2020 Instructions for Form 8915-E

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ffontiau Cymraeg

This publication is available in other languages and formats on request. Mae'r cyhoeddiad hwn ar gael mewn ieithoedd a fformatau eraill ar gais. [email protected] www.caerphilly.gov.uk/equalities How to type Accented Characters This guidance document has been produced to provide practical help when typing letters or circulars, or when designing posters or flyers so that getting accents on various letters when typing is made easier. The guide should be used alongside the Council’s Guidance on Equalities in Designing and Printing. Please note this is for PCs only and will not work on Macs. Firstly, on your keyboard make sure the Num Lock is switched on, or the codes shown in this document won’t work (this button is found above the numeric keypad on the right of your keyboard). By pressing the ALT key (to the left of the space bar), holding it down and then entering a certain sequence of numbers on the numeric keypad, it's very easy to get almost any accented character you want. For example, to get the letter “ô”, press and hold the ALT key, type in the code 0 2 4 4, then release the ALT key. The number sequences shown from page 3 onwards work in most fonts in order to get an accent over “a, e, i, o, u”, the vowels in the English alphabet. In other languages, for example in French, the letter "c" can be accented and in Spanish, "n" can be accented too. Many other languages have accents on consonants as well as vowels. -

Form IT-2658-E:12/19:Certificate of Exemption from Partnership Or New

Department of Taxation and Finance IT-2658-E Certificate of Exemption from Partnership (12/19) or New York S Corporation Estimated Tax Paid on Behalf of Nonresident Individual Partners and Shareholders Do not send this certificate to the Tax Department (see instructions below). Use this certificate for tax years 2020 and 2021; it will expire on February 1, 2022. First name and middle initial Last name Social Security number Mailing address (number and street or PO box) Telephone number ( ) City, village, or post office State ZIP code I certify that I will comply with the New York State estimated tax provisions and tax return filing requirements, to the extent that they apply to me, for tax years 2020 and 2021 (see instructions). Signature of nonresident individual partner or shareholder Date Instructions General information If you do not meet either of the above exceptions, you may still claim exemption from this estimated tax provision by Tax Law section 658(c)(4) requires the following entities filing Form IT-2658-E. that have income derived from New York sources to make estimated personal income tax payments on behalf of You qualify to claim exemption and file Form IT-2658-E by partners or shareholders who are nonresident individuals: certifying that you will comply in your individual capacity with • New York S corporations; all the New York State personal income tax and MCTMT estimated tax and tax return filing requirements, to the • partnerships (other than publicly traded partnerships as extent that they apply to you, for the years covered by this defined in Internal Revenue Code section 7704); and certificate. -

Left Ventricular Diastolic Dysfunction in Ischemic Stroke: Functional and Vascular Outcomes

Journal of Stroke 2016;18(2):195-202 http://dx.doi.org/10.5853/jos.2015.01669 Original Article Left Ventricular Diastolic Dysfunction in Ischemic Stroke: Functional and Vascular Outcomes Hong-Kyun Park,a* Beom Joon Kim,a* Chang-Hwan Yoon,b Mi Hwa Yang,a Moon-Ku Han,a Hee-Joon Baea aDepartment of Neurology and Cerebrovascular Center, Seoul National University Bundang Hospital, Seongnam, Korea bDivision of Cardiology, Department of Internal Medicine, Seoul National University Bundang Hospital, Seongnam, Korea Background and Purpose Left ventricular (LV) diastolic dysfunction, developed in relation to myo- Correspondence: Moon-Ku Han cardial dysfunction and remodeling, is documented in 15%-25% of the population. However, its role Department of Neurology and Cerebrovascular Center, Seoul National in functional recovery and recurrent vascular events after acute ischemic stroke has not been thor- University Bundang Hospital, oughly investigated. 82 Gumi-ro 173beon-gil, Bundang-gu, Seongnam 13620, Korea Methods In this retrospective observational study, we identified 2,827 ischemic stroke cases with Tel: +82-31-787-7464 adequate echocardiographic evaluations to assess LV diastolic dysfunction within 1 month after the Fax: +82-31-787-4059 index stroke. The peak transmitral filling velocity/mean mitral annular velocity during early diastole (E/ E-mail: [email protected] e’) was used to estimate LV diastolic dysfunction. We divided patients into 3 groups according to E/e’ Received: December 1, 2015 as follows: <8, 8-15, and ≥15. Recurrent vascular events and functional recovery were prospectively Revised: March 14, 2016 collected at 3 months and 1 year. Accepted: March 21, 2016 Results Among included patients, E/e’ was 10.6±6.4: E/e’ <8 in 993 (35%), 8-15 in 1,444 (51%), and *These authors contributed equally to this ≥15 in 378 (13%) cases. -

