Testing Feasibility of Measuring Market Risk by Predicted Beta with Liquidity Adjustment1

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Specialised Asset Management

specialised research and investment group Russian Power: The Greatest Sector Reform on Earth www.sprin-g.com November 2010 specialised research and investment group Specialised Research and Investment Group (SPRING) Manage Investments in Russian Utilities: - HH Generation - #1 among EM funds (12 Months Return)* #2 among EM funds (Monthly return)** David Herne - Portfolio Manager Previous positions: Member, Board of Directors - Unified Energy Systems, Federal Grid Company, RusHydro, TGK-1, TGK-2, TGK-4, OGK-3, OGK-5, System Operator, Aeroflot, etc. (2000-2008) Chairman, Committee for Strategy and Reform - Unified Energy Systems (2001-2008) Boston Consulting Group, Credit Suisse First Boston, Brunswick. * Top 10 (by 12 Months Return) Emerging Markets (E. Europe/CIS) funds in the world by BarclayHedge as of 30 September 2010 ** Top 10 (by Monthly Return) Emerging Markets (E. Europe/CIS) funds in the world by BarclayHedge as of 31 August 2010 2 specialised research and investment group Russian power sector reform: Privatization Pre-Reform Post-Reform Government Government 52% 1 RusHydro 1 FSK RAO ES RAO UES 58% 79% hydro generation HV distribution 53% Far East Holding control control Independent energos 53% 1 MRSK Holding 14 TGKs 0% (Bashkir, Novosibirsk, ~72 energos 0% generation (CHP) generation Irkutsk, Tat) 35 federal plants transmission thermal 11 MRSK distribution 51% hydro LV distribution 0% ~72 SupplyCos supply 6 OGKs other 0% generation 45% InterRAO 0% ~100 RepairCos Source: UES, Companies Data, SPRING research 3 specialised research -

Russian Withholding Tax Refund

Russian withholding tax refund Tax & Legal If you or your clients invested in Russian securities and are entitled to a substantial dividend or interest income, there is a chance that you overpaid your taxes and may qualify for a tax refund © 2018 Deloitte Consulting LLC Background Investors may apply a According to the The Russian The tax refund reduced tax rate for Russian tax withholding tax rate is practice in Russia is their interest and/or authorities, they are set at 15% on not well-developed: dividend income, ready to reimburse dividends and 20 the tax legislation depending on the overpaid taxes, if a percent on interest. does not provide for a conditions set by the full package of Effective from 1 specific list of Russian Tax Code or documents confirming January 2014, the documents to be applicable Double Tax the income payment duties of the tax collected and Treaties. Calculations chain and the agent for WHT requirements to be of a standard Russian investor’s rights to purposes were met. For these rate or the standard the income is transferred to the reasons, the process reduced Double Tax submitted. local Russian can be lengthy and Treaty rate, as well as custodian or, in a sometimes fruitless. submission of claims limited number of However, the trend is on tax can be cases, to the reassuring: the refunded, should be fiduciary, broker or number of successful made by investors issuer. refund claims and themselves within positive court three calendar years, decisions is growing. following the year in which it was withheld. -

a Leading Energy Company in the Nordic Area

- a leading energy company in the Nordic area Presentation for investors September 2007 Disclaimer This presentation does not constitute an invitation to underwrite, subscribe for, or otherwise acquire or dispose of any Fortum shares. Past performance is no guide to future performance, and persons needing advice should consult an independent financial adviser. 2 • Fortum today • European power markets • Russia • Financials / outlook • Supplementary material 3 Fortum's strategy Fortum focuses on the Nordic and Baltic Rim markets as a platform for profitable growth Become the leading Become the power and heat energy supplier company of choice Benchmark business performance 4 Presence in focus market areas Nordic Generation 53.2 TWh Electricity sales 60.2 TWh Distribution cust. 1.6 mill. Electricity cust. 1.3 mill. NW Russia Heat sales 20.1 TWh (in associated companies) Power generation ~6 TWh Heat production ~7 TWh Baltic countries Heat sales 1.0 TWh Poland Distribution cust. 23,000 Heat sales 3.6 TWh Electricity sales 8 GWh 2006 numbers 5 Fortum Business structure Fortum Markets Fortum's comparable Large operating profit in 2006 NordicNordic customers EUR 1,437 million Fortum wholesalewholesale Small Power marketmarket customers Generation Nord Pool and Markets 0% bilateral Other retail companies Deregulated Distribution 17% Regulated Transmission Power and system Fortum Heat 17% Generation services Distribution 66% 6 Strong financial position ROE (%) EPS, cont. (EUR) Total assets (EUR billion) 20 1.50 1.42 20.0 16.8 17.5 17.3 1.22 18 15.1 -

