Q2 2015 Fixed Income Release

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Medienmitteilung © 2020 Getty Images

Medienmitteilung © 2020 Getty Images Die Raiffeisen Super League ist zurück – erstmals auch in Schweizer Sportsbars Zürich, Mittwoch, 16. September Nach einer kurzen Sommerpause geht es bereits weiter: Der Ball rollt wieder auf den Schweizer Fussballplätzen! Teleclub zeigt alle Spiele der Raiffeisen Super League live. Und bietet ab sofort auch ein Angebot für Sportbarinhaber an. Die Saison startet mit dem Meister BSC Young Boys, der zu Hause im Wankdorf auf den FC Zürich trifft. Teleclub zeigt die Partie am Samstag, 19. September live und exklusiv. Bereits ab 18:15 Uhr senden Moderator Mevion Heim und die Teleclub Experten Rolf Fringer und Marcel Reif aus dem Studio, Kick-off ist um 19:00 Uhr. Auf diese Saison hin verstärkt der kürzlich zu- rückgetretene Fussballprofi Dennis Hediger das hochkarätige Expertenteam. Mit einer umfangreichen Berichterstattung rund um den Schweizer Fussball beweist Teleclub einmal mehr, das Zuhause des runden Leders zu sein. Auch in der Saison 2020/2021 sind alle Spiele der Raiffeisen Super League auf Teleclub zu sehen. Ebenso werden alle exklusiven Partien in Ultra High Definition (UHD) produziert. Auch in der Brack.ch Challenge League bleiben Fussballfans mit Teleclub am Ball: Der grösste Sportsender der Schweiz zeigt jeweils freitags ab 19:45 Uhr ein Live-Spiel im Free-TV auf Tele- club Zoom. Die zweithöchste Liga ist dank den beiden Absteigern Thun und Xamax sowie GC und Aarau so stark besetzt wie noch nie! Und bereits schon am Donnerstag, 17. September geht es für den FC Basel 1893 in der Quali- fikation zur UEFA Europa League weiter. Teleclub zeigt die Partie NK Osijek – FC Basel 1893 ab 20:30 Uhr live und exklusiv. -

Sky Deutschland AG | Geschäftsbericht 2012 Sky Deutschland AG | Geschäftsbericht 2012

Sky Deutschland AG | Geschäftsbericht 2012 Sky Deutschland AG | Geschäftsbericht 2012 Sky Deutschland AG | Geschäftsbericht 2012 Kennzahlenüberblick 2012 versus 2011 2012 2011 Veränderung (absolut) Veränderung (in %) Abonnenten Direkte Abonnenten1) zu Beginn (in Tsd.) 3.012 2.653 359 13,5% Bruttozugänge2) 728 671 57 8,4% Kündigungen3) –377 –312 –65 –20,9% Nettozugänge 351 359 –8 –2,4% Direkte Abonnenten zum Ende (in Tsd.) 3.363 3.012 351 11,6% Premium-HD-Abonnenten4) (in Tsd.) 1.514 974 540 55,5% Premium-HD-Penetration5) (in %) 45,0 32,3 12,7 – Sky+ Abonnenten6) (in Tsd.) 929 411 518 >100% Sky+ Penetration7) (in %) 27,6 13,6 14,0 – Programm-ARPU8) (in €, monatlich) 31,90 30,46 1,44 4,7% Kündigungsquote9) (in %, annualisiert) 11,8 11,0 0,8 – Kündigungsquote9) (in %, letzte 12 Monate rollierend) 11,8 11,0 0,8 – Finanzkennzahlen (in Mio. €) Umsatzerlöse 1.333,2 1.138,7 194,5 17,1% Operative Kosten 1.384,3 1.294,2 90,1 7,0% EBITDA –51,1 –155,5 104,4 67,1% Abschreibungen 72,3 56,1 16,2 28,8% Abschreibungen auf Abonnentenstamm 1,4 8,3 –6,9 –83,2% EBIT –124,8 –219,9 95,1 43,3% Finanzergebnis –65,4 –53,1 –12,3 –23,1% Steuern vom Einkommen und vom Ertrag –5,1 –4,6 –0,5 –10,6% Periodenergebnis –195,2 –277,6 82,4 29,7% 31.12.2012 31.12.2011 Veränderung (absolut) Veränderung (in %) Konzernbilanz (in Mio. €) Bilanzsumme 1.148,0 1.116,8 31,1 2,8% Eigenkapital 42,0 89,0 –47,0 –52,8% Netto-Finanzverbindlichkeiten 611,0 525,2 85,8 16,3% Mitarbeiter Ganztagskräfte 1.939 1.716 223 13,0% Kennzahlenüberblick Q4 2012 versus Q4 2011 Q4 2012 Q4 2011 Veränderung -