Typing in Greek Sarah Abowitz Smith College Classics Department

Typing in Greek Sarah Abowitz Smith College Classics Department Windows 1. Down at the lower right corner of the screen, click the letters ENG, then select Language Preferences in the pop-up menu. If these letters are not present at the lower right corner of the screen, open Settings, click on Time & Language, then select Region & Language in the sidebar to get to the proper screen for step 2. 2. When this window opens, check if Ελληνικά/Greek is in the list of keyboards on your computer under Languages. If so, go to step 3. Otherwise, click Add A New Language. Clicking Add A New Language will take you to this window. Look for Ελληνικά/Greek and click it. When you click Ελληνικά/Greek, the language will be added and you will return to the previous screen. 3. Now that Ελληνικά is listed in your computer’s languages, click it and then click Options. 4. Click Add A Keyboard and add the Greek Polytonic option. If you started this tutorial without the pictured keyboard menu in step 1, it should be in the lower right corner of your screen now. 5. To start typing in Greek, click the letters ENG next to the clock in the lower right corner of the screen. Choose “Greek Polytonic keyboard” to start typing in greek, and click “US keyboard” again to go back to English. Mac 1. Click the apple button in the top left corner of your screen. From the drop-down menu, choose System Preferences. When the window below appears, click the “Keyboard” icon. -

Kevin E. O'malley

KEVIN E. O’MALLEY Shareholder Gallagher & Kennedy 2575 E. Camelback Road, Suite 1100 Phoenix, AZ 85016 DIR: 602-530-8430 [email protected] My Practice INSURANCE - Coverage Analysis and Litigation for Insurance Companies, Insurance Disputes, Insurance for Individuals and Businesses PUBLIC BIDDING & PROCUREMENT - Business Law and Transactions, Claims, Disputes and Litigation, Compliance, Construction, Contract Negotiations, Government Affairs and Lobbying, Government Bid and Proposal Preparation and Submission, Intellectual Property ADMINISTRATIVE LAW - Public Bidding and Procurement Administrative Compliance PROFESSIONAL LIABILITY LITIGATION - Civil Defense Litigation, Class Actions, PB&P Claims, Disputes and Litigation, Real Estate Litigation CONSTRUCTION - Construction Litigation, Construction Public Bidding and Procurement PROFESSIONAL SUMMARY Kevin heads Gallagher & Kennedy’s litigation and public bidding and procurement departments. Keenly attuned to the needs of his wide array of clients, Kevin offers proven skill in developing strategy and implementing solutions that are singularly focused on each client’s often unique and/or specific goals. Over his 30-year career representing public and private companies across a wide range of industries, Kevin’s litigation skills have been honed to a razor’s edge. Notably, Kevin’s civil litigation experience is extensive and far reaching, both in and out of the courtroom. Kevin has managed many high profile and complex matters, including securities, commercial, environmental, governmental, construction, professional liability and insurance litigation cases. He offers significant class action and appellate experience. A veteran litigator and talented negotiator with a seemingly natural aptitude for advocacy and unwavering drive to win, Kevin is appreciated for his strategic, tactical and streamlined arguments and for his ability to transform client positions into compelling and easily understood talking points. -

I/B/E/S DETAIL HISTORY a Guide to the Analyst-By-Analyst Historical Earnings Estimate Database

I/B/E/S DETAIL HISTORY A guide to the analyst-by-analyst historical earnings estimate database U.S. Edition CONTENTS page Overview..................................................................................................................................................................................................................1 File Explanations ..............................................................................................................................................................................................2 Detail File ..................................................................................................................................................................................................2 Identifier File..........................................................................................................................................................................................3 Adjustments File..................................................................................................................................................................................3 Excluded Estimates File ...............................................................................................................................................................3 Broker Translations...........................................................................................................................................................................4 S/I/G Codes..............................................................................................................................................................................................4 -

Alphabets, Letters and Diacritics in European Languages (As They Appear in Geography)

