of Business, Bedfordshire University, UK - chairman Dr Rong Huang, Plymouth School of Tourism and Hospitality, UK Associate Prof Remigijus Kinderis, Klaipeda State College, Lithuania Feliks Mägus, Nordic Hotels OÜ, Chairman of the Management Board, General Manager of Nordic Hotel Forum, Estonia Rasmus Kuusemets, Lääne-Viru Rakenduskõrgkool, student, Estonia After the preparation phase, the work of the assessment panel in Estonia started on Monday 24th November 2014 with an introduction to the Higher Education System as well as the assessment procedure by EKKA, the Estonian Quality assurance organisation for higher education. The members of the panel agreed the overall questions and areas to discuss with each group at the three institutions, which were part of the assessment process. The distribution of tasks between the members of the assessment panel was then organised and the concrete schedule of the site visits agreed. -

Saare Maakonna Arengustrateegia 2019-2030 LISA 1 Hetkeolukorra Analüüs Tegevusvaldkondade Lõikes

Saare maakonna arengustrateegia 2019-2030 LISA 1 Hetkeolukorra analüüs tegevusvaldkondade lõikes Majanduskeskkond • Eesti majanduse ülevaade Rahandusministeeriumi 2018. aasta kevadise majandusprognoosi kohaselt kasvas Eesti majandus 2017. aasta viimases kvartalis kiiresti ehk 5% aasta ja 2,2% kvartali arvestuses. SKP reaalakasv 2017. aasta kokkuvõttes ületas prognoositut ning ulatus 4,9%-ni ja nominaalne kasv 9%-ni. Majanduskasv põhines peamiselt sisenõudlusel, kuid jätkus ka ekspordi kasv. Tegevusalades toodetud lisandväärtuse kasv kiirenes 2016. aasta 1,5%-lt 5,6%-ni, peamisteks vedajateks olid ehitus ja valdavalt sisetarbimisele suunatud teenindusharud, nagu info ja side ning kutse- ja tehnikalane tegevus, mis tagasid kokku üle poole kogu lisandväärtuse juurdekasvust. OECD ennustab Eesti majandusele aeglast kasvu: 2018. aastal 3,7% ja 2019. aastal 3,2%, kuna tööjõud väheneb. Eratarbimine suureneb tänu üksikisiku tulumaksu vähenemisele ja palgakasvule. Euroala paranenud majanduskasv stimuleerib eksporti ja seda vaatamata tööjõu kallinemisele. Rahandusministeeriumi prognoosi kohaselt jääb majanduskasv ka 2018. aastal tugevaks (4%), kuid 2019–2020 on oodata majanduskasvu aeglustumist. Majanduskasvu peaks nendel aastatel toetama töötlev tööstus ja ekspordile orienteeritud teenindusvaldkonnad. Tugev nõudlus toob kaasa investeerimisaktiivsuse ja tarbimisvõime suuremise, mis avaldub kaubanduse, ehituse ja teiste peamiselt sisenõudlusest sõltuvate valdkondade kasvus. Töötleva tööstuse toodang võib välis- ja sisenõudluse toel suureneda 2018. -

1941 EXECUTIONS in KURESSAARE CASTLE the Following Article Appeared in the Local Newspaper of Saaremaa

1941 EXECUTIONS IN KURESSAARE CASTLE The following article appeared in the local newspaper of Saaremaa “Saarte Hääl” (“Voice of the Islands”) on Sept. 13, 1988. As explained below, the old historical Kuressaare castle was used as a jail and execution site during the Soviet years. May the Sorrow of Their Suffering, Their Anguish and Their Agony Stay Forever in our Souls To this ancient castle...to the keeper of our history, people come alone, in groups, on excursion. We shriek on her walls as children, walk by them as lovers when we are young, and sit to rest on them in our twilight years. In the castle yard we have held festivals, some for just our islanders and some for all of Estonia. Until now, the merriment of our song and dance festivals have overshadowed the past and present significance of this old castle-fort. During these joyous moments we don't need to remember that the grief of the past, the anguish and pain of our forefathers lie beneath our celebrations. The passage of centuries allows us to rationalize some events into nonexistence or at least into incredibility. But what if the anguish and pain are not relics from past centuries? What if they are separated from us by no more than one generation? Would that knowledge cast a dismal shadow over our castle with its courtyard and walls, making them something to hate, or would it cause us to view them with greater tenderness, as something to cherish? For nearly half a century, most of us have been unaware that such a page of history even exists.