Stream Name Category Name Coronavirus (COVID-19) |EU| FRANCE TNTSAT ---TNT-SAT ---|EU| FRANCE TNTSAT TF1 SD |EU|

stream_name category_name Coronavirus (COVID-19) |EU| FRANCE TNTSAT ---------- TNT-SAT ---------- |EU| FRANCE TNTSAT TF1 SD |EU| FRANCE TNTSAT TF1 HD |EU| FRANCE TNTSAT TF1 FULL HD |EU| FRANCE TNTSAT TF1 FULL HD 1 |EU| FRANCE TNTSAT FRANCE 2 SD |EU| FRANCE TNTSAT FRANCE 2 HD |EU| FRANCE TNTSAT FRANCE 2 FULL HD |EU| FRANCE TNTSAT FRANCE 3 SD |EU| FRANCE TNTSAT FRANCE 3 HD |EU| FRANCE TNTSAT FRANCE 3 FULL HD |EU| FRANCE TNTSAT FRANCE 4 SD |EU| FRANCE TNTSAT FRANCE 4 HD |EU| FRANCE TNTSAT FRANCE 4 FULL HD |EU| FRANCE TNTSAT FRANCE 5 SD |EU| FRANCE TNTSAT FRANCE 5 HD |EU| FRANCE TNTSAT FRANCE 5 FULL HD |EU| FRANCE TNTSAT FRANCE O SD |EU| FRANCE TNTSAT FRANCE O HD |EU| FRANCE TNTSAT FRANCE O FULL HD |EU| FRANCE TNTSAT M6 SD |EU| FRANCE TNTSAT M6 HD |EU| FRANCE TNTSAT M6 FHD |EU| FRANCE TNTSAT PARIS PREMIERE |EU| FRANCE TNTSAT PARIS PREMIERE FULL HD |EU| FRANCE TNTSAT TMC SD |EU| FRANCE TNTSAT TMC HD |EU| FRANCE TNTSAT TMC FULL HD |EU| FRANCE TNTSAT TMC 1 FULL HD |EU| FRANCE TNTSAT 6TER SD |EU| FRANCE TNTSAT 6TER HD |EU| FRANCE TNTSAT 6TER FULL HD |EU| FRANCE TNTSAT CHERIE 25 SD |EU| FRANCE TNTSAT CHERIE 25 |EU| FRANCE TNTSAT CHERIE 25 FULL HD |EU| FRANCE TNTSAT ARTE SD |EU| FRANCE TNTSAT ARTE FR |EU| FRANCE TNTSAT RMC STORY |EU| FRANCE TNTSAT RMC STORY SD |EU| FRANCE TNTSAT ---------- Information ---------- |EU| FRANCE TNTSAT TV5 |EU| FRANCE TNTSAT TV5 MONDE FBS HD |EU| FRANCE TNTSAT CNEWS SD |EU| FRANCE TNTSAT CNEWS |EU| FRANCE TNTSAT CNEWS HD |EU| FRANCE TNTSAT France 24 |EU| FRANCE TNTSAT FRANCE INFO SD |EU| FRANCE TNTSAT FRANCE INFO HD -