1 Vigleik Leira (Norway): [email protected] Alphabets, Letters and Diacritics in European Languages (as they appear in Geography) To the best of my knowledge English seems to be the only language which makes use of a "clean" Latin alphabet, i.d. there is no use of diacritics or special letters of any kind. All the other languages based on Latin letters employ, to a larger or lesser degree, some diacritics and/or some special letters. The survey below is purely literal. It has nothing to say on the pronunciation of the different letters. Information on the phonetic/phonemic values of the graphic entities must be sought elsewhere, in language specific descriptions. The 26 letters a, b, c, d, e, f, g, h, i, j, k, l, m, n, o, p, q, r, s, t, u, v, w, x, y, z may be considered the standard European alphabet. In this article the word diacritic is used with this meaning: any sign placed above, through or below a standard letter (among the 26 given above); disregarding the cases where the resulting letter (e.g. å in Norwegian) is considered an ordinary letter in the alphabet of the language where it is used. Albanian The alphabet (36 letters): a, b, c, ç, d, dh, e, ë, f, g, gj, h, i, j, k, l, ll, m, n, nj, o, p, q, r, rr, s, sh, t, th, u, v, x, xh, y, z, zh. Missing standard letter: w. Letters with diacritics: ç, ë. Sequences treated as one letter: dh, gj, ll, rr, sh, th, xh, zh. -

List of Approved Special Characters

List of Approved Special Characters The following list represents the Graduate Division's approved character list for display of dissertation titles in the Hooding Booklet. Please note these characters will not display when your dissertation is published on ProQuest's site. To insert a special character, simply hold the ALT key on your keyboard and enter in the corresponding code. This is only for entering in a special character for your title or your name. The abstract section has different requirements. See abstract for more details. Special Character Alt+ Description 0032 Space ! 0033 Exclamation mark '" 0034 Double quotes (or speech marks) # 0035 Number $ 0036 Dollar % 0037 Procenttecken & 0038 Ampersand '' 0039 Single quote ( 0040 Open parenthesis (or open bracket) ) 0041 Close parenthesis (or close bracket) * 0042 Asterisk + 0043 Plus , 0044 Comma ‐ 0045 Hyphen . 0046 Period, dot or full stop / 0047 Slash or divide 0 0048 Zero 1 0049 One 2 0050 Two 3 0051 Three 4 0052 Four 5 0053 Five 6 0054 Six 7 0055 Seven 8 0056 Eight 9 0057 Nine : 0058 Colon ; 0059 Semicolon < 0060 Less than (or open angled bracket) = 0061 Equals > 0062 Greater than (or close angled bracket) ? 0063 Question mark @ 0064 At symbol A 0065 Uppercase A B 0066 Uppercase B C 0067 Uppercase C D 0068 Uppercase D E 0069 Uppercase E List of Approved Special Characters F 0070 Uppercase F G 0071 Uppercase G H 0072 Uppercase H I 0073 Uppercase I J 0074 Uppercase J K 0075 Uppercase K L 0076 Uppercase L M 0077 Uppercase M N 0078 Uppercase N O 0079 Uppercase O P 0080 Uppercase -

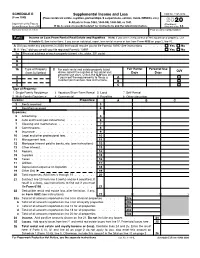

2020 Schedule E (Form 1040) 2020 Attachment Sequence No

SCHEDULE E Supplemental Income and Loss OMB No. 1545-0074 (Form 1040) (From rental real estate, royalties, partnerships, S corporations, estates, trusts, REMICs, etc.) ▶ Attach to Form 1040, 1040-SR, 1040-NR, or 1041. 2020 Department of the Treasury Attachment Internal Revenue Service (99) ▶ Go to www.irs.gov/ScheduleE for instructions and the latest information. Sequence No. 13 Name(s) shown on return Your social security number Part I Income or Loss From Rental Real Estate and Royalties Note: If you are in the business of renting personal property, use Schedule C. See instructions. If you are an individual, report farm rental income or loss from Form 4835 on page 2, line 40. A Did you make any payments in 2020 that would require you to file Form(s) 1099? See instructions . Yes No B If “Yes,” did you or will you file required Form(s) 1099? . Yes No 1a Physical address of each property (street, city, state, ZIP code) A B C 1b Type of Property 2 Fair Rental Personal Use For each rental real estate property listed QJV (from list below) above, report the number of fair rental and Days Days personal use days. Check the QJV box only A if you meet the requirements to file as a A B qualified joint venture. See instructions. B C C Type of Property: 1 Single Family Residence 3 Vacation/Short-Term Rental 5 Land 7 Self-Rental 2 Multi-Family Residence 4 Commercial 6 Royalties 8 Other (describe) Income: Properties: A B C 3 Rents received . 3 4 Royalties received . -