Emerging Index - QSR

2 FTSE Russell Publications 19 August 2021 FTSE RAFI Emerging Index - QSR Indicative Index Weight Data as at Closing on 30 June 2021 Index Index Index Constituent Country Constituent Country Constituent Country weight (%) weight (%) weight (%) Absa Group Limited 0.29 SOUTH BRF S.A. 0.21 BRAZIL China Taiping Insurance Holdings (Red 0.16 CHINA AFRICA BTG Pactual Participations UNT11 0.09 BRAZIL Chip) Acer 0.07 TAIWAN BYD (A) (SC SZ) 0.03 CHINA China Tower (H) 0.17 CHINA Adaro Energy PT 0.04 INDONESIA BYD (H) 0.12 CHINA China Vanke (A) (SC SZ) 0.09 CHINA ADVANCED INFO SERVICE 0.16 THAILAND Canadian Solar (N Shares) 0.08 CHINA China Vanke (H) 0.2 CHINA Aeroflot Russian Airlines 0.09 RUSSIA Capitec Bank Hldgs Ltd 0.05 SOUTH Chongqing Rural Commercial Bank (A) (SC 0.01 CHINA Agile Group Holdings (P Chip) 0.04 CHINA AFRICA SH) Agricultural Bank of China (A) (SC SH) 0.27 CHINA Catcher Technology 0.2 TAIWAN Chongqing Rural Commercial Bank (H) 0.04 CHINA Agricultural Bank of China (H) 0.66 CHINA Cathay Financial Holding 0.29 TAIWAN Chunghwa Telecom 0.32 TAIWAN Air China (A) (SC SH) 0.02 CHINA CCR SA 0.14 BRAZIL Cia Paranaense de Energia 0.01 BRAZIL Air China (H) 0.06 CHINA Cemex Sa Cpo Line 0.7 MEXICO Cia Paranaense de Energia (B) 0.07 BRAZIL Airports of Thailand 0.04 THAILAND Cemig ON 0.03 BRAZIL Cielo SA 0.13 BRAZIL Akbank 0.18 TURKEY Cemig PN 0.18 BRAZIL CIFI Holdings (Group) (P Chip) 0.03 CHINA Al Rajhi Banking & Investment Corp 0.52 SAUDI Cencosud 0.04 CHILE CIMB Group Holdings 0.11 MALAYSIA ARABIA Centrais Eletricas Brasileiras S.A. -

US Sanctions on Russia

U.S. Sanctions on Russia Updated January 17, 2020 Congressional Research Service https://crsreports.congress.gov R45415 SUMMARY R45415 U.S. Sanctions on Russia January 17, 2020 Sanctions are a central element of U.S. policy to counter and deter malign Russian behavior. The United States has imposed sanctions on Russia mainly in response to Russia’s 2014 invasion of Cory Welt, Coordinator Ukraine, to reverse and deter further Russian aggression in Ukraine, and to deter Russian Specialist in European aggression against other countries. The United States also has imposed sanctions on Russia in Affairs response to (and to deter) election interference and other malicious cyber-enabled activities, human rights abuses, the use of a chemical weapon, weapons proliferation, illicit trade with North Korea, and support to Syria and Venezuela. Most Members of Congress support a robust Kristin Archick Specialist in European use of sanctions amid concerns about Russia’s international behavior and geostrategic intentions. Affairs Sanctions related to Russia’s invasion of Ukraine are based mainly on four executive orders (EOs) that President Obama issued in 2014. That year, Congress also passed and President Rebecca M. Nelson Obama signed into law two acts establishing sanctions in response to Russia’s invasion of Specialist in International Ukraine: the Support for the Sovereignty, Integrity, Democracy, and Economic Stability of Trade and Finance Ukraine Act of 2014 (SSIDES; P.L. 113-95/H.R. 4152) and the Ukraine Freedom Support Act of 2014 (UFSA; P.L. 113-272/H.R. 5859). Dianne E. Rennack Specialist in Foreign Policy In 2017, Congress passed and President Trump signed into law the Countering Russian Influence Legislation in Europe and Eurasia Act of 2017 (CRIEEA; P.L. -