No. Channel Logo Features Comeback HD App TV

Features No. Channel Logo TV start TV comfort ComeBack HD App 1 SRF 1 HD 2 SRF zwei HD 3 Das Erste HD 4 ZDF HD 5 SAT.1 HD 6 ProSieben HD 7 RTL HD 8 3+ HD 9 4+ HD 10 RTL II HD 11 VOX HD 12 5+ HD 13 kabel eins HD 14 sixx HD 15 TV24 HD 16 S1 HD 17 ORF 1 HD 18 ORF 2 HD 19 ARTE HD 20 SRF info HD 21 TeleZüri 22 Nickelodeon CH HD 23 SUPER RTL HD 24 ServusTV HD 25 MTV CH HD 26 VIVA CH HD 27 RTL NITRO HD 28 Puls 8 HD 29 TV25 HD 30 ntv CH HD 31 Eurosport HD 33 Discovery Channel HD 34 Animal Planet HD 35 HISTORY HD 36 TNT Serie HD 37 TNT Film HD 38 AXN HD 39 MTV LIVE HD 40 FashionTV HD ftv 41 CHTV HD 42 3sat HD 43 KiKA HD 44 NDR HD 45 WDR Fernsehen HD 46 SWR HD 47 BR HD 48 ZDF Neo HD 49 ZDFinfo HD 50 PHOENIX HD 51 ANIXE HD 52 DMAX 53 TLC 54 ProSieben MAXX CH 55 SAT.1 Gold 56 TELE 5 57 gotv 58 DELUXE MUSIC 59 Schweiz 5 60 STAR TV HD 61 wetter.tv 62 Eurosport 63 SPORT1 64 Disney Channel 65 NATIONAL GEOGRAPHIC CHANNEL 66 TNT Serie 67 TNT Film 68 hr-fernsehen 69 MDR FERNSEHEN 70 rbb Fernsehen 71 ARD-alpha 72 tagesschau24 73 Einsfestival 74 N24 75 euronews 76 Deutsche Welle 77 Bloomberg TV 78 Bibel TV 79 HSE24 80 Teleclub Zoom 81 RTS Deux HD Features No. -

The History of the Development of British Satellite Broadcasting Policy, 1977-1992

THE HISTORY OF THE DEVELOPMENT OF BRITISH SATELLITE BROADCASTING POLICY, 1977-1992 Windsor John Holden —......., Submitted in accordance with the requirements for the degree of PhD University of Leeds, Institute of Communications Studies July, 1998 The candidate confirms that the work submitted is his own and that appropriate credit has been given where reference has been made to the work of others ABSTRACT This thesis traces the development of British satellite broadcasting policy, from the early proposals drawn up by the Home Office following the UK's allocation of five direct broadcast by satellite (DBS) frequencies at the 1977 World Administrative Radio Conference (WARC), through the successive, abortive DBS initiatives of the BBC and the "Club of 21", to the short-lived service provided by British Satellite Broadcasting (BSB). It also details at length the history of Sky Television, an organisation that operated beyond the parameters of existing legislation, which successfully competed (and merged) with BSB, and which shaped the way in which policy was developed. It contends that throughout the 1980s satellite broadcasting policy ceased to drive and became driven, and that the failure of policy-making in this time can be ascribed to conflict on ideological, governmental and organisational levels. Finally, it considers the impact that satellite broadcasting has had upon the British broadcasting structure as a whole. 1 TABLE OF CONTENTS Abstract i Contents ii Acknowledgements 1 INTRODUCTION 3 British broadcasting policy - a brief history -