Proposal for Generation Panel for Latin Script Label Generation Ruleset for the Root Zone

Generation Panel for Latin Script Label Generation Ruleset for the Root Zone Proposal for Generation Panel for Latin Script Label Generation Ruleset for the Root Zone Table of Contents 1. General Information 2 1.1 Use of Latin Script characters in domain names 3 1.2 Target Script for the Proposed Generation Panel 4 1.2.1 Diacritics 5 1.3 Countries with significant user communities using Latin script 6 2. Proposed Initial Composition of the Panel and Relationship with Past Work or Working Groups 7 3. Work Plan 13 3.1 Suggested Timeline with Significant Milestones 13 3.2 Sources for funding travel and logistics 16 3.3 Need for ICANN provided advisors 17 4. References 17 1 Generation Panel for Latin Script Label Generation Ruleset for the Root Zone 1. General Information The Latin script1 or Roman script is a major writing system of the world today, and the most widely used in terms of number of languages and number of speakers, with circa 70% of the world’s readers and writers making use of this script2 (Wikipedia). Historically, it is derived from the Greek alphabet, as is the Cyrillic script. The Greek alphabet is in turn derived from the Phoenician alphabet which dates to the mid-11th century BC and is itself based on older scripts. This explains why Latin, Cyrillic and Greek share some letters, which may become relevant to the ruleset in the form of cross-script variants. The Latin alphabet itself originated in Italy in the 7th Century BC. The original alphabet contained 21 upper case only letters: A, B, C, D, E, F, Z, H, I, K, L, M, N, O, P, Q, R, S, T, V and X. -

ALPHABET and PRONUNCIATION Old English (OE) Scribes Used Two

OLD ENGLISH (OE) ALPHABET AND PRONUNCIATION Old English (OE) scribes used two kinds of letters: the runes and the letters of the Latin alphabet. The bulk of the OE material — OE manuscripts — is written in the Latin script. The use of Latin letters in English differed in some points from their use in Latin, for the scribes made certain modifications and additions in order to indicate OE sounds which did not exist in Latin. Depending of the size and shape of the letters modern philologists distinguish between several scripts which superseded one another during the Middle Ages. Throughout the Roman period and in the Early Middle Ages capitals (scriptura catipalis) and uncial (scriptura uncialis) letters were used; in the 5th—7th c. the uncial became smaller and the cursive script began to replace it in everyday life, while in book-making a still smaller script, minuscule (scriptura minusculis), was employed. The variety used in Britain is known as the Irish, or insular minuscule. Insular minuscule script differed from the continental minuscule in the shape of some letters, namely d, f, g. From these letters only one is used in modern publications of OE texts as a distinctive feature of the OE alphabet – the letter Z (corresponding to the continental g). In the OE variety of the Latin alphabet i and j were not distinguished; nor were u and v; the letters k, q, x and w were not used until many years later. A new letter was devised by putting a stroke through d or ð, to indicate the voiceless and the voiced interdental [θ] and [ð]. -

Euler's Formula: 1 Powers of E: First Pass

Euler’s Formula: The purpose of these notes is to explain Euler’s famous formula eiθ = cos(θ)+ i sin(θ). (1) 1 Powers of e: First Pass Euler’s equation is complicated because it involves raising a number to an imaginary power. Let’s build up to this slowly. Integer Powers: It’s pretty clear that e2 = e e and e3 = e e e, × × × and so on. For any positive integer p, we have ep = e ... e, a total of p times. For negative integers, the definition is also pretty× clear.× For instance e−2 =1/(e e) and e−3 =1/(e e e). And so on. × × × Fractional Powers: How would you define e2/3. This really means the cube root of e e. So e2/3 is the number y such that y y y = e e. Using this system, it× is pretty clear that you can make good sense× × of ep/q×where p/q is any positive fraction. You can make sense of negative fractions using the formula e−p/q =1/ep/q. Real Powers: If a is a positive real number, then you could define ea to pn/qn be the limit of expressions of the form e , where pn/qn is a sequence of rational numbers converging to a. To give an example of what I’m talking about, let a = √2. 17/12 is close to √2 and e17/12 =4.1233529... • 41/29 is closer to √2 and e41/29 =4.111521... • 577/408 is closer to √2 and e577/408 =4.113259 • 1393/985 is closer to √2 and e1393/985 =4.1132488.