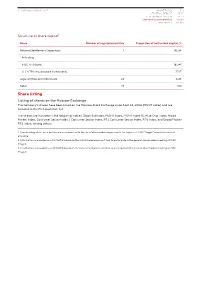

Share Listing

Annual Report 2018 | MAGNIT MAGNIT TODAY 3-11 99 STRATEGIC REPORT 13-27 PERFORMANCE REVIEW 29-53 CORPORATE GOVERNANCE 55-113 APPENDICES 115-189 Structure of share capital1 Name Number of registered entities Proportion of authorized capital, % National Settlement Depositary 1 95.54 Including: PJSC VTB Bank 18.342 LLC VTB Infrastructure Investments 7.723 Legal entities and individuals 24 4.46 Total: 25 100 Share listing Listing of shares on the Moscow Exchange The Company’s shares have been listed on the Moscow Stock Exchange since April 24, 2006 (MGNT ticker) and are included in the first quotation list. The shares are included in the following indices: Stock Subindex, MOEX Index, MOEX Index 10, Blue Chip Index, Broad Market Index, Consumer Sector Index / Consumer Sector Index, RTS Consumer Sector Index, RTS Index, and Broad Market RTS Index, among others. 1. Shareholding structure is provided in accordance with the list of shareholders registered in the register of PJSC “Magnit” shareholders as of 31.12.2018 2. Information is provided as of 12.11.2018 based on the list of shareholders entitled to participate in the general shareholders meeting of PJSC “Magnit 3. Information is provided as of 12.11.2018 based on the list of shareholders entitled to participate in the general shareholders meeting of PJSC “Magnit 100 101 Weight of shares in indices Ticker Index name Weight in index, % RDXUSD Russian Depositary Index USD 2.85 RDX Russian Depositary Index EUR 2.85 NU137529 MSCI EM IMI (VRS Taxes) Net Return USD Index 0.09 RIOB FTSE Russia IOB -

Dmitri V. Kovalenko

Dmitri V. Kovalenko Partner, Moscow Mergers and Acquisitions; Private Equity; Capital Markets Dmitri Kovalenko is co-head of the Moscow office and represents international and Russian clients on a broad range of mergers and acquisitions, private equity and joint venture transac- tions in Russia and other countries covering various industries and sectors. Mr. Kovalenko has practiced law in Skadden’s Moscow, Chicago and Paris offices since 1994. He is ranked in the top tier for Russia M&A and Russia capital markets work by Chambers Global and Chambers Europe, as well as for private equity in Russia by Chambers Europe. Mr. Kovalenko also was named as the 2021 Mergers and Acquisitions Lawyer of the Year and the 2020 Capital Markets Lawyer of the Year by The Best Lawyers in Russia, and was listed in the publication’s Global Business Edition. Additionally, he is listed as a leading individual in IFLR1000 and Who’s Who Legal, as well as repeatedly in The Legal 500 EMEA as a member of its Commercial, Corporate and M&A: Moscow Hall of Fame. T: 7.495.797.4600 F: 7.495.797.4601 His M&A and private equity experience has included advising: [email protected] - Mercury Retail Group in its US$1.2 billion sale of JSC Dixy Group to PJSC Magnit; - Horvik Limited in relation to its preconditional mandatory offer to acquire Trans-Siberian Gold Education plc, an AIM-quoted gold producer; LL.M. (with honors), Northwestern - Kismet Acquisition One, a special purpose acquisition company, in its US$1.9 billion initial University School of Law, Chicago, merger with Nexters Global Limited, the first-ever de-SPAC transaction involving a Russian USA, 1996 company. -