SVOD Digest: Table of Contents

SVOD Digest: Table of Contents Published in November 2017, the SVOD Digest report provides succinct state-of-play detail for 337 SVOD platforms across 50 countries. Price: £500/€600/$650 The 54-page report saves time for busy executives by presenting tabular information with one-page per country (OK – India and the US are two pages). Not every platform is listed – just the main ones in each country. We have concentrated on platforms providing TV episodes and movies – so not sports, for example. Our subscriber estimates only include paying subscribers at end-2017 – not trialists or those receiving free access. SVOD Digest platforms covered by country Country No of Platforms covered platforms Argentina 9 Netflix; Amazon Prime Video; Blim; Claro Video; Telefonica On Video; Arnet Play; HBO; Crackle; Qubit Australia 6 Netflix; Amazon Prime Video; Stan; Foxtel Play; YouTube Red; Hayu Austria 10 Netflix; Amazon Prime Video; Amazon Channels; Sky Ticket; Maxdome; A1 Now; TV Now Plus; Flimmit; Rakuten; 3TV Belgium 7 Netflix; Amazon Prime Video; Videoland; Yelo; RTL a l'Infiniti; Movies & Series; Be TV Brazil 6 Netflix; Amazon Prime Video; Claro Video; Globo Play; HBO; Crackle Bulgaria 4 Netflix; Amazon Prime Video; Voyo; Maxi Canada 5 Netflix; Amazon Prime Video; CraveTV; Illico; Fibe Alt TV Chile 8 Netflix; Amazon Prime Video; Blim; Claro Video; Movistar Play; HBO; Crackle; Qubit China 5 Youku Tudou; Iqiyi; Tencent Video; TMall Box Office; LeEco Colombia 8 Netflix; Amazon Prime Video; Blim; Claro Video; Movistar Play; HBO; Crackle; Qubit SVOD -

CSA FICHES CHAINES.Pdf

89, avenue Charles de Gaulle 92 575 Neuilly-sur-Seine Tél/Fax : 01 41 92 66 66 www.6ter.fr 6ter Société éditrice : Groupe Métropole Télévision SA Convention CSA : oui Forme juridique : S.A. à directoire et conseil Lancement de la chaîne : 12/12/2012 Capital : 39 000 € THEMATIQUE Généraliste PUBLIC VISE Famille / 25 – 49 ans, mixte PROGRAMMES PHARES Norbert commis d’office ; Départ immédiat ; cinéma ; séries. ACTIONNAIRE(S) M6 100 % ORGANIGRAMME Président Thomas VALENTIN Directrice générale Catherine SCHOFER Directeur de la communication Guillaume TURIN Directrice de la programmation Charlotte GALICE Responsable de l’antenne Karen KAbALO Responsable des productions Stéphanie SARTEL Responsable de la communication Valérie bOURDERIOUX Chargée de communication Carole GUINAND RESEAUX DE DIFFUSION / Disponible sur la TNT gratuite, le câble, le satellite, l’ADSL, les PC, tablettes et les mobiles. DISTRIBUTION DIFFUSION DANS LES DOM/TOM OUI DIFFUSION HORS DE FRANCE Suisse REDIFFUSION VIA MOBILE TABLETTE et PC UNE APPLICATION SUR : 6play 6play SERVICE DE TELEVISION TELEVISEUR INTERNET DE RATTRAPAGE 6play www.6play.fr RESEAUX SOCIAUX FACEBOOK TWITTER www.facebook.com/6ter @6terofficiel REGIE PUBLICITAIRE M6 Publicité Frédérique REFALO [email protected] 01 41 92 26 48 FICHES CHAÎNES - 102 42-44, rue Washington – Immeuble Monceau 75 408 Paris cedex 08 Tél/Fax : 01 70 60 79 00 www.13emerue.fr ème 13 RUE Société éditrice : NBC Universal Global Networks France S.A.S. Convention CSA : oui Lancement de la chaîne : 13/11/1997 Forme juridique : S.A.S. Effectif : 35 Capital : 225 000 € THEMATIQUE Fiction PUBLIC VISE Tout public PROGRAMMES PHARES Le meilleur des séries thriller et policières : Chance, Shooter, Lucifer, Loch Ness, Chicago Justice, Chicago Fire, Modus, Un chef en prison, Caméléon, etc ACTIONNAIRE(S) Universal Studios International b.V. -

Manufacturer's Code List Liste Des Codes De Fabricant Liste Der

4-170-687-11(1) English TV Brand Code No. Brand Code No. Brand Code No. Brand Code No. Brand Code No. City 00009 Grandin 00009, 00037, 00218, 00374, 00455, 01583, 00610, Marquant 02056 Profex 00009 Tatung 00037, 00072, 00516, 01248, 01324, 01556, 01720 The following tables show brand names (Brand) Téléviseur Clarivox 00037, 00070, 00418 00451, 00668, 00714, 00715, 00865, 00880, 01037, Mascom 01556 Profi 00009 TCL 01916 Code Fernsehgerät Classic 01308 01298 Mastec 01997 Profilo 01556 TCM 00714, 00808, 01289, 01308, 20001 and their corresponding code numbers ( Clatronic 00009, 00037, 00218, 00264, 00370, 00371, 00714, Grundig 00009, 00036, 00037, 00070, 00195, 00487, 01583, Master’s 01308 Profitronic 00037 Teac 00009, 00037, 00170, 01727, 00264, 00412, 00418, Tv 01324 00411, 00672, 01223, 01248, 01308, 01376, 01149, 00455, 00587, 00451, 00668, 00698, 00712, 00714, No.). 01869, 01916, 01935, 02007, 01531, 01037, 01687, Masuda 00009, 00037, 00218, 00264, 00371 Proline 00037, 00072, 00411, 00625, 00634, 01037, 01376, Clayton 01037 Materin 00858 01545, 01727, 02135 01037, 01149, 01363, 01687, 01755, 01812, 01985, Televisor 02200, 02239 02032, 02168 To set the manufacturer’s code, refer to the CME 01308 Grunkel 01149 Matsui 00009, 00035, 00036, 00037, 00072, 00195, 00208, Prosonic 00037, 00370, 00371, 00374, 00668, 00714, 01324, Televisor 01376, 01531, 01732, 01770, 01847, 01727, 02001, Tec 00009, 00037, 00335 Concorde 00009 GVA 01363 00235, 00335, 00355, 00371, 00455, 00487, 00516, Operating Instructions. 01583, 00714, 00744, 00880, 01037, -

|Fr|Hd| France ##### |Fr| Flix

##### |FR|HD| FRANCE ##### |FR| RTS UN HD |FR| CORONA VIRUS INFO |FR| RTS DEUX HD |FR| TF1 HD |FR| CSTAR HD |FR| FRANCE 2 HD |FR| LA CHAINE METEO HD |FR| FRANCE 3 HD |FR| MEZZO FR |FR| FRANCE 4 HD |FR| MUSEUM HD |FR| FRANCE 5 HD |FR| COMEDIE HD |FR| FRANCE 3 NOA HD |FR| COMEDY CENTRAL HD |FR| 6TER HD |FR| VIAGRANDPARIS |FR| M6 HD |FR| CANAL 31 |FR| TF1 SERIES FILMS HD |FR| CANAL 8 HD |FR| TFX HD |FR| CLIQUE TV HD |FR| RTL 9 HD |FR| EQUIPE 21 HD |FR| TEVA HD |FR| IDF 1 |FR| TMC HD |FR| OLYMPIA HD |FR| W9 HD |FR| KTO |FR| ARTE HD |FR| BOOSTER TV HD |FR| NON STOP PEOPLE HD |FR| LEMAN BLEU HD |FR| NOVELAS TV HD |FR| CANAL 9 HD |FR| ONE TV HD |FR| THE SWIZZ HD |FR| ROUGE TV HD |FR| OLTV ##### |FR|HD| CH. CANAL+ ##### |FR| FLIX MOVIES HISTORIQUE HD |FR| CANAL+ HD |FR| FLIX MOVIES DOCUMENTAIRE |FR| CANAL+ SPORT HD |FR| FLIX MOVIES ANIMATION HD |FR| CANAL+ PREMIER LEAGUE HD |FR| FLIX MOVIES JASON STATHAM |FR| CANAL+ SERIE HD |FR| FLIX MOVIES ANGELINA JOLIE |FR| CANAL+ FAMILY HD |FR| FLIX MOVIES TOM CRUISE |FR| CANAL+ DECALE HD |FR| FLIX MOVIES MORGAN FREEMAN |FR| CANAL+ CINEMA HD |FR| FLIX MOVIES JACKIE CHAN |FR| CANAL+ FORMULE1 HD |FR| FLIX MOVIES VAN DAMME |FR| CANAL+ MOTOGP HD |FR| FLIX MOVIES JOHN TRAVOLTA |FR| CANAL+ TOP14 HD |FR| FLIX MOVIES NICOLAS CAGE ##### |FR|HD| CINEMA ##### |FR| FLIX MOVIES MEL GIBSON |FR| FLIX MOVIES HD |FR| FLIX MOVIES ROBERT DE NIRO |FR| FLIX MOVIES ACTION HD |FR| FLIX MOVIES JIM CARREY |FR| FLIX MOVIES DRAMA HD |FR| ACTION HD |FR| FLIX MOVIES ROMANCE HD |FR| OCS MAX HD |FR| FLIX MOVIES COMEDY |FR| OCS CITY HD -