2017 Annual Report of PJSC Inter RAO / Report on Sustainable Development and Environmental Responsibility

INFORMATION TRANSLATION Draft 2017 Annual Report of PJSC Inter RAO / Report on Sustainable Development and Environmental Responsibility Chairman of the Management Board Boris Kovalchuk Chief Accountant Alla Vainilavichute Contents 1. Strategic Report ...................................................................................................................................................................................... 8 1.1. At a Glance .................................................................................................................................................................................. 8 1.2. About the Report ........................................................................................................................................................................ 11 Differences from the Development Process of the 2016 Report ............................................................................................................ 11 Scope of Information ............................................................................................................................................................................. 11 Responsibility for the Report Preparation .............................................................................................................................................. 11 Statement on Liability Limitations ......................................................................................................................................................... -

Public Joint-Stock Company Issuer’S Code: 10214-A

QUARTERLY REPORT "Interregional Distribution Grid Company of Centre", Public Joint-Stock Company Issuer’s code: 10214-A for Quarter 1, 2016 Location of the issuer: 2nd Yamskaya, 4, Moscow, Russian Federation, 127018 The information containing in this quarterly report is subject to disclosure in accordance with the legislation of the Russian Federation on securities ____________ O.Y. Isaev General Director signature Date: 13 May 2016 Chief Accountant - Head of Financial and Tax Accounting and ____________ L.A. Sklyarova signature Reporting Department Date: 13 May 2016 Contact person: Principal Specialist of Corporate Office of the Department for Corporate Governance and Interaction with Shareholders, Yulia Dmitrievna Naumova Phone: (495) 747-9292 #3286 Fax: (495) 747-9295 E-mail: [email protected] Internet site used by the issuer for the information disclosure, containing in this quarterly report: http://www.e-disclosure.ru/portal/company.aspx?id=7985; http://www.mrsk-1.ru/ru/information/. 1 Table of contents Table of contents .............................................................................................................................................. 2 Introduction ...................................................................................................................................................... 5 Section I. Data on bank accounts, on the auditor, appraiser and financial adviser of the issuer, and also persons, who signed the quarterly report ........................................................................................................................ -

Annual Report 2018 ABOUT THIS REPORT 02

AnnuAl RepoRt 2018 ABOUT THIS REPORT 02 1 / 2 ABOUT THIS REPORT Approach to the Report Boundaries of the Report Approval of the Report This Annual Report of Sberbank of Russia ¹ for 2018 (the “Report”) The financial data are presented in the Report Information on sustainable development is consoli- This Report received preliminary approv- in accordance with the IFRS consolidated financial dated by the major participants of the Group, which al by the Supervisory Board of Sberbank includes the performance results of Sberbank and its subsidiaries ² statements, unless otherwise specified in the text of have a significant impact on their regions of pres- (Minutes No. 11 of April 16, 2019). for the reporting period from January 1, 2018, to December 31, 2018. the Report. ence, and Sberbank Corporate University. The reliability of the data in the Report was con- Operational data are presented for PJSC Sberbank firmed by the Audit Committee of Sberbank. unless otherwise specified in the text of the Report. The Report has been prepared in accordance with In addition, the contents of the Report The Report was approved by the Annual General the legislation of the Russian Federation, including: comply with the following documents: Shareholder Meeting of Sberbank as of May 24, 2019 (Minutes No 32 as of May 29, 2019). ♦ Federal Law No. 39-FZ “On the Securities ♦ Requirements of the Moscow Stock The term “Group” as used in the sections “People: Nurturing New Skills in Effective Teams” Market” dated April 22,1996; Exchange on the preparation of annu- and “Impact on Society” includes Sberbank Corporate University and the following: al reports by joint stock companies; ♦ Federal Law No. -

Identifying Russia's Structural Leaders

June 7, 2011 GS SUSTAIN Equity Research Identifying Russia’s structural leaders Identifying long-term winners with SUSTAIN Russia Structural Leaders List We have applied the GS SUSTAIN framework to We have identified eight companies that have RUSSIA STRUCTURAL LEADERS 75 companies across our Russian coverage to delivered and in our view will continue to deliver y identify those well positioned to deliver long-term industry leading cash returns: Mechel, EDCL, Company Sector quality quartile position quartile Management CROCI CROCI average 2011- % 13E, CROCI change 2006-10, % quartile CROCI outperformance through sustained high cash Alliance Oil, Rosneft and Novatek in the natural Novatek Energy 32.1% 0.3% 1 1 1 Oil Serv & Pipe Eurasia Drilling Co 28.2% -2.1% 2 1 1 returns. The framework combines forecast cash resources space and Magnit, Cherkizovo and M- producers Mechel Steel 21.9% -0.6% 2 1 1 returns with objective measures of industry Video in the consumer segment. Investing in this Alliance Oil CompaEnergy 17.4% 0.8% 2 1 1 Magnit (GDR) Consumer 17.1% -0.2% 2 1 1 positioning and management quality, which in a list of companies would have generated over Cherkizovo Group Consumer 16.1% 1.2% 2 1 2 M-VIDEO Consumer 15.0% 1.4% 2 1 2 Russian context focus predominantly on 300% outperformance vs. the MSCI Russia since Rosneft Energy 13.9% 1.0% 2 1 2 ownership and corporate governance issues. January 2006. RUSSIA STRUCTURAL LEADERS WATCH LIST Russia at the intersection of global structural Russia Structural Leaders Watch List Company Sector dust y CROCI average 2011-13E, % CROCI change 2006-10, % quartile CROCI position quartile Management quality quartile trends Disclosure remains sub par in many Russian Uralkali Mining 38.3% 2.4% 1 1 3 Globaltrans Transport 20.3% 2.3% 1 1 3 Oil Serv & Pipe Russia’s economy and equity market are corporates and is the main reason why a number ChelPipe 18.0% -1.3% 2 1 3 producers undergoing a dramatic transformation through of companies that are forecast to generate Mail.ru Group Ltd. -

Factsheet: DWS Russia

Marketing Material Factsheet: DWS Russia Equity Funds - Emerging Markets August 2021 As at 31/08/2021 Fund Data Performance Investment Policy Performance - Share Class LC (in %) Equities of selected small, medium-sized and large Russian companies that we believe have a strong market position and good growth prospects; see the sales prospectus for details of the risks of focusing on a certain geographical area. Fund Benchmark* *Benchmark: MSCI Russia 10/40 (RI) ab 1.4.07 (vorher MSCI Russia Capped) Fund Management's Comment Calculation of performance is based on the time-weighted return and excludes front-end fees. Individual costs such as fees, commissions and other charges have not been included in this presentation and would have an adverse impact on returns if they were included. Past performance is not a reliable indicator of future returns. While Inflation surprised to the lower side lately, President Vladimir Putin announcement of two one-off payments to pensioners and military service personnel, which are to be Cumulative performance (in %) - share class LC dispensed in the coming quarters, are going 1 m 1 y 3 y 5 y s. Inception YTD 3 y avg 5 y avg 2017 2018 2019 2020 to slightly boost inflation and GDP at the same time, and are coming right ahead of the parliamentary elections. The majority of EUR 3.1 32.4 69.9 90.7 248.5 25.5 19.3 13.8 -10.0 -0.5 43.3 -6.7 Russian listed companies posted their BM IN EUR 2.0 31.5 64.6 89.5 531.0 23.3 18.1 13.6 -11.6 4.4 47.6 -11.2 earnings releases, resulting in positive sentiment on the market, and although an accident at a Gazprom facility was a short term headwind, the impact on production was considered limited.