Client-Facing Slide Templates

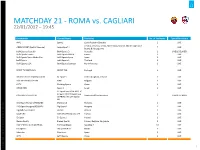

MATCHDAY 21 - ROMA vs. CAGLIARI 22/01/2017 – 19:45 Broadcaster Channel Name Territories No. of Territories Type of Broadcast AMC Sport1 Czech Republic/Slovakia 2 LIVE Croatia, Slovenia, Serbia, Macedonia, Kosovo, Montenegro and ARENA SPORT (Serbia Telecom) Arena Sport 4 7 LIVE Bosnia & Herzegovina beIN Sports Australia BeIN Sports 3 Australia 1 LIVE & DELAYED BeIN Sports France beIN Sports MAX 6 France 1 LIVE BeIN Sports Spain Media Pro beIN Sports Spain Spain 1 LIVE beIN Sports beIN Sports 1 Thailand 1 LIVE BeIN Sports USA BeIN Sports Connect North America 2 LIVE SPORT TV PORTUGAL SPORT.TV3 Portugal 1 LIVE BRITISH TELECOMMUNICATION BT Sport 3 United Kingdom, Ireland 2 LIVE BTV MEDIA GROUP EAD RING Bulgaria 1 LIVE CCTV Molding Sports China 1 LIVE CHARLTON Sport 2 Israel 1 LIVE TC Sport Live 04 DE HD / TC Linear 3 HD / TC Sport Live CINETRADE/TELECLUB Switzerland/Liechtenstein 2 LIVE & DELAYED 03 FR HD / TC 174 Sports HD DIGI Sport Hungary/RCS&RDS DigiSport 2 Romania 1 LIVE DIGI Sport Hungary/RCS&RDS DigiSport 1 Hungary 1 LIVE DigitAlb/SuperSport SS2HD Albania 1 LIVE DIGITURK beIN SPORTS HD 4 & OTT Turkey 1 LIVE Eir Sport Eir Sport 1 Ireland 1 LIVE Eleven Sports Eleven Sports Poland, Belgium, Singapore 3 LIVE FOX SPORTS LATIN AMERICA ESPN Caribbean See Slide 4 54 LIVE GO Sports GO Sports HD1 Malta 1 LIVE Movistar Movistar+ Spain 1 LIVE LETV LeTV Sports China 1 LIVE 2 Copyright ©2016 The Nielsen Company. Confidential proprietary. Nielsen and Confidential The Company. Copyright ©2016 MATCHDAY 21 - ROMA vs. -

Universal Remote Control and Get Support at SRU 5130/86

Register your product Universal remote control and get support at www.philips.com/welcome SRU 5130/86 EN Remote control 3 FR Télécommande 13 DE Fernbedienung 23 NL Afstandsbediening 33 DK Fjernbetjeningen 43 SV Fjärrkontrollen 53 NO Fjernkontrollen 63 FI Kaukosäätimen 73 2 Table of contents 1 Your universal remote control 3 ENGLISH 2 Installing the remote control 3-6 2.1 Inserting the batteries 3 2.2 Testing the remote control 4 2.3 Setting the remote control 4-6 3 Keys and functions 7-8 4 Extra possibilities 8-9 4.1 Adjusting device selection (Mode keys) 8-9 4.2 Restoring the original remote control settings 9 5 Frequently asked questions 10 6 Need help? 11 Code list of all brands / equipment 80-93 Information to the Consumer 97 1 Your universal remote control Congratulations on your purchase and welcome to Philips. To fully benefit from the support that Philips offers, register your product at www:philips.com/welcome. For quick, clean and easy setup go to: www.philips.com/urc After installing the universal remote control SRU 5130 you can operate a maximum of 3 different devices with it: TV, Set Top Box (satellite or cable decoder, digital terrestrial television), DVD player/HDD/recorder or VCR. 2 Installing the remote control 2.1 Inserting the batteries 1 Press the cover inwards and slide it in the direction of the arrow. 1 1 2 Place two AAA type batteries into the battery compartment, as shown. 3 Replace the cover and click it firmly into place. Installing the remote control 3 2.2 Testing the remote control ENGLISH The remote control has been programmed to operate most Philips devices. -

Client-Facing Slide Templates

MP & SILVA PRE-BROADCASTING SCHEDULE MATCHDAY 28 - GENOA VS. SAMPDORIA Expertise by Nielsen Sports Your contact person: Richard Mangan MATCHDAY 28 - GENOA vs. SAMPDORIA 11/03/2017 – 19:45 Broadcaster Channel Name Territories No. of Territories Type of Broadcast AMC Sport2 Czech Republic/Slovakia 2 LIVE & DELAYED Croatia, Slovenia, Serbia, Macedonia, Kosovo, Montenegro and ARENA SPORT (Serbia Telecom) Arena Sport 4 7 LIVE Bosnia & Herzegovina beIN Sports Australia BeIN Sports 1 Australia 1 LIVE & DELAYED beIN Sports beIN Sports 1 HD Hong Kong 1 LIVE & DELAYED BeIN Sports Spain Media Pro beIN Sports Spain Spain 1 LIVE beIN Sports BeIN Sports 4 Thailand 1 LIVE BeIN Sports USA BeIN Sports Connect North America 2 LIVE & DELAYED SPORT TV SPORT.TV3 Portugal 1 LIVE BRITISH TELECOMMUNICATION BT Sport 3 United Kingdom, Ireland 2 LIVE & DELAYED BTV MEDIA GROUP EAD RING Bulgaria 1 LIVE & DELAYED CHARLTON Sport 1 Israel 1 DELAYED TC Sport Live 25 DE HD / TC CINETRADE/TELECLUB Switzerland/Liechtenstein 2 LIVE & DELAYED Sport Live 13 FR HD DIGI Sport Hungary/RCS&RDS DigiSport 1 Hungary 1 LIVE & DELAYED DigitAlb SS2HD Albania 1 LIVE DIGITURK beIN SPORTS HD 2 & OTT Turkey 1 LIVE Eir Sport Eir Sport 1 Ireland 1 DELAYED Eleven Sports Eleven Poland 1 LIVE & DELAYED Argentina, Bolivia, Chile, Colombia, Ecuador, Panama, Paraguay Peru FOX SPORTS LATIN AMERICA Fox Sports 2 Cono Sur 9 LIVE & DELAYED & Uruguay GO Sports GO Sports HD1 Malta 1 LIVE Movistar Movistar + Spain 1 LIVE LETV LeTV China 1 LIVE 2 Copyright ©2016 The Nielsen Company. Confidential proprietary. Nielsen and Confidential Company.The Copyright ©2016 MATCHDAY 28 - GENOA vs.